Download a PDF copy of the weekly economic commentary here.

Markets

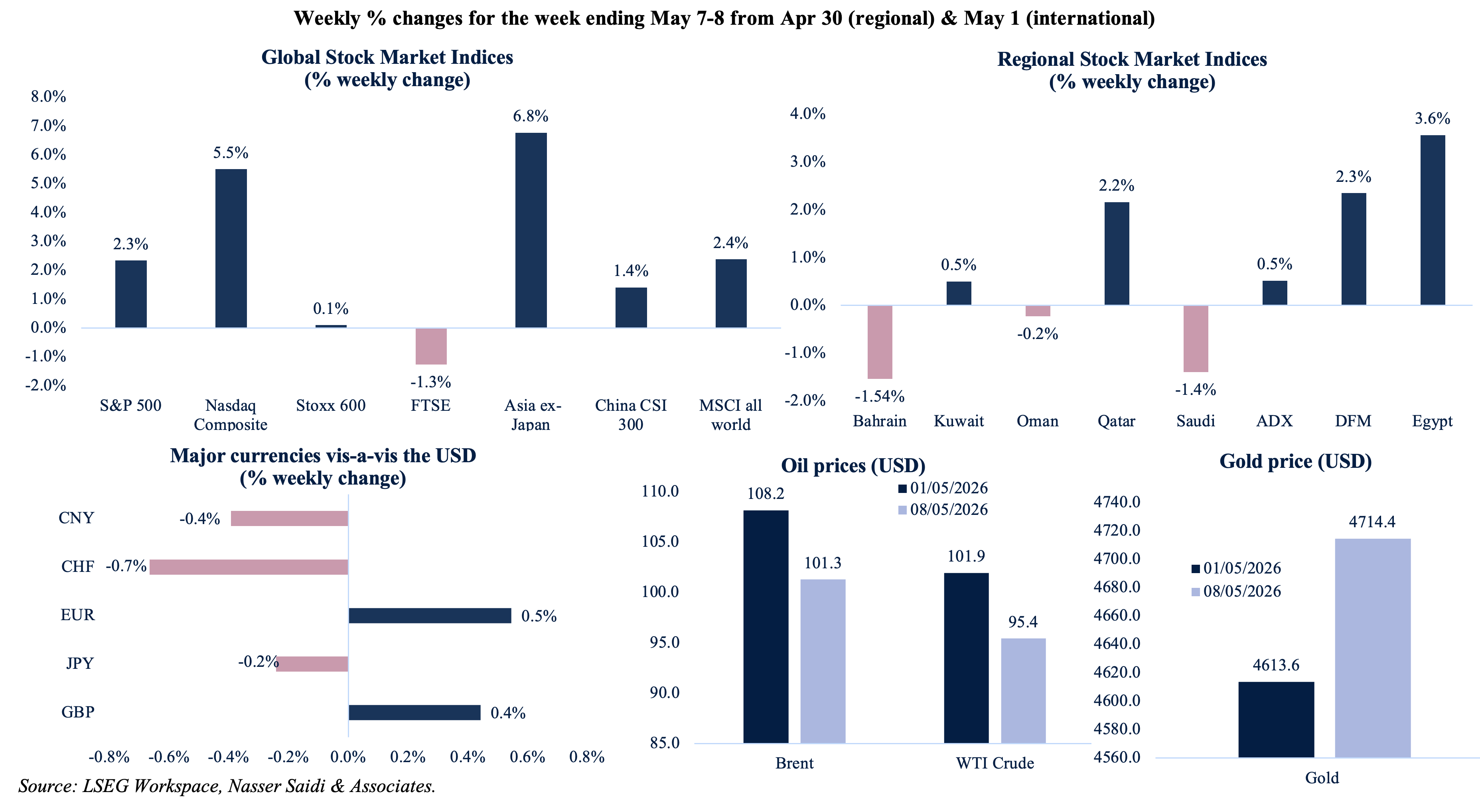

With a better-than-expected non-farm payrolls report, US equity markets (S&P 500 and Nasdaq) climbed to new records. European markets were mostly subdued, while Asian markets benefited from strong revenue results as well as a boost from US AI firms spending plans (that would help regional chip manufacturers). Most Gulf bourses rallied early in the week, supported by robust corporate earnings and optimism regarding a potential US-Iran peace agreement. However, this rally proved fragile amid renewed hostilities and fresh air strikes between US and Iran. Among currencies, the CNY was close to CNY 6.8 per dollar on Friday, almost the strongest since 2023; meanwhile, the Japanese yen steadied after hitting a two-year high – not due to a shift in fundamentals, but following suspected market interventions intended to stop speculation during this period of high volatility. Oil prices jumped upwards end of the week as hostilities flared and gold ended with a weekly gain as investors hedge against the uncertainty of a sustained truce.

Economic Consequences from the conflict in the Middle East & Policy Responses

President Trump’s rejection of Iran’s response to the US proposal as “totally unacceptable” has seen stocks fall today (11 May) alongside an uptick in oil prices. A fragile ceasefire is still holding, though persistent clashes and a high-stakes battle for control of the Strait of Hormuz cast significant doubt on how long the truce could hold. The industrial and energy fallout is equally profound. Saudi Aramco’s leadership warns that the loss of approximately one billion barrels of production will severely hamper the global oil market’s recovery. To mitigate this blockade, regional actors have resorted to unconventional tactics, such as the UAE utilizing hidden tankers to slip exports through the Strait undetected. Simultaneously, many countries in the GCC (notably UAE, Kuwait and Qatar) are actively intercepting drone and missile attacks (albeit at a much smaller scale compared to early-March).

The conflict’s fallouts and spillovers are widening across regional and global alliances. The US has intensified its pressure campaign, recently sanctioning Iraq’s Deputy Oil Minister and various militias for their alleged support of Iranian operations. As it stands, the friction between the Trump administration and traditional US allies over the conduct of the war is likely to persist long after current operations cease. However, IMF Managing Director Kristalina Georgieva warned at a Milken Institute event that the global economy is already in an “adverse scenario”, adding that if hostilities persist into 2027 with oil prices reaching USD 125, the resulting inflation de-anchoring would lead to a significantly worse global outcome. If negotiations remain stalled even by end-May, oil prices could face significant further upward pressure. The scale of market uncertainty is further evidenced by reports showing that speculative oil price bets totalling USD 7bn were placed in the days immediately preceding major war-related news.

Ahead of the Trump-Xi summit this week, in a strategic diplomatic push, US Treasury Secretary Bessent urged China to leverage its influence to reopen the Strait of Hormuz – noting that Beijing’s energy imports effectively fund the Iranian regime. Concurrently, Pakistani mediation secured a vital breakthrough, allowing the first Qatari LNG shipment to transit the blocked waterway since the war began, offering immediate relief to Pakistan’s energy crisis.

This week is also important from a data perspective: US inflation, producer prices and retail sales data will show how the spike in oil prices is translating into costs and consumer spending. This will be closely watched by the Fed (which showed a hawkish tilt after the previous meeting). Also on the cards are UK Q1 GDP data: while a strong reading is expected, March data will be key to see if there is any substantial war-related impact on businesses and consumer spending.

Countervailing Regional Policies & Developments

- Iraq’s USD 5bn Basra-Haditha pipeline (a land-based oil export route) was allocated USD 1.5bn to start work and is expected to create 15k jobs. The pipeline is being constructed under the oil-for-projects agreement signed by Iraq and China in 2019. Upon completion, this pipeline could transport exports of 2.5mn bpd. Together with the Kirkuk-Ceyhan pipeline (an estimated capacity of 1.6mn bpd), these will likely reduce Iraq’s systemic risk.

- Kuwait extended its USD 2bn deposit with the Central Bank of Egypt for an additional year, providing a critical buffer for Egypt’s foreign exchange reserves during the current crisis. This extension reflects a broader GCC strategy to prevent regional fiscal contagion and stabilize the balance of payments for strategic allies.

- The ongoing conflict has resulted in record-high Oman-Saudi border trade given the necessity of land-based logistics corridors to bypass maritime chokepoints. The value of goods crossing the border almost trebled to OMR 320mn in Mar (Feb: OMR 112mn). The conflict accelerated the integration of the two nations’ customs and transport networks, making the Empty Quarter crossing a vital artery for GCC trade. This record trade volume will likely lead to a new wave of investment in border-adjacent industrial zones.

- The Qatar Free Zones Authority reinforced its investor support measures – including financial incentives and enhanced logistical support – to ensure business continuity for the 14,500 foreign firms currently operating there. By shielding foreign capital from the geopolitical fallout of the war, Qatar is positioning its free zones as a resilient global hub.

- Saudi Arabia and Syria are exploring ways to improve bilateral cooperation in land transport to create a more resilient trans-regional trade routes between the Gulf and the Mediterranean, bypassing maritime chokepoints. This is likely to restore major trucking and rail links, leading to regional logistics integration and economic stabilization.

- The Central Bank of the UAE disclosed that its support package benefitted 60,559 individuals, 4,335 SMEs and 485 corporates to the tune of AED 6.2bn (USD 1.69bn). This liquidity package – which includes loan deferments, interest relief and fee waivers – ensures that banks can continue to support the private sector, providing a safety net that maintains credit flow to industrial and construction projects.

- The UAE is in discussions with the US to establish acurrency swap line, according to the trade minister. Such an agreement would provide the UAE with an uninterrupted dollar-liquidity buffer, reduce transaction costs and exchange-rate risk while ensuring that the local financial architecture remains resilient during periods of extreme volatility. This move underscores the deepening financial and strategic ties between the two countries.

- UAE’s trade resilience is largely dependent now on the eastern ports of Fujairah and Khor Fakkan, which act as a lifeline outside the Strait of Hormuz. These ports are seeing a massive influx of cargo and bunkering demand: Khor Fakkan terminal operator Gulftainer stated that the number of containers handled jumped roughly 25-fold. Rapid infrastructure expansion at these ports is likely to become a primary policy mandate, potentially making them a permanent exit point for GCC energy and industrial exports.

- UAE announced plans to develop a dedicated defence industrial free zone in Abu Dhabi to boost local manufacturing and national readiness. This initiative aims to localize the defence supply chain, foster technological sovereignty through strategic partnerships with global technology firms and will support UAE’s burgeoning home-grown defence sector.

- An AED 1bn contract has been awarded to build a major desalination plant in Fujairah, a critical step in supporting water security in the country. This facility will utilize a seawater reverse osmosis desalination technology to provide a reliable water supply: the plant has a capacity of 60mn imperial gallons per day and storage equivalent to 18 hours of production. Future water-security investments will likely focus on decentralized, solar-powered plants, that can operate independently of the central grid and maritime chokepoints.

- DP World introduced specialized war risk cover to back its trade routes, ensuring that shipping activity can continue despite the surge in insurance premiums due to the heightened risk environment. Gulf insurance premiums to cover political violence have risen at least 20-fold since the war began. By internalizing this risk, DP World is keeping the region open for trade in essential commodities.

- ADNOC CEO clarified that the UAE’s exit from OPEC was a strategic, value-driven decision and not directed against any specific partner; this also allows the UAE to prioritize its national industrial goals over traditional multilateral constraints. Separately, ADNOC revealed plans to embark on shale-style oil and gas projects to aggressively monetize its massive unconventional reserves. This allows for a more flexible production strategy, signals a pivot toward a more autonomous and supply-side energy policy and is expected to trigger a significant increase in upstream investment.

- Gulf airlines are witnessing a gradual and uneven recovery in traffic as the regional conflict continues to disrupt traditional flight corridors and passenger confidence. As of early-May, UAE-based Emirates is back at nearly 84% of its pre-conflict flight volume while Qatar Airways and flydubai are at 51%. Carriers are navigating a high-cost environment characterized by surging jet fuel prices and the logistical necessity of rerouting around restricted airspace. While long-haul transit remains resilient, travel into the region is weak and impacting tourism revenues.

- North African destinations, including Egypt, Tunisia and Morocco, are gaining tourists amid the conflict that has affected the GCC countries. Revenue per available room (RevPAR) was up between 20 and 50% in Marrakesh and Agadirin Morocco and the Egyptian resort of Sharm El Sheikh; Tunis saw RevPAR more than double and occupancy rise to 32% (from 16% last year). This (likely temporary) tourism shift provides a vital source of foreign exchange for North African economies that are also struggling with the wider regional fallout.

Macroeconomic Developments in the MENA region

- PMI in Egypt declined to 46.6 in Apr (Mar: 48.0), as orders books and output fell sharply amid weak demand conditions (the steepest drop was seen in manufacturing and wholesale & retail). Input prices rose at sharpest pace since Jan 2023 while firms raised their selling prices at the fastest rate since Aug 2024.

- Economic growth in Egypt is forecast at an ambitious 5.4% for the fiscal year 2026-27, with top contributions from manufacturing (29%), wholesale & retail trade (11.3%), tourism (9.3%), construction (7.2%) and agriculture (7%). Growth target for 2029-30 stands at 6.8%.

- Egypt’s urban annual inflation eased to 14.9% in Apr (Mar: 15.2%), supported by the base effect and previous currency stabilization efforts. Food and beverage costs rose to a 10-month high of 6.7% (from 5.8%) while housing & utilities ticked up (38.5% from 35.3%) due to higher electricity costs; transport costs eased but remained high (29.2% vs 39.4%).

- Egypt’s government is preparing for the IPOs of eight state-owned companies on the EGX, spanning the energy and industrial sectors. These listings are a necessity for deepening local capital markets and providing a transparent tool for Egypt’s divestment mandate.

- Egypt’s net foreign assets plunged by USD 6.07bn to USD 21.34bn in Mar, reflecting the high energy costs, weaker tourism and increased capital outflows during the period of extreme geopolitical volatility. Commercial banks’ foreign assets tumbled by about USD 3.59bn while assets at the central bank slid by USD 697mn.

- Egypt approved a revised mining investment law designed to streamline the licensing process: incentives include reducing the mining site lease by 60% for investors and lowering the required minimum government shareholding in the project to 10% from 25%. These reforms are expected to trigger a significant exploration boom and increase the mining sector’s contribution to GDP to 6% by the end of 2030 (from 0.5% currently).

- Transit trade in Egypt surged 35% yoy in Q1 2026, according to the minister of finance. He disclosed that the government is accelerating customs facilitation measures and leveraging infrastructure upgrades to position Egypt as a global logistics hub given that its ports currently offer a safer alternative maritime route in the region. Separately, trade deficit widened by 87.5% yoy to USD 5.1bn in Feb, driven largely due to imports growth (24.7% to USD 9.3bn) outpacing exports growth (11.6% to USD 4.2bn).

- The Suez Canal Economic Zone attracted USD 16bn in investments from 28 countries over the past four years, solidifying its status as a global logistics and manufacturing hub. Investment volume stands at USD 7.1bn during the current fiscal year so far, compared to USD 4.4bn in FY 2024-2025. About 172 factories are now under construction.

- Egypt signed a major deal with Trafigura to establish a large-scale aluminium smelter, integrating the country into the global metallurgical supply chain, and with an aim to double annual production (to 600k tonnes). The deal is expected to create thousands of specialized jobs and localize high-value industrial processing.

- Lebanon’s PMI remained in contraction territory in Apr (48.2) as export orders plunged to a six-year low of 30.0 while domestic orders ticked up due to the ceasefire. Inflationary pressures stood at their highest since early 2023: purchase price inflation accelerated to a 37-month high and the uptick in selling prices was the most since Mar 2023.

Macroeconomic Developments in the GCC

- Kuwait’s PMI stayed below-50 in Apr, unchanged at 46.3, as new orders fell more quickly versus Mar that was reflected in lower output, employment and purchasing activity declined for the second month in a row. The 12-month ahead business sentiment slipped to the lowest since Jun 2020.

- World Bank underscored that Oman’s structural reforms have increased its resilience: growth is forecast at 2.4% in 2026, thanks to a 3.5% non-oil sector expansion. Increased fiscal buffers (via expanded VAT revenues), industrial diversification and strategic logistics outside the Strait of Hormuz (in the backdrop of the war) have lowered Oman’s risk profile.

- Oman commissioned a comprehensive study for a large-scale hydrogen-to-power project, indicating a shift toward domestic green hydrogen integration. The assessment is for a new independent power project capable of operating on up to 100% hydrogen, with an indicative generation capacity in the range of 800 to 1,000MW.

- Qatar’s non-oil sector PMI increased to 46.4 in Apr (Mar: 38.7), as stocks of inputs contracted at the steepest rate since May 2020, total business activity declined and overall price pressures accelerated to a 16-month high. The ongoing ceasefire lowered the degree of pessimism: 29% of survey respondents reported negative sentiment with respect to the Future Output Index, down sharply from 70% in March.

- QatarEnergy extended its force majeure on LNG deliveries to Italy’s Edison, citing the continued blockade and physical constraints at export terminals. The company will not delivery two cargoes, on top of the 10 cancelled since the beginning of the conflict in the Middle East, highlighting the sustained disruption to the global gas supply chain. Edison received only 1.6 billion cubic metres (bcm) of gas of LNG from Qatar in Q1 (the contract is to supply 6.4bcm per year).

- Despite the war, Qatar’s international reserves increased 2.23% yoy to QAR 202.37bn in Apr; in addition, gold holdings grew by QAR 16.61bn to QAR 61.33bn and strong foreign bank holdings ticked up to QAR 23.65bn. The Central Bank also successfully utilized its liquid buffers to manage external volatility and ensure uninterrupted import financing.

- The ongoing conflict has slowed Qatar’s residential and commercial property growth, with buyers adopting a wait-and-watch approach: residential sales were down 11% mom to only 154 sales in Mar of which one-third were land sales. Qatar sold 675 residential units at around QAR 435 (USD 119.50) per square foot in Q1 2026.

- S&P Global stated that Qatar’s sovereign assets and massive net foreign asset position are sufficient to weather the long-drawn-out conflict. The low external debt-to-GDP ratio and profitability of its upstream assets provide a deep cushion against geopolitical scarring.

- Saudi Arabia posted a budget deficit of SAR 125.7bn in Q1 2026, more than double versus a year ago & the largest quarterly deficit on record. Total expenditures climbed 20% yoy to SAR 386.7bn, driven by a 26.0% rise in military spending (to SAR 64.7bn) and a massive three-fold increase in subsidies (to SAR 17.5bn) to mitigate conflict-driven cost-of-living pressures. Total revenues edged down by 1.0% yoy to SAR 261bn, hampered by a 3.0% decline in oil income (to SAR 144.7bn) as the blockade of the Strait of Hormuz and regional infrastructure damage impacted export volumes. Non-oil revenues rose 2.1% to SAR 116.3bn, supported by taxes on goods and services (+4.7% yoy to SAR 74.9bn). This highlights the success of continued efforts to diversify the fiscal base beyond crude oil.

- The Saudi National Debt Management Center had already secured 90% of its 2026 funding requirements pre-war, a move that insulates the country from rising global risk premiums. NDMC plans to use private channels and local markets as primary funding sources, should additional financing be required.

- Saudi Arabia’s PMI returned to growth in Apr (51.5 vs Mar’s 48.8) as domestic demand recovered from the initial shocks of the conflict; both new orders and output expanded supported by consistent government infrastructure spending, while export orders remained dampened (falling at the fastest rate on record, since 2009). Employment fell the first time in two years while price pressures were evident on both inputs (fastest rate of increase) and output charges (rose at the sharpest pace since Aug 2009).

- Saudi Arabia’s non-oil industrial activity grew by 1.4% mom and flat yoy in Mar, despite the overall industrial production down 22.2% mom and 14.1% yoy. Oil production fell by 30.8% mom and 20.0% yoy while manufacturing edged up by 1.1% mom. This momentum could make the manufacturing sector one of the primary drivers of 2026 non-oil GDP.

- Pointing towards the return of market confidence, the first Saudi IPO since the start of the conflict (Dar Albalad for Business Solutions Company, an IT services provider) is set to raise USD 55mn. The book-building process for the institutional tranche was oversubscribed 66.6 times, suggesting that institutional risk appetite is beginning to normalize. A successful offering will likely reopen the IPO window for a backlog of industrial and tech firms, providing a boost to Tadawul liquidity in Q3.

- The Chairman of the Saudi Capital Market Authority (CMA) disclosed that the CMA continues to process a high volume of domestic listing applications, reflecting a robust pipeline of private firms seeking capital. The authority plans to prioritise local companies and entrepreneurs to list on the market, to counter foreign companies’ capital outflows. A deeper equity market will likely lower the long-term cost of capital for Saudi firms.

- Saudi Public Investment Fund (PIF) raised a record USD 7bn in the debt markets (via its first Murabaha credit facility) to fund its various Vision 2030 development projects. This successful, more than three times oversubscribed issuance confirms that the PIF remains a major borrower in international markets.

- Saudi Arabia issued a significant number of new mining licenses in 2025, up 220% yoy, while the total investments jumped to SAR 44bn. Focusing on critical industrial and precious metals, total number of factories stood at 12,946 at end-2025, including 10,394 operational facilities employing around 903,547 workers.

- Reuters reported that Saudi Arabia and Turkey are reportedly set to scrap mutual visa requirements for some citizens, marking a resumption of diplomatic and economic integration. Removing travel barriers more widely will lead to a surge in bilateral tourism and cross-border investment flows during rising geopolitical tensions.

- PMI in the UAE remained in expansionary territory in Apr, at 52.1, though the growth momentum eased (Mar: 52.9) as the conflict impacted regional sentiment and supply chains. Lengthening delivery times and rising input costs (highest since Jul 2024) dampened manufacturing growth; new orders grew at the slowest pace in more than five years (52.5 from 54.5) and selling prices ticked up the most since June 2011.

- The UAE’s proactive Comprehensive Economic Partnership Agreement (CEPA) strategy has resulted in non-oil trade growing past the USD 1trn mark in 2025. UAE attracted 251 FDI projects in the industrial sector between 2015 and 2024 representing capital commitments of almost USD 33bn and the contribution of the In-Country Value programme exceeded AED 473bn (this was redirected into the national economy). The ramping up of global trade links will boost UAE’s industrial exports.

- The UAE expanded its industrial procurement programs to approximately USD 49bn to bolster domestic manufacturing.This procurement-led growth strategy ensures that local manufacturers (more than 5000 products) have guaranteed buyers within the national industrial ecosystem. Separately, the UAE announced it will provide up to AED 18bn in funding to support the rapid expansion of its industrial sector and manufacturing capabilities. This capital injection is geared towards increasing production, adopting advanced technologies and strengthening supply chains.

- The UAE Ministry of Human Resources and Emiratisation has set a strict mid-year deadline of June 30th for companies (with 50+ employees) to meet their H1 Emiratisation targets. This policy aims to integrate more nationals into the private sector workforce and companies failing to meet these quotas face significant financial penalties.

- Dubai International Airport handled 18.6mn passengers in Q1 2026 (+20.6% yoy) though only 2.5mn passengers went through in Mar (-65.7%). Between late-Feb to end-Apr, amid the regional conflict, the airport catered to 6mn passengers, 32k+ flights and 213k tonnes of cargo.

- Dubai’s taxi revenues saw a decline in Q1 (-12% yoy to AED 455mn) as the regional conflict dented passenger performance and transport demand. However, the sector is expected to rebound as maritime and aviation routes begin to normalize during the ceasefire.

Global Macroeconomic Developments

US/Americas:

The latest US macro data point to a gradually cooling labour market coupled with resilient industrial demand and shifting consumer sentiment. Nonfarm payrolls slowed significantly to 115k (down from March’s 185k), though it was the first back-to-back monthly increase in employment in nearly a year; the private sector added 109k jobs showing underlying strength. While the unemployment rate held firm at 4.3% and labour participation remained steady at 61.8%, wage pressures persisted as average hourly earnings ticked up 3.6% yoy (Mar: 3.4%). Non-farm productivity meanwhile eased to 0.8% in Q1 (Q4: 1.8%), though a sharp decline in unit labour costs to 2.3% (from 4.4%) provides a potential buffer against inflationary spikes. On the output side, factory orders grew by a robust 1.5% mom in March (the biggest gain since Nov), yet the goods and services trade deficit widened to USD 60.3bn (Feb: USD 57.8bn), reflecting persistent import demand. The services sector showed signs of moderation, with the ISM services PMI slipping to 53.6 as new orders cooled (53.5 from 60.6), while the housing market remained a notable outlier with new home sales surging 7.4% to 682k. Despite these pockets of activity, consumer morale remains historically low: the Michigan consumer sentiment index fell to 48.2 in May (Apr: 49.8), even as one and five-year inflation expectations eased to 4.5% and 3.4% respectively (from 4.7% and 3.5%).

Europe:

The European economic landscape shows strengthening demand amid persistent production difficulties. Manufacturing PMI in Germany reached 51.4 in Apr (from Mar’s 46-month high) while in the Eurozone itsettled at 52.2, both confirming a baseline of expansion. Data show rising inflationary pressure (input costs), supply chain disruptions and lower production expectations. However, the data reveals a major gap: while German factory orders surged by 5% mom and 6.3% yoy in March, industrial production unexpectedly contracted by 0.7% mom and 2.8% yoy, signalling potential capacity or supply-side constraints. This was also evident in Germany’s trade data, where a 5.1% surge in imports in Mar outstripped a modest 0.5% growth in exports, narrowing trade surplus to EUR 14.3bn. Consumer activity remained relatively steady with Eurozone retail sales up 1.2% yoy, despite a slight monthly dip of -0.1%. Perhaps most critical for policymakers is the sharp rebound in the eurozone’s Producer Price Index, which climbed 3.4% in Mar, marking a significant deviation from the deflationary trends seen in Feb (-3.0% yoy). Amidst these shifts, investor sentiment appears to be turning the corner, as the Sentix index improved to -16.4 in May (Apr: -19.2), suggesting that while the region remains in negative territory, the momentum is slowly shifting toward recovery.

Asia Pacific:

For now, China’s industrial and service engines appear to be in overdrive, with the RatingDog service PMI climbing to 52.6 and exports staging a dramatic 14.1% yoy surge, including an 11.3% rebound in shipments to the US. This trade momentum drove China’s monthly surplus wider to USD 84.8bn, providing substantial economic leverage as President Trump prepares to meet President Xi in Beijing on May 14-15. In the broader region, signals are more sedate: India’s manufacturing PMI moderated to 54.7, while Japan’s labour cash earnings growth slowed to 2.7%, a trend likely to feature prominently in future Bank of Japan policy deliberations. Meanwhile, South Korea is navigating a tightening supply-side squeeze as inflation accelerated to 2.6%. Looking ahead, the focus shifts entirely to the Beijing summit, where any potential deal could fundamentally alter and/or stabilize volatile economic and trade relations.

Media Review:

Markets are banking on the ‘Bliss trade’

https://www.ft.com/content/60f60089-9486-481c-859c-f29b8ccbbd90

UAE’s leap into energy independence and the new oil order: op-ed by Dr. Nasser Saidi

https://economymiddleeast.com/news/uae-leap-into-energy-independence-and-the-new-oil-order/

Financial Stability Risks Mount as Artificial Intelligence Fuels Cyberattacks

![]()