UAE & Qatar monetary stats. Saudi inflation.

Download a PDF copy of this week’s insight piece here.

Weekly Insights 21 Jun 2024: Robust monetary sector performance in the GCC as inflation stays muted

1. UAE banks’ deposits & assets post robust growth in Q1 2024

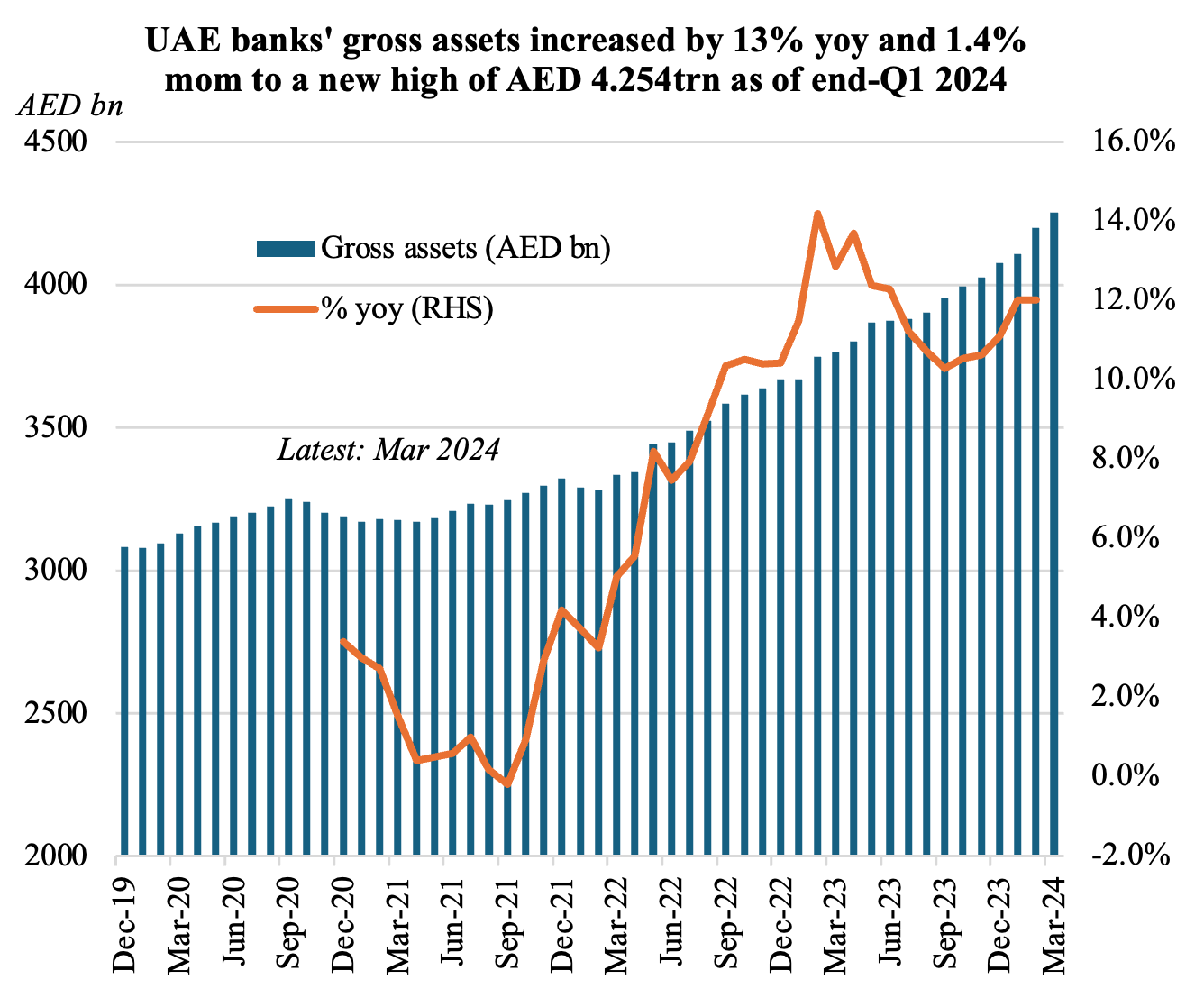

- UAE’s gross bank assets increased further in Mar 2024, rising to AED 4.254trn (up 1.4% mom and 13% yoy).

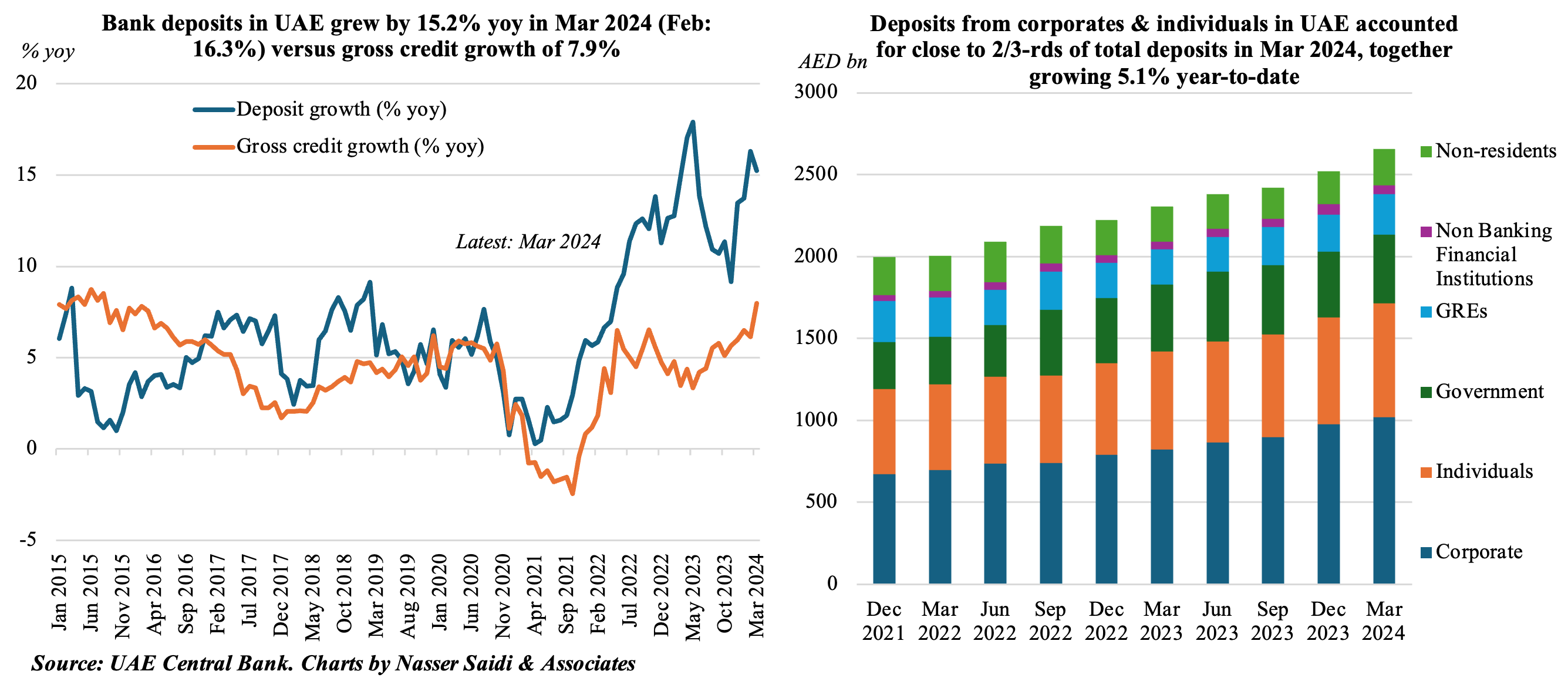

- Deposits in the UAE grew by 1.5% mom & 15.2% yoy in Mar, thanks to a healthy 1.5% mom & 16.4% uptick in resident deposits; non-resident deposits share was 8.3%.

- Private sector deposits account for 64.5% of total deposits and 70.3% of total resident deposits as of end-Q1 2024. This includes both corporates and individuals’ deposits: which grew at a very robust 24.2% yoy and 15.3% respectively.

- Government and GREs together accounted for one-fourth of total deposits in Mar; these grew by 4.5% and 10.7% year-to-date.

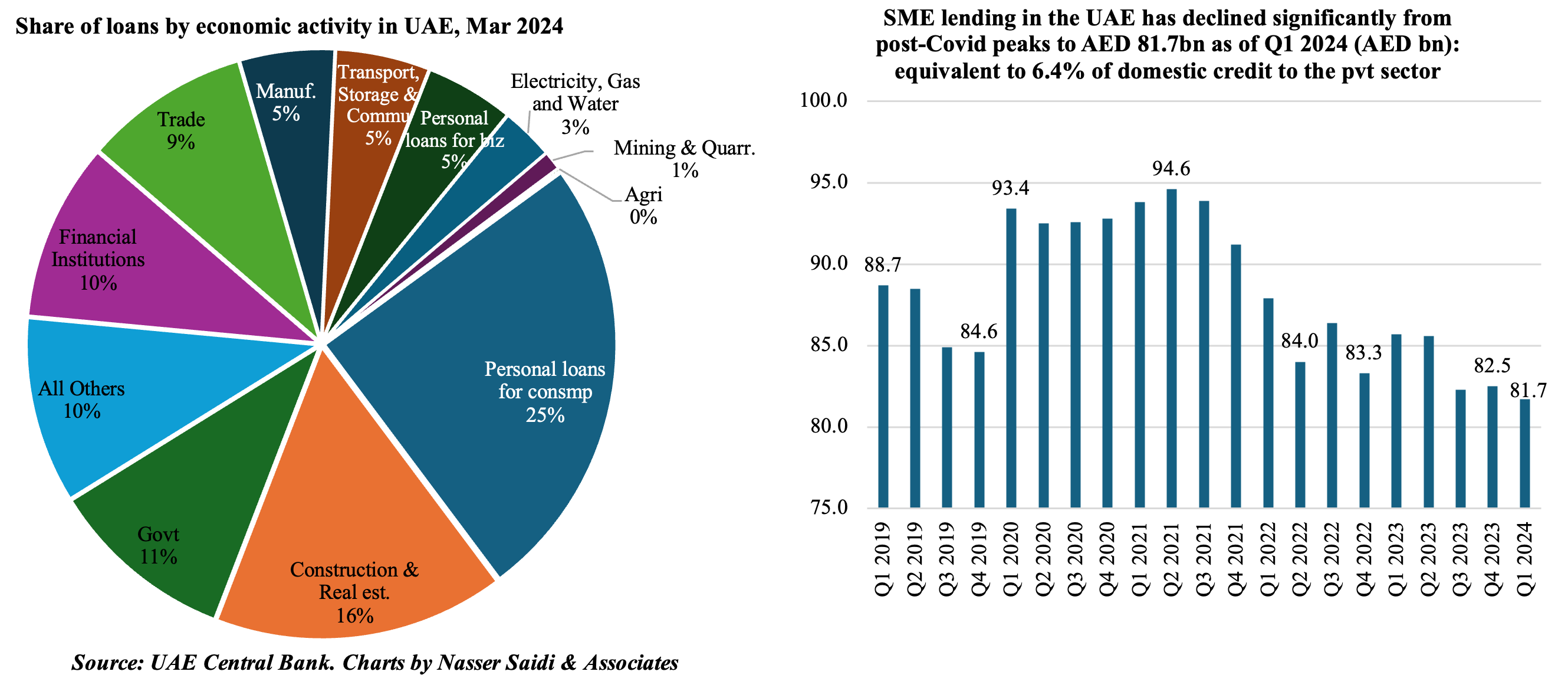

2. UAE’s domestic credit growth stood at 2.2% year-to-date (Q1 2024)

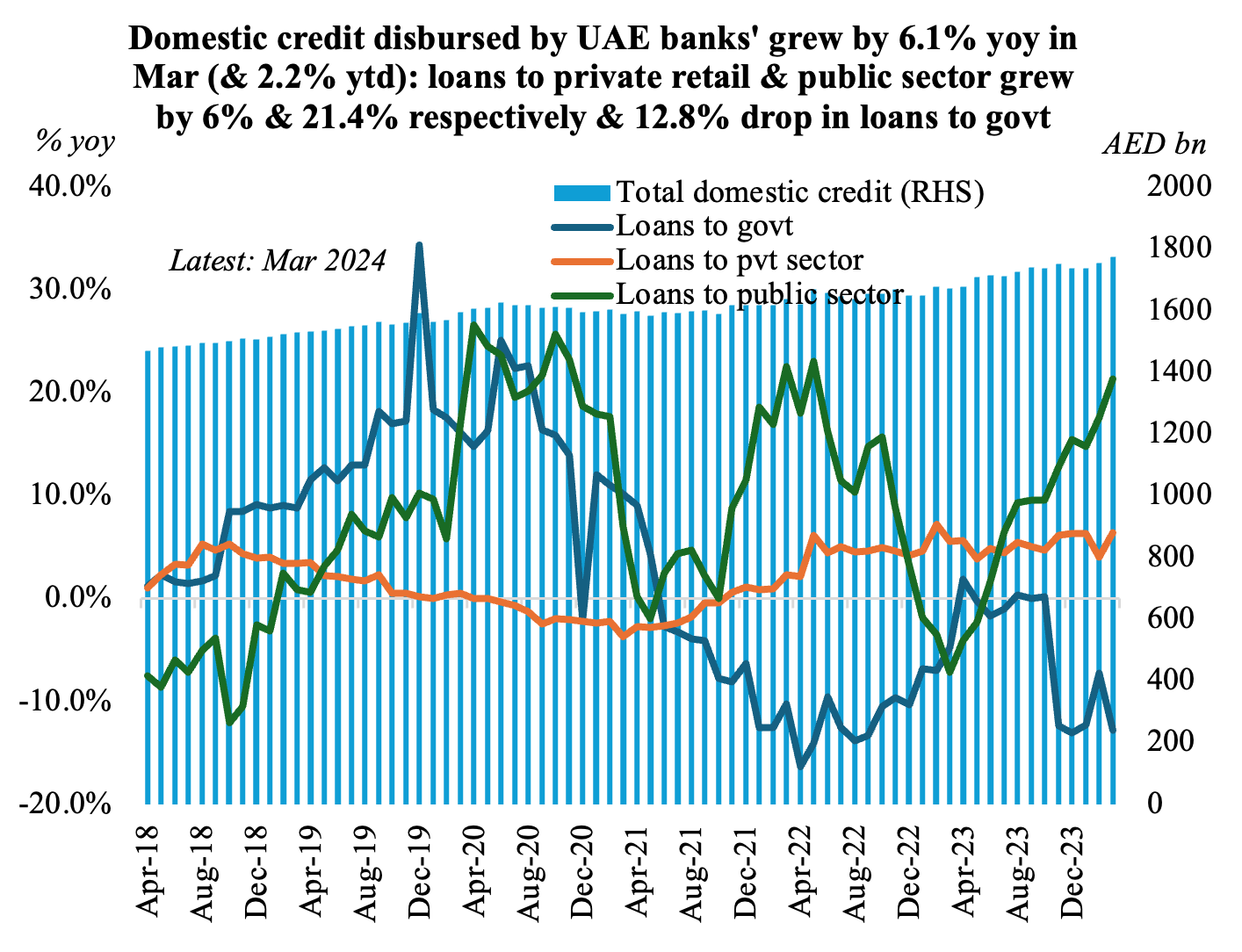

- Overall domestic credit in the UAE grew by 1.1% mom and 6.1% yoy to AED 1.776trn in Mar.

- Credit to the private sector accounted for 72% of domestic credit. Within the private sector, credit to business and industrial (at AED 841.7bn) accounted for 2/3-rds. Credit disbursed to SMEs stood at AED 81.7bn as of end-Mar, down by 4.7% yoy and 1.0% year-to-date, accounting for about 6.4% of total domestic credit to the private sector.

- Loans to the government and GREs have increased by 2.3% and 1.7% year-to-date.

- Bank credit to residents by economic activity show that personal loans for consumption purposes accounts for one-fourth of total, followed by construction & real estate (16%) and government (11%).

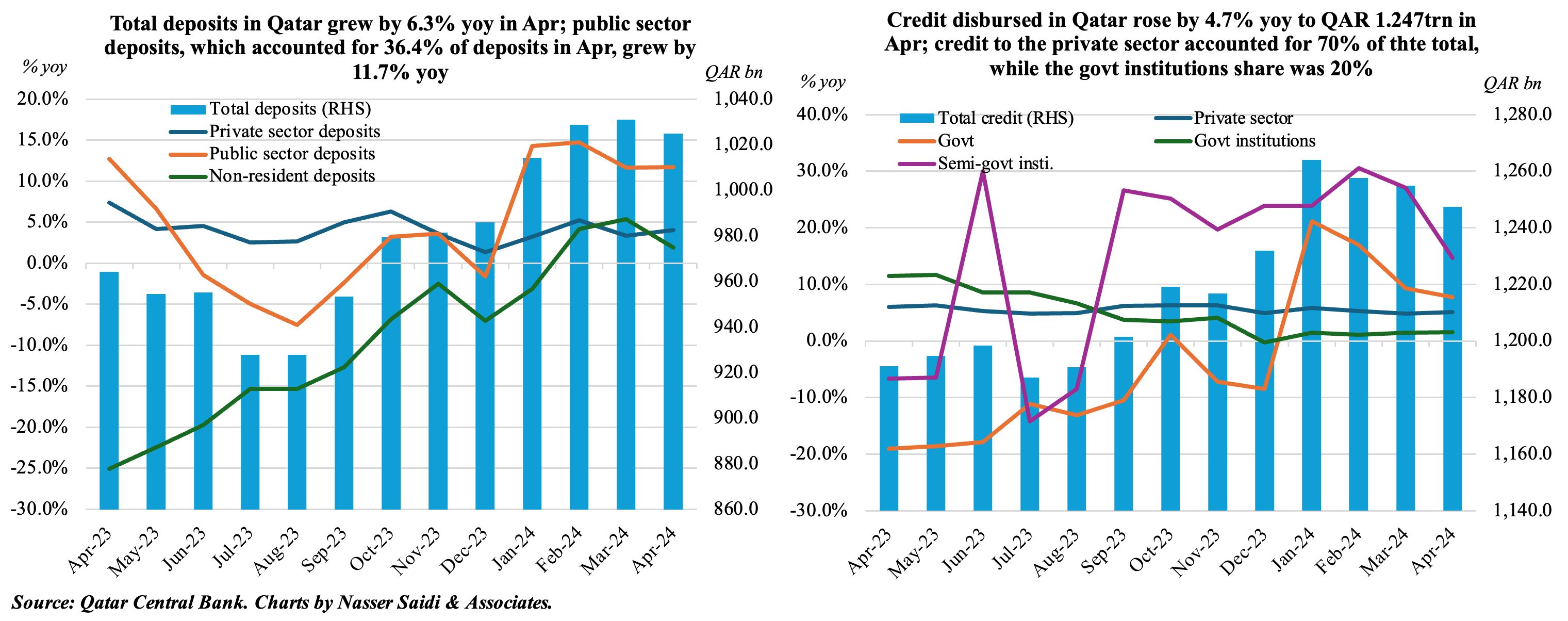

3. Qatar’s monetary sector performance in April shows robust credit & deposit growth

- Latest monetary statistics from the Qatar central bank shows a 6.3% increase in commercial bank deposits in Apr, driven by public sector deposits (+11.7% yoy and 0.9% mom to QAR 372.9bn; this accounted for 36.4% of total deposits); private sector deposits edged down slightly in month-on-month terms (-0.9%, but was up 4% yoy).

- Credit growth grew by 4.7% yoy in Apr (Mar: 4.9%). Claims to the private and government sectors increased by 5.1% (to QAR 867.3bn) and 7.8% (to QAR 111.1bn) respectively. Credit to government institutions accounted for 20% of total credit and edged up by 1.5% yoy to QAR 248.41bn.

- Meanwhile, money supply growth remained healthy: M2 and M3 were up by 5.7% and 7.2% respectively. Overall assets of commercial banks grew by 3.7% to QAR 1.96trn.

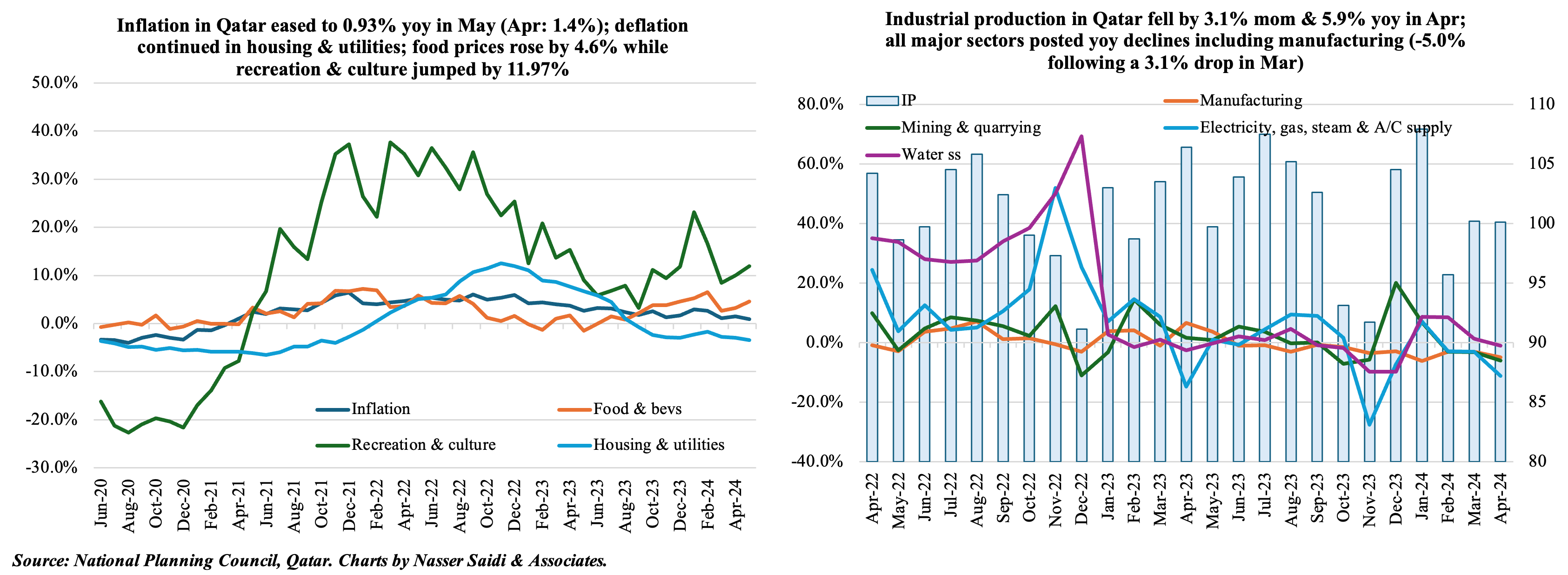

4. Inflation in Qatar eased in May; industrial production declined in Apr

- Inflation in Qatar eased to 0.93% yoy in May (Apr: 1.4%) as per data released this week by the National Planning Council. Food prices ticked up to 4.6% (from 3.2%) as did recreation costs (11.97% from 10%) while transport costs slowed (0.82% from 1.2%). Communication costs plunged by 12.73% in May while housing & utilities and restaurants & hotels continued in deflationary territory (at -3.4% and -1.9% respectively).

- Qatar’s industrial production declined by 3.1% mom and 5.9% yoy in Apr; this is the third consecutive month of yoy decline. Among the major sectors, mining & quarrying (with a relative weight of 82.46%) fell by 3.3% mom and 6.1% yoy.

- Manufacturing, with a 15.85% weight, also fell in Apr: down by 2.5% mom and 5% yoy. This was dragged down by multiple sectors including manufacture of basic metals (-22.5%), printing & reproduction of recorded media (-9.1%) and manufacture of cement & other non-metallic mineral products (-4.2%) among others.

- The forward-looking PMI rising to an 8-month high of 53.6 in May, on new orders and output, indicates an uptick in IP in coming months.

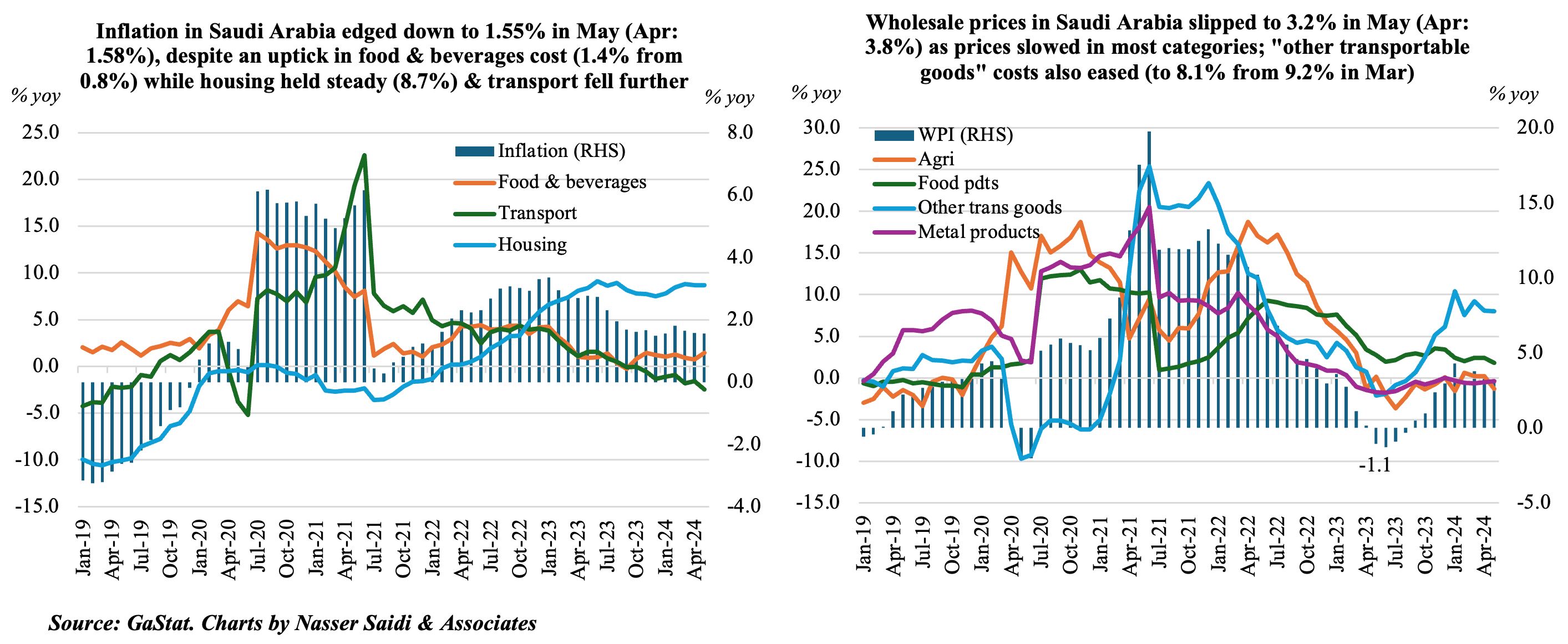

5. Consumer & wholesale price inflation in Saudi Arabia slowed further

- Consumer price inflation in Saudi Arabia eased to 1.55% yoy in May (Apr: 1.58%), though multiple categories posted slight increases including food & beverages (1.43% from 0.8%) and hotels & restaurants (2.48% from 2.0%) and education costs remained steady at 1.1% (from 1.2%). In month-on-month terms, prices rose by 0.2%, following Apr’s 0.33% gain.

- Housing costs held steady at 8.7% yoy though housing rents inched up slightly to 10.48% (from 10.42%). Recreation costs plunged further: -2.11% from Apr’s -1.4% and transport costs remained deflationary (-2.44% from -1.6%).

- Wholesale prices in Saudi Arabia slowed to 3.2% in May (Apr: 3.4%), with most categories posting declines. “Other transportable goods” category posted the highest readings (8.02% from 8.06% in Apr); within this category, prices accelerated most in basic chemicals (47%) and refined petroleum products (12.0%).

- Deflation continued in ores & minerals (-2.8% vs -2.3% in Apr) as well as in metal products, machinery & equipment (-0.42% from Apr’s -0.55%).

Powered by:

![]()