Download a PDF copy of the weekly economic commentary here.

Markets

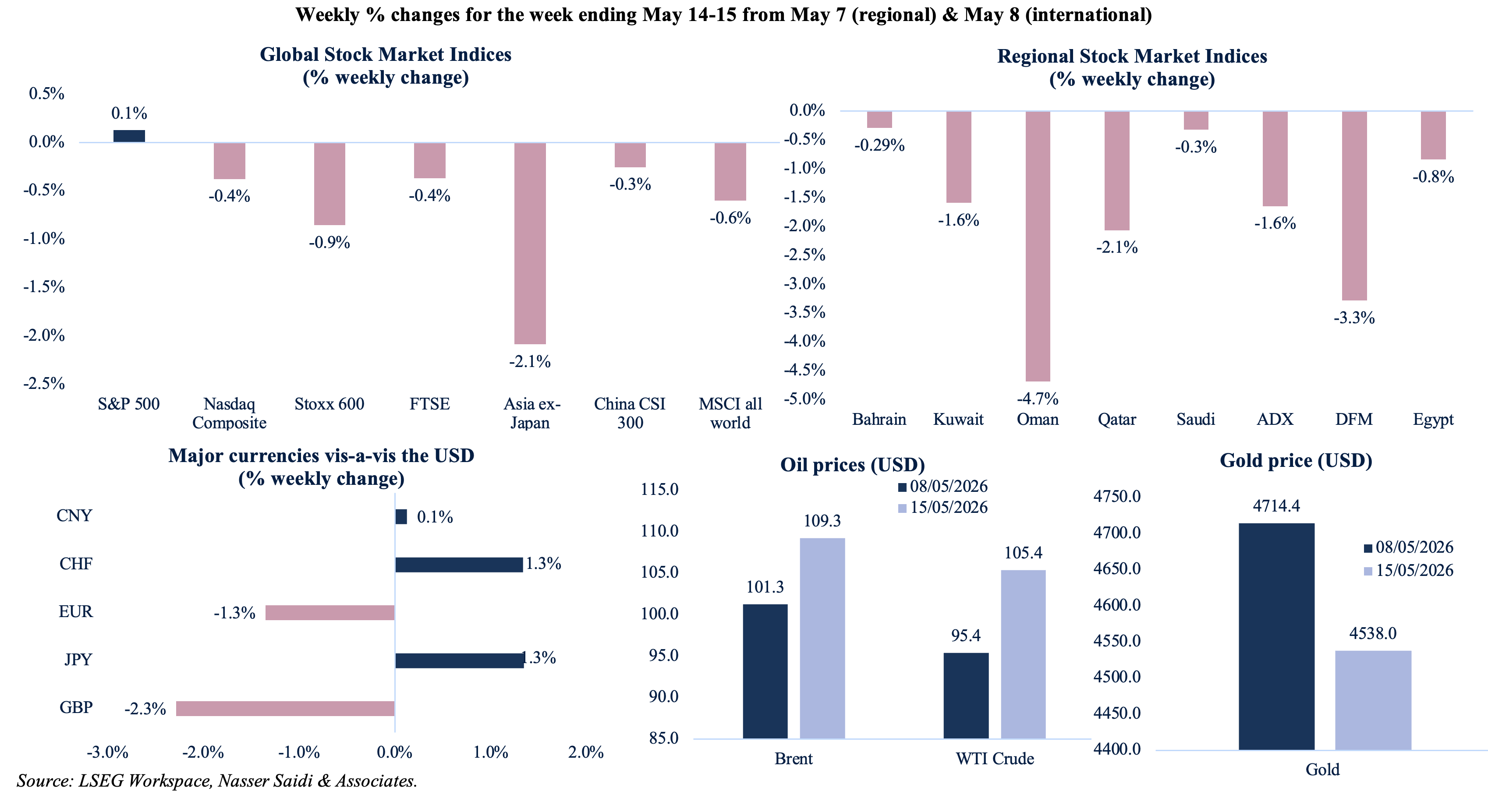

Global financial markets ended the week mostly in the red, with no new updates or clarity on the US-Iran negotiations, some cautious optimism over the Trump-Xi summit in Beijing amid increasing worries over a potential energy-driven stagflationary scenario. Most equity bourses in the region ended lower with no resolution from the multiple rounds of diplomatic negotiations. The latest drone attacks in Saudi Arabia and UAE accentuated the urgency for a permanent solution to the conflict in Iran. Among currencies, the Indian rupee plummeted to a historic record low past 96 per USD, given the surging oil import bill, while in the UK, the GBP and gilts fell amid the domestic political uncertainty and ongoing inflationary pressures. Crude oil prices continue to climb, propelled by ongoing fears of ship attacks, cargo seizures and prolonged chokepoint disruptions in the Strait of Hormuz. This is slowly leading to higher global inflation expectations feeding into futures markets, pushing sovereign bond yields upward and driving gold toward a weekly loss as markets prepare for a more restrictive monetary policy trajectory.

Economic Consequences from the conflict in the Middle East & Policy Responses

The global economic and geopolitical landscape in mid-May 2026 is still being dominated by the fallout of the US-Iran war, that has already cost the US an estimated USD 29bn according to the Pentagon. Though the Trump administration is still leaning toward securing a diplomatic victory, the last peace terms shared by Iran were dismissed as entirely “unacceptable” and new sanctions were placed on Chinese networks handling illicit Iranian oil flows. The deadlock risks prolonging the conflict, worsening instability in the Middle East and disrupting global energy markets, especially around the strategically vital Strait of Hormuz.

The US government’s energy intelligence arm expects that the Strait of Hormuz will remain effectively closed through late-May 2026. This protracted blockade implies an unprecedented supply disruption, with the broader oil market on track to lose nearly 100mn barrels every single week the chokepoint remains blocked. Consequently, the IEA warns that global oil supply will drop below total demand this year – can also be seen in OPEC’s April output plunging to historic lows due to a pause in export.

Compounded by ongoing Russia-Ukraine tensions, the conflict in the Middle East has handed global refining output its most severe contraction in years. Iran is actively leveraging its structural control over the Strait of Hormuz to forge new, politically driven energy transit and supply agreements with Iraq and Pakistan. Official maritime tracking indicates that Iraq successfully exported 10mn barrels of crude oil through the heavily contested Strait of Hormuz in April, though significantly below pre-war baselines. A Qatari LNG shipment was permitted to transit the blockaded Strait of Hormuz with delivery to Pakistan. Reuters reported that neither country had made direct payments to facilitate safe transits. Iran also formally established a preferential transit regime through the Strait, allowing the unhindered passage of Chinese-flagged and Chinese-coordinated vessels – highlights how Iran is utilizing its maritime chokepoint dominance to protect its relationship with its primary economic and political partner in Asia. Diplomacy has allowed Iran to weaponize its chokepoint, though such bilateral pacts will likely deepen regional fragmentation.

Last week also saw US President Trump travel to Beijing for a high-stakes meeting with President Xi, along with a high-profile business delegation (including the likes of Apple, Nvidia and Tesla to name a few). While the US has highlighted a few deals as positives from the trip – Boeing jets, purchases from US farmers – there was not much progress on key issues such as Iran, Taiwan, AI competition or broader tariff disputes.

Countervailing Regional Policies & Developments

- Bahrain introduced a comprehensive economic assistance package designed to insulate 7,250 small, medium and micro enterprises from the logistical and inflationary pressures of the regional conflict. The intervention includes financial grants, covering essential operating expenses and financing facilities to support businesses operational needs. This proactive fiscal buffering will minimize bankruptcy risks and stabilize consumer sentiment amid volatility.

- Aluminium Bahrain (Alba) posted an extraordinary 316% yoy surge in profit attributable to equity holders to BHD 75mn in Q1 2026 despite a significant disruption to its export sales volumes (-17% to 312,563 tonnes) due to maritime transport blockades.

- Iraq has officially approached the IMF to secure emergency financial assistance to finance its budget deficit, given the severe revenue shortfall due to lower oil exports from the disruptions of the ongoing conflict. Separately, the IMF’s MD had stated earlier that the IMF could see demand from at least 12 countries for between USD 20-50bn due to conflict-related impact, though no country details were disclosed.

- Israel and Lebanon agreed to a 45-day extension of the ceasefire last week. While the truce remains highly fragile and subject to sudden violations, it offers a temporary relief, as Israel continued military operations in South Lebanon.

- Saudi conducted counter-militia air operations in Iraq against hostile pro-Iran militias during the peak of the recent escalation, reported Reuters. This direct military intervention reflects a significant shift in regional defence postures, demonstrating willingness to use unilateral force to protect its borders and vital infrastructure from external asymmetric threats.

- UAE announced accelerated construction of a new oil pipeline to double export capacity via Fujairah, designed to permanently bypass the Strait of Hormuz chokepoint. The completion of the fast-tracked corridor (expected to be operational by next year) would permanently de-risk UAE’s energy export infrastructure.

- The UAE’s Habshan gas-processing facility is currently running at 60% capacity and will reach 80% by year-end, disclosed Adnoc Gas. The UAEss biggest gas plant will not be fully repaired until mid-2027 after suffering two Iranian attacks last month.

- The Ministry of Energy reiterated that UAE’s historic exit from OPEC was a sovereign, value-driven strategic decision aimed at maximizing the monetization of its massive unconventional assets, rather than a political gesture.

- The Chairman of the UAE Banks Federation confirmed that the country had experienced zero capital flight despite the proximity of the ongoing conflict in Iran. This institutional stability is supported by consecutive years of record banking sector profitability, conservative capital adequacy ratios and the UAE’s status as a global safe haven for international private wealth. He also disclosed that lenders have required minimal utilization of the Central Bank’s expanded emergency liquidity packages during the ongoing conflict (versus relief disbursed during Covid years) demonstrating exceptional resilience.

- The UN World Food Programme was forced to halve its emergency food assistance to Syria and dismantle essential bread subsidies due to critical international funding shortages. The number of people receiving emergency food aid in Syria fell to 650k in May from 1.3mn, while operations were scaled back to just seven from all 14 Syrian governorates. This threatens to trigger acute food insecurity and deep social strains.

Macroeconomic Developments in the MENA region

- Egypt outlined an ambitious development plan targeting EGP 3.4trn (USD 70bn) in total investments for FY2026-27, allocating roughly 45% to public investments and 55% to private capital participation. The government aims to stabilize the macroeconomic environment, prioritize human development, local industrial localization and infrastructure projects while stimulating robust private sector participation and drive its 5.4% growth target.

- Egypt increased its fuel import budget by nearly 40% to USD 5.5bn for the 2026-2027 fiscal year. The funds will be used to secure supplies of gasoline, diesel and LPG amid higher global prices (due to the Iran war) to guarantee uninterrupted power and industrial production.

- Egypt plans to establish seven new dedicated investment zones to capture EGP 3.75trn (USD 77.6bn) in capital injections over the next twenty years. These specialized hubs will provide enhanced corporate regulatory ease, streamlined customs handling and modern infrastructure networks to optimize export-oriented industrial clustering. This development model aims to yield a consistent USD 4bn in annual foreign and domestic inflows.

- Egypt’s government announced a comprehensive mandate to transition its entire state vehicle fleet to electric power. This strategy will reduce the government’s spending on subsidized fuel while embracing a domestic EV assembly and supply chain ecosystem.

- The tourism sector in Egypt posted a record-breaking USD 16.7bn in revenue for the fiscal year 2024-25. The resulting foreign exchange injection has provided the central bank with a vital macro-stabilizing cushion during a period of acute external strain.

- Egypt secured USD 1bn in financing from the World Bank to support its private sector, including a USD 200mn credit guarantee from the UK. This multilateral credit focuses on enhancing private-sector competitiveness, stabilizing fiscal frameworks and driving sustainable green growth initiatives.

- Egypt has implemented a series of electricity tariff hikes across commercial service sectors, heavy industries and metro operations to offset escalating power generation costs. This pricing adjustment, while designed to narrow the fiscal deficit and alleviate state utility subsidy, is likely to introduce immediate cost-push challenges for local service and transport operators.

- Egypt is advancing its New Delta megaproject, a massive agricultural reclamation initiative spanning over two million feddans to secure national food sovereignty. By utilizing advanced wastewater recycling infrastructure and automated modern farming techniques, the project aims to substantially lower Egypt’s high reliance on imported strategic grains and wheat. Phased cultivation of the New Delta is expected to slash Egypt’s agricultural import bill by up to 25% by 2028, easing long-term structural strain on foreign currency reserves.

- Egypt’s Technical Gas Services Company won a contract to repair Lebanon’s 30km gas distribution network, a critical step as Lebanon prepares to receive natural gas through Jordan.

- Syria has finalised exploration frameworks for a major gas and oil offshore sector with Chevron and QatarEnergy. Technical operations are likely to start in the summer, with advanced geological imaging used to unlock fresh upstream reserves in a historically under-invested energy corridor. Successful exploration outputs will likely redefine the Eastern Mediterranean gas architecture, transforming the Levant coast into a critical export hub.

Macroeconomic Developments in the GCC

- Headline CPI in Oman eased to 3.3% yoy in Apr, following Mar’s 3.7% (highest since Feb 2022).The food & non-alcoholic beverages segment emerged as a primary driver of domestic price hikes (6.2% yoy vs Mar’s 4.3%). Transport costs and miscellaneous goods & services costs remained high (6.0% and 9.2% respectively), though lower compared to Mar.

- The Oman-India free trade agreement is highly anticipated to officially take effect on June 1st, disclosed India’s commerce minister. The deal will establish a powerful low-tariff trade corridor – structurally lower import costs for critical Indian industrial inputs and open a massive consumer market to Omani non-oil exports, specifically petrochemicals and minerals.

- Omani workforce in the private sector increased by a robust 8.8% yoy to 436,098 by end-Mar, reflecting the enforcement of localization quotas and structural labour market reforms.

- Oil production in Oman grew by 4.8% yoy to 93.1mn barrels as of end-Mar 2026. Average daily oil production saw a significant rise of 6.7% to 1.1mn barrels per day in Mar. Oman’s geography gives it more flexibility than other GCC producers heavily dependent on the Strait of Hormuz: this shows in oil exports up 3.2% yoy to 26.5mn barrels in Mar. Natural gas supply also rose, with total domestic production and imports of natural gas up 2.5% yoy to 13.7bn cubic meters by end-Mar. Industrial sector was the largest consumer of natural gas (share of 18.1%) followed by power generation (under 10%).

- The value of Oman’s digital payment transactions surged by 76.3% yoy to OMR 3.2bn in 2025, driven by the Central Bank’s regulatory mandates, modernized retail infrastructure and strong consumer demand. The digital ecosystem significantly lowers transaction costs and facilitates purchasing processes.

- The Oman Investment Authority strategically acquired significant equity stakes in Turkish mining and defence companies, marking a targeted expansion of its sovereign wealth portfolio. This secures technological transfer in defence manufacturing and broadens Oman’s exposure to critical industrial metals outside the region.

- Oman is on track to raise the share of renewable energy in its national power mix to at least 10% by the end of 2026. This rapid scaling of utility-scale solar and wind infrastructure aims to displace domestic natural gas consumption, freeing up lucrative hydrocarbon volumes for export or high-value petrochemical processing.

- Oman has officially updated its national Net-Zero Strategy to achieve carbon neutrality by 2050, strengthen its position as a regional hub for green hydrogen & renewable energy and launched a regulatory framework for carbon markets to regulate industrial emissions (including structured carbon tracking and trading readiness). Separately, Oman announced plans to develop its first-ever Round-The-Clock (RTC) renewable energy project, combining solar, wind and advanced utility-scale battery storage to ensure uninterrupted clean baseload power. This will provide a highly reliable power source for heavy industries and data centres outside the traditional grid.

- South Korea’s electric vehicle manufacturer EL B&T committed to a USD 250mn investment to establish an advanced EV production facility in Oman. The project will reach a production capacity of up to 60k electric vehicles annually and 1.6mn battery cells upon completion of Phase II: expanding Oman’s non-oil export into sustainable transport sectors.

- FDI inflows into Qatar grew by 2.0% to a record USD 45.43bn in 2025, reflecting growth in the stock of FDI by local enterprises, while outward FDI jumped 8.1% to USD 57.69bn. Net FDI stock touched QAR 44.6bn, up 39% yoy.

- The GCC Railways Authority confirmed that the 1,700km GCC railway project officially crossed the 50% completion milestone. A full operational launch is expected by Dec 2030 and is projected to handle 6mn passengers and 200mn tonnes of freight annually by then (rising to 8mn+ passengers and 271mn tonnes freight by 2045). This project will integrate air, road and maritime transit and significantly enhance regional supply chain resilience and cross-border trade efficiency.

- High-level negotiations for the GCC-UK Free Trade Agreement are gathering momentum (with ministers citing “significant progress”) as part of a push to unlock trade opportunities and diversify cross-border capital flows. The proposal aims to eliminate industrial tariffs, harmonize cross-border regulatory frameworks and deepen integration across the digital and financial services sectors among others.

- GCC sukuk issuance volume expanded by 13.1% yoy in Jan-Apr 2026, driven primarily by robust local-currency programs in Saudi Arabia, according to S&P Global. While the global Islamic finance expansion is projected to slow to 5-10% in 2026 due to the Middle East conflict (2025: +10.2%), weaker sovereign fiscal balances are actively driving debt issuance.

Saudi Arabia Focus:

- Saudi Arabia’s inflation was remarkably resilient, rising 1.7% yoy in Apr (Mar: 1.8%), given slowing housing costs (3.8% from 3.9%) alongside slightly higher costs of food (0.6% from 0.3%) and transport (1.0% from 0.9%). Wholesale price index was stable at 3.3% yoy in Apr: other transportable goods surged 6.4% (unchanged from Mar) while ores and minerals prices stayed deflationary (-0.3% yoy from -0.2%).

- Despite the broader economic shock, the Saudi Ministry of Industry and Mineral Resources issued188 new industrial licenses in Mar 2026, attracting over SAR 1.81bn in investments – emphasizing the rapid acceleration of domestic manufacturing. This follows Feb’s strong performance (38 new mining licenses issued). Additionally, 78 new factories commenced actual production, representing SAR 870mn in investment & creating nearly 1,500 new jobs.

- Saudi Arabia’s financial sector continued to expand, with the number of finance licenses climbing to 74 (after a new BNPL firm was approved) and payment providers touching 32.

- Saudi Arabia’s crude oil exports to China are expected to reach a record low in Jun. Aramco was set to export 10mn barrels of oil or about 33k barrels per day (vs 1.39mn bpd sent in 2025) but the reduction in the official selling price of June Arab Light crude to Asia (USD 15.5 a barrel from USD 19.5 the month before) was smaller than expected. Lower volumes to China amid rising competition from discounted supplies will benefit other Asian buyers.

- Saudi ports handled over 14.53mn tonnes of cargo in April, down 34.58% yoy, while the number of containers handled fell 18.65% to 508,801 TEUs. This volume, amidst lower trade activity during the ongoing conflict, highlights the ability of Red Sea gateways like Jeddah Islamic Port and King Abdullah Port to bypass conflict chokepoints.

- The Public Investment Fund’s latest regulatory filings reveal a slightly reduced US equity portfolio of USD 12bn in Q1 2026 (vs USD 12.9bn at end-2025). The filing showed a reduced number of holdings alongside retained stakes in Lucid Group, Electronic Arts Inc, Uber Technologies, and Claritev Corp. Separately, the PIF revealed that it is consolidating its presence in Asia by opening a second office in China – this underscores the strategic pivot toward deepening investment and long-term economic partnerships with China.

- Saudi budget carrier Flynas reported a fall in profits, directly attributing the decline to higher fuel and maintenance costs.

- Coordinated government interventions are actively shielding Hajj pilgrims from war-driven inflation, rising aviation costs and hospitality price surges. The Saudi government as well as governments in India, Indonesia and Pakistan (among others) have deployed targeted subsidies (e.g. air fares) and logistical support to ensure the accessibility. These cost-stabilization measures will likely guarantee high pilgrim turnout for this season.

- Saudi Arabia and Russia have implemented a bilateral agreement to lift mutual visa requirements (effective May 11th), a diplomatic move intended to enhance tourism, business mobility and cross-border investment. This policy shift directly targets a massive expansion of the leisure and business travel segments amid complex global geopolitical re-alignments.

- Saudi Arabia’s ACWA Power successfully secured USD 226mn in funding for a new wind farm project in Uzbekistan. This highlights the continued export of Gulf renewable energy expertise and capital to emerging Central Asian markets.

UAE Focus:

- India and UAE formalized landmark pacts covering strategic petroleum reserves, long-term LPG supply, a USD 5bn investment pledge and an 8-exaflop artificial intelligence supercomputing cluster with G42 during the Indian PM’s visit last week. These strategic agreements increase UAE participation in India’s petroleum reserves to 30mn barrels and establish critical frameworks for defence industrial collaboration and technology sharing.

- The Make it in the Emirates event saw aggregate deals worth AED 171bn (USD 46.56bn) being announced, including investments worth AED 48.5bn and AED 19.2bn in financing. The UAE’s Minister of Industry and Advanced Technology revealed that industrial exports from the UAE have grown to AED 262bn, including AED 92bn in advanced industrial exports. Furthermore, the value of industrial procurement opportunities in the UAE is expected to rise by 7% to AED 180bn over the next decade from AED 168bn currently. One of the biggest domestic deals was between Abu Dhabi’s Ta’ziz and Alpha Dhabi, aiming for USD 10bn in capital investment in its new industrial chemicals ecosystem in the emirate.

- UAE’s Minister of Energy & Infrastructure announced that Abu Dhabi will see an unprecedented domestic infrastructure spending wave over the next four to six years: to this end, Abu Dhabi unveiled an ambitious USD 57bn infrastructure project pipeline across 500 projects (though no details were provided). Separately, Abu Dhabi unveiled a massive AED 55bn Public-Private Partnership (PPP) investment pipeline for 2026-27, comprising 24 developments and targeting primary transport & public service networks.

- Bilateral non-oil trade between the UAE and Syria reached a record USD 1.4bn in 2025, up by a staggering 132% yoy. At the inaugural Syrian-Emirati Investment Forum, officials formalized a series of preliminary agreements spanning construction, infrastructure, logistics, tourism, agriculture and aviation. This reconnection underscores a strategy to diversify land-based regional logistics corridors and capture reconstruction and redevelopment opportunities.

- ADNOC Drilling has declared its operational readiness to expand the UAE’s oil production capacity beyond its current 2027 target of 5mn bpd, following the UAE’s exit from OPEC. The listed firm outpaced initial expectations by deploying 142 rigs by 2025 (ahead of a target of 127 by 2030) and maintained a remarkable 98% rig availability in Q1 despite ongoing regional tensions. By utilizing land routes and port facilities in Fujairah, the company has successfully bypassed the bottlenecked Strait of Hormuz.

- Dubai Holding became the dominant shareholder in Emaar Properties after acquiring a 22.27% stake from the Investment Corporation of Dubai in an off-market transaction valued at approximately USD 6.5bn; this raises Dubai Holding’s total ownership to 29.73%.

- Dubai toll operator Salik reported a modest 3.0% yoy decline in total revenue to AED 728.9mn in Q1 2026. The compression was primarily driven by lower toll usage and a softer traffic environment in March linked to regional geopolitical tensions. However, efficient cost management and Dubai’s peak-hour variable toll pricing model allowed net profits to remain stable at AED 369.3mn, with EBITDA margins expanding slightly to 69.6%.

- The Central Bank of the UAE granted in-principle approval to establish “Omla Community Bank” in Umm Al Quwain. The new digital bank is designed as an AI-native institution, deeply integrating AI across its risk management, compliance, governance and customer experience frameworks.

Global Macroeconomic Developments

US/Americas:

On the output front, growth remains resilient, as evidenced by industrial production rebounding by 0.7% mom in April and the NY Empire State manufacturing index surging to 19.6 in May (Apr: 11.0). This went hand-in-hand with robust consumer demand: retail sales grew 0.5% mom (and a strong 4.9% yoy) in Apr, while the housing market saw existing home sales inch up by a modest 0.2% mom to a 4.02 million annualized pace. This underlying economic optimism was mirrored by small businesses, with the NFIB index creeping up to 95.9 in Apr (Mar: 95.8). Meanwhile, initial jobless claims crept up to 211k in the latest reporting week, the four-week moving average remained exceptionally anchored at 203.75k. Despite the uptick, claims remain at relatively low levels overall, suggesting the US labour market continues to show resilience with only gradual signs of softening. Price pressures are however building up: headline inflation marched upward to 3.8% yoy in April, with core CPI rising to 2.8%; the pipeline pressures look even more severe as the Producer Price Index jumped to 6.0% in Apr (Mar: 4.3%) and core PPI surged to 5.2% (Mar: 4.0%). These readings are tempering any near-term case for monetary easing: the Fed’s “higher-for-longer” narrative is rapidly transitioning into a “higher-for-even-longer” reality.

Europe:

In the Eurozone, real output remains exceptionally fragile, with Q1 GDP growth crawling at 0.1% qoq (and 0.8% yoy). This stagnation is driven by a deep supply-side contraction, as Eurozone industrial production collapsed by 2.1% yoy in March. The epicentre of this remains Germany, where the ZEW current situation index plunged further to a dismal -77.8 in May, even though the forward-looking ZEW economic sentiment index moderated its negative trajectory to -10.2 (mirroring a broad Eurozone sentiment improvement to -9.1). Crucially, this output stagnation is paired with severe supply-side shocks, as the German wholesale price index surged to 6.3% yoy in April, indicating sharp cost-push pressures filtering through the industrial value chain. From a monetary policy perspective, the ECB will likely hold rates steady through H2 2026: the combination of near-zero growth and a 6.3% surge in wholesale prices presents a textbook stagflationary dilemma. Conversely, the UK demonstrated unexpected resilience, with Q1 GDP expanding by 0.6% qoq and 1.1% yoy, supported by strong service sector activity and a rebound in construction. UK also posted a robust 1.2% rebound in manufacturing output despite flat headline industrial production. However, this growth momentum faces domestic headwinds, as a sharp 3.4% yoy drop in BRC like-for-like retail sales in April signals that the UK consumer is feeling the strain of prolonged living-cost pressures.

Asia Pacific:

In China, while the headline consumer inflation crawled upward to a modest 1.2% yoy in April, the Producer Price Index surged to 2.8% (up from March’s 0.5%), signalling a rapid pass-through of global commodity and energy costs. This contrast sharply with credit allocation, where despite steady broad money supply (M2) growth of 8.6%, new bank loans contracted by CNY 10 bn, as commercial lenders are reluctant to extend credit despite stable systemic liquidity. Japanese overall household spending collapsed by a sharp 2.9% yoy in March, while the external sector saw the current account surplus rise to JPY 4.68 trillion; the leading economic index climbed to 114.5, suggesting that industrial exporters are successfully capturing global market share despite weak domestic demand. In India, headline consumer inflation crept up to 3.48% in April, but the Wholesale Price Index (WPI) surged dramatically to 8.3% (up from 3.88% in March), indicating a massive, impending cost-push shock. Overall, the Asian growth outlook will depend on how firms absorb severe cost-push pressures against an uneven global demand backdrop.

Media Review:

Trump’s geopolitical brinkmanship has hit a wall with Iran

Global bonds tumble on fears of inflation shock from Iran war

https://www.ft.com/content/02015e49-fe11-488f-9e45-9fe70943d155?syn-25a6b1a6=1

AI super-apps are remaking China’s internet

https://www.economist.com/business/2026/05/17/ai-super-apps-are-remaking-chinas-internet

Powered by:

![]()