“War: Reconfiguring the Energy & Water Landscape”, Oped for the Clean Energy Business Council, 3 Apr 2026

The oped titled “War: Reconfiguring the Energy & Water Landscape” was published as part of the Clean Energy Business Council’s newsletter issued 3rd April 2026.

War: Reconfiguring the Energy & Water Landscape

Nasser Saidi

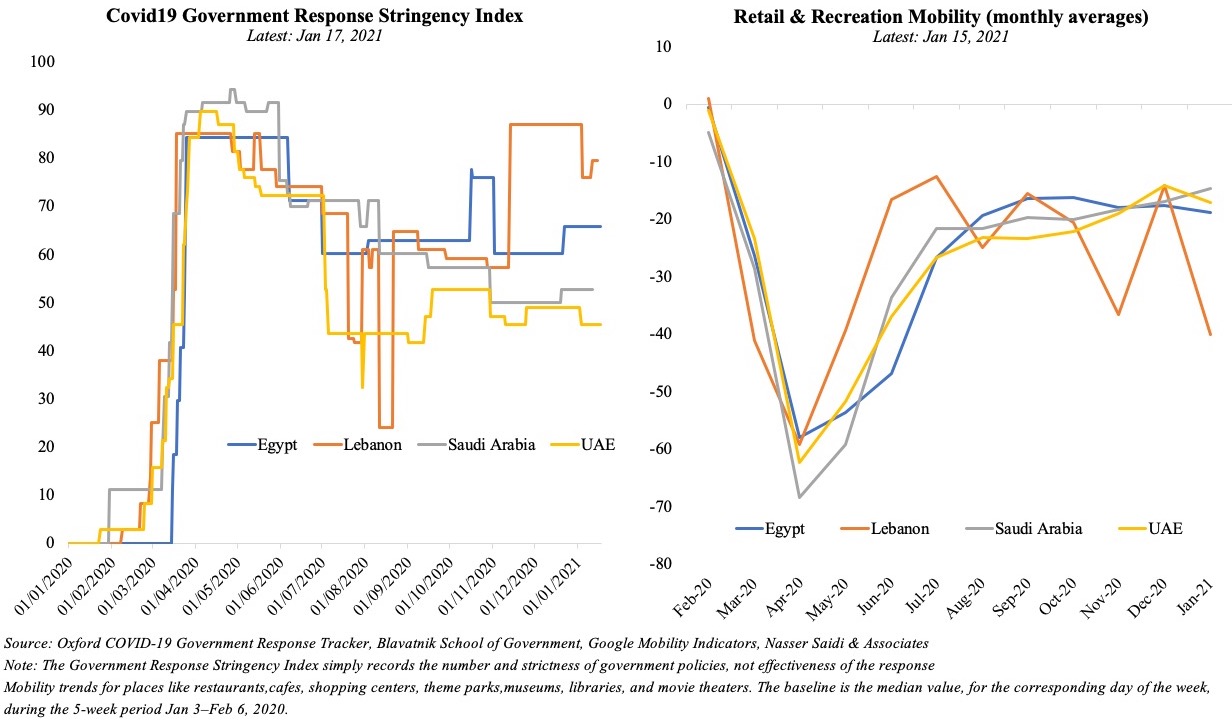

The ongoing war in the region is multifaceted, with economic, security, financial, environmental and socio-economic consequences. The effects will depend on the duration (weeks, months, years), intensity, depth and breadth (activities, countries, regional and global) of the shocks, and the extent to which core infrastructure is impacted. The shocks, and their consequences are still unfolding, with growing uncertainty as to outcomes. Already, the past year since the onset of global trade wars in April 2025, has been one of a spike and unprecedentedly high levels of economic and trade policy uncertainty, which are now being galvanised by heightened geopolitical uncertainty.

While the uncertainty is impacting both the private and public sectors, governments are pro-actively rolling out measures ranging from support for the private sector (recent announcements from the UAE central bank and Dubai Executive Council) to facilitating logistics via alternative routes given the near-closure of the Strait of Hormuz (Saudi’s Yanbu port, a Saudi-Jordan railway freight corridor, new shipping lines, expanded land transport connections etc).

The year 2026 has underlined global energy security given the disruption of traffic in the Strait of Hormuz: trade flows through Hormuz represent some 40% of global crude, 30% of LPG and 20% of LNG exports. The IEA is calling this “the largest supply disruption in the history of the global oil market”. Beyond oil, supplies of critical inputs from aluminium to helium, sulphur and fertilisers (urea, ammonia, phosphates) are being disrupted leading to price hikes and spilling over into the agricultural and food markets, vehicles, semi-conductor and AI industries.

The Resurgence of Coal Power?

While the immediate energy crisis has seen countries tighten their energy consumption belt (through higher consumption prices, rationing and by pushing work from home policies, shorter work weeks etc), it has forced some nations into a tactical retreat toward coal. Countries like India, South Korea, Thailand and Vietnam, that were heavily reliant on currently unavailable LNG from the Middle East, have been forced to ramp up coal-fired power generation to keep their grids alive; coal exporters Indonesia and Australia are prioritising domestic consumption over exports. Even China, which saw coal-fired power generation decline in 2025 (for the first time since 2015), has hit a temporary plateau as it prioritizes immediate energy security over decarbonization targets. However, coal resurgence is a stop-gap measure and not a strategy.

Renewables: From Sustainability to Energy Diversification & Independence

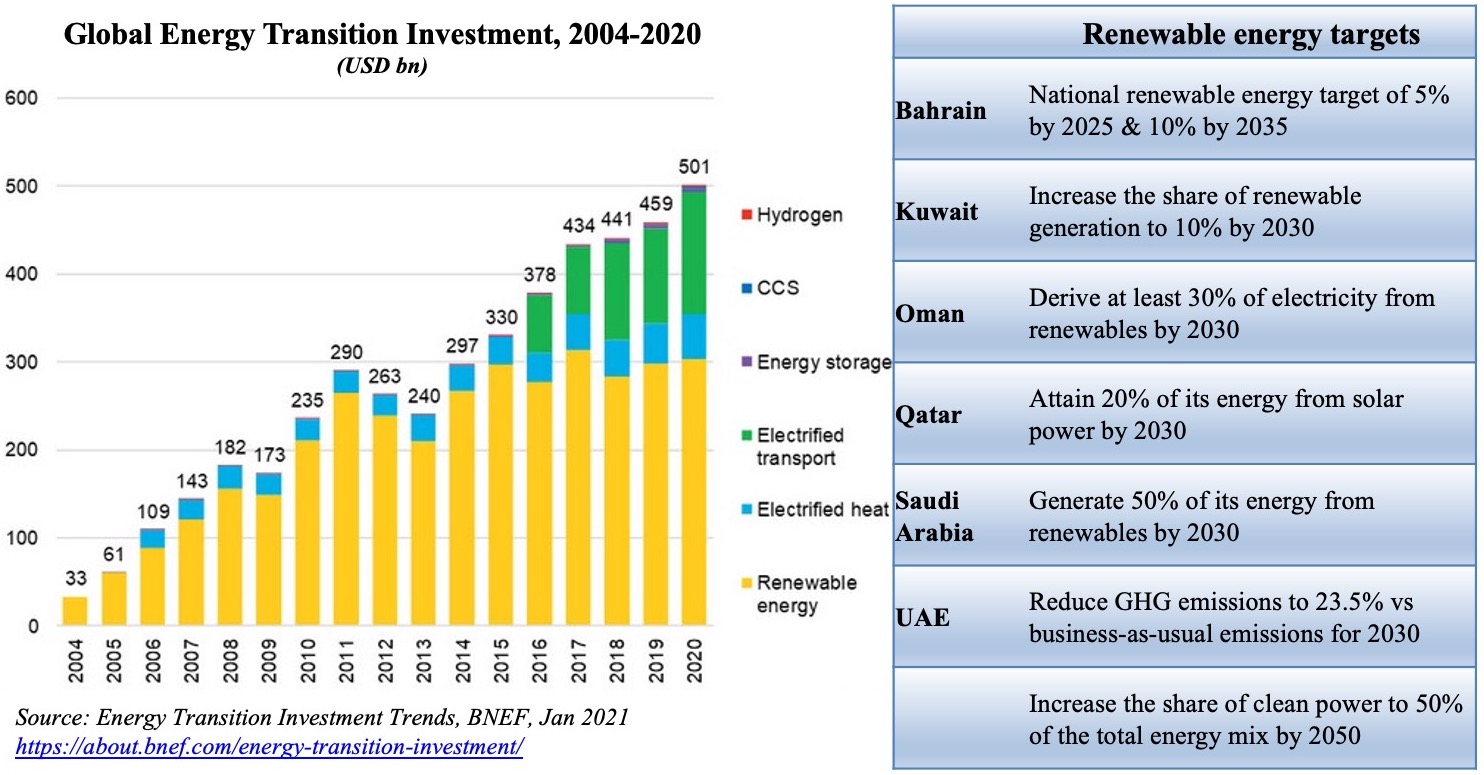

The war spurs a strong case for renewable energy (despite the Trump administration’s push away from renewables) and a new status for desalination as the region’s most critical strategic infrastructure in tandem with energy infrastructure.

In the backdrop of the Iran war, renewable energy will transition from an ESG (Environmental, Social, and Governance) goal to a pillar of energy diversification and independence. Unlike gas or oil, solar and wind energy are decentralised and locally available. Once the infrastructure is built, these assets are largely immune to maritime blockades or sanctions and the weaponization of finance that has plagued global markets. Solar and wind are now meeting nearly 20% of global power demand, proving that they are “faster to deploy and harder to disrupt” than traditional power platforms. Long term, geostrategic challenges could drive renewables to overtake coal as the world’s largest source of electricity.

The war is pushing global consumers towards EVs, solar panels and induction stoves: there is anecdotal evidence of increased EV purchases across Europe, and a 50% jump in solar panel sales in the UK since the war began. Electric motors are now up to four times more efficient than internal combustion engines and the running costs of EVs have collapsed to nearly 10 times cheaper than petrol on a per-kilometre basis. Even for corporate fleet operators and logistics giants like Maersk, switching to electric is no longer just about emissions: it is becoming integral to risk management strategy. Electric fleets provide budget predictability through fixed electricity rate contracts, bypassing the volatile “war-risk” pricing of petroleum.

Water, more strategic than oil & the GCC’s Desalination Plants

Perhaps the most significant shift in the 2026 landscape is the elevation of desalination plants as critical, strategic infrastructure.Recent strikes on desalination plants in Bahrain and Iran have exposed an existential, strategic vulnerability. Because many desalination facilities are co-located with power stations, a single successful hit can wipe out both water and electricity for major urban centres in the country. In the Gulf, countries like Kuwait and Qatar rely on desalination for more than 90% to 99% of their drinking water (in the UAE it is close to 42%). With the desalinated water also used for industry, from petrochemicals to data centres, these plants have become existential resources/ lifelines. This vulnerability turns desalination into a defence priority. Governments are no longer just expanding capacity for growth; these facilities are essential for national survival. The future depends on decentralized, solar-powered reverse osmosis plants that can operate independently of the central grid and maritime chokepoints.

Concluding Remarks

Amid the ongoing war, the GCC countries priorities should be to focus on multi-modal regional connectivity to minimise supply chain disruptions, through building renewable-powered desalination hubs and land-based trade corridors that can function even if the sea becomes a war zone.

While a short-term pivot to coal is understandable, investments should flow into more sustainable sources such as BESS (Battery Energy Storage Systems), EV infrastructure and resilient water technologies to name a few. Gulf Sovereign Wealth Funds have been investing in renewable energy projects across the globe, while pursuing ambitious net-zero goals. Masdar alone has invested in numerous renewable energy projects globally in over 40 countries across six continents with a combined capacity of more than 51GW; in 2025 alone, it made investments worth USD 15bn in RE projects. Post-war, the GCC SWFs need to invest in technologies such as renewable energy and decentralized desalination – allowing the region to no longer be held hostage by the vulnerabilities of war.

Nasser Saidi is the Chairman of the Clean Energy Business Council.

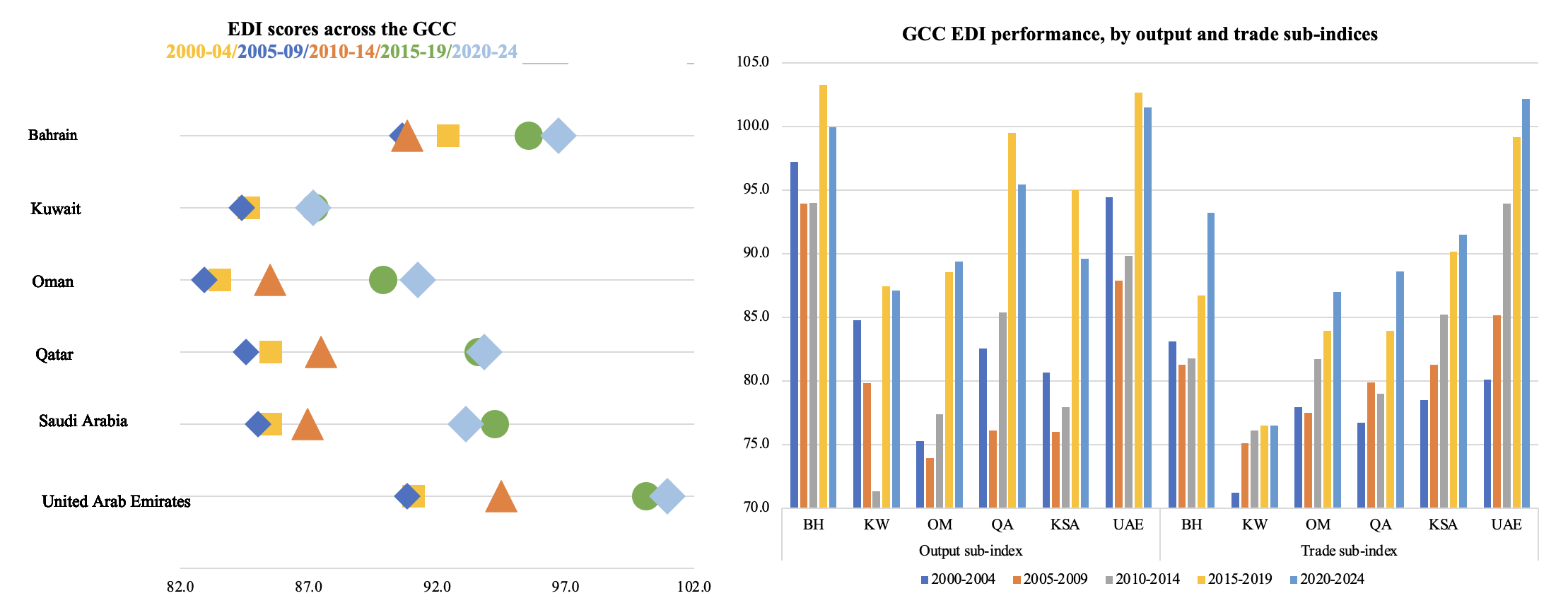

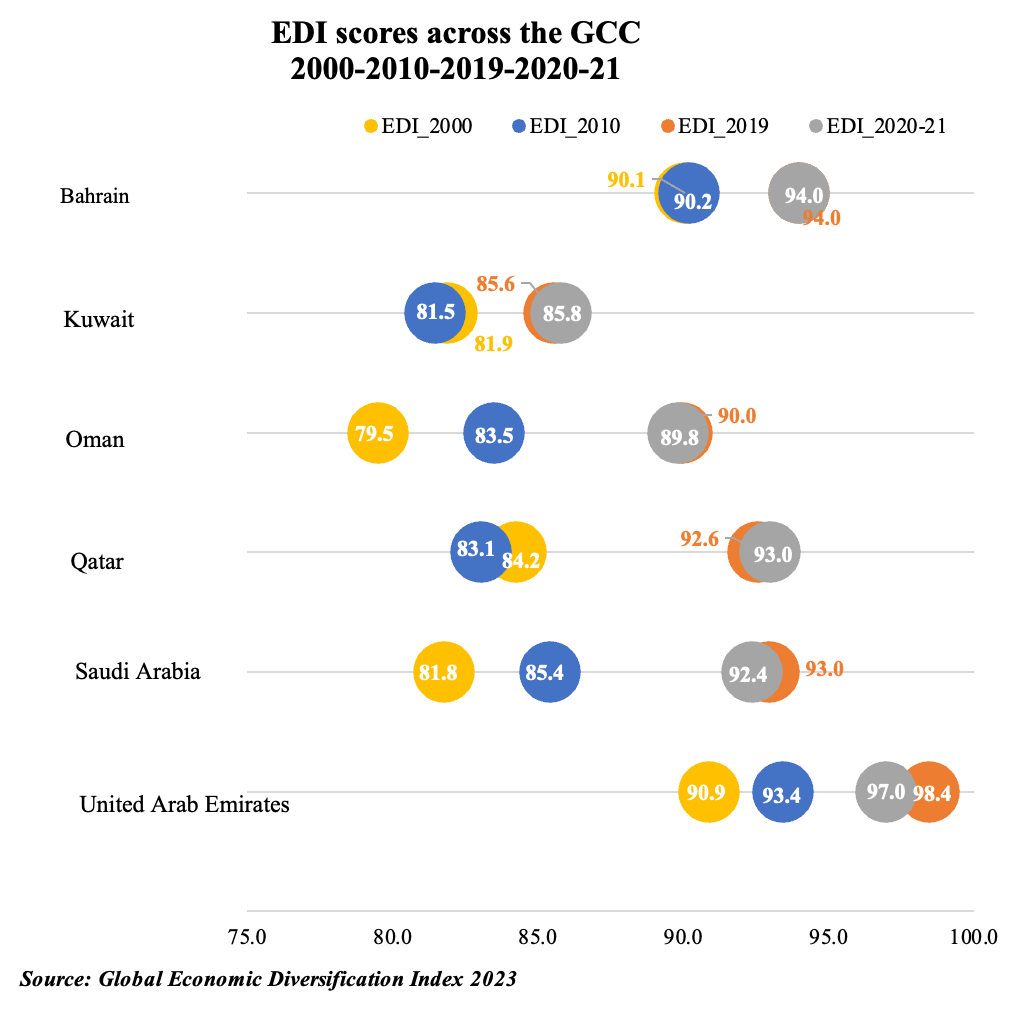

The MENA region has lagged behind its regional peers with respect to diversification yet it has caught up relatively fast. This has been supported by diversification strategies introduced by many oil-producing nations in recent years, including the introduction of non-oil taxes (excise, customs and value added taxes to name a few), alongside various liberalisation measures ranging from rights to establishment to trade facilitation measures, and improvements to hard and soft infrastructure.For resource-dependent countries, economic diversification (activity, trade and government revenue) is a strategic imperative given their demographics and job creation requirements, as well as their need to achieve sustainable development and to mitigate the macroeconomic risks of volatile commodity prices and markets. The Global EDI aims to provide guidance for countries, policy makers and analysts to design successful diversification strategies and policies, turning resource rents into an engine of growth rather than a barrier to economic development and thereby avoiding the “resource curse”.

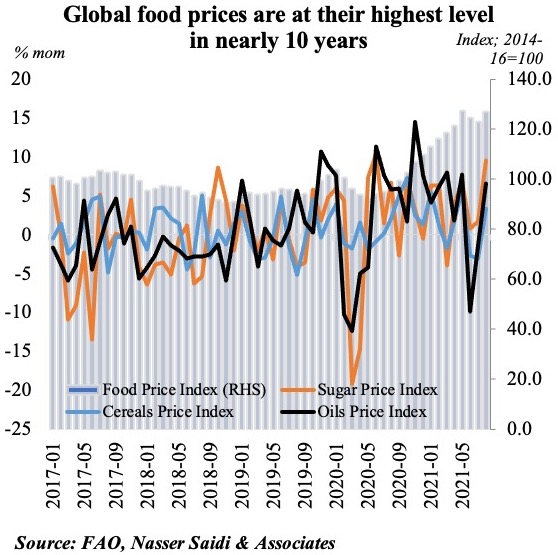

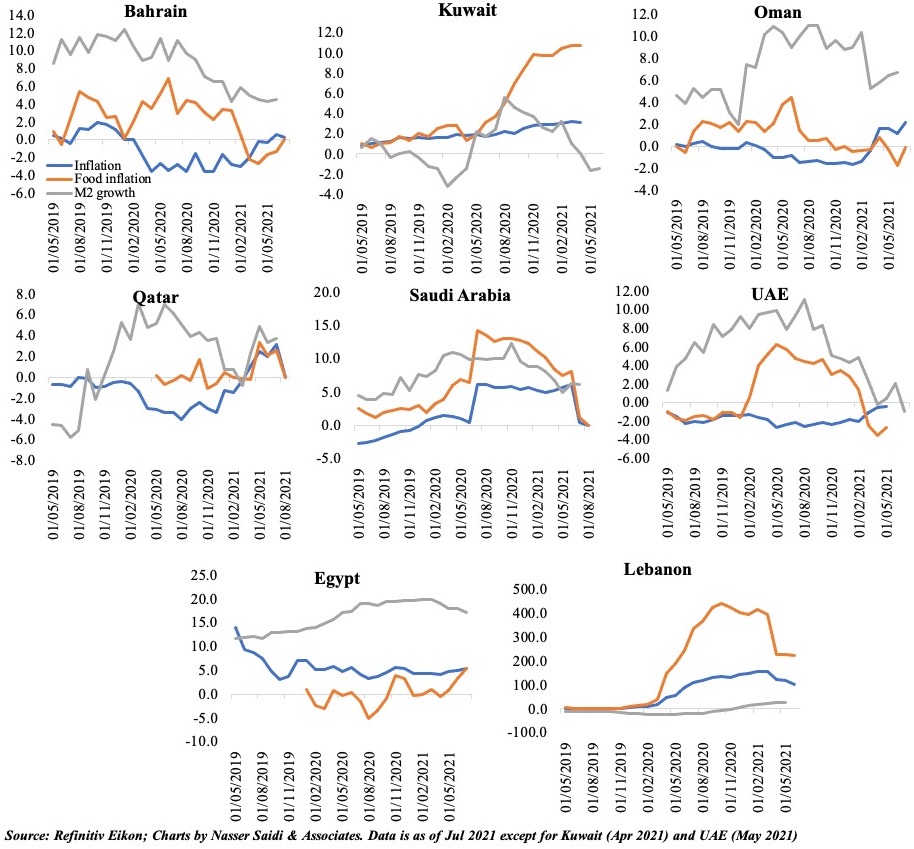

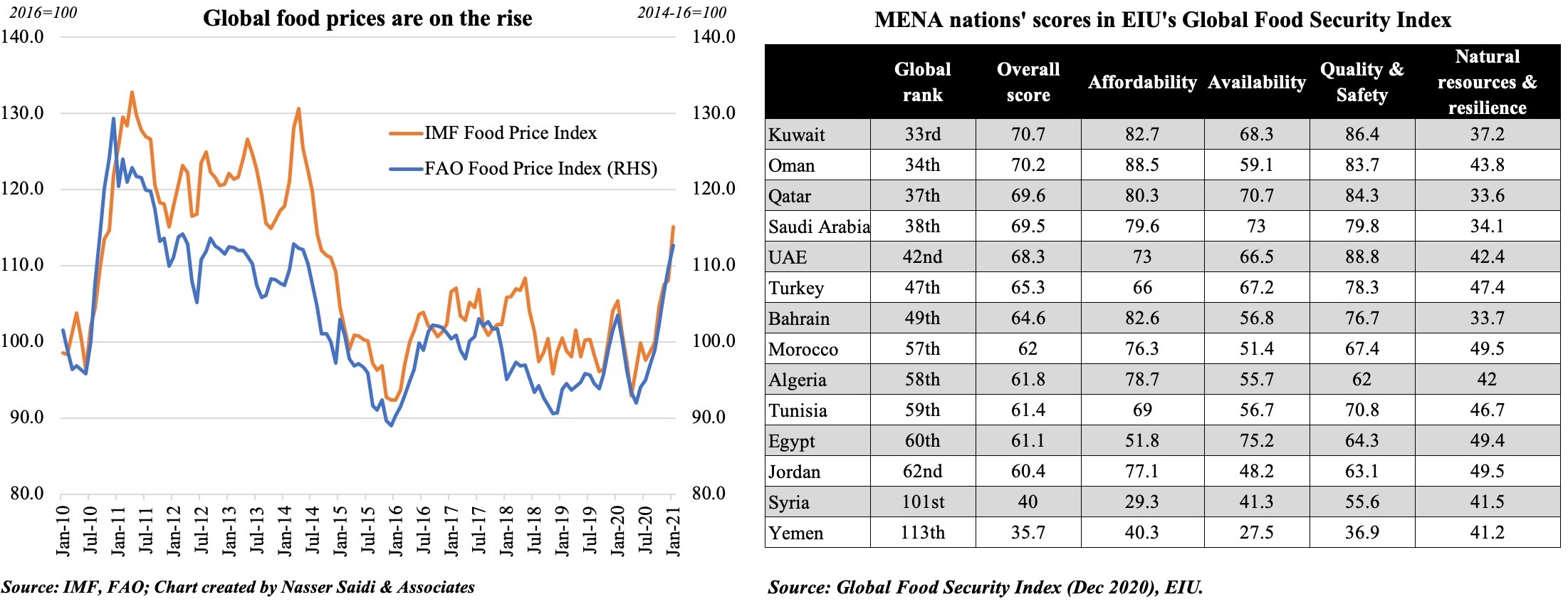

The MENA region has lagged behind its regional peers with respect to diversification yet it has caught up relatively fast. This has been supported by diversification strategies introduced by many oil-producing nations in recent years, including the introduction of non-oil taxes (excise, customs and value added taxes to name a few), alongside various liberalisation measures ranging from rights to establishment to trade facilitation measures, and improvements to hard and soft infrastructure.For resource-dependent countries, economic diversification (activity, trade and government revenue) is a strategic imperative given their demographics and job creation requirements, as well as their need to achieve sustainable development and to mitigate the macroeconomic risks of volatile commodity prices and markets. The Global EDI aims to provide guidance for countries, policy makers and analysts to design successful diversification strategies and policies, turning resource rents into an engine of growth rather than a barrier to economic development and thereby avoiding the “resource curse”. Both food and energy prices have been rising the past few months. The FAO food price index for Aug showed a 3.1% mom and 32.9% yoy increase, rebounding after 2 consecutive months of declines. Since prices had been subdued during the initial stages of the pandemic, the year-on-year surge can be associated with base effects, but the month-on-month prices have been creeping up as well. For countries highly dependent on food and other staple goods imports (especially the MENA region), the inflationary pressure will grow if this persists and also affect poorer countries disproportionately. It is worthwhile to remember that social unrest leading up to the Arab Spring a decade back came after months of rising food costs (food price inflation in Egypt had hit ~19%)!

Both food and energy prices have been rising the past few months. The FAO food price index for Aug showed a 3.1% mom and 32.9% yoy increase, rebounding after 2 consecutive months of declines. Since prices had been subdued during the initial stages of the pandemic, the year-on-year surge can be associated with base effects, but the month-on-month prices have been creeping up as well. For countries highly dependent on food and other staple goods imports (especially the MENA region), the inflationary pressure will grow if this persists and also affect poorer countries disproportionately. It is worthwhile to remember that social unrest leading up to the Arab Spring a decade back came after months of rising food costs (food price inflation in Egypt had hit ~19%)!

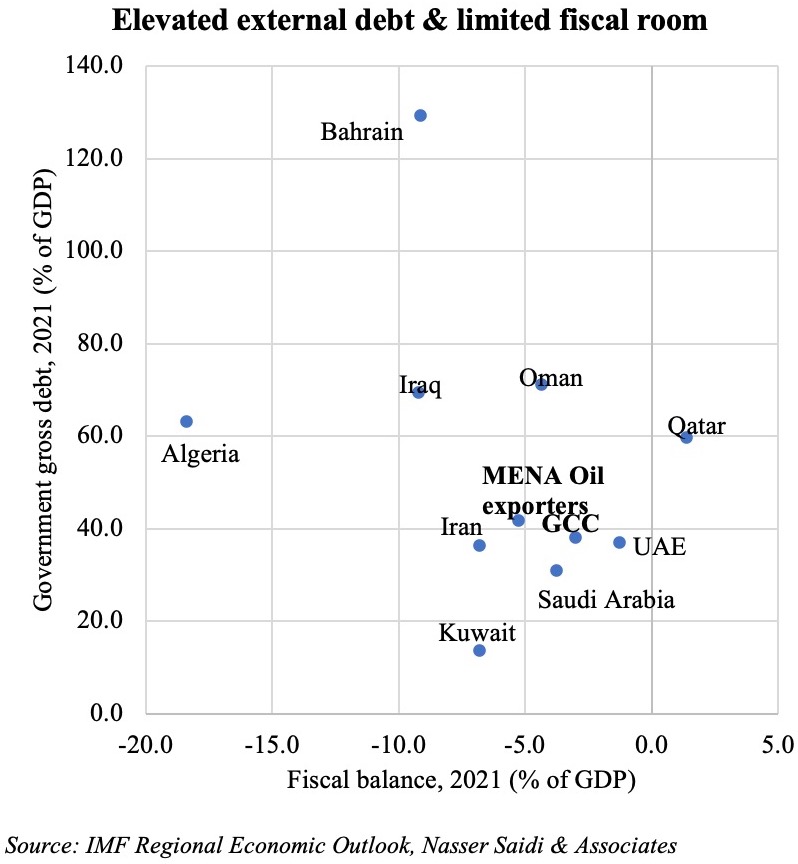

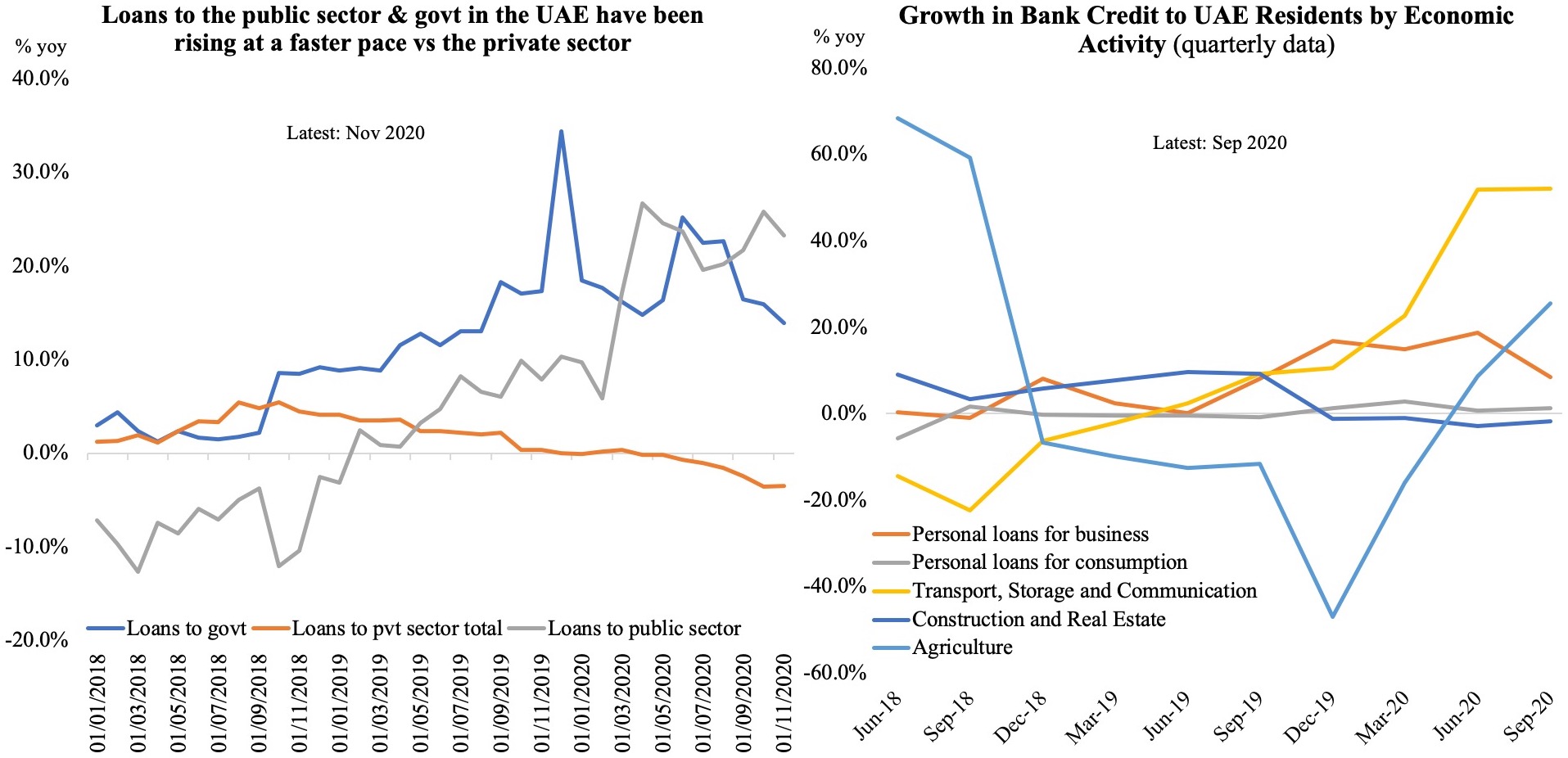

Public and external debt have risen significantly for the median emerging market economy, reaching 59 and 44% of GDP, respectively, in 2020, and gross financing needs are projected to stay above 10% of GDP in 2020–21, according to

Public and external debt have risen significantly for the median emerging market economy, reaching 59 and 44% of GDP, respectively, in 2020, and gross financing needs are projected to stay above 10% of GDP in 2020–21, according to  In the MENA region, almost half the nations have gross government debt above 70% of GDP and one in 4 had public gross financing needs above 15% of GDP by end-2019. The pandemic led to a significant loss in revenues (both oil and non-oil) and though international financial markets were tapped, domestic financing increased. According to the IMF, governments in Egypt, Jordan, and Tunisia covered more than 50% of their public gross financing needs with domestic bank financing in 2020. Such bank exposure to the public sector could also crowd out the private sector at a time when a private activity push is required for higher economic growth and job creation. A surge in inflation can lead to a reduction in the real value of domestic debt – Lebanon is a good example, but the sharp currency depreciation makes the debt burden unsustainable.

In the MENA region, almost half the nations have gross government debt above 70% of GDP and one in 4 had public gross financing needs above 15% of GDP by end-2019. The pandemic led to a significant loss in revenues (both oil and non-oil) and though international financial markets were tapped, domestic financing increased. According to the IMF, governments in Egypt, Jordan, and Tunisia covered more than 50% of their public gross financing needs with domestic bank financing in 2020. Such bank exposure to the public sector could also crowd out the private sector at a time when a private activity push is required for higher economic growth and job creation. A surge in inflation can lead to a reduction in the real value of domestic debt – Lebanon is a good example, but the sharp currency depreciation makes the debt burden unsustainable.

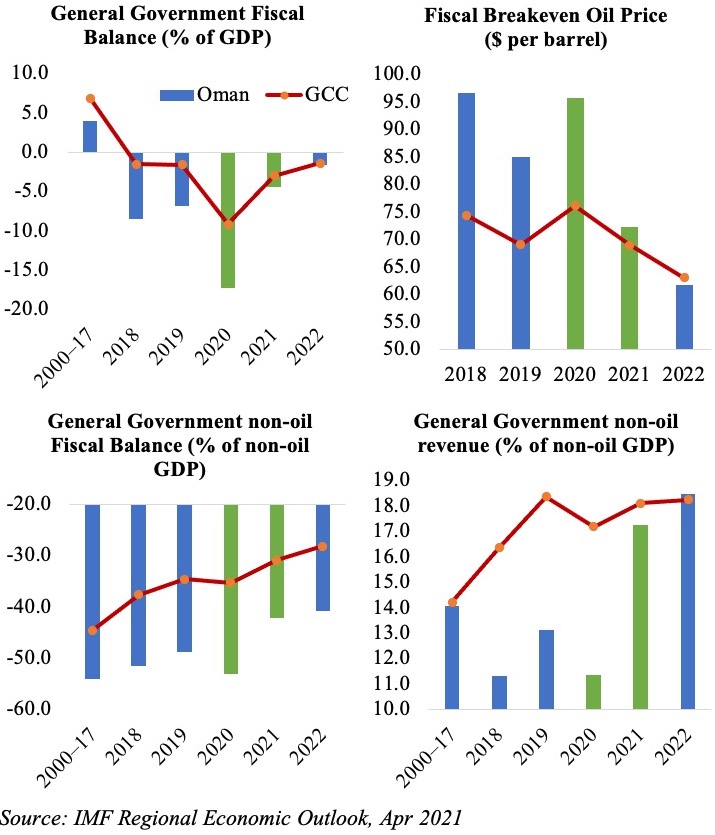

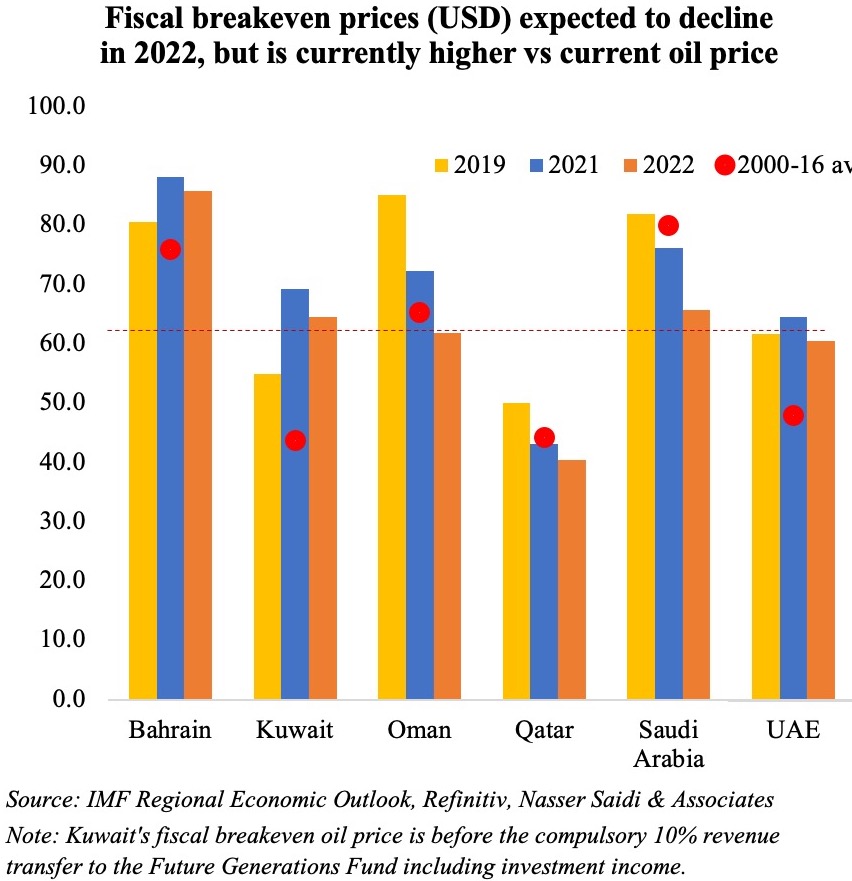

However, policy measures introduced to support the economy during the pandemic is creating immense fiscal strain. Fiscal deficits widened to 10.1% of GDP in 2020 in the MENA region from 3.8% in 2019. It was severe in the GCC as well: fiscal deficit widened to 7.6% of GDP last year (2019: -1.6%), as the impact was from both lower oil and non-oil revenues. The fiscal breakeven price this year ranges from a high USD 88.2 in Bahrain to a low USD 43.1 in Qatar. While, it is expected to decline across the board next year, it still remains higher than the current oil price levels for most nations. Given new rounds of restrictions and with oil demand not yet at pre-pandemic levels, the OPEC+’s recent decision to roll back production cuts are likely to depress oil prices. As real oil prices trend downward, fiscal sustainability becomes increasingly vulnerable.

However, policy measures introduced to support the economy during the pandemic is creating immense fiscal strain. Fiscal deficits widened to 10.1% of GDP in 2020 in the MENA region from 3.8% in 2019. It was severe in the GCC as well: fiscal deficit widened to 7.6% of GDP last year (2019: -1.6%), as the impact was from both lower oil and non-oil revenues. The fiscal breakeven price this year ranges from a high USD 88.2 in Bahrain to a low USD 43.1 in Qatar. While, it is expected to decline across the board next year, it still remains higher than the current oil price levels for most nations. Given new rounds of restrictions and with oil demand not yet at pre-pandemic levels, the OPEC+’s recent decision to roll back production cuts are likely to depress oil prices. As real oil prices trend downward, fiscal sustainability becomes increasingly vulnerable.

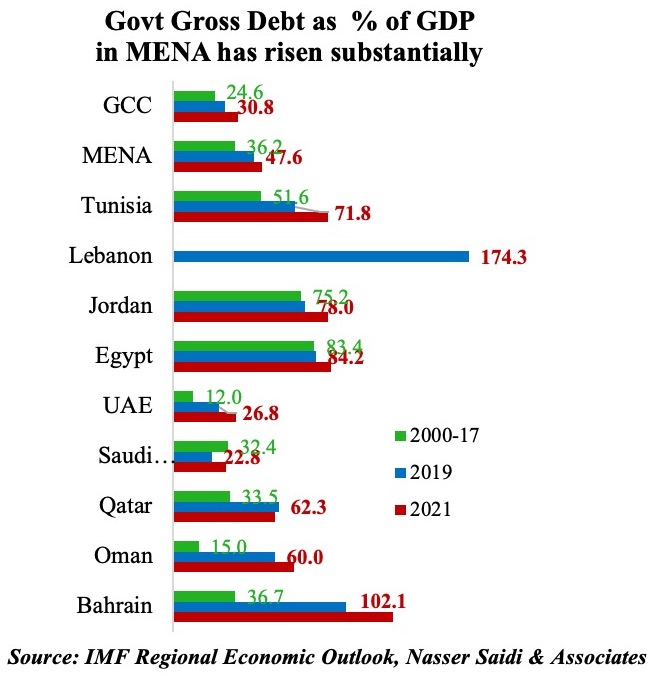

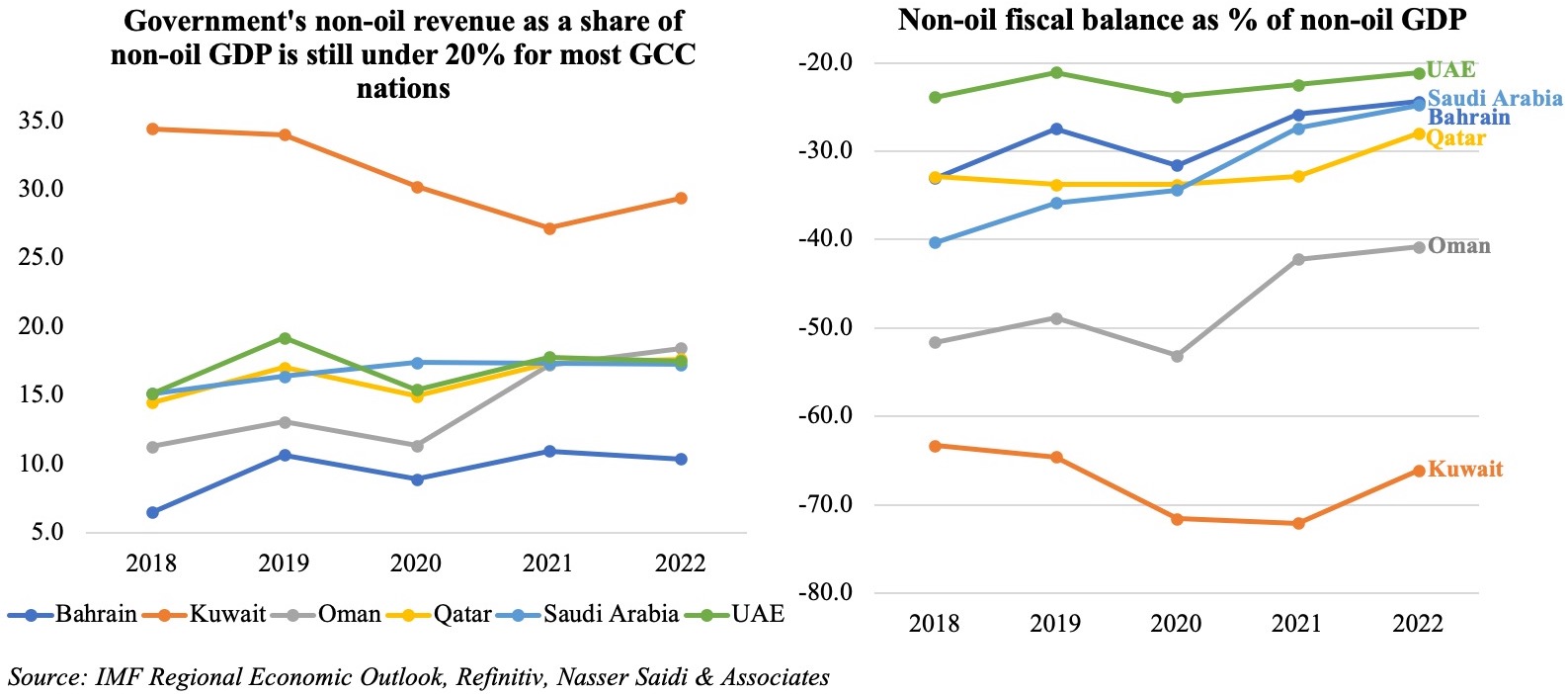

Higher deficits and negative economic growth resulted in governments resorting to multiple financing options: borrowing from commercial banks, tapping international and regional markets (bond issuances, commercial loans) as well as drawing down from international reserves at the central banks/ sovereign wealth funds. Government debt levels increased to 56.4% and 41% in the MENA and GCC regions last year. Though it is forecast to fall slightly this year, it still remains higher than the 2000-17 average of 36.2% and 24.6% respectively. The IMF estimates financing needs in the MENA to touch USD 919bn for this year and next. Public-financing requirements were likely to stay above 15% of GDP in most parts of the region through end-2022.

Higher deficits and negative economic growth resulted in governments resorting to multiple financing options: borrowing from commercial banks, tapping international and regional markets (bond issuances, commercial loans) as well as drawing down from international reserves at the central banks/ sovereign wealth funds. Government debt levels increased to 56.4% and 41% in the MENA and GCC regions last year. Though it is forecast to fall slightly this year, it still remains higher than the 2000-17 average of 36.2% and 24.6% respectively. The IMF estimates financing needs in the MENA to touch USD 919bn for this year and next. Public-financing requirements were likely to stay above 15% of GDP in most parts of the region through end-2022.

Middle Eastern and Gulf Cooperation Council (GCC) economies are heading toward a recession in 2020 as a result of the COVID-19 pandemic, collapsing oil prices, and the unfolding global financial crisis.