The other challenge is whether the banking system has sufficient liquidity to make repayments to depositors. “The short answer is ‘no’,” said Nasser Saidi, a former economy minister and deputy governor of Lebanon’s central bank. He said it was impossible to know if banks had sufficient liquidity without a forensic audit of the lenders and the BDL.

Additionally, the draft law promises to create future liabilities without clearly specifying how these will be financed. “There is a great deal of vagueness and opaqueness in the draft law. There is uncertainty: who does what, who assesses the amount of losses, who administers etc, which opens the process to potential litigation and legal uncertainty,” Mr Saidi said.

A major issue with the draft law is that it does not add new liquidity into the banking system, but rather focuses on the balance sheets of the commercial banks and the BDL. “This is a flawed static approach. You need both solvency and liquidity and long-term sustainability requiring a dynamic analysis,” said Mr Saidi.

New capital and financial resources will need to be injected in the banks to provide credit and finance to stabilise and restore economic growth.

“This is not a zero-sum game,” he added. “The risk is that absent resolution of uncertainties, the restructuring process will end up being a failed, negative-sum game – a situation in which the total losses of all participants exceed the total gains, resulting in a net loss for everyone involved, that will not restore trust to revive a cash-based, informal economy.”

Comments on “The ebb and flow of Saudi Arabia’s US Treasury strategy” in Arab News, 25 Oct 2025

Nasser Saidi, founder and president of Nasser Saidi & Associates, a specialized economic and financial advisory services company, echoed this perspective, emphasizing that the decision is “primarily taken by the Saudi Central Bank, keeping in mind its strategic goals of currency stability, directed partly by the need to hold US dollar as part of international reserves to maintain the dollar peg and liquidity and safety.” For Saidi, who served as Lebanon’s minister of economy and trade and minister of industry from 1998 to 2000, US Treasuries are a critical pillar of stability, as “holding treasuries allows Saudi Arabia to meet its international payment obligations — finance imports, service external debt, portfolio, and capital flows — provide a buffer against oil revenue shocks, while also generating a steady, low-risk stream of income.”

Saidi pointed to multiple drivers behind these shifts, noting that the rise until September 2024 reflected the Saudi Central Bank, known as SAMA, capitalizing on higher US interest rates, supported by strong oil revenues from the preceding period.

He added that the drop to a six-year low of $108 billion in June 2023 followed a significant transfer of funds to the Public Investment Fund, and the subsequent rise reflected Aramco dividend transfers, which “would have some impact on inflows of US dollar into the central bank in 2024.”

Speaking to Arab News, Saidi explained that the decline to $126.4 billion by February “is likely a combination of factors – expectations that interest rates would stay higher for longer plus a soft landing in the US, portfolio rebalancing away toward higher-yield investments in the backdrop of lower oil production and prices, SAMA withdrawing to meet domestic spending needs / managing liquidity in the banking system,” adding that after a return to stabilization was seen.

For Saidi, the pattern underscores that “SAMA acts as both the traditional central bank, and also actively manages its reserve holdings to accommodate funding needs as per Vision 2030, mainly via the PIF.”

The interplay between SAMA and the PIF is central to understanding the bigger picture. Saidi explained that their mandates are different as SAMA’s role is to provide currency, banking, and financial market stability, dictating conservative policies.

Saidi emphasized that US Treasuries will likely remain the anchor of SAMA’s portfolio due to the dollar peg, but the PIF’s strategy points to greater diversification in the non-reserve segment, with more aggressive investments in private equity, infrastructure, and renewables, as well as artificial intelligence, data centers, technology, and other asset classes.

“Saudi [Arabia] is unlikely to fully abandon the US dollar, despite de-dollarization talks, but expect more diversification and the prospect of a greater role for the Petro-Yuan, given the growing trade and investment links with China, increased holdings in other currencies for trade purposes, and increased holding of gold as a hedge,” Saidi, who has also served as vice governor of the Central Bank of Lebanon for two successive mandates, said.

He added that people should be prepared for the rollout and increased use of a central bank digital currency, a digital riyal, for cross-border transactions as well in the near future.

Comments on “Can Lebanon’s new central bank governor break the cycle of economic crisis?” in Arab News, 31 Mar 2025

Echoing the prime minister’s apprehensions is Nasser Saidi, a former Lebanese economy minister and central bank vice governor, who raised concerns about the selection process for the new central bank chief, warning that powerful interest groups may have too much influence.

He told the Financial Times that the decision carried serious consequences for Lebanon’s economic future, saying that one of Souaid’s biggest challenges will be convincing the world to trust the nation’s banking system enough to risk investing in its recovery.

“The stakes are too high: You cannot have the same people responsible for the biggest crisis Lebanon has ever been through also trying to restructure the banking sector,” said Saidi, who served as first vice governor of the Banque du Liban for two consecutive terms.

“How are we going to convince the rest of the world that it can trust Lebanon’s banking system, and provide the country with the funding it needs to rebuild (after the war)?”

Lebanese economist Saidi said that the IMF “quite correctly and wisely” demanded comprehensive economic reforms.

In a March 14 interview with BBC’s “World Business Report,” he said that the government must address fiscal and debt sustainability, restructure public debt, and overhaul the banking and financial sector.

But hurdles remain. Saidi added that while Lebanon “has a government today that I think is willing to undertake reforms, that does not mean that parliament will go along.”

Lebanon also needs political and judicial reform, including an “independent judiciary,” he added.

Nevertheless, Saidi told the BBC that Lebanon, for the first time, has “a team that inspires confidence” and has formed a cabinet that secured parliament’s backing. Despite this positive step, Lebanon must still address structural failures in its public institutions, rooted in decades of opacity, fragmented authority and weak accountability.

Saidi highlighted the broader challenges Lebanon faces, cautioning that without financing for reconstruction, achieving socioeconomic and political stability will remain elusive.

“If you don’t have financing for reconstruction, you’re not going to have socioeconomic stability, let alone political stability,” he said.

“There has to be a willingness by all parties to go along with the reforms,” he added, highlighting that this is where external support is crucial, particularly from Saudi Arabia, the UAE, France, Europe and the US. Saidi said that support must go beyond helping bring the new government to power — it must include assistance, especially in terms of security.

Comments on Lebanon’s next central bank lead, FT, 26 Mar 2025

Dr. Nasser Saidi commented on the choice of Lebanon’s next central bank governor in the FT article titled “Lebanon closes in on next central bank head” published on 26th March 2025.

Nasser Saidi, a former minister and BdL vice-governor, warned that powerful interest groups were wielding too much influence over the selection process. “The stakes are too high: you cannot have the same people responsible for the biggest crisis Lebanon has ever been through also trying to restructure the banking sector,” he said.

“How are we going to convince the rest of the world that it can trust Lebanon’s banking system, and provide the country with the funding it needs to rebuild [after the war]?”

“What does Lebanon’s new government mean for its future?”, Chatham House webinar, 6 Mar 2025

Dr. Nasser Saidi participated in the panel discussion titled “What does Lebanon’s new government mean for its future?” hosted by Chatham House on March 6th, 2025.

The webinar examines the new government’s likely approach to political and economic reform, Lebanon’s evolving position in regional and international affairs, and the impact of U.S. policy on the country’s future.

Hope and optimism follow the arrival of a new prime minister and president

The nomination of Nawaf Salam as Lebanon’s prime minister under President Joseph Aoun, following more than two years of political vacuum, marks a turning point for the country.

This moment has the potential to be as transformative as the 1989 Taif agreement, which ended the civil war and restored political stability.

A major factor behind the developments in Lebanon is the significant shift in regional dynamics. This has been driven by the war in Gaza, the collapse of the Assad regime in Syria, the severe degradation of Hezbollah’s capabilities and the apparent collapse of Iran’s “axis of resistance”.

Together, these events have created a powerful impetus for change.

For the leading powers in the GCC – Saudi Arabia and the UAE – this moment provides an opportunity to displace Iran from Lebanon, Iraq and Syria while reasserting their own influence. Both regional and international stakeholders share an interest in promoting stability.

Lebanon’s political landscape has been historically paralysed by internal fragmentation. Now, at last, the country’s political class, plagued by a lack of credibility, incompetence and failure to address Lebanon’s many crises or implement long-overdue reforms, is passing on the baton.

But Salam and Aoun inherit a heavy legacy.

Since the Arab Spring in 2011, Lebanon has battled stalled institutional reforms, unsustainable fiscal and monetary policies and overvalued exchange rates. These factors contributed to significant deficits in the government budget and current account, along with massive debt accumulation.

The country’s central bank, the Banque du Liban, allegedly ran a Ponzi scheme for many years during the tenure of Riad Salameh, who was its governor for three decades. He has denied all wrongdoing and the notion that the bank was operating a Ponzi scheme.

The bank’s activities contributed significantly to Lebanon’s economic collapse, depleting international reserves, sparking a 99 percent depreciation of the exchange rate, hyperinflation, a collapse of the banking system and one of the deepest financial crises in the country’s history.

Central bank losses exceeded 200 percent of GDP. Lebanon became a cash – and increasingly dollarised – economy. The polycrisis (economic, monetary and financial, institutional, security, political and governance), along with the Beirut Port explosion and the Israel-Hezbollah war, turned Lebanon from a fragile state into a failed one.

Despite the long road ahead for Aoun and Salam, we have reasons for optimism.

The president’s inaugural speech encapsulated much promise for a new Lebanon. There were strong messages on political reform, rebuilding the state and its institutions, focusing on judicial and administrative reform, the rule of law, accountability and fighting endemic corruption.

Institutional and judicial reform will be complemented by a national anti-corruption drive and transparency initiatives while demanding accountability for multiple crises and destruction.

President Aoun’s political vision mirrors that of former President Fouad Chehab (1958-1964), who introduced reforms and built state institutions. With extensive military and security experience, President Aoun is adept at establishing domestic and external national security.

A packed agenda starts with forming a reform-centric, cohesive, competent and effective cabinet. The critical portfolios are justice, foreign affairs, defence and internal affairs, as well as finance.

With the Israel-Lebanon ceasefire agreement set to expire on January 26, the immediate need is to negotiate a permanent ceasefire to restore internal security and stability and enable the return of the displaced to the south, Bekaa and other areas.

Macroeconomic stabilisation and growth require fiscal consolidation and tax reform, modernising and digitising all government functions, administrative reform (over half of director-level posts are vacant), downsizing the bloated public sector, restructuring and effecting good governance of the state-owned enterprises (SOEs) responsible for public services.

An independent National Wealth Fund should be established to professionally manage all SOEs, commercial public assets and future oil and gas revenues.

Credible monetary reform requires a strong, professional and politically independent central bank. Monetary policy should be directed at controlling inflation and accompanied by a flexible exchange rate regime.

Additionally, a comprehensive overhaul of Banque du Liban’s governance structure is necessary to implement meaningful change and restore confidence.

To make the BDL accountable, a new governor (and deputy governors by June 2025) and radical changes to governance are required. The Banking Control Commission of Lebanon, the Special Investigation Commission and the Capital Markets Authority should also be independently governed institutions.

Furthermore, an independent Bank Resolution Authority must restructure the banking system based on recapitalisation (starting with existing shareholders), mergers and acquisitions, and bail-ins of large depositors to maximise deposit recovery.

The implementation of political reforms, a comprehensive restructuring agenda, and institutional and structural changes will pave the way for a revised International Monetary Fund programme and renewed engagement with the GCC.

These efforts can support Lebanon’s reintegration into the Arab world, facilitate funding for redevelopment and address substantial reconstruction needs, estimated at approximately $25 billion.

In essence, this is a historic opportunity for Lebanon, the GCC and the wider region.

Dr Nasser Saidi is the president of Nasser Saidi and Associates. He was formerly chief economist and head of external relations at the DIFC Authority, Lebanon’s economy minister and a vice governor of the Central Bank of Lebanon

“Time to address Lebanon’s crippling banking crisis”, guest article for Arab Banker, Autumn 2024

Lebanon has been mired in economic crisis for almost five years. A combination of acute negligence and mismanagement on the part of the government, the central bank and key institutions culminated in a series of economic and political crises that have left the banking sector on its knees and more than three-quarters of the population living in poverty.

In the guest article for Arab Banker,Dr. Nasser Saidi, founder and president of Nasser Saidi & Associates, and Alia Moubayed, emerging markets economist, analyse how the crisis unfolded and chart a proposed roadmap to recovery.

Weekly Insights 29 Sep 2020: Supporting the recovery of UAE’s private sector (focus on SME finance)

[This is an edited version of the post issued originally on 29th Sep; Table 1 & related text have been updated]

Supporting the recovery of UAE’s private sector: focus on SME finance

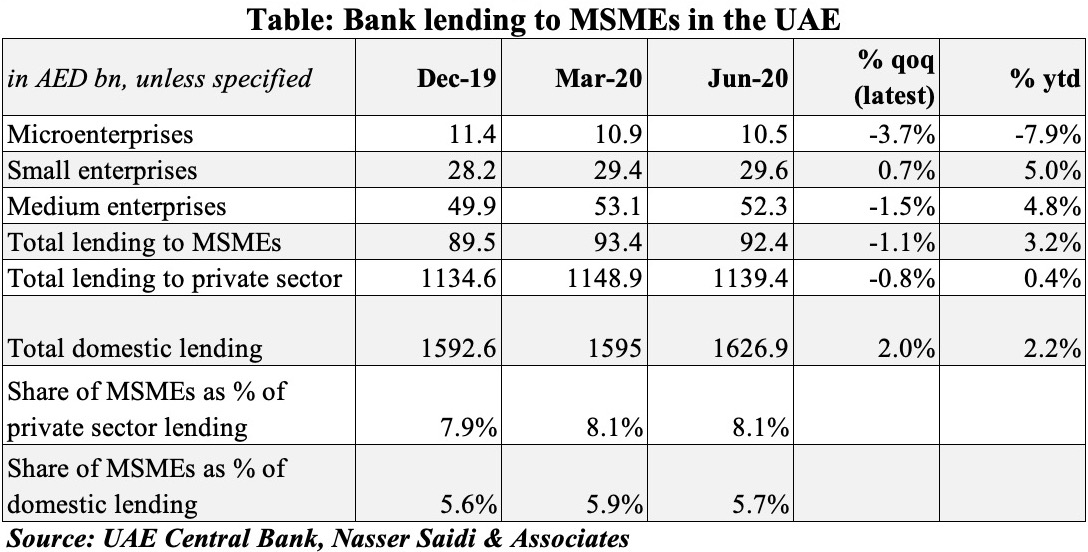

To support the UAE economy in the backdrop of Covid19, the central bank (since Mar 2020) has rolled out a number of measures including liquidity injection via loosening of banks’ capital requirements, loan repayment deferrals and the Targeted Economic Support Scheme (TESS) among others. According to the UAE central bank, as of end-Jul, banks and financial institutions had availed AED 44.72bn worth of interest-free loans (89.44% of total) as part of the TESS facility. It needs to be highlighted that banks used close to 95% of these funds towards postponing loan payments for the affected sectors. It was also disclosed separately that 300k individuals, 10k SMEs and more than 1500 private sector firms had used the economic stimulus.

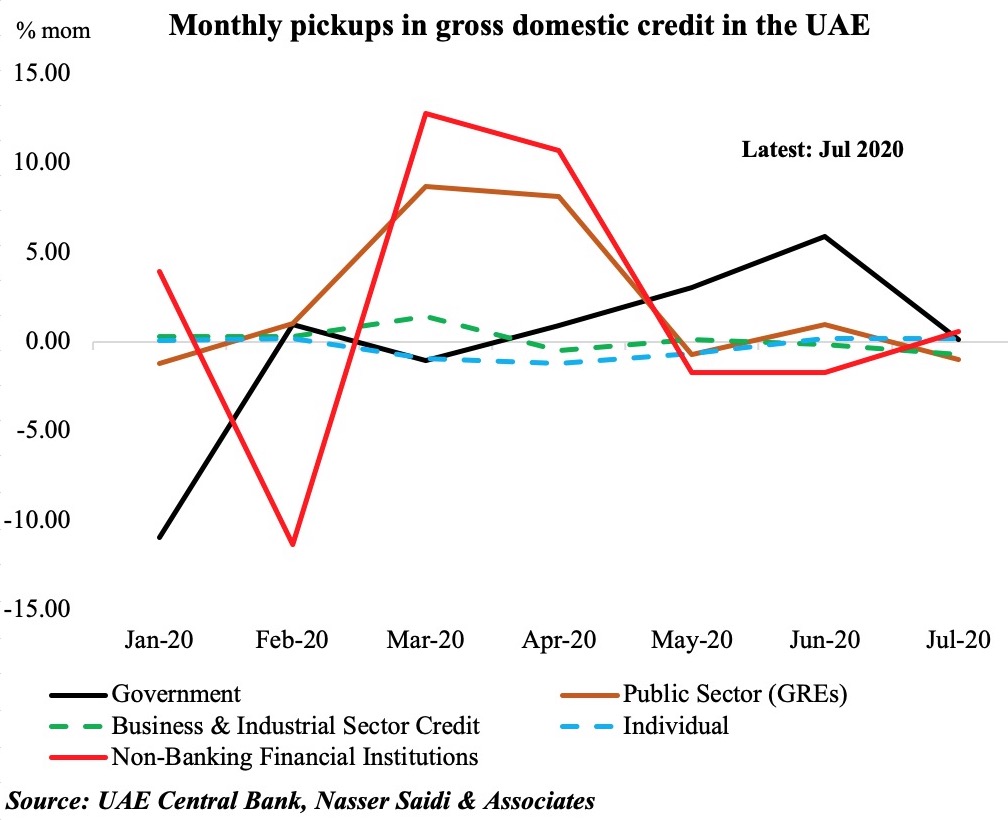

The latest data from the UAE central bank shed some light on the broader credit movements: the accompanying chart shows the monthly changes in gross domestic credit. The dotted lines are credit to businesses and individuals (the private sector) which show no substantial increases – in fact, it increased by an average 0.9% year-to-date (ytd) for businesses and dropped by 2.1% ytd for individuals. The uptick in lending to the public sector (government related entities) and government have been discussed previously here and here, but the non-bank financial institutions (which include private equity & venture capital firms, other investment firms, alternative asset managers, insurance firms and others) has also witnessed a 11.8% rise in credit ytd. There is not much visibility of the activities of NBFIs in the UAE (in terms of publicly available data), and it is not clear if the SME customer segment, important for recovery, was catered to (via consumer finance, SME financing & credit card products, to name a few).

However, at the risk of sounding like a broken record, the question is whether the package has achieved its goal of supporting the economy or whether it resulted in a crowding out of the private sector (businesses and individuals) in favour of the government, public sector & also the financial institutions? The UAE central bank’s latest quarterly report does mention that MSMEs (Micro, Small and Medium Enterprises) benefitted from the economic package – highlighting the 10.4% yoy increase in lending in Q2 this year. But, at the end of the day, share of SME lending in total domestic lending was at 5.7% in Q2 (Q2 2019: 5.6%), lower than 5.9% share as of end-Q1.

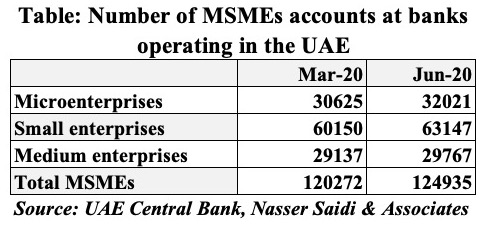

Additional data is beneficial: the tables below provide more details of bank lending to the MSMEs, segregated by micro, small and medium enterprises[1]. Within the MSME segment, as of end-Q2, the largest share of loans was disbursed to medium-sized firms (56.6%) and close to 1/3-rd to the small enterprises.

The number of MSMEs in the UAE have increased by 3.9% qoq to 124,935 as of end-Jun – not surprising given the central bank’s mandate of reduced duration for opening new SME accounts (all banks need to open accounts for SME customers within a maximum timeframe of two days, provided documentation and AML/CTF obligations are met). The number of accounts in the micro- and small segments increased by 4.6% and 5% qoq in Q2. Nevertheless, if we consider the amount disbursed per firm, medium enterprises pocketed AED 1.76mn in Q2: this is 3.7 times the amount disbursed per small firm and more than 5.3 times the amount disbursed to microenterprises.

The results are quite eye-opening, but not surprising (unfortunately): the GREs have benefitted in terms of the pace of overall domestic lending during the Covid19 period (remember that many of these firms are part of the sectors most affected by the pandemic!) and while lending to the SMEs has been dismal, within the SMEs, the medium-sized firms have benefitted the most. Considering how significant SMEs are to the UAE[2], it is imperative that financial institutions support them to bring the economy back on track. Some of the policies rolled out by the central bank had a 6-month deadline, and since no announcements have been made (yet) regarding extensions, anecdotal evidence points to banks winding down loan repayment deferrals and similar policies (for businesses/ individuals).

With the economy not yet back on the pre-Covid19 track, and the central bank’s own call of a 4.5% decline in non-oil GDP this year, targeted policy stimulus measures need to continue. With rising indebtedness of both individuals (due to job losses or pay cuts) and businesses (directly and indirectly affected by Covid19), there are likely to be spillovers into the financial sector via rising non-performing loans.

Furthermore, as companies wind down operations in the near- to medium-term, nascent insolvency and bankruptcy frameworks in the UAE are likely to be tested. According to the World Bank Doing Business 2020 report’s resolving insolvency sub-category, the UAE’s recovery rate was 27.7 cents on the dollar (vs OECD high income nation’s average of 70.2 and MENA average of 27.3), at a cost of 20% of the estate (vs 9.3 in OECD and 14% in MENA), taking 3.2 years to resolve (vs OECD’s 1.7 and MENA’s 2.7)[3]. However, the strength of the insolvency framework – given recent but untested legislation – stood at an impressive 11 (out of a total score of 16; compares to the OECD average of 11.9 and higher than MENA’s 6.3).

Support of the private sector is critical for economic recovery

To provide adequate ongoing backing to the private sector (including the SMEs) is essential. What policy measures need to be in place? (a non-exhaustive list)

Banking sector continues to support the private sector via reduced bank charges and fees, reduction in minimum balance requirements, zero-interest instalment plans etc.; of course, banks’ compliance/regulatory departments need to ensure that firms they lend to follow practices of good financial reporting and governance.

Limited funding to SMEs from the banking sector is likely to continue, given the current status of opaque information/ reporting/ data. Lack of collateral and issues of transparency are oft-cited constraints to SME lending in the region. The recently announced credit guarantees for loans to SMEs is likely to provide support and if successful, could be continued at a nominal rate. Open lines of communication with the credit bureaus can help manage credit risks and ease SME’s access to credit. Two ways to resolve the issue of collateral: 1. Expand the nature of acceptable collateral to both movables and immovables; 2. Establish transparent, blockchain-based collateral registries/ platforms. Furthermore, an SME rating agency (like in India) could provide additional information to lenders. Resolving this constraint alone could kickstart a new wave of entrepreneurship in the country.

Backing from the government can come via a simple move like reducing the cost of doing business (various free zones have reduced fees and related charges for a short period) or ensuring no payment delays or boosting specific sectors (Abu Dhabi’s recent announcement to develop AgriTech) or through a wider mandate by instructing the various sovereign wealth funds to invest in local companies, through a dedicated fund, based on best practices.

Leapfrog on the massive changes Covid19 has brought about in the adoption of technology: varied e-commerce offerings, such as helping SMEs establish interactive websites, to creating innovative payment systems to neo-banking options. Alongside embracing the technology and greater digitalisation, it is necessary to also invest in and create the right ecosystem (bringing together the necessary skillset, retraining existing employees, reducing set-up and ongoing/ recurring business costs etc.).

[1] The UAE central bank expanded the definition of SMEs so that a larger segment will be in a position to qualify for SME lending.

[2] According to Ministry of Economy, the SME sector represents more than 94% of total firms operating in the UAE, accounting for more than 86% of the private sector’s workforce. In Dubai alone, SMEs make up nearly 95% of all companies, employing 42% of the workforce and contributing ~40% to Dubai’s GDP.

"Lebanon: a multi-pronged tragedy with unforeseeable consequences", CJBS Perspectives Interview with Dr. Jenny Chu, Sep 2020

How has the Beirut explosion disaster been exacerbated by the global pandemic, economic crisis and the failures in government leadership? What is needed to rebuild Lebanon? Dr. Nasser Saidi shared his thoughts when interviewed by Dr. Jenny Chu as part of the University of Cambridge Judge Business School (CBJS) Perspectives series.

Watch the interview below:

"Staring into the Abyss: Where does Lebanon go from here?", Brookings Doha Centre webinar, 17 Aug 2020

Dr. Nasser Saidi joined the Brookings Doha Center webinar (held on 17th Aug 2020) for a discussion on the dire political and economic situation in Lebanon. The session addressed the following questions: Is the country on its way to becoming a failed state, or will the repercussions of the Beirut blast lead to serious reform? Does the French political initiative steered by President Emmanuel Macron have the potential to resolve the crisis? What are the prospects for economic recovery amid stalled negotiations between the Lebanese government and International Monetary Fund? And what role can the international community play in order to assist Lebanon?

Watch the webinar below:

UAE, Covid19 & economic activity after re-opening post-lockdown

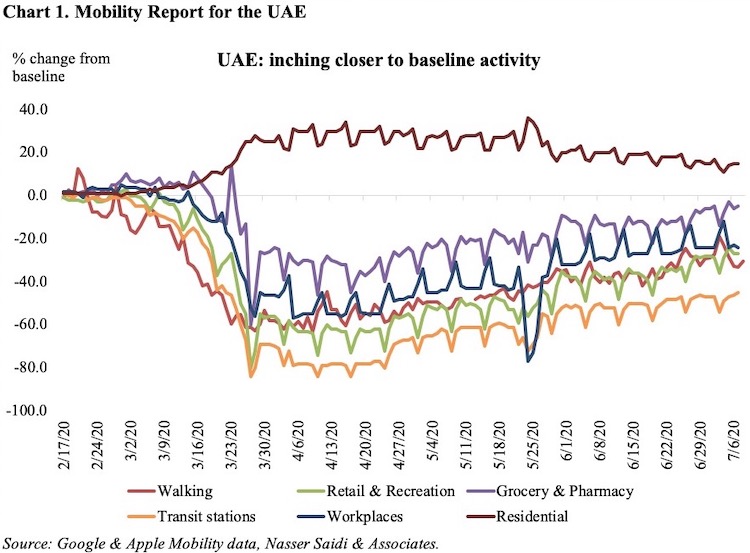

With UAE easing restrictions imposed due to the Covid19 outbreak and opening the economy in phases, a pickup in economic activity is inevitable. The Oxford Government Stringency Index (which records the number and strictness of government policies) scores the UAE at 69.44 in the beginning of Jul, down from a high of 89.81 recorded during the first two weeks of Apr (a higher score indicates a stricter government response). The question however remains whether residents have embraced the “re-opening” and gone back to “business as usual”.

Few economic indicators are released monthly in the UAE and hence the availability of Google and Apple Mobility numbers offer a good perspective of where the economy is headed to, reopening after the lockdown. Google Mobility indicators show trends over several weeks on how visits to various sectors – retail & recreation, grocery and pharmacy, parks, transit stations, workplaces – compare to a baseline value for that day of the week [1] while residential shows a change in duration of time spent at home. Apple Mobility indicators track resident activity – walking and driving – which can also be read into as “confidence” indicators i.e. you are more likely to be out exercising if you have accepted the new Covid19 realities (social distancing, wearing masks etc).

These high-frequency indicators offer an insight into retail behaviour (visit to recreation, retail outlets, groceries), as well as economic activity (transit stations, workplaces and residential) while parks and walking can be interpreted as “social well-being”, an equally important measure.

The lockdown phase in the UAE (towards the end of March) is evident from Chart 1, with the various indicators dipping to near -100%. Of the indicators, the two that are inching back to baseline are visits to groceries and pharmacies as well as workplaces. During the peak of the outbreak, when severe restrictions were in place, there was a surge e-commerce activity (especially online shopping platforms) which still continues, and could explain the current gap to baseline activity.

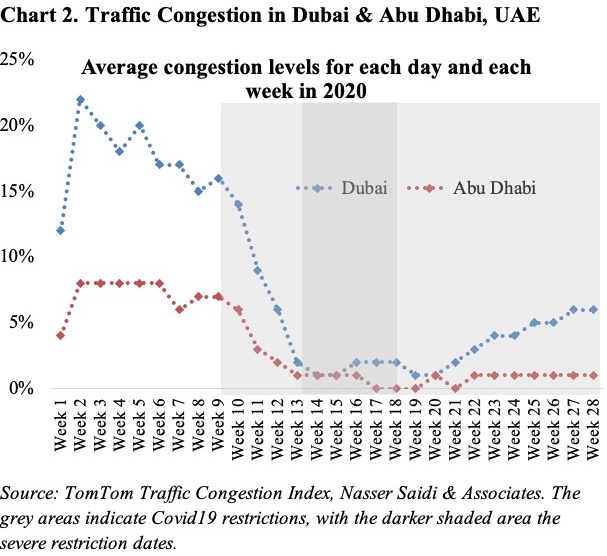

Workplaces are still 24% below the baseline, implying that working from home is still an option being provided by many offices. If companies continue to offer flexible work options, this would reduce office space and rents, while employees can stay at cheaper home locations, save on rents, and telecommute. Congestion statistics already show a return to normal, more so in Dubai than Abu Dhabi (Chart 2). However, to fully realise the benefits of telecommuting, it requires removing barriers by amending labour laws (e.g. part-time work/ freelancing options versus being tied to a specific company) and liberalising VoIP services (for businesses, especially for SMEs).

The uptick in “workplaces” has not been mirrored in “transit stations”. This is likely the result of a combination of two factors: (a) prevalence of using cars to travel – a report in Dec 2018 disclosed that UAE had an average ratio of one car to every three residents; average congestion is picking up faster in Dubai than in Abu Dhabi; (b) public transport is more frequently used by those without the option of personal transport, and who are more likely working in the services sector (e.g. in retail, hospitality sector and the like). Working in the hardest hit sectors during the Covid19 outbreak, these persons could have witnessed job losses or reduced working hours resulting in a slower uptick in “transit stations” category.

In spite of retail and recreation outlets operating at full capacity now, the return to baseline hasn’t been as smooth. One of the reasons could be the launch of online shopping by many retailers; another restriction is related to F&B operations: social distancing rules mean curtailed capacity, implying it will take longer for the sector to recover. Even during the Eid holidays in end-May, the uptick in this category was muted though lifting of restrictions mid-Jun on entry of kids and persons aged 60+ seems to have had a positive impact. With tourists back in Dubai starting Jul 7, the picture could change in the retailers’ favour.

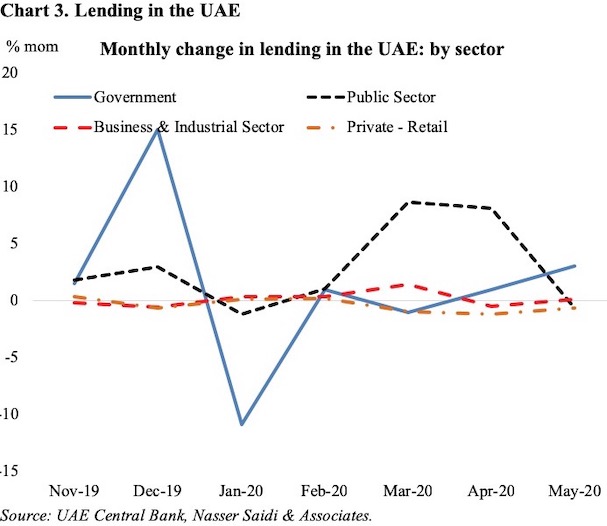

Last, but not the least, the UAE central bank has released monthly statistics for May – the 2nd month after lockdown was initiated towards end-Mar. The Central Bank had launched a AED 256bn Targeted Economic Support Scheme for banks to provide temporary financial relief for individuals, SMEs and other private businesses affected by the pandemic, following which banks offered relief for customers’ loans. Alongside, support was specifically initiated for SMEs – be it to open new bank accounts faster to providing credit guarantees. However, this does not seem to be reflected in the gross credit disbursed to UAE firms (Chart 3). Loans to the government rose by 3.06% mom in May while loans to the retail sector declined in month on month terms (-0.6%). Public sector entities (i.e. state-owned enterprises/ GREs) saw two consecutive 8%+ mom increase in loans before dropping by -0.7% mom in May.

So, what does all this mean from a policy perspective? The UAE’s drive to greater digitalization will gain traction in the new Covid19 normal: from varied e-commerce offerings to creating innovative payment systems to neo-banking options (ADGM announced associated regulations last year). A future UAE where work from home is commonplace, delinking jobs and visas are norm, and online payments are king (vs cash currently) is not far-fetched any more. The role of the private sector (including investments) is critical in achieving this goal alongside government support, and to this extend might need specific support for the SME sector which is oft sidelined given relatively lower turnover, lack of security/ collateral as well as potential for non-performing loans (and “absconding” owners). [1] The baseline is the median value, for the corresponding day of the week, during the 5-week period Jan 3–Feb 6, 2020.

[Updated 21/6/2020] GCC responses to tackle the Covid19 outbreak

As the GCC nations roll out various economic, financial, health and travel-related initiatives, the latest country-by-country measures is compiled below. Scroll down to see a map of the confirmed Covid-19 cases in the Middle East & North Africa region. The list is update as of 3:00pm on 21st June, 2020.

Table: GCC responses to tackle the Covid19 outbreak

Bahrain

Economic & Financial

Health & travel-related

Will slash spending by ministries and government agencies by 30%

BHD 4.3bn stimulus package: Doubling the Liquidity Fund to BHD 200mn + Waiver on utilities bills for 3 months + Delay in loans installments for 6 months + Supporting wages of citizens in pvt sector

BHD 5m allocated to Bahraini families in need & individuals affected by Covid-19

BHD 177mn (USD 470mn) will be added to this year’s budget to tackle emergency expenses related to the Covid19 outbreak

Central bank moves:

– Banned lenders from freezing customers’ accounts in case of lost jobs or retirement

– Cut overnight lending rate to 2.45% from 4% to ensure “smooth functioning of the money markets” (before Fed moves)

Parliament:

– Approved measures like reduction of commercial registration fees as well as labour & utility charges for 6 months

Cabinet authorised the finance minister to directly withdraw funds with a 5% ceiling from the public account

Bahrain will not collect rents and allowance from all tenants of municipal properties for three months starting from Apr

– All non-essential medical services resume operations

– Shops and industrial enterprises opened on May 7; restaurants remain closed still for dine-in customers

– Plans to resume Friday prayers postponed

– Schools scheduled to reopen in Sep

– Bans public gatherings of more than 5 individuals

– Bahrain will allow passengers to transit through the international airport; entry into the country will be limited to only citizens; mandatory 14-day self-isolation

Kuwait

Economic & Financial

Health & travel-related

Central bank:

– Reduced the discount rate to 1.5% (from 2.5%) a record-low

– Reduced liquidity and capital adequacy requirements for banks & cut risk weighting for SMEs (estimated to raise bank lending by USD 16bn)

– Domestic banks will defer paymentof consumer & SME loans and financing, credit card instalments for six months

Set up a KWD 10mn (USD 33mn) fund, to be financed by Kuwaiti banks

Government authorized additional funding of KWD 500mn (USD 1.5bn) to ministries and state agencies for fight against Covid19

Suspended fees on point of sales devices and ATM withdrawals + increased the limit for contactless payments to KWD 25 from KWD 10

The Kuwait Fund for Arab Economic Development pledged almost USD 95mn to support government efforts

– Kuwait eases “total curfew” to between 7pm to 5am; lockdown on Hawally area has been lifted

– Parliament suspended for 2 weeks (from Jun 18); public sector employees not be allowed to return to offices from this week (starting Jun 21)

– Expiring residence permits/ visas expiring in Jun extended for 3 months

– All educational institutions in Kuwait will reopen on 4th Aug

Oman

Economic & Financial

Health & travel-related

CB announces a $20bn incentive package

– Repo rate cut by 75bps to 0.5%;

– Reduce Capital Conservation Buffers for banks to 1.25% from 2.5%;

– Lending Ratio / Financing Ratio for lenders increased to 92.5% up from 87.5%

– banks and financial institutions to freeze repayments of personal and housing loans for three months, effective from May

– Reduce existing fees related to banking services + avoid introducing new fees

Finance ministry slashed approved budgets of civil, military and security agencies by 5%

All government companies have to reduce approved expenditures for 2020 by 10% + no execution of new projects or capital expenditures for the year; all exceptional bonuses for state employees would be halted

Other measures include tourism & municipality tax breaks, free government storage facilities and postponement of credit instalment payments

– Lockdown in Muscat ended; Dhofar Governorate in Oman closed from 12 noon of June 13 until July 3 for tourism

– At least 50% of employees in government entities will work from the offices starting May 31

– Oman has closed its borders; all domestic and international flights to and from airports suspended from 12 noon of Mar 29

– Covid-19 tests and treatments will be done for free for all communities

– Suspend issuance of tourist visas; will not allow cruise ships to dock at its ports during this period

– Schools closed; all public parks closed, public gathering prohibited, Friday prayers at mosques suspended; limited staffing at estate entities

– Few shops in Oman (consulting, law, audit firms, flower shops, boutiques etc) to reopen

– Restrictions are still in place on gatherings (of more than 5 individuals) on beaches and other public places

Qatar

Economic & Financial

Health & travel-related

A $23.3bn stimulus package

– QAR 75bn ($20.6bn) to provide financial + economic incentives for private sector

– CB to put in place an appropriate mechanism to encourage banks to postpone loan installments and obligations of the private sector with a grace period of 6 months

– Qatar Development Bank to postpone installments for all borrowers for 6 months

– Qatar’s government entities directed to reduce costs for non-Qatari employees by 30% as of Jun 1 (either pay cuts or layoffs)

– Directing govt funds to increase investments in the stock exchange by QAR 10bn ($2.75bn)

– Exempting food & medical goods from customs duties for 6 months

– Utilities bill exemption for SMEs, affected sectors; rent exemption for 6 months

– Four-phased recovery programme planned: Mosques to reopen Jun 15th, restaurants to partially reopen (Jul 1)

– All international flights suspended from Mar 18; cargo aircraft, transit flights exempt; travel ban on all travelers except Qatari nationals

– Qatar Airways grounds its A380 fleet; to temporarily reduce 40% of staff (in food and beverage, retail & ground staff) at Hamad Airport

– Educational institutions closed; parks and public beaches closed

– Bans social gatherings; introduces enforcement measures: checkpoints and mobile police patrols

– Private sector companies instructed to have 80% of their staff work from home, effective Thurs (Apr 2) for an initial 2 weeks

– Public transport modes have been stopped

– 6 tonnes of aid sent to Iran (medical equipment & supplies); donating $150mn in aid to Gaza

Saudi Arabia

Economic & Financial

Health & travel-related

– SAR 120bn worth measures to support the pvt sector including postponement of VAT/ excise/ income tax/ Zakat payments, exemptions of govt dues etc

– SAMA’s SAR 50bn stimulus package: financing support for SMEs (including deferred loan payments, concessional loans) and coverage of points of sale & e-commerce fees

– SAMA’s measures for supporting & financing the private sector: adjusting or restructuring the current funds without any additional costs or fees + reviewing reassessment of interest rates and other fees on credit cards + refunding travel-related forex transfer fees

– SAR 7bn allocated to Health Ministry in addition to the SAR 8bn package earlier + SAR 32bn approved for healthcare facilities

– Government will cover 60% of private sector salaries (of Saudi citizens) hit by Covid-19; first payment to be send on May 3.

– Will allow private businesses (affected by Covid19) to reduce working hours and permit wages to be reduced by not more than 40%

– Additional set of measures announced: SAR 50bn to accelerate payment of private sector dues & provide liquidity to several sectors while a further SAR 47bn was set aside for the health sector

– Saudi Industrial Development Fund revealed a SAR 3.7bn (USD 3.62bn) stimulus package for industrial sector companies

– Initiatives to reduce private sector’s burdens related to manpower: e.g. lifting halts on non-payment of fines, fines related to workers recruitment etc.

– Saudi Arabia will cut SAR 50bn (USD 13.32bn or less than 5%) of the 2020 budget; cost of living allowance scrapped

– VAT to be tripled to 15% starting 1st Jul

– Land borders with UAE, KW, Bahrain closed except for commercial trucks; shipping services suspended from 50 countries; cargo traffic not affected

– Restrictions eased across the nation: Saudi Arabia initiates the 3rd phase of its recovery plan by opening most commercial activities from Jun 20. Mosques in Makkah are also set to reopen with social distancing measures in place.

– Domestic flights resume; intl passenger flights still suspended + workplace attendance in both public and private sectors

– Malls reopen with multiple safety measures

– Mosques reopened with restrictions; Umrah pilgrimages to Mecca & Medina under a temporary ban

– Capital Markets Authority urgedshareholders & invested in listed companies to vote electronically in upcoming meetings; Tadawul reduces trading hours

United Arab Emirates

Economic & Financial

Health & travel-related

UAE announces a 2-phase recovery plan: short-term gradual re-opening (includ the AED 282.5bn stimulus) + focus on sectors “with high potential” in the long-term (AI, 5G, IoT, Blockchain, RE, EVs, 3D printing, robotics…)

Central bank:

– AED100bn stimulus to facilitate temporary relief on private sector loans & promote SME lending; support also the real estate sector

– 50% reduction in reserve requirements for demand deposits to 7% (releasing ~ USD 16.6bn in liquidity)

– Banks to reschedule loans contracts + grant deferrals on monthly loan payments (till end-2020) + reduce fees and commissions

UAE Cabinet: additional AED 16bn stimulus to reduce cost of doing business, support small business, accelerate implementation of govt infrastructure projects

Ministry of Economy reduced fees of 94 services

Dubai: AED 1.5bn stimulus package to support businesses affected by Covid19 including 10% reduction in utilities bills

Abu Dhabi: AED 5bn in utilities subsidies; free road tolls till end-2020, 20% rebate on rental values for restaurants + tourism & entertainment sectors (+ faster implementation of Ghadan-21 initiatives)

Dubai Freezones launch stimulus package: rents postponed for six months; cancellation of fines; free movement of labour with temporary contracts

Federal Tax Authority extends the Excise Tax return submission deadline for March and April 2020 to May 17, 2020

– Varied restriction across emirates: Abu Dhabi imposes movement ban from/to the emirate till Jun 23rd;

– Dubai permits shopping malls and private businesses to operate at full capacity

– Metro services re-open; buses and taxis are operational

– 30% of federal employees return to work from May 31; full capacity in Dubai’s govt offices & 30% in Sharjah’s govt offices from Jun 14

– Curfews reduced to between 10pm-6am; in Dubai from 11pm to 6am

– Entry for residents overseas to start from Jun 1; temporary ban to issue new visas

– All inbound, outbound and transit flights suspended from Mar 25; Emirates bookings are open from Jul 1 for 12 Arab nations; UAE airports welcome transit passengers.

– Schools to be closed till end-Jun; distance learning extended. Schools will reopen in Sep, though discussions ongoing regarding the method of learning in the 2020-21 academic year.

– Mosques, churches and other places of worship remain closed

– Opened, with social distancing measures: public parks, beaches, cinemas, gyms

– Supporting others: Sends 2 batches critical medical aid to Iran in Mar + flew 215 people from different countries out of Wuhan to Abu Dhabi’s Emirates Humanitarian City

Map: Number of Confirmed Covid19 cases by country (Source: Johns Hopkins University)

google.charts.load('current', {

'packages':['geochart'],

// Note: you will need to get a mapsApiKey for your project.

// See: https://developers.google.com/chart/interactive/docs/basic_load_libs#load-settings

'mapsApiKey': 'AIzaSyA4Q3e-hV2dI5w-sv8d4jG0V2jS1dXidTM'

});

google.charts.setOnLoadCallback(drawRegionsMap);

function drawRegionsMap() {

var data = google.visualization.arrayToDataTable([

['Country', 'Confirmed cases'],

['Bahrain', 21331],

['Kuwait', 39145],

['Oman', 29471],

['Qatar', 86488],

['Saudi Arabia', 154233],

['Lebanon', 1536],

['Iraq', 29222],

['Jordan', 1015],

['United Arab Emirates', 44533],

['Syria', 204],

['Iran', 202584],

['West Bank & Gaza', 448]

]); var options = {

region: '145', // Middle East

colorAxis: {colors: ['#00853f', 'black', '#e31b23']},

};

var chart = new google.visualization.GeoChart(document.getElementById('regions_div')); chart.draw(data, options);

}

google.charts.load('current', {

'packages':['geochart'],

// Note: you will need to get a mapsApiKey for your project.

// See: https://developers.google.com/chart/interactive/docs/basic_load_libs#load-settings

'mapsApiKey': 'AIzaSyA4Q3e-hV2dI5w-sv8d4jG0V2jS1dXidTM'

});

google.charts.setOnLoadCallback(drawRegionsMap); function drawRegionsMap() {

var data = google.visualization.arrayToDataTable([

['Country', 'Confirmed cases'],

['Algeria', 11631],

['Morocco', 9957],

['Tunisia', 1156],

['Djibouti', 4565],

['Libya', 544],

['Sudan', 7007],

['South Sudan', 1882],

['Iran', 202584],

['Egypt', 53758],

['Syria', 204],

['Yemen', 922]

]); var options = {

region: '015', // North Africa

colorAxis: {colors: ['#00853f', 'black', '#e31b23']},

};

var chart = new google.visualization.GeoChart(document.getElementById('regions_div2')); chart.draw(data, options);

}

google.charts.load('current', {

'packages':['geochart'],

// Note: you will need to get a mapsApiKey for your project.

// See: https://developers.google.com/chart/interactive/docs/basic_load_libs#load-settings

'mapsApiKey': 'AIzaSyA4Q3e-hV2dI5w-sv8d4jG0V2jS1dXidTM'

});

google.charts.setOnLoadCallback(drawRegionsMap); function drawRegionsMap() {

var data = google.visualization.arrayToDataTable([

['Country', 'Confirmed cases'],

['Iran', 202584],

['Syria', 204],

['Afghanistan', 28833]

]); var options = {

region: '034', // SAsia

colorAxis: {colors: ['#00853f', 'black', '#e31b23']},

};

var chart = new google.visualization.GeoChart(document.getElementById('regions_div3')); chart.draw(data, options);

}

Middle East

North Africa

Iran & Afghanistan

Interview with Dubai Eye – Jan 15, 2013

Listen to my interview with Dubai Eye on the UAE central bank’s cap on mortgages: http://www.dubaieye1038.com/page/Dr._Nasser_Saidi_15.01.2012/85621?feed=5

Mitigating the Risks of Another UAE Real Estate Bubble

Making the case for active approach to real estate lending and management, a version of this op-ed piece was published in The National on Jan 14, 2013 (http://www.thenational.ae/thenationalconversation/industry-insights/property/proactive-approach-can-allay-fears-of-boom-and-bust).

ral bank shed some light on the broader credit movements: the accompanying chart shows the monthly changes in gross domestic credit. The dotted lines are credit to businesses and individuals (the private sector) which show no substantial increases – in fact, it increased by an average 0.9% year-to-date (ytd) for businesses and dropped by 2.1% ytd for individuals. The uptick in lending to the public sector (government related entities) and government have been discussed previously

ral bank shed some light on the broader credit movements: the accompanying chart shows the monthly changes in gross domestic credit. The dotted lines are credit to businesses and individuals (the private sector) which show no substantial increases – in fact, it increased by an average 0.9% year-to-date (ytd) for businesses and dropped by 2.1% ytd for individuals. The uptick in lending to the public sector (government related entities) and government have been discussed previously