Markets

The major world stock benchmarks (with the exception of Topix) ended lower for the holiday-shortened week. Amid modest trading volumes large-cap indexes were hit early in the week by concerns that the pick up in the US economy would induce the Fed to raise interest rates sooner than expected and the usual hysteria over the Greek bail out. The Nasdaq endured a smaller loss, helped by news of a significant merger in the semiconductor industry. Adding to investor uncertainty, several major economies — including US, Canada and Switzerland — reported contraction in Q1. Regional markets were mostly down or modestly up (Oman, KSA and Morocco) faring much better than the emerging markets. The 10-year US Treasury yield slipped back to 2.11%, and the 10-year German bund yield fell to 0.5%. The US dollar gained ground on major crosses while the yen fell sharply. The price of Brent and WTI held up, but the gold price dropped significantly despite bad economic news.

Global Developments

US/Americas:

- Real GDP in the US fell 0.7% qoq ann in Q1, according to the second estimate, compared to 2.2% in Q4 2014 and an advance estimate of 0.2%. Lackluster exports and destocking were the main causes of the dismal performance. The lack of performance will likely delay any Fed tightening and any raising of interest rates.

- New orders for durable goods fell -0.5% in April. Weakness was concentrated in transport goods mainly nondefense aircraft orders. Orders excluding transportation rose 0.5% and orders excluding defense added 0.2%.

- Existing-home price inched up 5% in Q1, similar to the three months ending Feb. The 10-city composite index was up 4.7% yoy, while the 20-city index is up by 5% yoy. Seasonally adjusted the 10-city and 20-city index were up 0.9%mom and 1% mom respectively. New-home sales surprised upside by 6.8% mom and by 26.1% yoy.

- The Conference Board Consumer Confidence Index rose by a modest 1.1 points in May to 95.4 from a downwardly revised 94.3 in Apr.

- Initial claims for unemployment insurance benefits rose from 275,000 to 282,000. The four-week moving average rose by 5,000 to 271,500.

Europe:

- ECB vice president Vitor Constancio said: “the European Central Bank’s monetary policy, aimed at raising inflation in the euro zone area, is working according to plan”.

- The Eurozone’s M3 money supply grew 5.3% yoy in Apr, following a 4.6% increase in Mar.

- The Eurozone’s economic sentiment indicator remained unchanged at 103.8 in May, near its long-term high reached in Apr. The Conference Board Leading Economic Index for the Eurozone rose to 105.9 in Apr from 105.4 in Mar.

- U.K. GDP grew 0.3% qoq in Q1 following a 0.6% expansion in Q4, while Spain’s GDP climbed 2.7% yoy in Q1, the largest increase in seven years, following a 2% yoy rise in Q4.

- Spain’s PPI fell -1% yoy in Apr, following a revised -1.3% decrease in Mar driven by the energy and intermediate goods prices, French PPI also fell -2% yoy in Apr, following a revised -2.2% decrease in Mar driven by weaker prices of energy and intermediate goods and Italy’s PPI fell -2.3% yoy in Apr, following a -2.4% decline in Mar.

- The U.K. GfK consumer confidence index fell in May to 1 from 4 in Apr and France’s consumer confidence index dipped to 93 in May from 94 in Apr.

- French household consumption rose 0.1% mom in Apr, following a -0.7% decline in Mar.

- Spanish retail sales climbed 2.5% yoy, following a 3.8% rise in Mar driven by lower nonfood sales.

- Business confidence in Russian manufacturing remained in negative territory in May, with the Rosstat confidence indicator at -6, a 1-point deterioration from Apr.

Asia and Pacific:

- Japan’s consumer price index experienced a slight 0.3% yoy increase in Apr, much below Mar’s 2.2% gain, indicating a loss in inflation momentum, far below Bank of Japan’s 2% target.

- Japan’s housing starts rose 0.5% yoy in Apr. on track with Mar’s 0.7% rise. Starts are stabilizing on yearly basis after yearlong misfortunes in 2014. Japan’s industrial production rose 1% mom in Apr. reversing two consecutive falls in Mar. (0.8%) and Feb. (3.1%).

- Japan’s retail sales exceeded expectations rising 5% yoy in Apr. after Mar’s 9.7% slump and consecutive falls in Jan. and Feb. Yet, falling oil prices, static wage growth, volatility and high tax are keeping spending down.

- India’s Q1 GDP recorded an expansion rate of 7.5% yoy, after a revised 6.6% the previous quarter, putting India ahead of China growth-wise. However, considerable uncertainties arise from the switch to the new GDP series.

- Singapore’s industrial production fell -8.7% yoy in Apr, following a -5.5% drop in Mar. The decline was driven by a dramatic drop in pharmaceutical exports.

- Philippines GDP growth surprised on the downside at 5.2% in Q1 (vs. expectations of 6.6%), the slowest pace since Q4 2011.

- Thailand’s private consumption fell -0.2% yoy in Apr, down from a revised 1% rise in Mar. Massive household debts still weighing on consumers purchasing activities.

- Thailand’s industrial production continues to fall reaching -5.3% yoy in Apr. from -1.8% in Mar. Rate cuts announced earlier this month seem insufficient as manufacturing sectors continue to struggle.

Bottom line: The GDP contraction in the US is another blow to the hopes of a quick pick up in the global economy. Even in emerging markets patches of weakness are emerging (Philippines and Singapore) which do not bode well for the first half of the year. A catalyst for growth is not in sight and the weak start of 2015 might extend to the rest of the year. The mood in stock markets reflects such more somber outlook.

Regional Developments

- Bahrain will begin reducing subsidies to cope with the pressure from lower oil prices, according to the Minister of State for Information Affairs. He also stated that citizens of the country would be provided cash subsidies to offset price rises when the subsidies are removed.

- Egypt’s bourse is changing rules and will reduce the free float required for new companies to list on its benchmark EGX30 from Aug 1 – to a minimum 5% free float as long as the market value of the float is at least EGP 100mn, from the 15% currently.

- The IMF criticized Egypt’s decision to postpone implementation of the capital gains tax, stating that this “will mean that more of the cost of reducing the budget deficit will now be paid by people who are less able to afford it”.

- The Islamic Development Bank (IDB) revealed that its funding portfolio for Egypt reached USD 12.5bn, with a USD 3.1bn increase in 2014 alone.

- Egypt’s Investment Minister revealed that free zones accounted for 25% of the country’s export volume (USD 8.2bn annually) and that total invested capital in the free zones reached USD 10bn recently.

- Jordan’s Planning Ministry launched a new solar power project last week and this is expected to reduce its annual electricity bill by 20%. According to official figures, the ministry’s electricity bill amounted to JOD 137k in 2014, when it consumed 586,967 kilowatt hours. Additionally, the Ministry also signed a MoU with the Japanese Embassy towards a soft loan of approximately USD 196mn.

- Lebanon’s central bank announced plans to establish an electronic exchange for startups: “preparations are underway to establish an electronic stock market that would allow startup companies to sell their shares to the public if they choose not to sell their businesses to other companies”, according to the governor. The central bank also launched a package worth over USD 1bn to encourage startups in Lebanon.

- Oman’s government revenues fell by 23.9% yoy to OMR 2,447.3mn in Q1 from OMR 3,214.4mn, predominantly due to a plunge in oil revenues.

- Oman’s conventional banks recorded in Q1 a 11.6% yoy growth in net loans and advances at OMR 17.41bn.

- Qatar trade surplus was down by a whopping 50% yoy to QAR 52.8bn in H1 2015, with total exports amounting to QAR 82.1bn (down 38% yoy and 21.2% qoq).

- The banking sector in Qatar saw a dip in loans and deposits in the month of Apr: banks’ loan book decreased by 0.5% mom and deposits dipped by 0.2% mom. Furthermore, the public sector pulled down total credit growth with a decline of 4.7% mom and down 5.9% year-to-date.

- Net foreign assets held by SAMA in Saudi Arabia dipped 1.7% mom and 6.8% yoy to SAR 2.546 trillion in Apr, recording the lowest level since May 2013.

- Saudi Arabia’s exports dropped by 8.9% to SAR 1.3trillion last year, while imports were up by 3.3% to SAR 651.9bn. As for top trade partners, US accounted for 12.6% of total exports, followed by China (12.5%) and Japan (12.2%) while China accounted for the largest proportion of imports at 13.6%, closely followed by US (13%) and then Germany (7.2%).

- The Capital Market Authority (CMA) in Saudi Arabia stated that it would raise the proportion of shares allocated to institutional investors in initial public offers, in a bid to reduce market volatility. In a recent IPO of Saudi Company for Tools and Hardware, the CMA allocated 60% of shares to institutional investors and 40% to retail investors.

- Growing GCC economic integration: The Ministries of Commerce and Industry across the GCC nations are unifying 6 trade laws including a unified trade system, consumer protection law, commercial anti-cheat system, trademarks law, anti-dumping law, compensation measures and a competition system.

UAE Focus

- The UAE Banking Industry Association revealed that it had discussed the possibility of creating a centralised Sharia board to monitor Islamic banking, along the lines of the central bank’s recommendation to set up a Higher Sharia Authority intended to complement and oversee the work of Sharia boards at individual Islamic banks.

- Bank lending in the UAE was up 8.4% in Apr (Mar: 8.2%) while money supply (M3) fell to 6.4%, recording the slowest pace since Sep 2012.

- Net investment flow from foreign investors into the UAE touched AED 4bn in 2014, compared to AED 1.7bn net investment the year before. Additionally, foreign institutional investors on the Abu Dhabi Securities Exchange more than doubled to 791 in Sep 2014 (after the MSCI reclassification) over the previous year.

- Dubai, which has spent AED 80bn on infrastructure projects since 2005, has saved the economy an estimated AED 87bn in time and fuel terms, according to the Director General of RTA.

- Dubai World Trade Centre (DWTC) reported a 10% yoy increase in visitor arrivals to 2.45mn in 2014, and also a 16% growth in number of exhibitions and a 40% rise in number of association meetings and congresses held at the venue.

- Etihad Airways announced that the airline would be supporting the US economy with 23,400 jobs and contributing USD 2.9bn to GDP in 2015, and according to Oxford Economics estimates this would almost double to USD 6.2bn by 2020.

Media Review

Four Years After the Arab Spring: IMF

http://www.imf.org/external/pubs/ft/fandd/2015/06/mazarei.htm

Chinese Renminbi is no longer undervalued, says the IMF

http://www.ft.com/intl/cms/s/0/11e96e1e-03a7-11e5-b55e-00144feabdc0.html#axzz3bDlicxVq

Will Iraq oil flood the market?

http://www.bloomberg.com/news/articles/2015-05-26/iraq-about-to-flood-oil-market-in-new-front-of-opec-price-war

Some quick facts on China’s mountain of debt

http://marginalrevolution.com/marginalrevolution/2015/05/china-fact-of-the-day-28.html

The AIIB: a South-South development-finance landscape

http://www.project-syndicate.org/commentary/china-silk-road-fund-development-financing-by-richard-kozul-wright-and-daniel-poon-2015-05

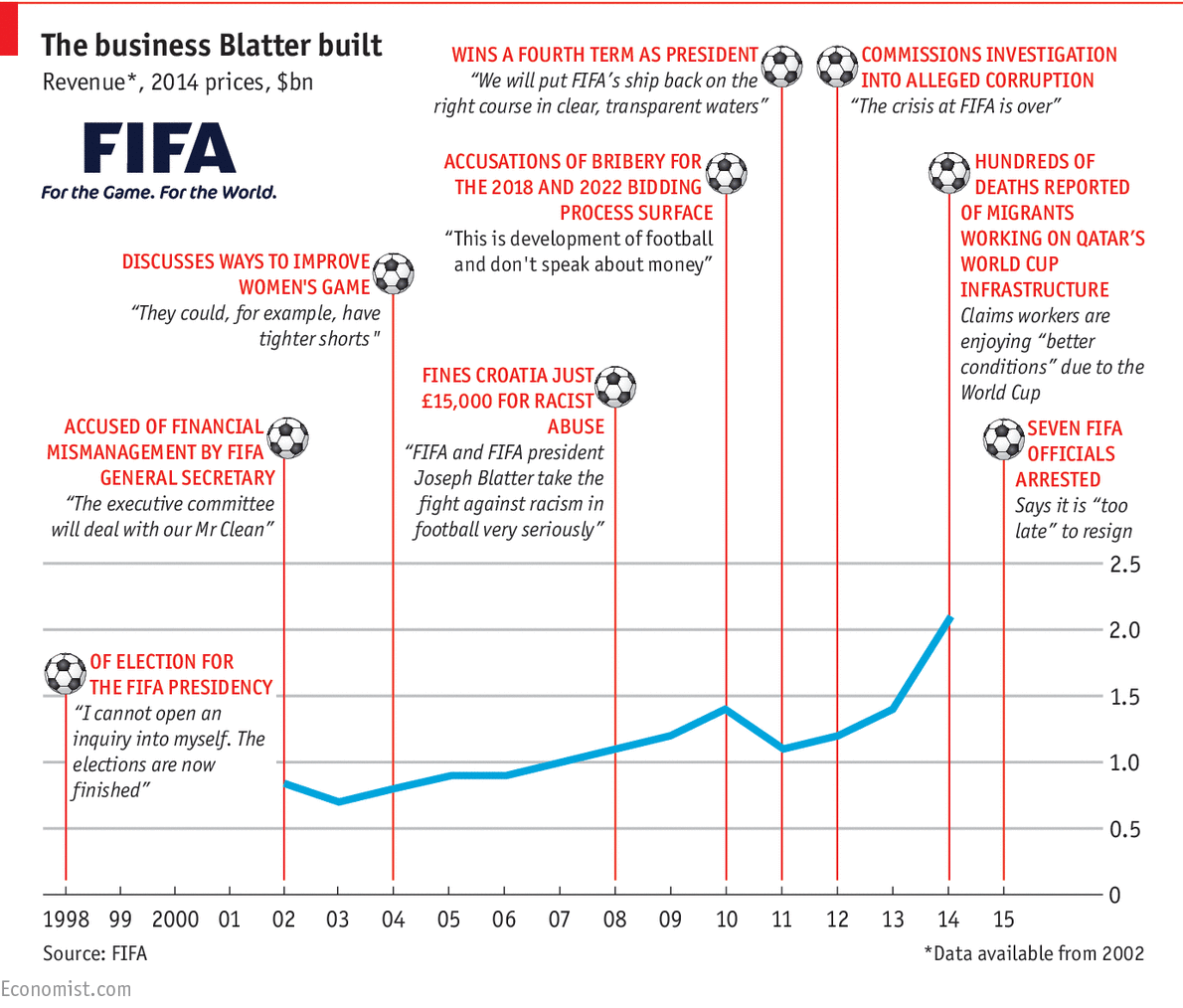

FIFA: The Business Blatter Built

http://cdn.static-economist.com/sites/default/files/imagecache/original-size/images/2015/05/blogs/game-theory/20150530_woc984_0.png

http://www.economist.com/blogs/gametheory/2015/05/sepp-blatters-fifa

{kind=link}