Ceasefire. Regional reconfiguration. Lebanon GDP. Oman & Saudi foreign trade.

Download a PDF copy of this week’s insight piece here.

Ceasefire Illusions, Structural Shocks: Weekly Insights 24 Apr 2026

1. The Ceasefire: Market Euphoria vs. Operational Reality

(a) Geopolitical & Market Context

- The extension of the ceasefire has brought a significant de-escalation of destruction.

- Despite the Strait of Hormuz remaining mostly closed, the US stock markets seem to be in an optimistic mode, driven by a tech story & potential negotiations.

- Brent closed just over USD 105 this week, a jump down from when Dated Brent touched a record USD 144.42 on Apr 7. A geopolitical premium is likely to remain with Iran demonstrating its ability to choke a vital global waterway.

- While fuel costs have dropped, the price spike has already permeated manufacturing & logistics costs globally.

- Central banks will face the underlying dilemma between managing inflation and supporting growth.

(b) Logistical & Infrastructure Hurdles

- More than 10 million barrels per day of products (10% of global supply) is still stranded behind the Strait; a return to normal operations could take months even if the ceasefire holds.

- Physical damage cannot be quickly reversed; to wit, 17% of Qatar’s export capacity that is currently offline.

- Key signals to monitor recovery include the actual daily tanker transit volumes and whether Brent/WTI forward curves continue to price in a supply crunch.

- The crisis is pushing new logistics corridors, land bridges, transport corridors & alternative export pipelines; is also expected to accelerate the push toward renewables (e.g. European demand for rooftop solar since the outbreak of war).

2. Regional Reconfiguration, Strategic Pivot to Asia & New Logistics Corridors

(a) Macroeconomic Vulnerabilities in MENA

- MENA region is navigating unexpected, unprecedented multiple shocks that require deep structural reforms as automatic stabilizers are largely absent.

- Regional defence spending likely to surge further; Saudi Arabia was the third largest recipient of major arms during 2021-2025.

- Energy and food importers face major risks: exchange rate depreciation, capital outflows & potential balance of payments crises.

- Countries with high debt and tighter financial conditions will likely require external intervention from the IMF, World Bank & the AMF.

(b) The Economic Power Shift to the GCC

- Economic and financial power is shifting toward the GCC over time; greater regional integration required.

- Pivot to Asia: Gulf-Asia trade at a record USD 516bn in 2024, with trade between the Gulf & China overtaking trade with Western economies for the first time.

- Intra-regional trade needs strengthening. It is low at 10-15%, while MENA-Developing Asia trade jumped sixfold in 2025 vs 2005.

- Central banks are diversifying reserves into gold & Asian currencies; adopting digital settlement platforms like mBridge to bypass Western corridors, given weaponisation of the USD.

(c) Infrastructure & New Routes

- Strategic derisking involves developing new land-based trade routes and rail networks from East to West across the Arabian Peninsula.

- Saudi Arabia is evaluating an expansion of its East-West pipeline, alongside rehabilitating pipelines through Iraq, Syria & Lebanon.

- The 380km Habshan-Fujairah pipeline remains a critical 1.5 million bpd alternative route bypassing the Strait of Hormuz.

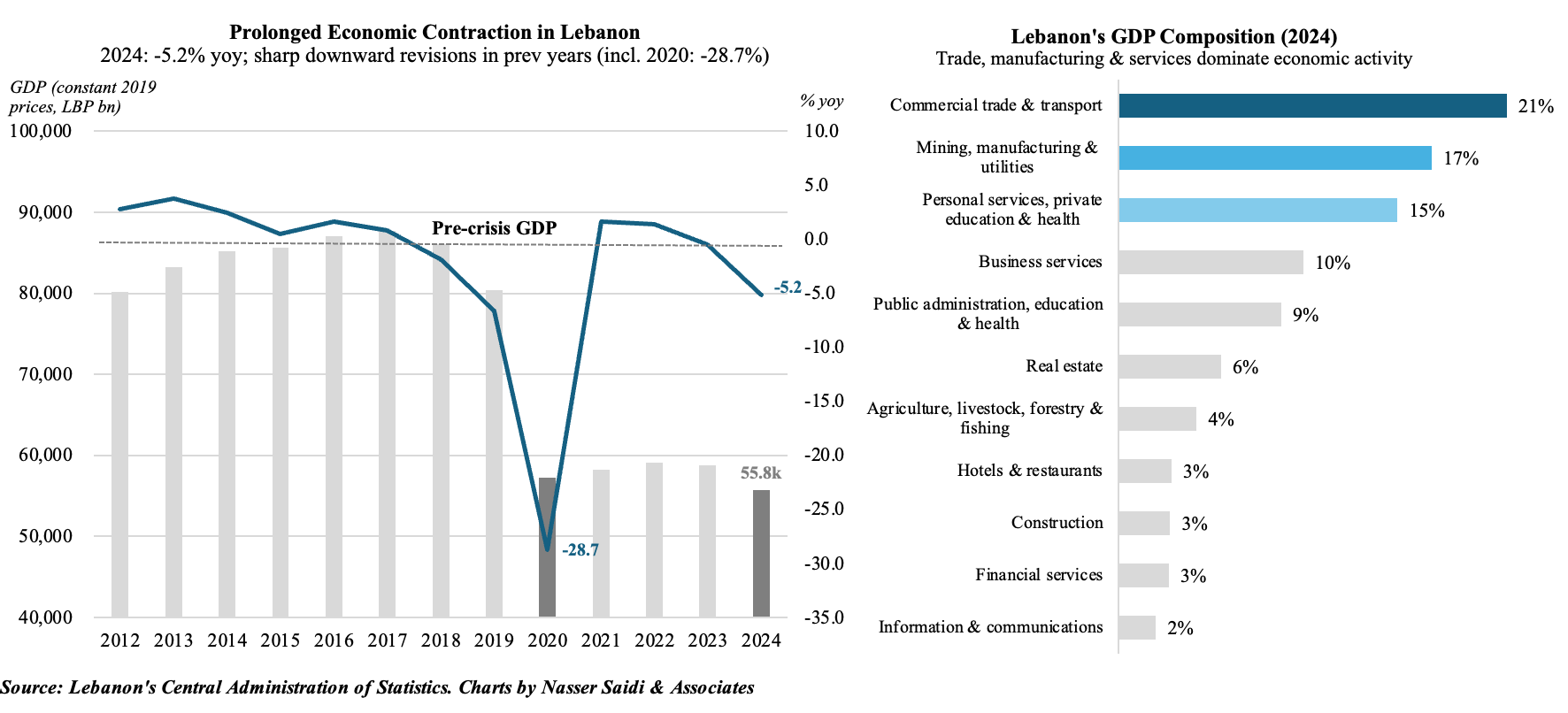

3. Lebanon GDP to plunge up to 20% in 2026; substantial downward revisions to prior years

- Lebanon’s Central Administration of Statistics show significant downward revisions in GDP for 2024 & prior years. The ongoing security crisis will only exacerbate this structural decline.

- Approximately 22% of Lebanon’s agricultural land has been destroyed. The massive infrastructure damage – the final crossing over the Litani River has been destroyed & Israel is creating a 10-km “buffer zone”, and occupying most of the South: territorial structural losses that will delay recovery beyond the end of the conflict.

- Remittances are set to fall (latest available data: USD 6bn, of which around 60% come from the GCC), further endangering the one million+ displaced people who currently lack a formal social safety net. Flight traffic at Beirut airport has plunged nearly two-thirds (vs pre-war); targeting of border crossings like Masnaa has choked customs revenue & export capacity.

- Recovery and Policy Path: (a) recovery is contingent on an permanent verifiable ceasefire; (b) mobilization of national institutional capacities for post-conflict reconstruction; (c) re-engagement with the IMF: A revised macro-fiscal framework is essential to conclude a program with the IMF and restructure the banking sector under current realities.

- Revised statistics showed real GDP contracted by 5.2% yoy in 2024. Nominal GDP was revised to LBP 2,728trn (~USD 30.5bn at an exchange rate of LBP 89,500 to USD. GDP deflator rose sharply (27.4% in 2024), reflecting the ongoing decoupling between nominal prices & real output.

- Covid-affected 2020 was revised down to a 28.7% contraction (prev: -25.9%); 2021 and 2022 were lowered to 1.6% and 1.4% respectively.

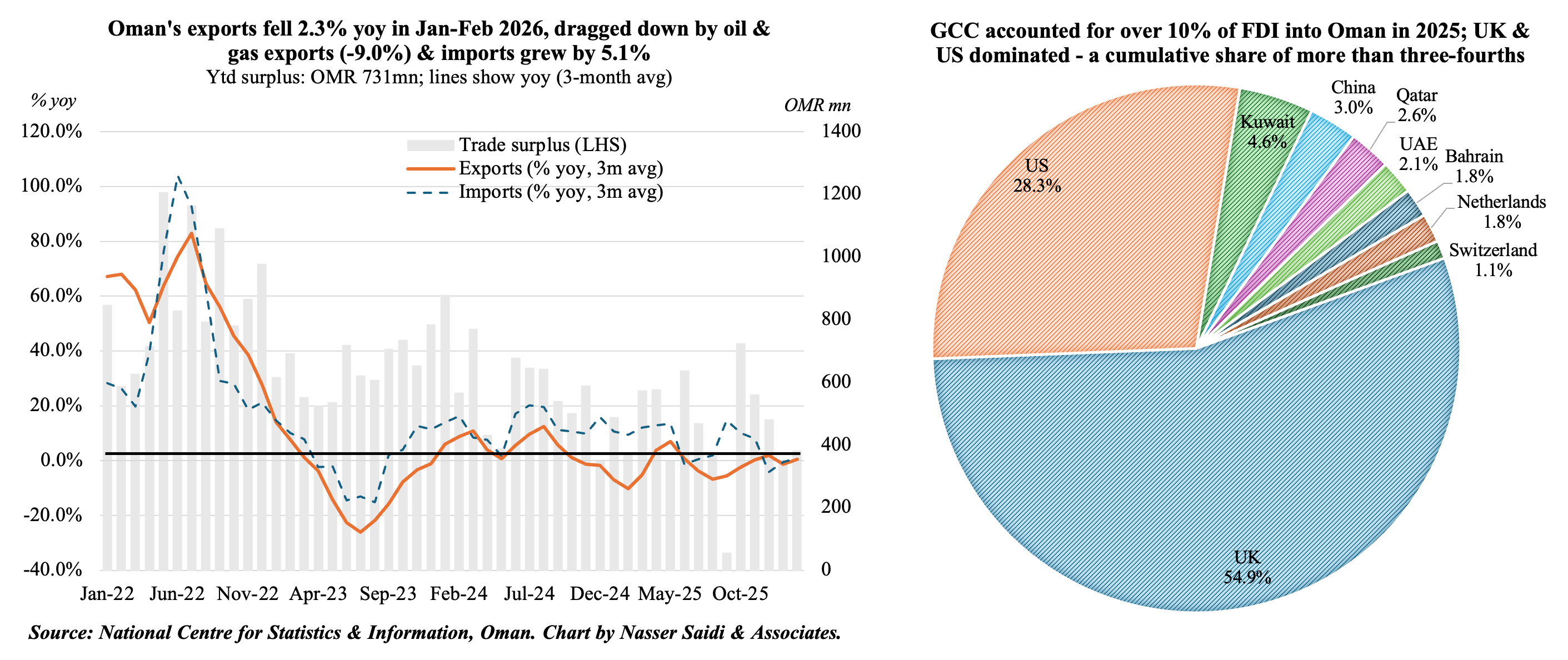

4. Oman’s existing trade links with the GCC likely strengthened by the war in Iran

- Ports in Salalah and Duqm have become key logistics centres during the war in Iran – supporting the GCC.

- Even pre-war, Oman’s re-export growth was enabled by growth in its SEZs (e.g. Duqm) and increased rail & road connectivity with Saudi and the UAE. UAE was Oman’s largest non-oil trading partner, with gains in direct non-oil exports (37.5% to OMR 258mn in Jan-Feb) & re-exports (1.7% to OMR 80mn). Re-exports to KSA surged 389.9% to OMR 55mn.

- Oman’s non-oil exports grew by 11.4% yoy to OMR 1.1bn in Jan-Feb, thanks to an acceleration in industrial sectors such as base metals.

- Merchandise exports saw a decline (-2.3% yoy to OMR 3.6bn in Jan-Feb 2026) due to a 9.0% drop in oil and gas exports; imports grew by 5.1%; trade surplus was a healthy at OMR 731mn ytd.

- FDI in Oman surged 8.1% yoy to OMR 31.4bn at end-2025.

- The most popular sectors that attracted FDI were oil & gas exploration (81% of total), manufacturing (8.5%), financial intermediation (4.8%) and real estate (1.9%) which together accounted for 96.1% of the total. Fastest growth was recorded in construction (11.1%) and oil & gas exploration (11.0%).

- UK topped the list of countries with investments in Oman (OMR 16.4bn, or 52.3% of the total and up 10.5% yoy) followed by the United States (OMR 8.5bn) and Kuwait (OMR 1.36bn).

- Regional investment seems to be strong, with Kuwait, UAE, Qatar & Bahrain accounting for 10.6% of FDI in Oman. Fastest growth was seen in FDI from China (+11.2% yoy to OMR 887.3mn), reflecting a broader strategic engagement with Asia.

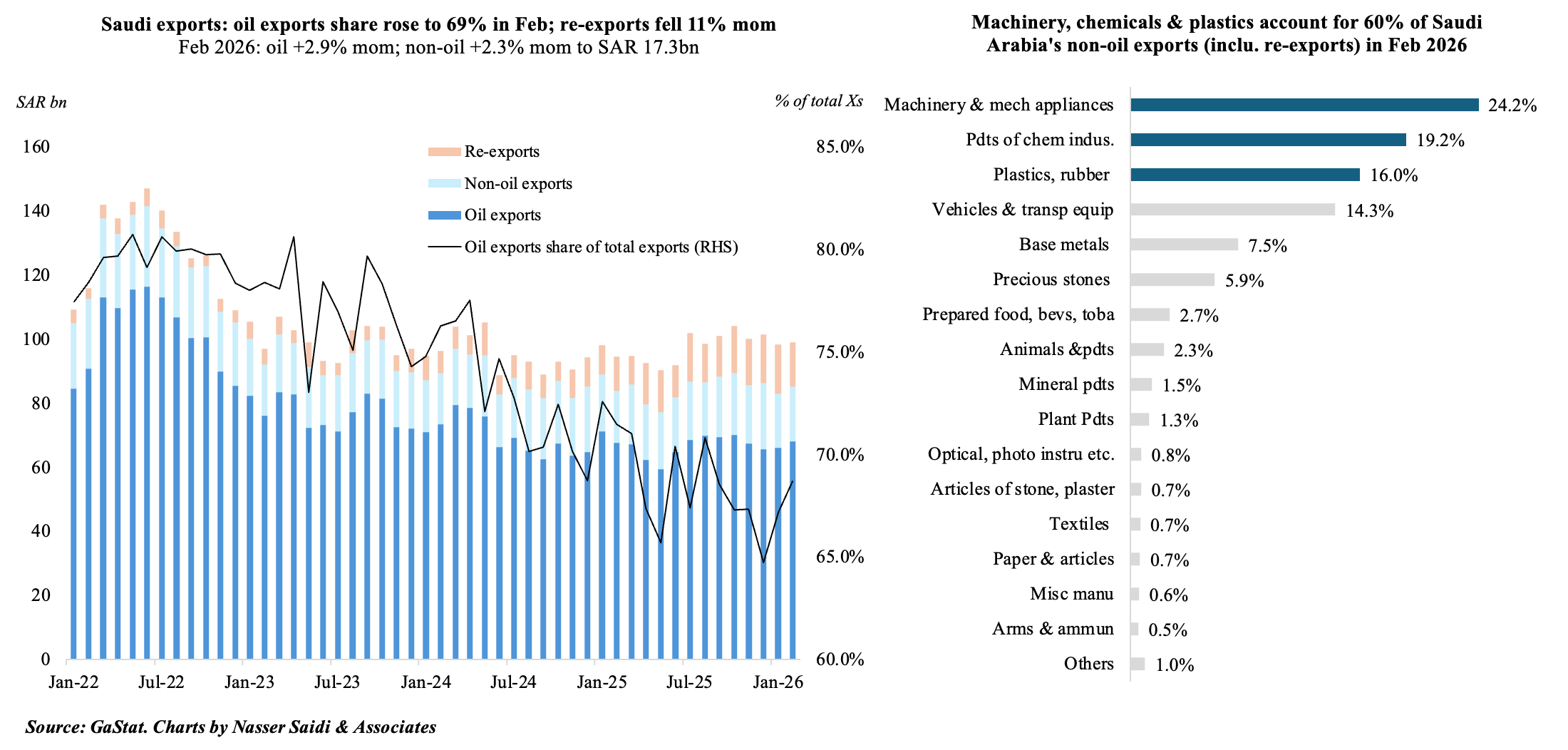

5. Saudi non-oil exports share at 31% in Feb; finalizing alternative logistics corridors

- Total merchandise exports increased modestly by 4.7% yoy to SAR 99.1bn in Feb 2026, with oil exports rising only 0.6%. The share of oil in total exports inched up to 68.7% in Feb. Non-oil exports rose strongly, increasing 15.1% year-on-year to SAR 31bn. Re-exports were a key component of non-oil exports: though it slipped 10.8% from Jan’s record high, it was up 28.5% yoy.

- Machinery was the largest segment of total non-oil exports (24.2%; this also made up over half of re-exported goods), followed closely by chemicals & products (19.2%) and plastics, rubber & articles (16.0%). These are the high-value industrial inputs required for manufacturing.

- Imports grew faster than exports (+6.6% yoy), leading to a slight narrowing of the trade surplus (-1.0% yoy to SAR 22.95bn).

- China remained the top trade partner (largest export destination and import source) while UAE & India were also key export markets.

- UAE alone accounted for 31.6% of Saudi non-oil exports; share of non-oil exports to GCC was 40%. Jeddah Islamic Seaport and King Abdulaziz International Airport handled a combined 31.7% of non-oil exports in Feb.

- With the Strait of Hormuz largely closed, the East-West Pipeline continues to be the main alternative corridor. Though attacked earlier this month, it was ramped to its full 7 million barrels per day (bpd) capacity, with full pumping functionality restored by April 12 after repairs. Saudi also launched a new 1700km railway freight corridor to Jordan, establishing a critical alternative land route for non-oil trade.

- KSA is also reinventing NEOM as an alternative logistics hub, part of the wider Red Sea logistics corridor to bypass the Strait of Hormuz. This is being used by importers from several European countries according to Neom.

Powered by:

![]()