Download a PDF copy of the weekly economic commentary here.

Markets

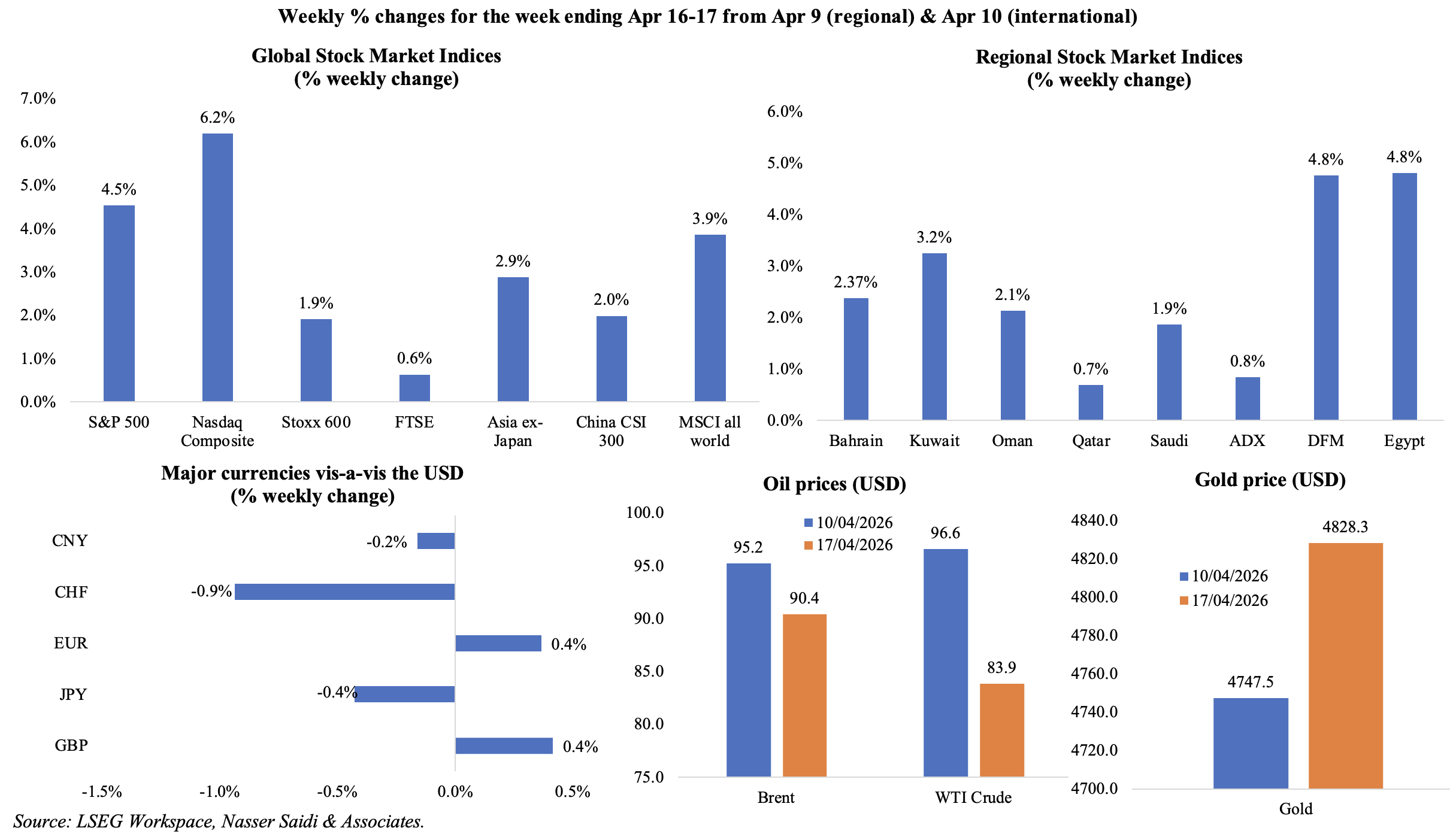

Global equity markets reflected optimism at the end of last week on Iran’s announcement about the Strait of Hormuz being open while the ceasefire was in place and news about a deal to end the war “soon”. US markets S&P 500 and Nasdaq posted record closes and markets across Europe and Asia closed higher; even Japan’s Nikkei closed at a record (despite concerns of energy imports from the Middle East). In the Gulf, Dubai surged to a six-week high as traders priced in a potential de-escalation of the Iran conflict; its 4.8% gain was the most in nine months.

The USD edged lower against the EUR, GBP and JPY as peace hopes diminished its safe-haven appeal. Oil prices dropped by more than 9% on Friday on the prospect of revived supply, though the IEA warned that energy output recovery would take about two years to recover. Gold price continued its ascent, posting its third weekly gain on its safe-haven status.

With mixed messaging over the weekend (opening and closing of the Strait, threat to resume bombing if no peace deal was reached) and US seizure of an Iranian vessel, hopes for a deal hang in the balance once again. Equity markets in Asia and Europe this morning have given up some of the gains clocked in last week and oil price was up more than 5% on rising tensions.

Economic Consequences from the conflict in the Middle East & Policy Responses

The global economic landscape continued to process cautious diplomatic optimism and severe scarring resulting from the conflict with Iran. Statements from the Trump administration on Friday suggested “good news” regarding a potential de-escalation and Iran announced the opening of the Strait of Hormuz being open; more than 20 vessels passed the Strait of Hormuz on Saturday (Source: Kpler), the highest number of ships crossing the waterway since March 1. However, the latest news reveals a volatile mix of diplomatic signals and maritime tension between the US and Iran. The White House announced that it is sending a delegation to Pakistan this week. However, the US seizure of an Iranian vessel has thrown a spanner in the works – Iran is yet to confirm any such plan. The absence of a potential peace deal has left the international community stranded. The global economy has been fundamentally reconfigured by the war via energy infrastructure destruction, trade and supply chain disruptions and rising inflation expectations and for policymakers and investors, peace remains elusive for now.

The IMF has slashed its growth forecasts for the global economy, emerging economies and Middle Eastern exporters, warning that the fallout remains profoundly uneven. Global economic growth is forecast to slow to 3.1% in 2026 (2025: 3.4%) before ticking up to 3.2% in 2027 – figures that remain well below pre-pandemic averages. However, in a severe scenario, involving broader & longer regional instability, IMF warns growth could be constrained to 2.0% this year and next. For oil and gas exporters most exposed to the hostilities, the IMF projects significant economic contractions in 2026: Iran (-6.1%), Iraq (-6.8%) and Qatar (-8.6%) – driven by damage to energy infrastructure and the functional closure of the Strait of Hormuz. Saudi Arabia, UAE and Oman are expected to maintain positive growth though at reduced rates: we believe that the forecasts are on the optimistic side. The toll on energy is particularly staggering: Rystad Energy estimates that damage to regional energy assets could reach USD 58bn; the IEA warned that even if a ceasefire holds, the loss of energy output will take approximately two years to fully recover, as the strikes on critical processing hubs have created a structural supply gap that cannot be closed through diplomatic gestures alone.

In response to these supply shocks, the global financial architecture is undergoing a strategic pivot. Indian refiners have reportedly begun settling Iranian oil payments in yuan via ICICI Bank, signalling a move toward non-dollar trade as a hedge against the weaponization of finance. Central banks in affected emerging market economies will face a difficult decision regarding rates amid rising risk of stagflation (Philippines and Indonesia are likely hold rates steady this week on weak growth); the former US Treasury Secretary, Janet Yellen, expects that a Fed rate cut is possible this year. Meanwhile the IMF has cautioned governments against broad fuel subsidies that could further strain fiscal deficits. The private sector is being affected across the globe as well: firms are delaying IPOs and slashing dividends as market volatility persists.

Separately, the UN has called for urgent investment to mitigate the humanitarian crisis (USD 6bn investment could prevent 32mn persons from slipping into war induced poverty), the White House is seeking USD 1.5trn in annual military budget (no estimate was offered for the cost of war so far). For now, Asia remains the world’s growth engine (China’s Q1 GDP growth a case in point), but that engine is running on a leaner mix. Success will be defined by the ability to balance industrial output with domestic demand while operating under a new global energy map.

Countervailing Regional Policies & Developments

- Bahrain’s central bank issued directives for loan instalment and credit card payment deferrals (both principal and interest) for a period of three months, to support individuals and corporates.This is backed by the BHD 7bn (USD 18.6bn) in liquidity support extended via a repo facility as well as reduced reserve requirements and key liquidity ratios. However, Moody’s shifted Bahrain’s outlook to “negative” from “stable”, citing the risks posed by the ongoing regional conflict on top of the country’s weak fiscal and debt indicators.

- Iran plans to allocate a portion of its oil revenues specifically for the reconstruction of energy assets damaged in recent attacks, according to the oil minister. He also stated that oil facilities continue to operate and that oil exports were not halted “even for a single day” including at key export hubs such as Kharg Island.

- In a positive signal, Iraq’s oil ministry expects oil exports to resume from all fields within days, potentially easing global supply constraints. Reuters reported, citing other sources, that southern oil exports resumed Friday after more than a month of pause (due to shipping disruptions) and that one tanker had started loading crude.

- Lebanon and Israel began a ten-day ceasefire on Thursday to end six weeks of conflict, and as it holds, Lebanon is in talks with the IMF for between USD 800mn to USD 1bn in rapid financing for budget support and humanitarian response. Lebanon’s President, in a televised address, stated that the ceasefire should be transformed into “permanent agreements”.

- Oman approved a OMF 50mn (USD 130mn) financial aid package for farmers to ensure domestic food security amidst supply chain challenges and disruptions. This will also support the setting up of regional food depots to establish a secure supply chain to its GCC neighbours via land (bypassing the maritime channels). The warehouses will be ready by this week and will connect with the Hafeet railway (that Oman and UAE began building last year).

- Saudi Finance Minister cautioned that it would take significant time for oil-producing nations to ramp up output to pre-war levels. This is compounded by forecasts that Saudi crude sales to China could halve in May. He stated that unless there was a durable de-escalation in hostilities, insurance companies would not feel comfortable backing shipments – another major challenge.

- UAE and Jordan are advancing a USD 2.3bn Aqaba Port Railway project: the is a 360-km network connecting the facility with major phosphate and potash production sites. While financial close is expected by early next year, construction is likely to take around five years.

- Abu Dhabi, Qatar and Kuwait successfully raised close to USD 10bn through private bond sales since the start of April, reported FT. Abu Dhabi’s deals (USD4.5bn in Apr) have raised its international bond borrowing so far this year to USD 8bn versus just over USD 3bn in 2025. While Saudi has yet to disclose any post-war deals, many state-owned banks in the GCC have raised funds via private placements of bonds and other short-term debt. Though the war had pushed up CDS spreads, a notable decline since the ceasefire suggests returning investor confidence in the region’s ability to manage its debt obligations.

- AD Ports is in talks to leaseEgypt’s Red Sea oil storage facilities for crude oil and petroleum products, reported Asharq Business, a move that strengthens the UAE’s alternative logistics network as the Strait of Hormuz remains nearly closed. An agreement is expected before end-Q2 about the number and location of storage tanks plus lease duration and terms.

- In response to the disruption of traditional maritime routes, Iraq is actively seeking torevive its four-decade-old oil pipeline through Saudi Arabia. This strategic move aims to bypass the Strait of Hormuz, providing a hardened land-based export route to the Red Sea, which is essential for ensuring supply continuity and minimizing geopolitical risk premiums for Iraqi crude. Iraq has already started transporting fuel oil through Syria.

Macroeconomic Developments in the MENA region

- Egypt’s economy demonstrated robust momentum with 5.3% growth in H1 FY 2025-26, though the planning minister projects a slight cooling to 4.8%–5.0% in Q3 amid heightened global uncertainty. He also stated that the overall budget deficit narrowed to 5.2% of GDP during Jul-Mar, down from 6.0% in the previous fiscal year, and primary surplus stood at 3.5% of GDP (thanks to a 29% surge in tax revenues). The IMF has praised these efforts, with the IMF MD stating that economic reforms have helped it absorb external pressures and that it “is now in a better position to face this shock”. She stated that “we see Egypt as one of the good examples of a country that has gone through difficult reforms, has built responsible policies, and is acting in a way that helps people that most need this help”.

- Central bank data showed Egypt’s current account deficit narrowed by 13.6% to USD 9.5bn in Jul-Dec 2025 (H1), thanks to a 28.4% jump in net unrequited current transfers as well as increased Suez Canal and tourism receipts, strengthening the nation’s external buffer

- S&P Global Ratings affirmed Egypt’s “B/B” rating with a stable outlook, reflecting strong momentum in macroeconomic reforms and stronger external buffers amid risks from regional geopolitical tensions. It also warned that any reversal of key reforms (particularly exchange rate flexibility) could result in a downgrade.

- Egypt has initiated the temporary listing of 10 petroleum companies on the EGX, a move designed to deepen capital markets and accelerate the state’s IPO program.

- Fitch Ratings ranked Egypt third in the MENA region (among 18 others) for investment openness, highlighting its improved regulatory environment for FDI. Egypt aims to attract around USD 60bn in FDI between 2026 and 2030, a target which Fitch describes as achievable (Egypt has usually attracted USD 9bn to USD11bn annually, excluding mega-projects).

- To mitigate the social impact of structural reforms, Egypt’s FY 2026-2027 budget has allocated EGP 823.3bn (USD 15.6bn) for social protection, up 12% yoy. Of this AED 175.3bn has been set aside for food subsidies (10% yoy, benefitting 60mn persons) while electricity subsidies jumped 39% to EGP 104.2bn. Egypt will also raise the minimum income for state employees to EGP 8,000 starting Jul, bringing wage allocations to a total EGP 821bn. This targeted spending is crucial for maintaining domestic stability while the government continues its path toward fiscal sustainability and debt reduction.

Macroeconomic Developments in the GCC

- Bahrain’s real GDP grew by 4.6% yoyin Q4 2025, with non-oil GDP growth accelerating 7.4%, amid a 12.3% drop in crude oil & petroleum activity. Overall GDP grew by 3.5% in 2025: oil-related activities contracted 0.3% while the non-oil sector surged by 4.1%. Financial and insurance activities was the largest contributor to GDP (17.6%) followed by manufacturing (15.1%) and public administration (8.4%).

- Consumer price inflation in Oman rose 3.6% yoy in Mar (Feb: 2.0%), driven by sharp increases in food & non-alcoholic beverages (4.3% from 2.8%) and transport (9.4% from 0.2%) while other categories such as miscellaneous goods & services and restaurants & hotels remained high at 13.8% and 5.8% respectively. On a monthly basis, prices increased by 1.3%, the highest in nearly five years, following a 0.2% rise in Feb.

- Total FDI stock in Oman accelerated by 8.1% yoy to OMR 31.38bn (USD 80.5bn) by end-2025, with investments focused on the oil & gas (OMR 25.41bn) and manufacturing (OMR 2.67bn) sectors. UK remained the largest investor into Oman, accounting for 52.3% of total FDI (OMR 16.42bn), followed by the US (OMR 8.45bn) and Kuwait (OMR 1.36bn).

- Hotel revenues in Oman jumped 18.5% yoy to OMR 69mn (USD 179.2mn) by end-Feb 2026, despite a slight decline in total guest numbers (-3.6% to 439k). Though domestic visitors as well as those from the GCC fell by 5.3% and 18.4% respectively to 129.7k and 22k, Asian hotel guests grew by 4.5% to 61.5k.

- Oman is advancing its green aluminium projects in the Duqm SEZ: this includes a 530k tonnes per annum (tpa) capacity smelter backed by CMOC Group Limited of China, the Geely Green Aluminium Project and the Pearl Green Iron and Aluminium Project. By integrating low-carbon energy (e.g. green hydrogen) into heavy industry, Oman is positioning itself to meet the growing global demand for sustainably produced materials.

- Oman signed aUSD 130mn contract for the Muscat Airport City development: this project is designed to create an economic zone around the Muscat’s main gateway, to support tourism growth and attract further investment in retail and hospitality.

- Total assets in the Qatari banking sector reached QAR 2.173trn (USD 596.9bn) in Feb 2026; total assets have expanded 5% over the past five years, underscoring the sector’s liquidity and stability.

- The average value of real estate transactions in Qatar surged by 35% yoy in Q1 2026, driven by growing activity in higher-value assets and sustained demand for luxury and premium residential and commercial assets.

- Qatar’s upstream outlook was further boosted by a significant hydrocarbon discovery in Congo, where QatarEnergy holds a strategic 15% stake, diversifying its international production portfolio. This discovery – equal to about 100mn barrels of recoverable resources when combined with another recent find nearby in the same licence area – exemplifies Qatar’s strategy of internationalizing its energy portfolio to mitigate domestic geographic risks.

- Saudi inflation rose slightly to 1.8% yoy in Mar (Feb: 17-month low of 1.7%).Housing and utility costs were up 3.9%, but eased compared to Feb’s 4.1%, stemming from actual rents (4.8% from 5.1%). Prices of insurance and financial services ticked up (2.1% vs 1%) as did recreation, sport and culture costs (2.0% vs 1.8%). Wholesale price index rose 3.3% in Mar, driven mainly by a 6.4% increase in prices of other transportable goods, excluding metal products, machinery, and equipment.

- Saudi Arabia issued 221 new industrial licenses during Feb, according to the National Center for Industrial and Mining Information, while 112 new factories started production. This will not only boost localized manufacturing and allow the economy to be insulated from global trade shocks but is also together expected to create 1995+ job opportunities in the country.

- Saudi Arabia announced a USD 3bn deposit with Pakistan’s central bank and extended for an unspecified period an existing USD 5bn deposit to help the latter support its foreign reserves and balance of payments.

- Saudi Arabia awarded over SAR 15.6bn (USD 4.2bn) in contracts in war-affected March, up 45.8% mom, reflecting ongoing large-scale infrastructure and real estate developments under Vision 2030. Building and construction projects accounted for nine of the 11 contracts awarded in Feb, and the bulk of total value (SAR 15.5bn).

- The Public Investment Fund (PIF) has set a new five-year strategy. The investments will be grouped into three: a Vision Portfolio focused on domestic projects that can attract foreign capital; a Strategic Portfolio managing key national assets; and a Financial Portfolio covering global investments. Six sectors that will form PIF’s investment focus include tourism, urban development, advanced manufacturing, industrials & logistics, clean energy, water & renewables infrastructure and Neom. Significant capital injections continue, including an additional USD 550mn into Lucid, although PIF is reportedly considering force majeure on certain non-core commitments like LIV Golf to prioritize essential national projects.

- Saudi Arabia is fortifying its regional alliances, approving a new economic deal with Jordan to enhance economic cooperation as well as trade and investment connectivity. Saudi investments currently account for around 7% of total FDI in Jordan.

- Saudi Arabia’s tourism sector continues to show resilience: domestic tourists grew 16% yoy to approximately 28.9mn with their spending up 8% to SAR 34.7bn, supported by Ramadan and Eid holidays. Total tourism volume (domestic and international) was estimated at approximately 37.2mn trips in Q1 with overall spending at SAR 82.7bn.

- Dubai’s rental market recorded contracts worth AED 32.2bn (USD 8.8bn) in Q1 from 118,385 new contracts and 135,607 renewals, according to the Dubai Land Department. Separately, Dubai’s real estate market recordedAED 15.39bn (USD 4.19bn) in resale transactions in Mar from 3308 transactions, according to a report by fam properties, signalling robust secondary market demand.

- UAE investedUSD 95mn in Turkey between Jan-Feb 2026, becoming one of the top three investors in the country.

- Saudi Arabia’s holdings of US Treasuries surged by 26.9% yoy & 19% mom to USD 134.8bn in Jan, the most since Mar 2020. Saudi ranked 17th globally, rising one place ahead of South Korea which decreased its holdings (to USD 140.9bn). UAE increased its holdings further to USD 119.9bn (6.7% mom & flat in yoy terms), the highest since Feb 2025, to become the 19th largest holder globally. Kuwait’s holdings dipped slightly to USD 65.59bn (-1% mom).

Global Macroeconomic Developments

US/Americas:

- The Fed’s Beige Book highlights uncertainty from the war in the Middle East and rising operational costs that are beginning to erode margins. Reports indicate that while economic activity “increased at a slight to modest pace in eight of the twelve Federal Reserve Districts”, businesses are increasingly vocal about the rising energy and fuel costs, in addition to input cost pressures, rising insurance costs and persistent wage pressures, leading to a more cautious outlook for H2 2026; “firms [are] adopting a wait-and-see posture”.

- Industrial production in the US fell by 0.5% mom in Mar (Feb: 0.7%), the sharpest monthly decline since Sep 2024. A surprise dip in March manufacturing production (-0.1% from Feb’s 0.4% gain) suggests that the sector is still reeling from supply chain reconfigurations and import tariffs. Motor vehicle production dropped 3.7% (Feb: +2.6%), as did mining output (-1.2% vs Feb’s 2.1%) and energy production (-1.6%); durable and non-durable manufactured goods fell 0.2% and 0.1% respectively.

- Existing home sales fell by 3.6% mom to a 9-month low of 3.98mn in Mar, struggling from elevated mortgage rates and tight inventory.Inventory remains limited and sales volumes stagnant as high borrowing costs discouraged current homeowners from moving.

- Producer price index in the US surged in Mar: up 0.5% mom and 4.0% yoy (Feb: 0.5% mom and 3.4% yoy); the yoy increase the most since Feb 2023. Core PPI inched up 0.1% mom and 3.8% yoy. Good prices jumped 1.6% mom, driven by the 15.7% in gasoline prices and a 30.7% surge in cost of jet fuel.

- Business confidence indicators continue to suggest a highly localized and uneven industrial landscape: NY Empire State manufacturing index rebounded in Apr (11 from Mar’s -0.2) and Philadelphia Fed manufacturing survey unexpectedly increased to 26.7 in Apr (Mar: 18.1). The NFIB business optimism index slipped to an 11-month low of 95.8 in Mar (Feb: 98.8). Small firms are citing inflation and labour quality as their top concerns, with a significant percentage delaying capex as they wait for clearer signals from the FOMC. Financial markets are pricing in roughly a one-in-three chance of a rate cut this year.

- Initial jobless claims declined by 9k to 207k in the week ended Apr 11, with the 4-week average edging up to 209.75k (from 209.25k) while continuing jobless claims rose to 1.818mn in the week ending Apr 4 (from 1.787mn).

Europe:

- EU inflation was revised higher to 2.6% in Mar (prelim: 2.5%; Feb: 1.9%), as energy prices rose 5.1% (prelim: 4.9%) – the first annual gain in nearly a year and the strongest since Feb 2023. Core inflation stood unchanged at 2.3%.

- Industrial production in the eurozone rebounded in Feb, up 0.4% mom (Jan: -0.8%), thanks to rebounds in non-durable consumer (2.6% vs Jan’s -5.0%), capital (1.0% vs -1.7%) and intermediate goods (0.5% vs. -1.4%) while energy output fell (-2.1% vs 5.5%). In yoy terms, it contracted 0.6%.

- Wholesale price index in Germany jumped by 2.7% mom and 4.1% yoy in Mar (Feb: 0.6% mom and 1.2% yoy), with price increases recorded for mineral oil products (18.8% mom and 17.8% yoy).

- UK GDP expanded by a surprisingly strong 0.5% mom in Feb (Jan: 0.1%), thanks to strong performances from services and production (both up by 0.5%) and a recovery in construction (+1.0%).

- BRC like-for-like retail sales in the UK grew by 3.1% yoy in Mar (Feb: 0.7%), the strongest growth since Apr 2025. Despite the broader growth figures, the BRC Retail Sales Monitor indicates that consumer spending remains unpredictable, as early Easter holidays boosted sales but with the Middle East uncertainty still impacting household decisions.

Asia Pacific:

- GDP in China grew by 1.3% qoq and 5.0% yoy in Q1 2026 (Q4: 1.2% qoq and 4.5% yoy), in line with 2025 growth and the fastest since Q2 2025. Services sector grew by 5.2%, much quicker than manufacturing (4.9%) and primary (3.8%) sectors.

- Industrial production increased by 5.7% in Mar (Jan-Feb: 6.3%), led by sectors such as semiconductors (20.6%) and rail, ships & aeroplanes (13.3%) while retail sales slowed (1.7% from 2.8%) suggesting that domestic consumers remain cautious despite the industrial boom. Fixed asset investment growth edged down slightly to 1.7% yoy in Q1, down from 1.8% in the Jan-Feb.

- China’s new loans surged to CNY 2.99trn in Mar (Feb: CNY900bn), outstanding yuan loans grew 5.7% (Feb: 6.0%) while money supply growth slowed to 8.5% yoy (Feb: 9.0%).

- Exports from China grew by 2.5% yoy in Mar, weakening from the 21.8% clocked in during Jan-Feb while imports were up 27.8% (Jan-Feb: 19.8%), the strongest growth since Nov 2021. Trade surplus stood at a total of USD 264.3bn in Q1. China’s exports to the US fell 26.5% in Mar while imports ticked up by 1%.

- Retail inflation in India increased to 3.4% yoy in Mar (Feb: 3.21%), driven primarily by prices of personal care products (18.7%) and food costs (3.87% from 3.47%), though remaining below the central bank’s 4% target. WPI inflation surged in Mar, up 3.88%, accelerating from Feb’s 2.13%. This was the fastest gain since Jan 2023, due to higher manufacturing (3.39%, the most since Nov 2022 and from Feb’s 2.92%) and fuel & power prices (1.05% from -3.78%).

- Singapore’s GDP contracted by 0.3% qoq in Q1 2026 (Q4: 1.3% qoq); GDP grew 4.6% yoy in Q1 2026 moderating from Q4’s 5.7% gain, supported by strong readings in wholesale trade (6.7%) and construction (9.0%) sectors.

- The Monetary Authority of Singapore tightened monetary policy for the first time in four years. MAS stated that it would “increase slightly” the slope of the SGD NEER policy band (the main monetary policy tool). The SGD NEER is an index of the Singapore dollar’s trade-weighted exchange rate against the currencies of the island’s major trading partners.

Media Review:

The coming global food crisis: FT

https://www.ft.com/content/36343e24-b06f-434d-a7e5-6046e7bcf3df

A fragile truce hinders the recovery of Gulf carriers

https://www.arabnews.com/node/2639765/business-economy

How 50 days of the Iran war led to the loss of $50 billion worth of oil

https://www.reuters.com/business/energy/how-50-days-iran-war-led-loss-50-billion-worth-oil-2026-04-17/

CNBC Interview with Dr. Nasser Saidi on Lebanon’s ceasefire

https://www.cnbc.com/video/2026/04/17/lebanon-faces-economic-hit-of-up-to-20-percent-of-gdp-saidi.html

IMF Regional Economic Outlook update: Middle East & Central Asia

https://www.imf.org/-/media/files/publications/reo/mcd-cca/2026/english/text.pdf

Powered by:

![]()