Download a PDF copy of the weekly economic commentary here.

Markets

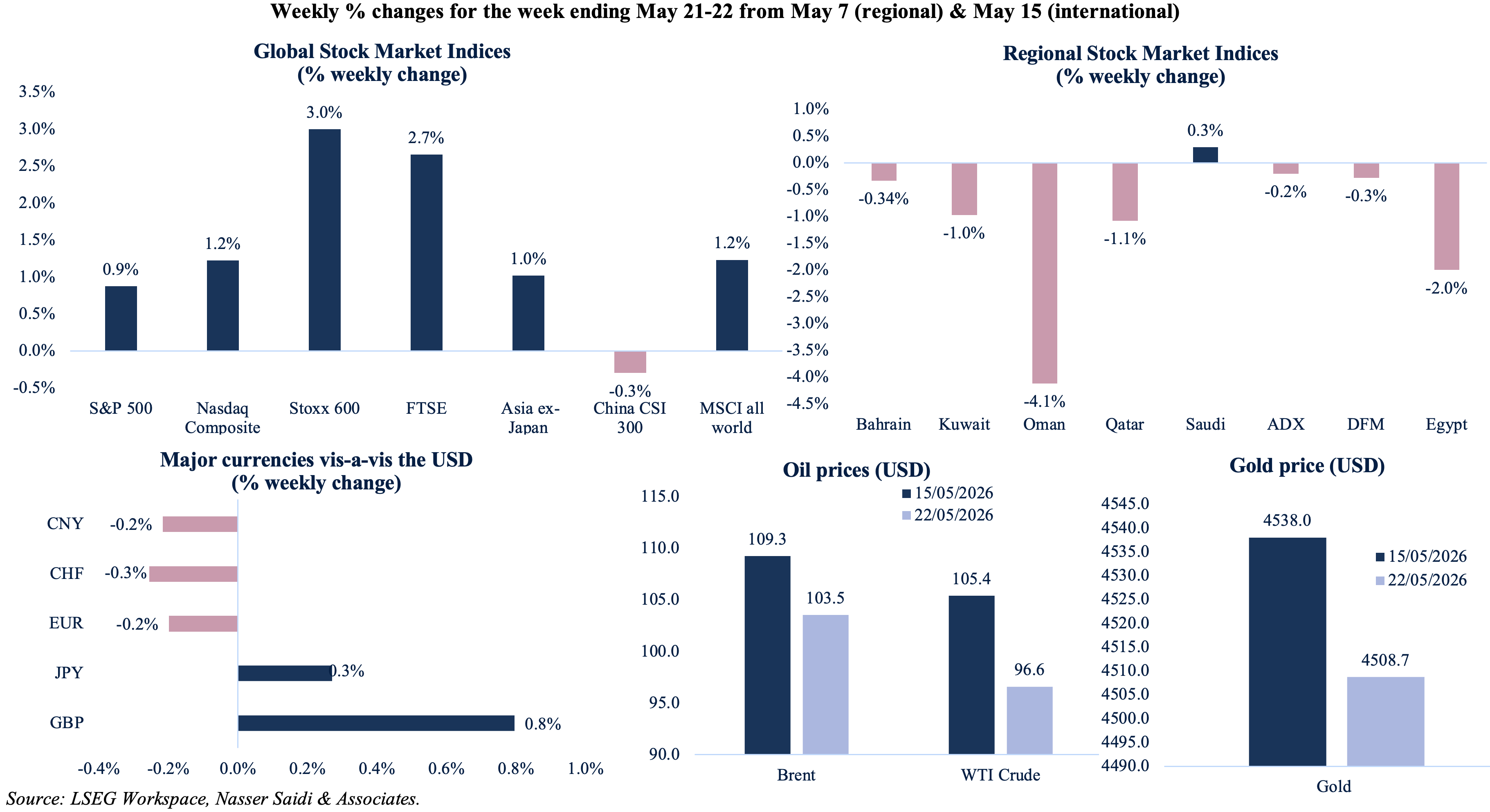

Global equity markets continue to wait for a potential US-Iran diplomatic breakthrough. Global indices were quite volatile based on conflicting announcements regarding the final stages of peace negotiations. S&P 500 posted an eighth consecutive week of gains, Dow posted a record closing high and European markets were also supported by tech stocks gains. Mirroring the tentative optimism, major Gulf equity bourses rebounded strongly on Thursday, with Oman’s index recovering from a nine-session losing streak and Dubai advancing after the announcement of an additional economic incentives package. The US dollar stayed near a six-week high. Though crude oil prices posted a weekly loss, it climbed on Friday driven by record drawdowns in US strategic stockpiles and IEA’s warning of a severe summer deficit. Gold price fell last week, for the second week in a row.

Economic Consequences from the conflict in the Middle East & Policy Responses

As of this morning (25 May), official reports indicate that bilateral talks to conclude the war have progressed significantly, with negotiators close to agreeing on a Memorandum of Understanding. This potential diplomatic de-escalation is affecting global asset prices, with oil prices falling (Brent is below USD 100). However, strains seem to still exist with the US Secretary of State revealing that the deal is “still a work in progress” and President Trump stating that the US will not “rush into a deal”. Meanwhile, Iran’s creation of a new “Persian Gulf Strait Authority” last week claiming “Iranian armed forces oversight” extending into the territorial waters of Oman and the UAE drew sharp criticism with the UAE and four Gulf States rejecting such a claim.

Despite the closure of the Strait of Hormuz, selective trade corridors are operational. Three super tankers successfully exited the waterway carrying 6 million barrels of Middle East crude oil, while a third Qatari LNG carrier has been routed toward Asian destinations. This underscores China’s strategic relationship with Iran, allowing its long-term energy inflows through while the rest of the world faces the blockade.

The ongoing supply disruption will hit global commodities severely: the UN’s FAO warned that the prolonged Hormuz closure will trigger a severe global “systemic agrifood shock” and retail price crisis within 6-12 months. Because synthetic nitrogen fertilizer inputs are dependent on Gulf natural gas processing, the current supply halt will translate into shortfalls in harvest by late autumn (a crisis that could deepen with the onset of El Niño weather phenomenon). Furthermore, the IEA Chief cautioned that global oil balances will enter a critical “red zone” by July and August as peak summer demand coincides with depleting inventories across the globe. Separately, the head of ADNOC stated during an event that global oil flows may take at least four months to recover to 80% of pre-conflict levels after the Iran war ends. This assessment emphasizes that the global energy deficit will persist well into H2 2026, irrespective of near-term truces.

In the industrial metals space, though the production of aluminium in the GCC has hit a 10-year low, it is not yet reflected in the London Metal Exchange (LME) price, However, multiple warning signals are evident: surge in physical premiums and a sharp tightening in LME’s benchmark cash-to-three-months spread. Ultimately, while OPEC+ leaders are expected to marginally raise their Jul oil output targets on paper (to stabilize global balances), the combination of reduced oil imports in Asia (to a 10-year low in April) and surging US crude exports is paving the way for a fragmented, multi-speed global macro recovery. On the sidelines, according to Reuters, 27 highly vulnerable developing countries are actively seeking to immediate access to the World Bank’s crisis toolkit amid the global economic fallout of the US-Iran war. This reflects the severe balance-of-payments strain and rising food and energy import costs among net-importing emerging markets as global commodity corridors remain compromised.

Lastly, despite the ceasefire, both Saudi Arabia and the UAE confirmed drone strikes last week, underscoring the persistent threats targeting the region’s infrastructure assets in the absence of a permanent agreement. The drone strike in Abu Dhabi caused a localized fire at the Barakah Nuclear Power Plant but no injuries or baseline grid disruption were reported.

Countervailing Regional Policies & Developments

- In a major diplomatic and economic milestone, the GCC and UK signed a landmark trade and investment agreement, in the backdrop of the yet unresolved US-Iran war. The GCC nations combined are equivalent to UK’s 10th largest trade partner. The FTA is expected to boost UK GDP by approximately USD 5bn annually in the long run, reduce tariffs on 93% of UK exports to GCC, simplifies customs procedures (targets to clear goods within 48 hours and perishables within 6 hours) and secures deep reciprocal commitments for Gulf investments into UK clean energy and infrastructure assets. The timing of the signing underscores a mutual mandate to establish secure, alternative trade corridors.

- The Central Bank of Egypt held its key overnight interest rates unchanged for the second consecutive meeting, opting to monitor volatile supply-side pressures stemming from regional trade disruptions; growth slowed in Q1, but remains at a robust 5.0% according to the central bank (versus Q4’s 5.3%). The overnight deposit and lending rate were left at 19% and 20% respectively alongside the discount rate at 19.5%. The apex bank will likely maintain this hold through Q3 2026, but any further escalation in global energy shocks will force a rate hike.

- In the first major MENA sovereign debt placement since the start of the US-Iran war, Egypt successfully raised USD 1bn via USD-denominated social and development bonds; the eight-year bonds received orders upwards of USD 3.9bn. The funds are earmarked to finance development projects (including healthcare and education) while providing critical social safety nets from recent cost-of-living increases.

- Egypt’s national carrier, EgyptAir, has resumed most of its operations (except to Kuwait, Bahrain and Iraq – which are under review) after seeing operations fall by almost 25% after the start of the US-Iran war. The chairman disclosed that the company is in a “healthy and good” financial and operational position despite severe airspace closures, re-routing challenges and higher airfares due to surge in jet fuel prices.

- Facing sharp revenue declines from the ongoing maritime blockades and disruption of crude oil movement through the Strait of Hormuz, Kuwait has been tapping the bond market. The central bank issued KWD 150mn in bonds last week, with the issue nearly four-times oversubscribed. Local bonds issued this fiscal year has crossed KWD 700mn and close to KWD 3.2bn since the enforcement of the public debt law in Mar 2025.

- Oman’s logistics and port sectors have successfully increased operational throughput, handling re-routed trade volumes. The value of logistics operations surged 45% mom to OMR 1.4bn in Apr, according to the director general of Oman Logistics Centre. Given its strategic geographic positioning outside the Strait of Hormuz, ports like Salalah and Duqm have successfully operated as major transit hubs for transportation of food, construction materials, fertiliser, medicine and manufacturing products.

- The Qatar Central Bank launched the working capital stabilization financing guarantee program specifically designed to shield domestic private-sector enterprises from liquidity problems during the ongoing conflict. The central bank has asked all banks to cooperate with the Qatar Development Bank program supporting specific sectors. This targeted programme is intended to protect corporate cash flows, prevent supply-chain bottlenecks and stabilize the private sector.

- Qatar Airways reported a decline in net profits in 2025-26 (-9% yoy to QAR 7.1bn) and headline passenger numbers (-3% yoy top 42mn), partly given the severe airspace restrictions and long, costly detours around the active war zone. Operational costs have increased significantly due to increased jet fuel prices and higher insurance risk premiums.

- The retail tranche of the first Saudi Arabian IPO since the outbreak of the regional war was heavily oversubscribed (+376% with orders totalling SAR 231mn), validating local retail confidence.

- ADNOC’s head confirmed that the construction of UAE’s strategic new crude oil pipeline, designed to bypass the volatile Strait of Hormuz, officially crossed the 50% completion milestone. This high-capacity, fast-tracked overland infrastructure is being built to route massive volumes of crude directly to export terminals on the East Coast in Fujairah.

- Dubai proactively approved a second economic incentives package valued at AED 1.5bn to lower operational overheads and streamline regulatory costs (such as exemption / deferral of license renewal fees, rents, financial obligations). This fiscal intervention aims to strengthen resilience and prioritize business continuity across sectors.

- Abu Dhabi Global Market (ADGM) announced a substantial increase in registrations and asset management licenses in Q1 2026, despite the US-Iran war and related geopolitical turmoil. ADGM announced a 5.2% increase in new active licenses in Mar and a 57% yoy surge in assets under management in Q1 2026.

- DP World confirmed securing AED 854mn (USD 230mn) in investments into the Jebel Ali Free Zone (Jafza) in Jan-Apr 2026, with more than 43% of these commitments coming during the months of war. International manufacturing and logistics firms are actively expanding, choosing Jafza as their base for the long haul – backed by its multi-modal sea-air-land alternative transport corridors.

- Emirates Airline commenced construction on a massive, state-of-the-art USD 5bn engineering and maintenance facility at Dubai World Central (Al Maktoum International). The complex, with an expected completion in 2030, is designed to secure the carrier’s fleet maintenance, repair, and overhaul (MRO) lifecycle.

- Reaffirming UAE’s commitment to energy transition, Masdar revealed it had deployed USD 45bn in capital on global renewable energy projects across six continents. It is fast-tracking utility-scale solar, wind and green hydrogen projects across strategic international corridors and has exported 65GW of renewable energy capacity worldwide.

- Dubai’s Knowledge and Human Development Authority (KHDA) officially confirmed a freeze on tuition fees for all private schools for the upcoming 2026–2027 academic year. This proactive intervention is designed to support household’s cost-of-living during a period of regional geopolitical uncertainty.

- GCC sovereign investors appear to have adopted a more cautious stance re US Treasuries holdings during war-affected March. Saudi Arabia’s holdings of US Treasuries fellby 6.73% mom to USD 149.6bn in Mar. Saudi still ranked 17th globally, a place ahead of South Korea. UAE also lowered its holdings in monthly terms (-4.8% mom to USD 114.1bn), but remaining the 19th largest holder globally. In contrast, Kuwait increased its holdings slightly to a new record USD 66.5bn (1.4% mom).

- British Airways officially pushed back its scheduled resumption of core Middle East flight networks to the start of August, citing prolonged airspace security hazards and highly volatile insurance risk premiums over these travel corridors.

Macroeconomic Developments in the MENA region

- The IMF began its seventh review of Egypt’s Extended Fund Facility (EFF) program, to potentially unlock USD 1.6bn in new financing. This team is also conducting the second review under the Resilience and Sustainability Facility (RSF) and discussing the impact of the war on the country which has “remained relatively contained” so far.

- According to CAPMAS, Egypt’s headline unemployment rate declined to of 6.0% in Q1 2026, down by 0.2 percentage points from Q4, highlighting labour market resilience amid a highly volatile regional backdrop. The number of unemployed persons fell 1.2% qoq to 2.126 million in Q1, equal to 6.0% of the total labour force.

- In a major subsidies overhaul, Egypt announced plans to transition from in-kind support to a targeted cash subsidy system by end of 2026. It was also revealed that there would be no further fuel price hikes before year-end. This is expected to eliminate fiscal leakage while insulating low-income households from the inflationary fallout of the nearby conflict.

- The Egyptian Exchange (EGX) expects close to 20 IPOs from state-owned companies by end-2026. This pipeline is driven by the government’s state asset-monetization mandate, and two state-owned companies (Egypt Education Platform and Egyptian Spinning & Weaving) will list on the main market within two months according to the Deputy Chairman of EGX.

- Egypt’s Ministry of Planning projects five sectors – manufacturing, wholesale & retail trade, tourism, construction and agriculture – to lift real GDP growth in the fiscal year 2026-27. GDP growth is forecast to range between 5.2%-5.4% in 2026-27 (vs H1 2025-26: 5.3%).

- Egypt set an aggressive target of achieving USD 6bn in cross-border digital exports in 2026, after clocking in a total of USD 5.2bn in 2025. The Minister of Communications and Information Technologydisclosed that there were more than 270 outsourcing centres in the country servicing international clients.

- Syria finalized an agreement with French shipping and logistics group CMA CGM to manage and operate two major inland dry ports. The operationalization of these dry ports will drastically reduce transit times across the Levant and could establishing Syria as an important land-based transit route for non-hydrocarbon trade corridors.

Macroeconomic Developments in the GCC

- Inflation in Kuwait accelerated to 2.6% yoy in Apr (the highest since Sep 2024) while monthly CPI strengthened sharply (0.65% mom) – a signal that supply-chain disruption and logistics costs are beginning to pass through to consumers. Food & beverages costs surged to 6.3% yoy from 5.7% as did transport costs (4.46%) while housing & utilities, education and restaurant/hotel prices remained relatively stable.

- In a major move toward digital infrastructure modernization, Kuwait awarded a Public-Private Partnership (PPP) deal to build a digital telecommunications network. This long-term project aims to overhaul the fixed telecommunications network, including the development of next-generation network systems, while it will be financed and developed by Bahrain’s Beyon Group.

- Oman’s fiscal position improved in Q1 2026 despite heightened regional instability. Total public revenues rose 13.3% yoy to OMR 2.98bn (with the rebound in energy revenues the primary driver) while the fiscal deficit narrowed sharply to just OMR25mn (Q1 2025: OMR136mn), reflecting both stronger hydrocarbon receipts and continued fiscal discipline. Public expenditure continued to rise, increasing 8.6% yoy to OMR3.01bn in Q1. Current spending accounted for 70.4% of the total while development expenditure surged, rising 31.5% to OMR 334mn), given reallocation to improve logistics and transport connectivity.

- Oman signed a contract for a continuous renewable power deal that combines wind, solar and battery storage, to reduce the country’s reliance on domestic natural gas for electricity generation. The scheme is part of a wider 2.7 GW hybrid renewable energy development spanning the Mahout and Duqm areas on Oman’s coast.

- The Oman Investment Authority (OIA), which manages about USD 60bn in assets, recorded USD 7.8bn in profits and achieved a 14.6% return on investments in 2025. Though OIA portfolio spans 52 countries, two-thirds of its holdings remain in Oman.

- Qatar’s CPI softened on a monthly basis in Apr, falling 0.74% mom, suggesting temporary demand weakness and administrative price rigidities helped cushion the initial energy shock. Headline inflation eased to 2.62% yoy (Mar: 4.17%); food and beverages costs surged to 10.4% yoy from 8.8% and clothing was up 4.71% while prices declined across health (-0.9% yoy), recreation & culture (-3.2%) and transport (-0.55%).

- Expanding its global upstream footprint, QatarEnergy acquired interests in three offshore exploration blocks in Uruguay. This international capital deployment is the firm’s first entry into Uruguay’s upstream sector and underscores a long-term strategy to diversify its hydrocarbon asset portfolio outside the Middle East. No financial details were provided.

- Qatar’s Estithmar Holding is working with Rothschild & Co to manage an IPO of its healthcare subsidiary Apex Health on the Qatar Stock Exchange, reported Bloomberg. No decision has been made on the timing or size of the IPO but it would give the exchange a boost as Qatar has raised only USD 375mn through two listings since 2020.

- A comprehensive economic impact assessment showed that the FIFA Arab Cup hosted by Qatar generated over QAR 2.89bn (USD 790mn), via contributions to tourism, hospitality, transport, and media sectors. The tournament, which attracted more than 305k international visitors, generated spending across aviation (QAR 289mn), hospitality (accommodation of QAR 315mn and F&B at QAR 246mn) and localized transport (QAR 84mn).

- Ratings updates across the GCC: Fitch affirms UAE’s AA- rating with stable outlook citing its strong external asset position, high per capita GDP and low consolidated government debt. Moody’s meanwhile affirmed A1 ratings of Saudi Arabia (with a positive outlook) and Kuwait (with a stable outlook).

Saudi Arabia Focus:

- Saudi Arabia’s total merchandise exports increased by 21.5% yoy to SAR 115.2bn in Mar 2026, with oil exports leading the surge (37.4%) due to the massive increase in oil prices. Oil exports touched SAR 92.5bn in Mar, the highest reading since Oct 2022; the share of oil in total exports jumped to 80.3% in Mar (Feb: 68.7%). Re-exports grew by a modest 2.5% yoy to SAR 9.2bn (a 12-month low). Imports grew at a slower pace than exports (12.2% yoy), leading to a wider trade surplus – the highest since Oct 2022 (SAR 57.4bn vs SAR 19.0 in Feb & SAR 18bn in Mar 2025). China remained the top trade partner, both the largest export destination and import source.

- Operating Revenues Index in Saudi Arabia recorded a 10.2% yoy increase in Mar, thanks to sectors including transportation (+25.8%), mining (25.5%), information & communications (18.5%) and financial services (17.6%) while manufacturing gained 4%. Overall Employee Compensation Index grew by10% yoy with gains across multiple sectors.

- The Saudi Ports Authority (Mawani) launched direct express container shipping service between the King Fahd Industrial Port in Yanbu, Ain Sokhna Port in Egypt and Aqaba Port in Jordan. This initiative will see faster cargo handling, shorter waiting times, and improved supply chain efficiency.

- Saudi Aramco unveiled the country’s first quantum computer dedicated to optimizing energy modelling as well as upstream reservoir and supply chain operations. The computer was developed in partnership with the French quantum computing company Pasqal.

- Saudi Capital Market Authority (CMA) announced an easing of regulatory rules for securities offerings, including the lowering of the minimum capital requirement for securities businesses by 60% to SAR 20mn. These amendments are expected to lower barriers to entry, simplify disclosure requirements while driving transparency.

- Construction costs in Saudi Arabia ticked up by 2.4% yoy in Apr, as equipment rental and labour costs increased. In residential sector, energy prices and labour costs were up by 3% and 2.8% respectively while both increased by 3% in the non-residential sector.

- With Saudi Arabia reviewing spending on its giga projects, NEOM announced the cancellation of a contract for building the USD 1.6bn rail link project to connect the Oxagon port and industrial hub with The Line development.About 20% of this project work is complete, according to Italy’s Webuild that was awarded the contract.

- Authorities finalized contracts worth OMR 74mn (USD 192mn) to develop infrastructure in an economic zone near the Saudi-Oman border. This cross-border economic cluster will further increase trade across the border – which almost tripled to OMR 320mn in Mar (Feb: OMR 112mn).

- The Public Investment Fund (PIF) is exploring the possibility to merge its rail, ports shipping assets into a single, unified entity. While discussions began pre-war, according to Bloomberg, such a consolidation will lower supply chain costs and maximize efficiencies in the current trade landscape.

UAE Focus:

- UAE and Austria are exploring trade and investment partnerships, focusing on energy diversification and future-oriented technologies. UAE’s non-oil foreign trade with Austria grew by 16.4% yoy to USD 2.1bn in 2025 and a significant 87.7% increase since 2019.

- Dubai Investments is moving ahead with a listing of Dubai Investment Park (DIP) on DFM before end of the year, selling 24% of the unit. Details are expected to be released later as the “group continues to assess the optimal timeline for the IPO and remains engaged with the relevant… stakeholders”.

- Etihad Rail completed construction of its first passenger train station in the emirate of Fujairah, a major milestone in the UAE’s inter-emirate rail network. Official information states that travel time between Fujairah and Abu Dhabi will be 105 minutes, with trains accommodating almost 400 passengers and running at up to 200kms per hour.

Global Macroeconomic Developments

US/Americas: The latest US macro data and FOMC meeting minutes indicate a stagflationary economic landscape that suggests a highly restrictive monetary stance from the Fed (that just saw a new governor being sworn in). On the labour front, initial jobless claims slipped by 3k to 209k in the week ending May 16 and the four-week moving average stood at a low 202.5k, even as continuing claims crept up slightly to 1.782mn. This tight labour market data was accompanied by bunch of mixed macro signals: housing sector statistics showed pending home sales expanding by 1.4% mom and building permits jumping 5.8% to 1.442mn in Apr, even as housing starts fell by 2.8% to an annualized 1.465mn. Similarly, while the headline Philadelphia Fed manufacturing index plunged to -0.4 in May (Apr: 26.7), the broader S&P Global manufacturing PMI accelerated to an expansionary 55.3 (Apr: 54.5), contrasting with a minor softening in services PMI to 50.9. Most concerning was the University of Michigan consumer sentiment index which collapsed to a record-low of 44.8 in May, with expectations also deteriorating to 44.1. Driven by rising energy costs (average gasoline price in the US has risen more than 50% since the war began) and supply chain disruption, the one-year and five-year inflation outlooks jumped to 4.8% and 3.9% respectively (from preliminary readings of 4.5% and 3.4% respectively). According to the FOMC minutes, this combination of sticky (and above-target) inflation, robust manufacturing activity and tight labour market is leading to a more hawkish consensus, signalling that interest rates must remain “higher-for-even-longer” potentially dismissing rate cuts in the rest of the year.

Europe: In the Eurozone, the flash manufacturing PMI edged down to 51.4 (Apr: 52.2), as new orders fell and employment decreased, while also dragged down by Germany’s preliminary manufacturing PMI slipping back into contractionary territory at 49.9 (Apr: 51.4). Rising energy and raw material costs are a big worry (from the PMI readings), also evidenced by the German Producer Price Index jumping 1.2% mom and 1.7% yoy in Apr (it was the first yoy increase since Feb 2025). Business and consumer sentiment in contrast were rising in May: the German Ifo business climate index rose to 84.9 from April’s 6-year low (with its current assessment rising to 86.1 and expectations improving to 83.8) and the German GfK consumer confidence index climbed to -29.8 in June (May: -33.1). It was a data-heavy week in the UK – headline CPI eased to 2.8% yoy, core CPI moderated to 2.5% and the retail price index cooled to 3.0%, though producer input prices accelerated sharply to 7.7% (Mar: 5.3%). Unemployment inched up to 5.0% in the three months to March and core regular wage growth slipped to 3.4% (from 3.6%). While UK retail sales collapsed (-1.3% mom in Apr, the sharpest drop since May 2025), flash manufacturing PMI steady at 53.7 in May and GfK consumer confidence inching up to -23 (from Apr’s -25) were two silver linings.

Asia Pacific: The People’s Bank of China maintained its benchmark policy rate at 3.0% (for the 12th straight month), even as the growth momentum seems to be slowing – fixed asset investment fell by 1.6% yoy in Jan-Apr, retail sales posted a mere 0.2% growth in Apr (weakest gain since Dec 2022) and industrial output slipped to 4.1% yoy (Mar: 5.7%). Conversely, Japan’s real economy showed Q1 GDP expanding at a 2.1% annualized pace (and 3.4% yoy). However, this was supported by external trade component while consumption and capex inched up only 0.3% qoq. Exports surged further in Apr, up by 14.8% yoy while trade surplus narrowed by nearly half to JPY 301.9bn due to inflated imported energy and raw material costs. Headline inflation in Japan meanwhile eased to 1.4% and core inflation softened to a 4-year low of 1.4%, weakening the case for a BoJ hike, while the preliminary manufacturing PMI softened to 54.5 and the services PMI hit a neutral 50.0.

Media Review:

The energy crisis may just be starting

https://www.ft.com/content/fb290ca1-4fa0-4309-b406-8c850d0b2449?syn-25a6b1a6=1

Three months in, is Trump losing the Iran war?

https://www.reuters.com/world/asia-pacific/three-months-is-trump-losing-iran-war-2026-05-23/

Responding to the Energy and Food Price Shock: Getting the Policy Details Right

Investors fear another surge in inflation

https://www.economist.com/finance-and-economics/2026/05/19/investors-fear-another-surge-in-inflation

Powered by:

![]()