Saudi foreign trade. Oman fiscal picture. Inflation in Kuwait & Qatar. UK-GCC FTA. GCC US Treasuries holdings.

Download a PDF copy of this week’s insight piece here.

GCC: Trade Dynamics, Fiscal Shifts & Inflation Risks, Weekly Insights 23 May 2026

1. Saudi oil exports surged in Mar to the highest since Oct 2022, despite low production & export volumes

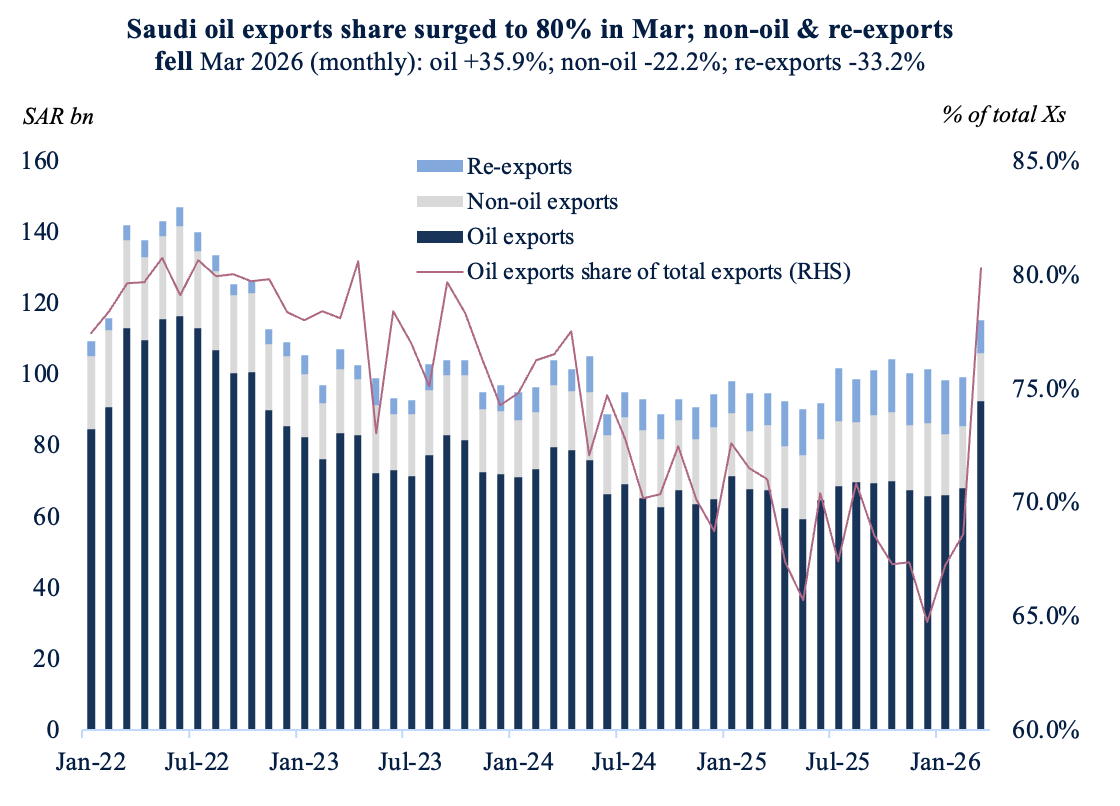

- Total merchandise exports surged by 21.5% yoy to SAR 115.2bn in Mar 2026, with oil exports leading the surge (37.4%) due to the massive increase in oil prices. Oil exports touched SAR 92.5bn in Mar, the highest reading since Oct 2022; the share of oil in total exports jumped to 80.3% in Mar (Feb: 68.7%). Re-exports grew by a modest 2.5% yoy to SAR 9.2bn (a 12-month low).

- Oil production and export volumes were the lowest on record in Mar due to traffic disruption at the Strait of Hormuz; but the re-routing of crude exports to the Red Sea port Yanbu & oil prices surge led to higher value oil exports.

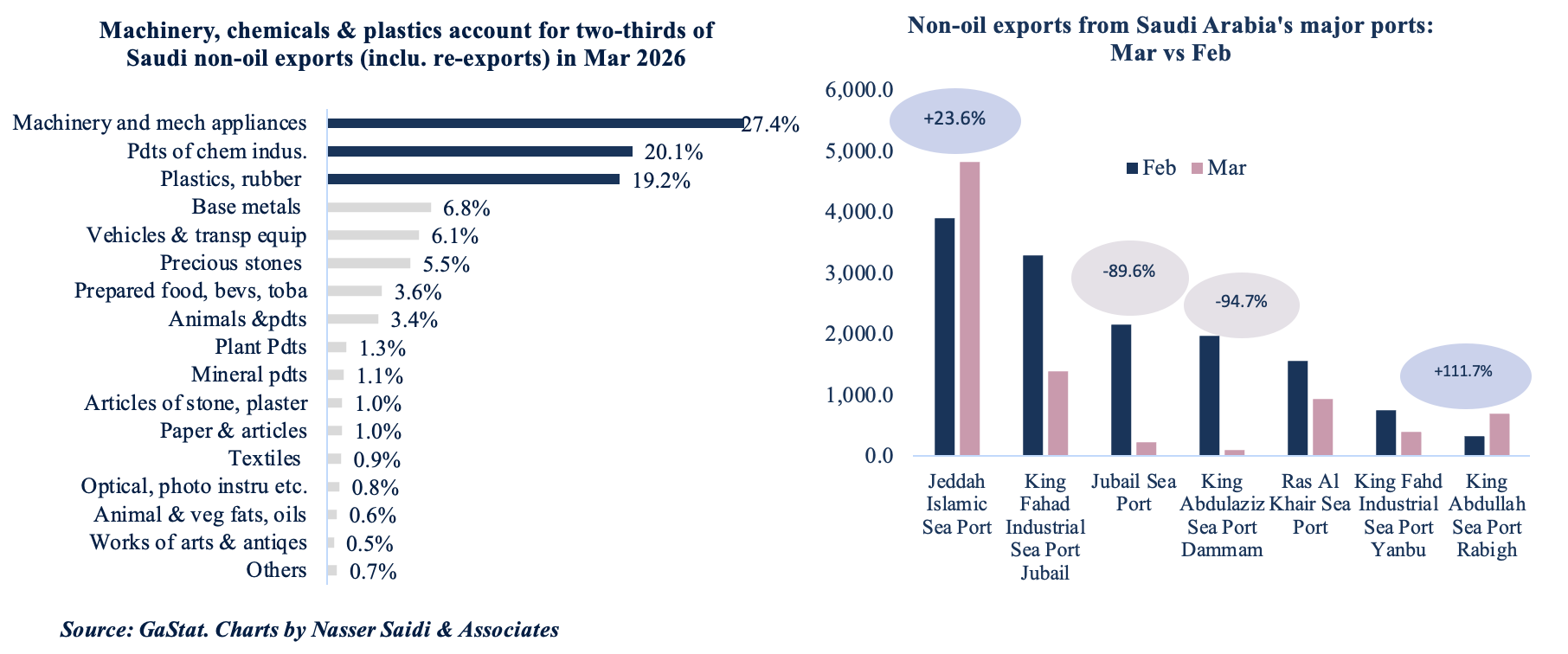

- Non-oil exports (including re-exports) declined 17.3% yoy to SAR 22.7bn in Mar. Machinery was the largest segment of total non-oil exports (27.4%; this also made up over half of re-exported goods), followed closely by chemicals & products (20.1%) and plastics, rubber & articles (19.2%). These are the high-value industrial inputs required for manufacturing.

- Imports grew at a slower pace than exports (12.2% yoy), leading to a wider trade surplus – the highest since Oct 2022 (SAR 57.4bn vs SAR 19.0 in Feb & SAR 18bn in Mar ‘25).

- China remained the top trade partner (largest export destination and import source); India & Japan followed closely as export partners, driven by higher value of oil exports. Among import partners, US & UAE were the closest to China.

- UAE alone accounted for 32.7% of Saudi non-oil exports; share of non-oil exports with GCC was 42.5%.

- Jeddah Islamic Seaport and King Abdulaziz International Airport handled a combined 44.5% of non-oil exports in Mar. The disruption at main ports is evident from the monthly drop in non-oil exports across Jubail Sea Port and the Sea Port Dammam.

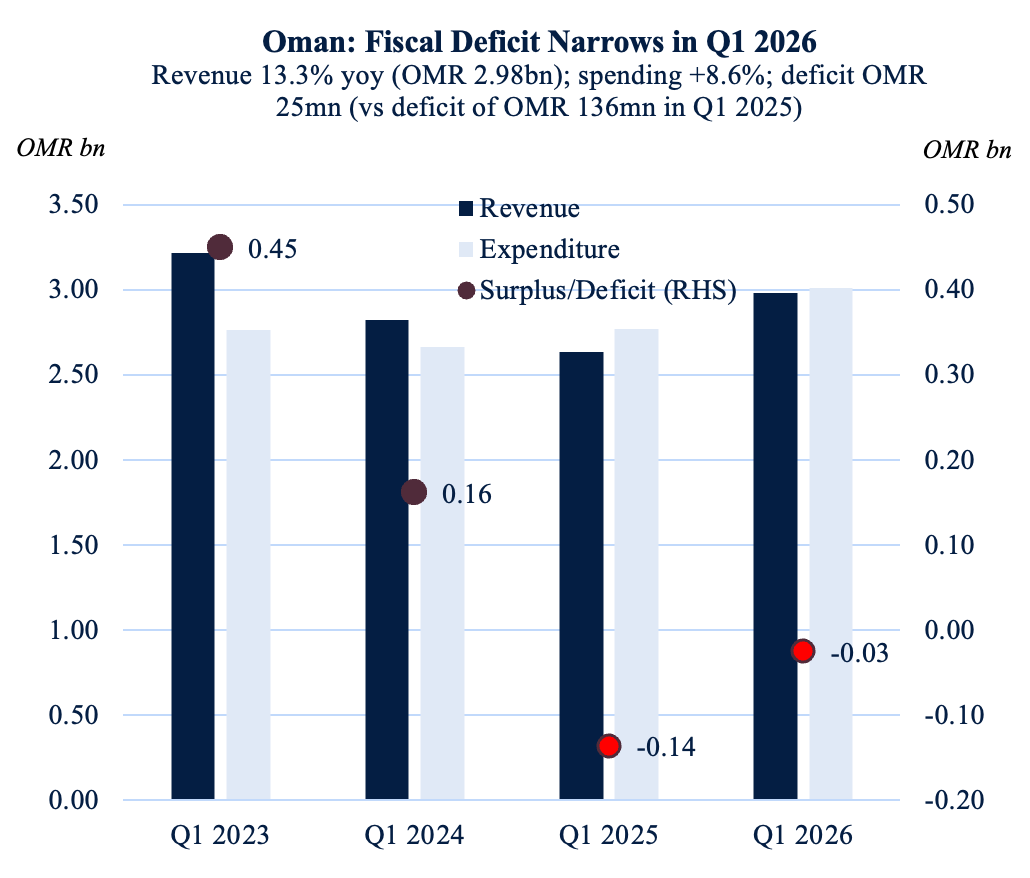

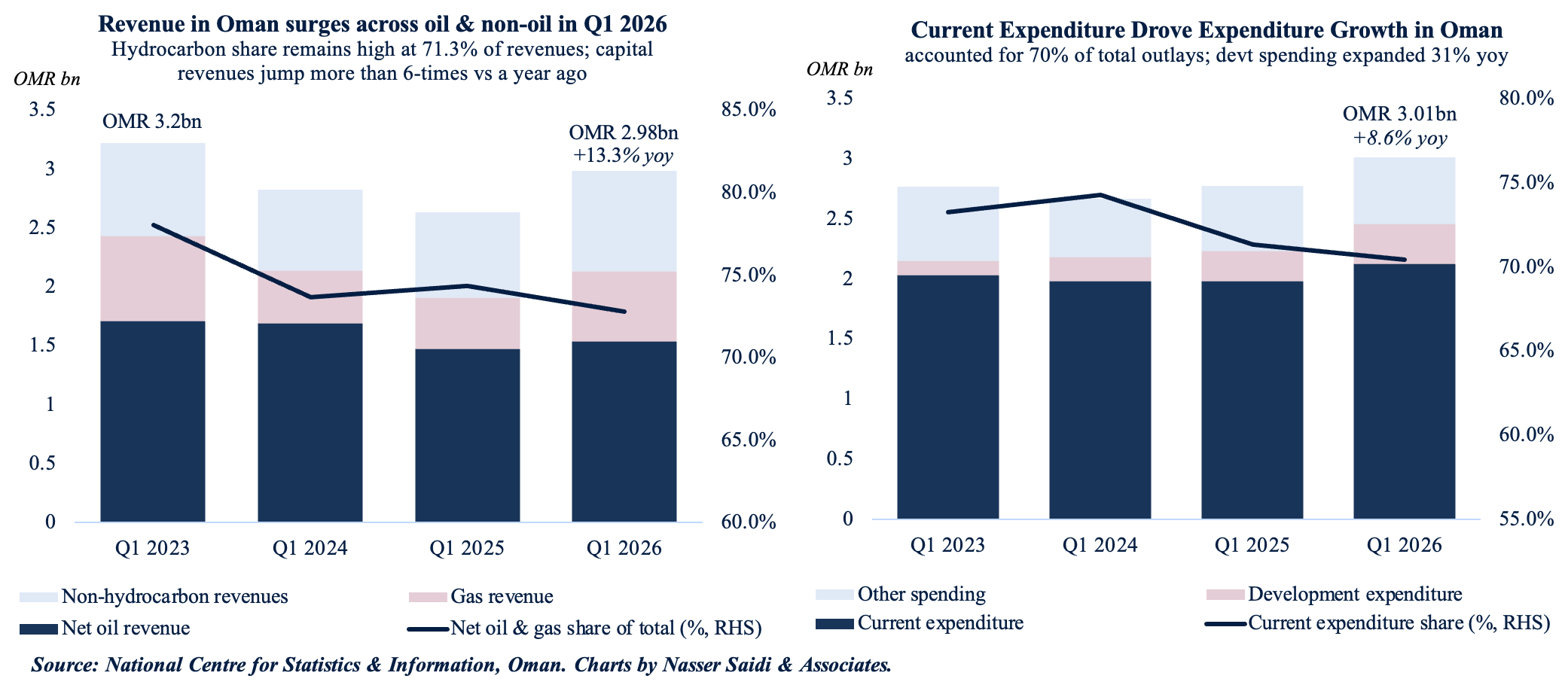

2. Oman’s fiscal deficit narrowed to OMR 25mn in Q1 ’26 as revenues surge 13.3%

- Oman’s fiscal position improved in Q1 2026 despite heightened regional instability. Total public revenues rose 13.3% yoy to OMR 2.98bn, while the fiscal deficit narrowed sharply to just OMR25mn (Q1 2025: OMR136mn), reflecting both stronger hydrocarbon receipts and continued fiscal discipline.

- The primary driver was the rebound in energy revenues. Net oil revenues increased 4.6% to OMR1.54bn in Q1, while gas revenues surged 36.0% to OMR 593mn. Oman benefitted from higher production (oil: 4.8% to 93.1mn barrels and a 2.5% jump in natural gas output) as well as elevated regional energy prices following the outbreak of the Iran war and disruptions across other major GCC export routes. Unsurprisingly, hydrocarbons accounted for 71.3% of revenues.

- However, non-hydrocarbon revenues in Oman also grew by 17.2% yoy to OMR 857mn, largely given the six-fold increase in capital revenue to OMR 40mn.

- Public expenditure continued to rise, increasing 8.6% yoy to OMR3.01bn in Q1. Current spending accounted for 70.4% of the total while development expenditure surged, rising 31.5% to OMR 334mn), given reallocation to improve logistics and transport connectivity (e.g. Hafeet Railway, multi-modal hubs of Salalah & Duqm).

- The government undertook fiscal interventions to support its residents: established regional food depots & essential material reserves, OMR 50mn aid package was aimed at subsidizing domestic farmers).

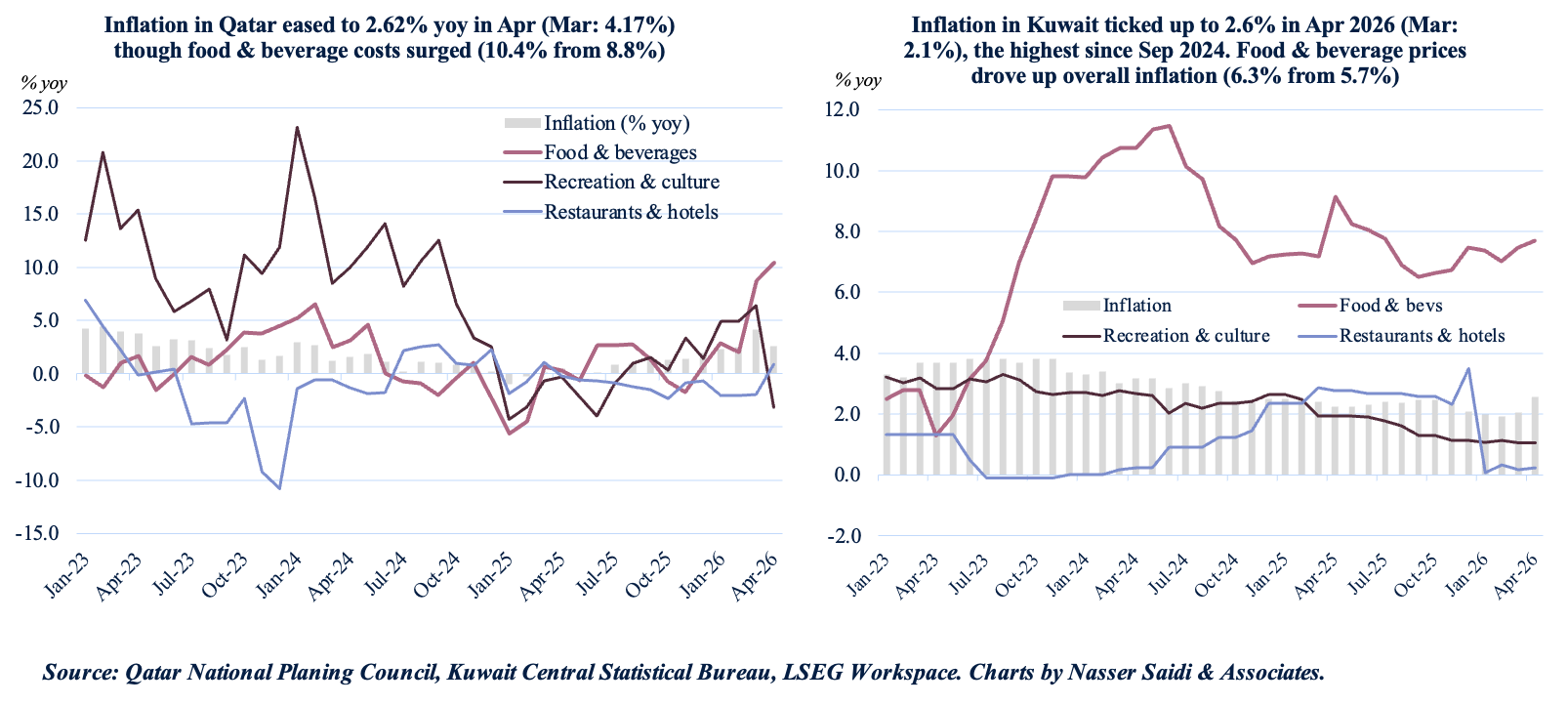

3. Though inflation stayed relatively muted at 2.6%, April inflation dynamics diverged notably between Qatar and Kuwait

- Both Qatar and Kuwait are visibly experiencing second-round effects from the Iran war. The near-closure of the Strait of Hormuz has significantly disrupted regional supply chains as well as increased delivery times and import costs across the GCC.

- Qatar’s CPI softened on a monthly basis in Apr, falling 0.74% mom, suggesting temporary demand weakness and administrative price rigidities helped cushion the initial energy shock.

- Kuwait, by contrast, is showing clearer signs of imported inflation pressure. Inflation accelerated to 2.6% yoy in Apr (the highest since Sep 2024) while monthly CPI strengthened sharply (0.65% mom) a signal that supply-chain disruption and logistics costs are beginning to pass through to consumers.

- The common point was the surge in food & beverages costs (weights of 13.5% in Qatar and 16.7% in Kuwait). In Qatar, it surged to 10.4% from 8.8% while in Kuwait it jumped to 6.3% from 5.7%. Qatar recorded decline in prices across health (-0.9% yoy), recreation & culture (-3.2%) and transport (-0.55%). For now, housing & utilities, education and restaurant/hotel prices have remained relatively stable in both.

- Looking ahead, three indicators should be watched closely: first, whether shipping disruptions through Hormuz persist into summer; second, whether food inflation accelerates materially across the GCC; and third, whether governments maintain subsidies and price controls despite rising fiscal costs.

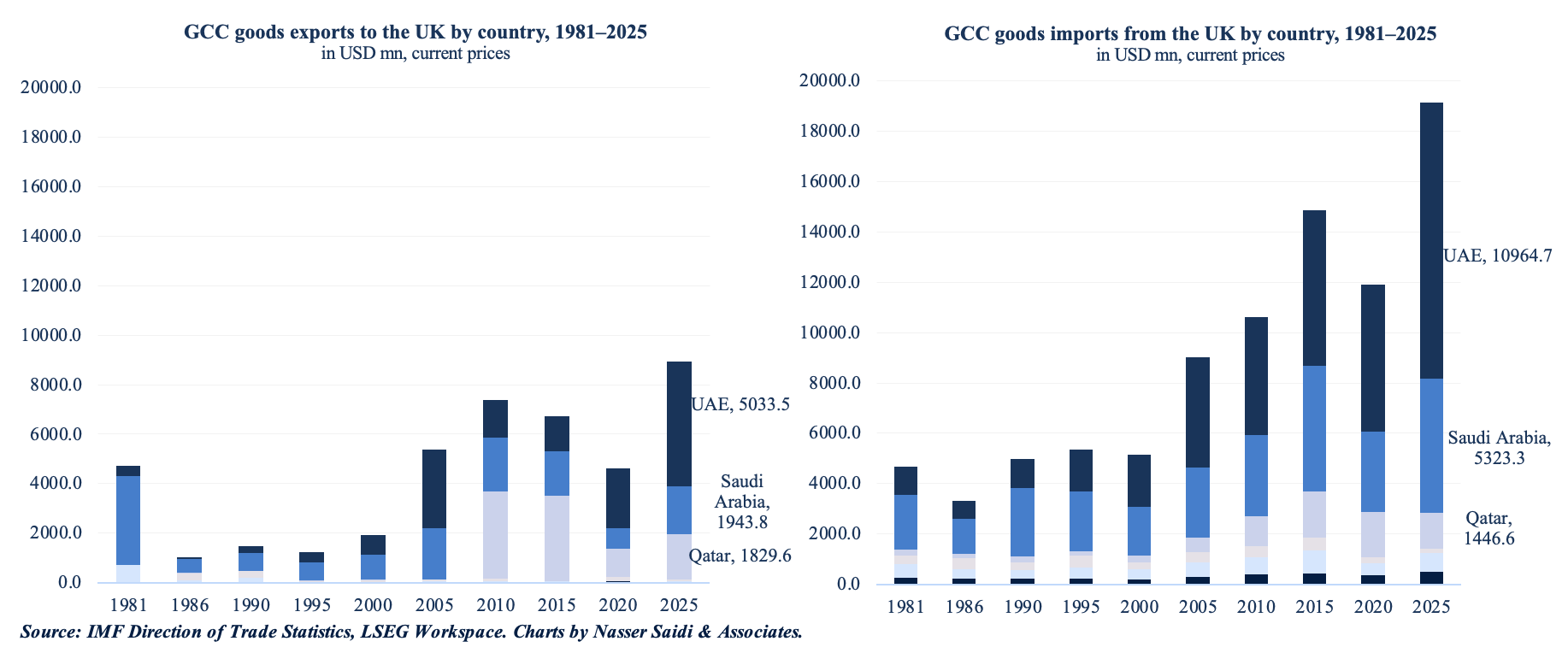

4. Landmark UK-GCC FTA signed

- The GCC and the UK concluded a landmark free trade agreement (FTA) this week after negotiations that began in 2022, making UK the first G7 country to secure a comprehensive FTA with the GCC. The GCC nations combined are equivalent to UK’s 10th largest trade partner.

- GCC-UK goods trade has expanded over time, with expansion driven much more by GCC imports from UK than by GCC exports to UK. Trade has become increasingly concentrated in Saudi Arabia and UAE over time; UAE accounts for half of total GCC-UK goods trade.

- The FTA is expected to boost the UK by approximately USD 5bn annually in the long run, while reducing tariffs on 93% of UK exports to GCC countries. This will lower import costs for UK food, drink and manufacturing items entering the GCC, while optimizing the supply chains of GCC industrial exporters by removing duties on petroleum products, chemicals, and plastics. Around GBP 360mn worth of duties will be removed immediately once the deal enters into force.

- The FTA also strengthens investment protections and services access for businesses on both sides, while also simplifying customs procedures with targets to clear goods within 48 hours and perishables within 6 hours. Moving beyond traditional merchandise trade, the FTA breaks down non-tariff barriers in professional services, with provisions for digital trade, cross-border data flows and IP protection. The UK exported more than GBP 20bn in services to GCC last year.

- The FTA comes at a critical juncture, allowing for bilateral investment in energy transition (including carbon capture and offshore wind technology) as well as securing critical supply lines (provisions for simplified, fast-tracked customs procedures and multi-modal transit coordination will allow for trade continuity).

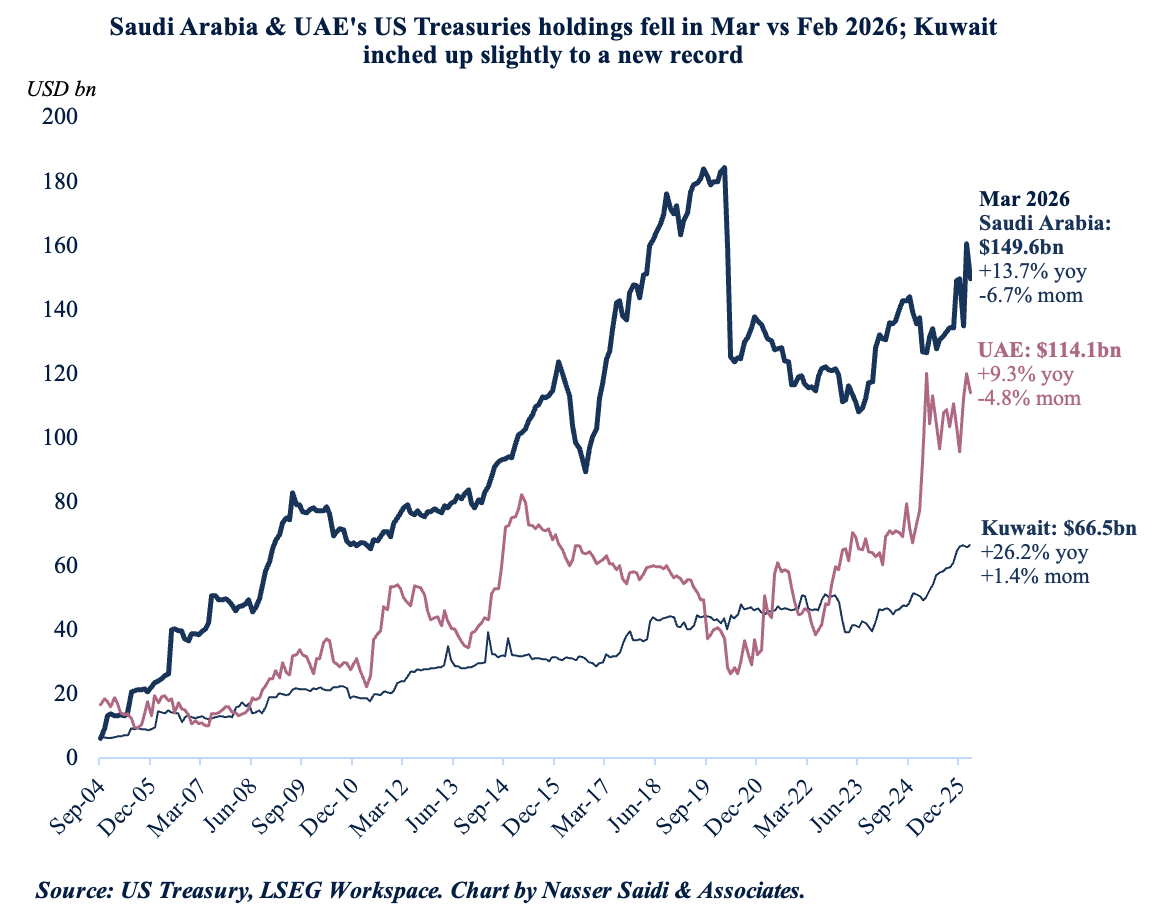

5. Saudi Arabia & UAE US Treasuries holdings slip in Mar from Feb

- Foreign holdings of US Treasury securities fell by 1.5% mom to USD 9.35trn in Mar from Feb’s record high, reflecting heightened geopolitical conditions, rising oil prices and renewed concerns over the US fiscal outlook in the backdrop of the Iran war.

- Japan remained the largest foreign holder of US Treasuries despite a sharp reduction in exposure (-3.8% mom to USD 1.192trn). China continued to trim its exposure (potentially driven by sanctions risk, reserve diversification and growing gold accumulation): holdings fell 6.0% mom to USD 652.3bn, the lowest level since Sep 2008 and more than 14% since early 2025. The UK, which functions as a global custody and hedge fund hub, saw its holdings rise 3.3% to USD 926.9bn.

- GCC sovereign investors appear to have adopted a more cautious stance during war-affected March.

- Saudi Arabia’s holdings of US Treasuries fell by 6.73% mom to USD 149.6bn in Mar. Saudi still ranked 17th globally, a place ahead of South Korea.

- UAE also lowered its holdings in monthly terms (-4.8% mom to USD 114.1bn), but remaining the 19th largest holder globally.

- In contrast, Kuwait increased its holdings slightly to a new record USD 66.5bn (1.4% mom).

- Higher percentage holdings by GCC are also a reflection of lower holdings by China and others, resulting in higher relative shares.

- Worth watching if the GCC will increase Treasury purchases later this year as elevated oil revenues rebuild external surpluses.

Powered by:

![]()