Download a PDF copy of the weekly economic commentary here.

Markets

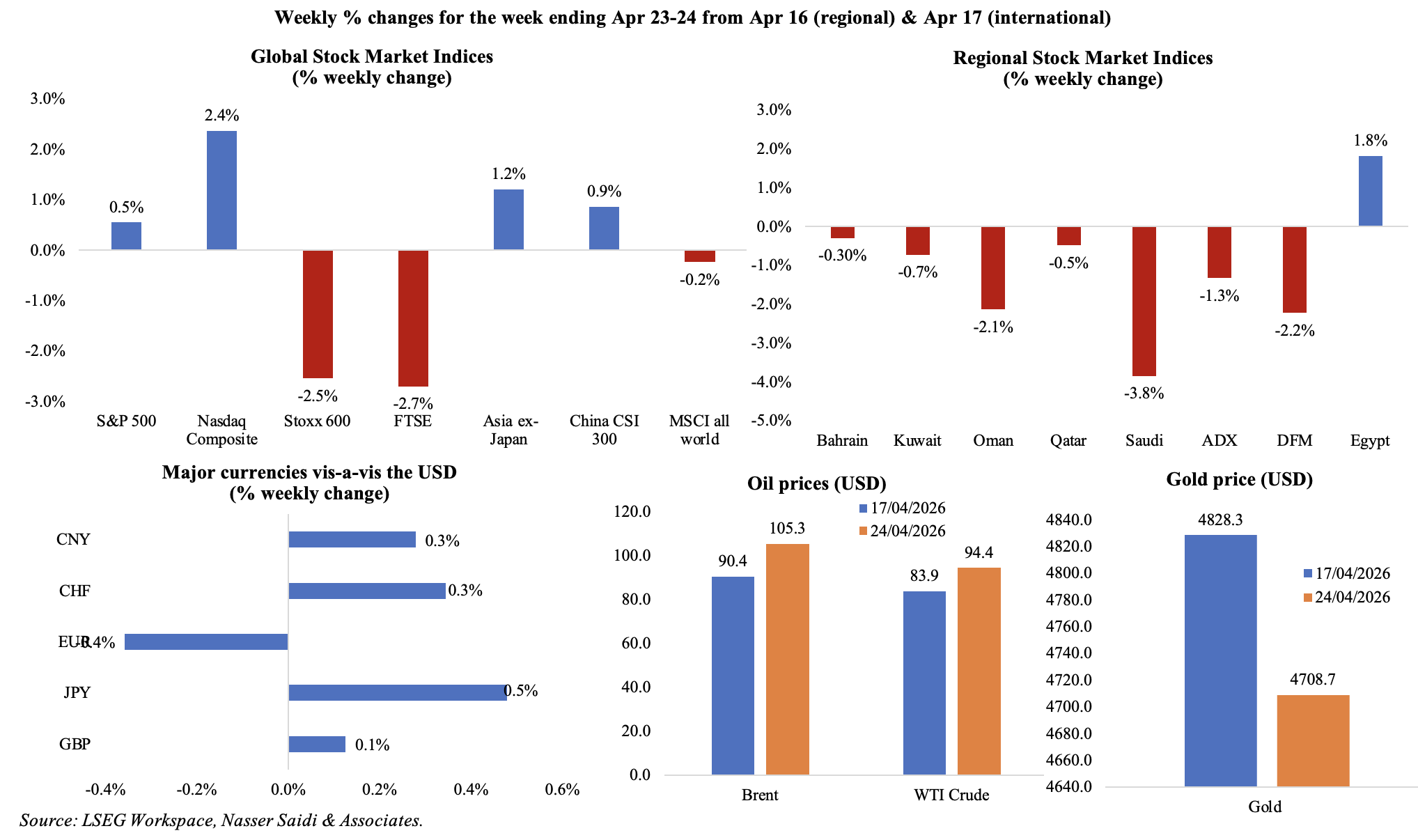

Global markets continue to navigate a volatile landscape amid on-and-off diplomatic efforts in Pakistan. US equities markets closed on record-highs last Friday, while European stocks dropped to a two-week low, and Asian markets edged up slightly. Regional markets were mostly down, with only Egypt posting a gain; UAE’s DFM and ADX fell by 2.2% and 1.3% respectively. The US dollar remains the primary beneficiary of stalled US-Iran talks, maintaining its strength against a basket of major currencies as geopolitical uncertainty peaks. The Indian rupee’s valuation fell to over a decade low, bruised by sustained portfolio outflows and the rising cost of energy imports. Oil prices rose – Brent and WTI by 16% and 13% respectively – as military tensions escalated with no clear solution to the current impasse. Gold price seems to have lost its safe-haven shine, staying about 10% lower compared to pre-war levels.

Economic Consequences from the conflict in the Middle East & Policy Responses

The global economic landscape in late April 2026 continues to be defined by trade disruptions as the conflict with Iran continues to raise economic and trade policy uncertainty. While the OECD maintains that a full-scale risk of stagflation remains contained, the reality is becoming increasingly grim. The traffic through the Strait of Hormuz has been almost standstill for weeks; about five ships transited on the 24th of Apr and approximately 20,000 seafarers remain stranded there. This maritime blockade has triggered a 20% drop in global LNG supply, pushing worldwide oil inventories toward record lows and sparking warnings of a surge in global insolvencies as trade and energy costs become unsustainable.

For now, there is evidence of the economic fallout moving beyond energy, hitting Asia’s polyester suppliers and global fast-fashion retailers. The UN warns that the war is pushing more than 30 million people back into poverty. In Europe, the crisis is leading to a call for energy independence, reviving demand for rooftop solar as households and firms seek to insulate themselves rising energy prices.

The four major central banks are set to meet on policy this week, and all are widely expected to hold rates steady. However, the policy moves going forward will be dependent how quickly the current conflict in the Middle East can be resolved and the outlook for higher inflation rates. On the one hand, US Treasury Secretary Bessent confirmed that talks are ongoing with GCC and Asian partners to establish dollar swap lines to maintain liquidity while on the other, the US has also strategically blocked USD shipments to Iraq to squeeze Iran-backed militias, further weaponizing the global financial system. Separately, Bloomberg reported that a major US asset manager has extended USD 10bn in loans to Gulf investors since the onset of the conflict. This highlights that the region is undertaking a re-routing of capital toward private markets as public equity and bond premiums fluctuate while underscoring that institutional lenders remain bullish on the long-term resilience of the GCC.

For now, a diplomatic breakthrough has remained elusive. Despite the triple whammy of trade, energy and financial shocks, Goldman Sachs expects a potential rebound in Gulf oil output within a few months should the Strait reopen. Success in this period will be defined by the speed at which land-based corridors and multi-modal logistics can bypass maritime chokepoints and the ability of central banks to maintain liquidity and credit flows amid rising economic scarring.

Lastly, global military spending surged by 2.9% to almost USD 2.9trn in 2025, driven largely by the systemic instability in the Middle East and the Indo-Pacific; this figure represents 2.5% of the world’s GDP, the highest percentage since 2009, according to SIPRI. The global increase persists despite a dip in US spending in 2025, which was hampered by domestic political freezes over Ukraine aid. For Middle Eastern policymakers, this global trend underscores the recent pivot toward domestic defence autonomy, such as Abu Dhabi’s and Saudi Arabia’s planned investments in localized defense technologies.

Countervailing Regional Policies & Developments

- To bridge the fiscal gap created by the Strait of Hormuz blockade, Kuwait issued KWD 400mn (USD 1.3bn) in local bonds, split into two tranches carrying a 3% rate with two- and three-year maturities. The issuance was reportedly oversubscribed more than three times by local banks, reflecting abundant liquidity even as lower oil revenues and Hormuz disruption worsen the deficit outlook.

- Lebanon and Israel extended their ceasefire by three weeks after US hosted talks at the White House, even though deadly strikes and clashes continue to this day in southern Lebanon. The extension aimed to reduce immediate escalation risk, but durable progress will depend on whether the talks can move from temporary de-escalation to concrete steps on Israeli withdrawal, border rules and Hezbollah’s role.

- The conflict has lowered traffic at the Muscat International Airport: international passengers at Omani airports fell by 2.4% yoy to 2.86mn in Q1. In Mar, passenger arrivals stood at 728,588 from over 1.2mn in Jan 2026.

- Oil spillage from stranded tankers poses environmental threats to Oman’s coastline and could potentially harm the tourism industry. Currently about 30% of the more than 200 oil tankers stuck due to the Hormuz blockade are in the Gulf of Oman.

- Oman is inviting investments for 11 projects worth around OMR 96mn (nearly USD 250mn) across agriculture, fisheries and related industries – in a bid to fortify its domestic supply chain against global disruptions.

- QatarEnergy’s first tanker has arrived in Texas for the Golden Pass LNG project. QatarEnergy owns 70% of the project, so the story is about Qatar expanding its LNG reach via US export capacity even while its own regional assets face disruption.

- To shore up its forex reserves, Pakistan’s central bank received a second tranche of USD 1bn from Saudi Arabia as part of the latter’s USD 3bn support commitment, alongside the extension of an existing USD 5bn deposit (together this accounts for roughly half of Pakistan’s central bank reserves). The inflow is meant to shore up reserves after Pakistan repaid USD 1.4bn in Eurobonds and USD 2bn in loans to the UAE.

- The war has necessitated a refocusing of capital: notably, the New York’s Metropolitan Opera has lost up to USD 200mn in Saudi funding. Pre-war, the deal being discussed would have provided the Met with funding over eight years and required the opera to take up residency in the Royal Diriyah Opera House for three weeks in Feb. Officials reportedly cited war-related economic damage and a need to prioritize domestic spending programs.

- Saudi crude output fell 23% mom to 76mn barrels per day in March, but the fall was partly dampened by a 63%surge in Brent prices during then, according to Al Rajhi Capital.

- In a strong signal of confidence and message of continuity, UAE’s PM and Ruler of Dubai declared that work on major construction projects will not stop despite regional tensions. The pace of development is expected to accelerate given announcements of the AED 34bn Gold Line metro project and the AED 500mn Al Mamzar Beaches development among others.

- Emirates Global Aluminium (EGA) is set to acquire 80% of an Italian aluminum recycler Eco Green (handling more than 70k tonnes annually), enabling the EGA’s total recycling capacity to exceed 400k tonnes per year after completion. The strategic point is that EGA is expanding deeper into European scrap flows and secondary aluminium at a time when recycling is becoming a more important competitive advantage. This follows a similar hedging strategy by Bahrain’s Alba, prioritizing industrial footprint diversification.

- Inter-GCC Connectivity: The Oman-UAE rail network is now 40% complete, marking a critical step toward land-based logistics independence. It will connect Sohar Port free zone (in north-eastern Oman) to the UAE rail network and will include two 2.5km tunnels and 36 bridges. Simultaneously, Saudi Arabia and Jordan are advancing plans for a rail link to boost business and create a trade corridor that bypasses maritime chokepoints. This builds on existing strong links – Saudi Arabia is the largest foreign investor in Jordan, accounting for nearly 16% of total capital flows of around JOD 2.02bn (USD 2.8bn) in 2025.

- Regional Agricultural Partnerships:Qatar and Algeria have launched the second phase of a USD 3.5bn farm project, emphasizing a shift toward food-sovereignty investments. The project is intended to scale milk, fodder and meat production and eventually support a herd of 270,000 cattle (and produce 1.7bn litres of milk per year). Such trans-regional partnerships are increasing as policymakers move to prioritize food security.

- Foreign investors were net buyers of USD 1.47bn in GCC equities markets in Q1, reversing USD 313.5mn of net selling in Q4, according to Kamco Invest; Saudi Arabia led with USD 2.6bn in net buying. This suggests investors viewing the GCC as a good opportunity based on diversification efforts, capital market reforms and strong fiscal positions. However, the durability of inflows will depend on whether reform momentum can keep outweighing war-risk concerns.

Macroeconomic Developments in the MENA region

- Egypt has set a target of 5.4% GDP growth for FY 2026-27, with a goal of growth rising to 6.8% by 2030. The Minister of Planning and Economic Development stated that the plan prioritizes living standards, public services, productivity, and food & energy security, with five key sectors (manufacturing, trade, tourism, construction & agriculture) expected to drive roughly 64% of growth in 2026-27.

- Egypt’s next budget aims to reduce foreign debt by up to USD 2bn, relying on stronger public revenues (+30% from previous budget to EGP 4trn) from exports and government stakes sales, also signalling a rigorous commitment to fiscal discipline and debt sustainability. Spending stands at nearly EGP 5.1trn and deficit is estimated at 4.9% of GDP while borrowing will be lowered to around 10% of GDP. Debt servicing will be reduced to about 35% in the medium term, according to the finance minister.

- Egypt successfully raised approximately USD 6bn from 19 full and partial state-exit deals, revealed the PM. This represents 48% of its USD 12.2bn target under the offering program up to June 2025 and reflects a sustained appetite for strategic assets despite regional conflicts. The EGX is arranging for six temporary listings (with four headed to the main market and two to the SME market) and plans for several petroleum-sector IPOs to deepen capital markets and attract institutional inflows.

- The Egyptian Exchange reported that retail and Investor engagement has reached record levels, with a 200% surge in new investors to 164,230 during Q1 2026. By mid-April, the total number of new investors had climbed to 191,034 from 51,992 in Q1 2025.

- Egypt posted a significant rise in the financial inclusion rate to 77.6% in 2025, up from 27.4% in 2016, with 54.7 million people holding active transaction accounts (2016: 17.1mn). Financial inclusion among women and youth also jumped to 71.4% and 56.8% respectively. This expands the domestic liquidity pool, and such broader account ownership can support digital payments, savings mobilization and more inclusive credit growth over time.

- Egypt launched a three-month campaign to promote its investment zones. So far, a total 12 investment zones attracted EGP 66.3bn in investments and created more than 77,500 jobs.

- In a landmark development for regional stability, Libya approved its first unified budget of LYD 190bn (USD 29.95bn) in 13 years. This fiscal milestone coincides with the country hitting record oil output – 1.43mn barrels per day (bpd),the highest in more than a decade, with a target of 2mn bpd to reach by 2030. The rising oil & gas revenues will provide Libya with the means for national reconstruction and the restoration of institutional creditworthiness.

- To address peak summer demand and enhance regional energy security, Egypt plans to commission the first phase of the Egypt–Saudi electricity interconnection before end-Q2 2026. The project will have an initial capacity of 1500 MW and eventual capacity of 3000 MW. A successful implementation will strengthen the case for more regional grid integration.

- Strategic cross-border partnerships are maturing, evidenced by an Egypt-UAE consortium investing in a major tourism project in Morocco to diversify regional revenue streams. The EUR 200mn project includes 800 hotel rooms over five years, with the first phase targeting completion by end-2027.

- Syria plans to launch the Damascus Market for Foreign Exchange and Gold, a regulated electronic platform intended to unify price references, reduce distortions, improve transparency and support monetary policy and financial stability.

- Lebanon’s Central Administration of Statistics show significant downward revisions in GDP for 2024 and prior years. The ongoing security crisis will only exacerbate this structural decline. Revised statistics showed real GDP contracted by 5.2% yoy in 2024. Nominal GDP was revised to LBP 2,728trn (~USD 30.5bn at an exchange rate of LBP 89,500 to USD. GDP deflator rose sharply (27.4% in 2024), reflecting the ongoing decoupling between nominal prices & real output. Covid-affected 2020 was revised down to a 28.7% contraction (previous: -25.9%); 2021 and 2022 were lowered to 1.6% and 1.4% respectively.

Macroeconomic Developments in the GCC

- Bilateral trade between Bahrain and France surged by 77% yoy to USD 757.9mn in 2025, highlighting deepening economic ties with European partners.

- Inflation in Kuwait edged up to 2.06% yoy in Mar (Feb: 1.92%).

- UAE was Oman’s largest non-oil trading partner, with gains in direct non-oil exports (37.5% to OMR 258mn in Jan-Feb) & re-exports (1.7% to OMR 80mn). Re-exports to KSA surged 389.9% to OMR 55mn. Oman’s non-oil exports grew by 11.4% yoy to OMR 1.1bn in Jan-Feb, thanks to an acceleration in industrial sectors such as base metals. Merchandise exports saw a decline (-2.3% yoy to OMR 3.6bn in Jan-Feb 2026) due to a 9.0% drop in oil and gas exports; imports grew by 5.1%; trade surplus was a healthy at OMR 731mn ytd.

- FDI in Oman surged 8.1% yoy to OMR 31.4bn at end-2025. The most popular sectors that attracted FDI were oil & gas exploration (81% of total), manufacturing (8.5%), financial intermediation (4.8%) and real estate (1.9%) which together accounted for 96.1% of the total. Fastest growth was recorded in construction (11.1%) and oil & gas exploration (11.0%). UK topped the list of countries with investments in Oman (OMR 16.4bn, or 52.3% of the total; +10.5% yoy) followed by the US (OMR 8.5bn) and Kuwait (OMR 1.36bn).

- Oman’s Salalah Free Zone attracted a total of OMR 395mn in new private-sector investment (via 16 agreements) in 2025, raising total investment to OMR 5.52bn. The zone is likely to receive further investments given its trade activity through the Port of Salalah as an alternative to the Strait of Hormuz.

- Oman’s tourism consumption increased by 11.6% yoy to OMR 1.18bn (USD 3.06bn) in 2025, while direct tourism GDP grew 3.7% to OMR 1.14bn. Separately, hotel revenues hit a record OMR 297.3mn last year, up more than 22% yoy, helped by 2.4 million guests (+11% yoy), occupancy of nearly 57% (+13.6%) and higher room rates (+4.7% to OMR 49). Oman’s hospitality sector is expanding, with another 2,400 rooms expected to hit the markets this year.

- Saudi Arabia’s total merchandise exports increased modestly by 4.7% yoy to SAR 99.1bn in Feb 2026, with oil exports rising only 0.6%. The share of oil in total exports inched up to 68.7% in Feb. Non-oil exports rose strongly, increasing 15.1% year-on-year to SAR 31bn. Re-exports were a key component of non-oil exports: though it slipped 10.8% from Jan’s record high, it was up 28.5% yoy. China remained the top trade partner (largest export destination and import source) while UAE & India were also key export markets. UAE alone accounted for 31.6% of Saudi non-oil exports; share of non-oil exports to GCC was 40%. Jeddah Islamic Seaport and King Abdulaziz International Airport handled a combined 31.7% of non-oil exports in Feb.

- As a sign of market resilience, a Saudi IT company (Dar AlBalad for Business Solutions) is pursuing the first GCC IPO since the war began, with plans to float 21 million shares (equal to 30% of its capital) and book-building began this week. Additionally, bottled water company Berain Water Company was also given approval to list 66mn shares on the Saudi Exchange, with a timeline until October to proceed with the IPO.

- In a significant move for institutional liquidity, Saudi Arabia is set to join the JPMorgan Emerging Market Bond Index by early 2027, with Saudi expected to reach a 2.52% weight once fully phased in. Bloomberg will also include Saudi sukuk in its Emerging Market Local Currency Government Index with the end-Apr 2027 rebalancing. These moves expected to attract substantial passive capital index-linked inflows.

- Saudi Arabia’s Construction Cost Index rose 2.0% yoy in March, the highest annual gain, led by higher equipment rental and labour costs, with residential costs up 1.9% and non-residential costs up 2.2%. Equipment and machinery rental (+4.5%), labour (2.7%) and energy costs (3%) were the main drivers, which suggests project delivery is becoming incrementally more expensive even as some parts of the real estate market cool.

- Saudi Arabia’s real estate price index fell by 1.6% yoy in Q1 2026, mainly due to the fall ion residential segment (-3.6%, due to a 3.9% drop in residential land prices), alongside a rise in commercial prices (+3.4%). In effect, it shows a softer housing market alongside firmer demand in commercial property assets.

- Saudi Arabia awarded a second infrastructure contract for the Riyadh Expo 2030 site to Al Yamama Company and the scope includes internal roads and smart mobility systems; another local contractor was in Jan awarded the utilities and civil works contract at the site.

- Current sports-sector investment opportunities in Saudi Arabia amount to SAR 18bn (USD 5bn) and could rise to around SAR 85bn by 2030. A large part of the pipeline is tied to preparation for the 2034 FIFA World Cup, including at least 135 training camp sites and broader sports infrastructure.

- Saudi Arabia’s government accelerates emerging tech adoption. Saudi Arabia’s Digital Government Authority says 76.04% of 54 government entities are now prepared to adopt and activate emerging technologies, up from 74.69% (of 49 entities) in 2025.

- Saudi Arabia and Switzerland signed an agreement on the promotion and reciprocal protection of investments, focusing on technology transfer and financial services during the Swiss Confederation President’s visit. The pact is intended to stabilize the investment environment, protect investor rights and encourage two-way investment flows.

- The UAE approved a new government framework to deployAgentic AI, allowing the transformation of 50% of government sectors, services and operations within two years; ministers and entities will be assessed on how quickly and effectively they implement it. The UAE could hence set an early benchmark for AI-led public administration, way beyond just simple automation tasks.

- Dubai is significantly expanding its transit network with the AED 34bn (USD 9.3bn) “Gold Line” Metro project: the 42 km, 18-station project will be Dubai’s first fully underground metro line, passing through 15 strategic locations, connecting 55 major real estate developments that are under construction and serve over 1.5mn people. The line, due to open on 9 Sep 2032, will expand the metro network by 35% and generate a 430% cumulative economic return over 20 years.

- The UAE established a AED 1bn (USD 272mn) national fund to support the industrial sector. The National Industrial Resilience Fund will “strengthen resilience, expand local production, secure supply chains, and scale the use of artificial intelligence across production and operations”.

- Masdar continues its global expansion with new renewable projects in Montenegro in a 50-50 JV with Elektroprivreda Crne Gore (EPCG), Montenegro’s national power utility. While the size of investment was not disclosed, the project will support local energy needs and support the export of renewable power to the Western Balkans and Southern Europe.

- Bloomberg reported that Abu Dhabi is considering a merger of the China-based assets of L’imad and Mubadala to streamline strategic investments and avoid the emirate’s sovereign investors competing for the same deals.

- Saudi Arabia ranked first among high-income economies in entrepreneurial finance in the Global Entrepreneurship Monitor 2025–2026 report and placed third globally in the National Entrepreneurship Context Index. Also revealed was a sharp increase in early-stage entrepreneurial activity to 28.9% in 2025 (2018: 12.1%) and a doubling in entrepreneurial intentions to 48.5% (2018: 26.8%).

- A GCCStat report finds that 7.3mn women are now employed across the GCC, from 5.7mn in 2020, representing a fundamental shift in the regional labour market and consumer base. Female labour-force participation across the GCC rose to 39.3% in 2025, while female unemployment fell to 10.5% and female citizens accounted for 40.5% of total employed nationals. Gains are tied to diversification efforts in countries such as Saudi and the UAE.

Global Macroeconomic Developments

US/Americas:

- Retail sales in the US grew by 1.7% mom in Mar (Feb: 0.7%), largely due to the record 15.5% jump in gas station receipts (the largest on record). Higher fuel costs are likely to crowd out discretionary spending, with restaurants sales already looking soft (0.1% vs Feb’s 0.5% gain). In annual terms, overall sales grew by 4%.

- US pending home sales increased by 1.5% mom in Mar (Feb: 2.5%) and inventory levels remained tight. Pending sales were down 1.1% yoy, with an uptick in the average 30-year mortgage rate (6.38% at end-Mar vs 5.98% in end-Feb) making affordability a constraint.

- Chicago Fed national activity index fell to -0.2 in Mar (Feb: 0.03) with three of the four major categories deteriorating and production making the largest negative contribution; payrolls were still resilient. Kansas Fed manufacturing activity slipped to 10 in Apr (Mar: 11) as export orders eased, employment softened and prices paid index jumped to 63 from 37.

- S&P Global manufacturing PMI rose to 54 in Apr (Mar: 52.3), as production growth stood at a four-year high and new orders rose at the fastest pace since May 2022; part of the rise was due to longer supplier delivery times (some delays linked to Middle East war-related supply constraints); employment was the only component in contraction. Services PMI moved to expansionary territory, from 51.3 (From 49.8).

- The Michigan consumer sentiment index fell to a record low of 49.8 in Apr (Mar: 53.3) while expectations were up to 48.1 (from 51.7). The one- and five-year consumer inflation expectations stood at 4.7% (from 3.8%) and 3.5% (from 3.2%). This is directly linked to fuel and broader price pressures from the Hormuz blockade, even after the ceasefire was extended.

- Initial jobless claims increased by 6k to 214k in the week ended Apr 18, with the 4-week average edging up to 210.75k (from 210k) while continuing jobless claims rose by 12k to 1.821mn in the week ending Apr 11.

Europe:

- Germany’s flash manufacturing PMI declined to 51.2 in Apr (Mar: 52.2) as both output and new orders decelerated on rising geopolitical uncertainty. In contrast, eurozone’s manufacturing PMI rose to 52.2 (from 51.6) on stronger production (fastest since Aug 2025) and export orders (the first rise since Feb 2022. The preliminary manufacturing PMI in the UK also increased to 53.6 in Apr (Mar: 51.0), as production rebounded, new orders were higher and employment rose for the first time since Oct 2024. Inflationary pressures were rising across the board due to the conflict in the Middle East.

- The ZEW Economic Sentiment Index in Germany continued to fall in Apr: to -17.2 (Mar: -0.5) while the current situation also slipped (-73.7 from -62.9). The eurozone’s Economic Sentiment Index also declined to -20.4 (Mar: -8.5).

- Consumer confidence in the eurozone plunged to -20.6 in Apr (Mar: -16.3), the lowest since Dec 2022. Separately, German Ifo business climate worsened to 84.4 in Apr (Mar: 86.3), the lowest level since May 2020. The current assessment slipped to 85.4 (from 86.7) and expectations were down to 83.3 (Mar: 85.9).

- Germany producer prices rebounded in Mar: up 2.5% mom (Feb: -0.5%), it was the largest increase since Aug 2022 as energy costs surged (7.5%). Prices fell 0.2% yoy (Feb: -3.3%).

- Inflation in the UK rose to 3.3% yoy in Mar (Feb: 3.0%), driven by higher transport (4.7%) and fuels (4.9%) costs due to the conflict in the Middle East; services price inflation rose unexpectedly to 4.5% (Feb: 4.3%). Core CPI weakened to 3.1% (Feb: 3.2%).

- Unemployment rate in the UK eased to 4.9% in the three months to Feb (prev: 5.2%). Average earnings including and excluding bonus slowed, increasing by 3.8% and 3.6% yoy in the 3 months to Feb (prev: 4.1% and 3.8%).

- UK GfK consumer confidence fell for the third month in a row, to -25 in Apr (Mar: -21): the measure for personal financial situation over the last 12 months weakened to -11 points (vs -7 points) while the measure for personal financial situation fell to -4 (from +1 point).

Asia Pacific:

- The People’s Bank of China left unchanged the one-year Loan Prime Rate at 3.00% and the five-year rate at 3.50%, extending the hold for an 11th straight month. With Q1 growth and a pickup in inflation reducing the urgency for broad easing, policymakers appear to prefer targeted support over a fresh rate-cut cycle.

- FDI in China fell by 7.3% yoy in Q1 (Jan-Feb: -5.7%) even though 13,987 new foreign-invested enterprises were established, up 11% from a year earlier. Though overall inflows were weaker, high-tech and selected R&D-related segments still attracted strong interest; double-digit gains were reported in FDI from Luxembourg, Switzerland, France and South Korea.

- Inflation in Japan inched up to 1.5% in Mar (Feb: 1.3%), below the BoJ target for the second month running. Excluding food and energy, prices slipped to 2.4% (from 2.5%). Excluding fresh food, prices rose for the first time in five months: to 1.8% (from 1.6%). The Bank of Japan is expected to hold rates steady at its April meeting given that the Middle East conflict raised uncertainty and energy costs are pushing inflation risks higher.

- Exports from Japan grew for the 7th consecutive month, up by 11.7% yoy in Mar (Feb: 4%), with demand tied to data centres and semiconductors. Imports grew by 10.9%, slightly higher than 10.3%. Trade surplus widened to JPY 667bn (Feb: JPY 44.3bn). Exports to the Middle East plunged 45.9%, dragged down automobile shipments (-36.8%) but was offset to degree by exports to the US (+3.4%) and China (+17.7%).

- Japan’s preliminary manufacturing PMI rose to 54.9 in Apr (Mar: 51.6), the fastest pace since Jan 2022. Output grew at its quickest rate since Feb 2014 while delivery times lengthened sharply, input-cost inflation accelerated and business sentiment weakened because of uncertainty tied to the Middle East conflict.

- India’s preliminary manufacturing PMI increased to 55.9 in Apr (Mar: 53.9) with faster growth in output and export orders rising at the quickest pace in nine months while cost pressures remained elevated (due to fuel and raw material prices).

- South Korea’s GDP grew by 1.7% qoq and 3.6% yoy in Q1 (Q4: -0.2% qoq and 1.6% yoy), driven by a 5.1% qoq jump in exports led by AI-related semiconductor demand. This was the strongest quarterly growth since Q3 2020.

Media Review:

Top central banks gamble they have time on inflation risks

https://www.ft.com/content/7205961b-1c20-4699-b491-d9c45b278d1f?syn-25a6b1a6=1

Will Kevin Warsh Trumpify the Federal Reserve?

https://www.economist.com/finance-and-economics/2026/04/26/will-kevin-warsh-trumpify-the-federal-reserve

IMF Regional Economic Outlook Middle East & Central Asia Report Launch (webinar), with panel participation by Nasser Saidi

https://www.imf.org/en/videos/view/6393664974112

Forbes Middle East Cast: The Shock That Could Break the Global Economy with Dr. Nasser Saidi

https://www.youtube.com/watch?v=-kw0P_3Rikw

There is no such thing as a petrodollar: FT

https://www.ft.com/content/be345914-7b4b-4264-bcbd-6e5e33b798c7

Powered by:

![]()