Strait of Hormuz blockade & prices. GCC responses. Saudi monetary stats & labour stats.

Download a PDF copy of this week’s insight piece here.

GCC: Navigating War-Driven Economic Shocks, Weekly Insights 3 Apr 2026

1. The fifth week of war on Iran / Middle East conflict

- The ongoing war in the region is multifaceted, with economic, security, financial, environmental and socio-economic consequences. The shocks and their consequences are still unfolding, with growing uncertainty as to outcomes.

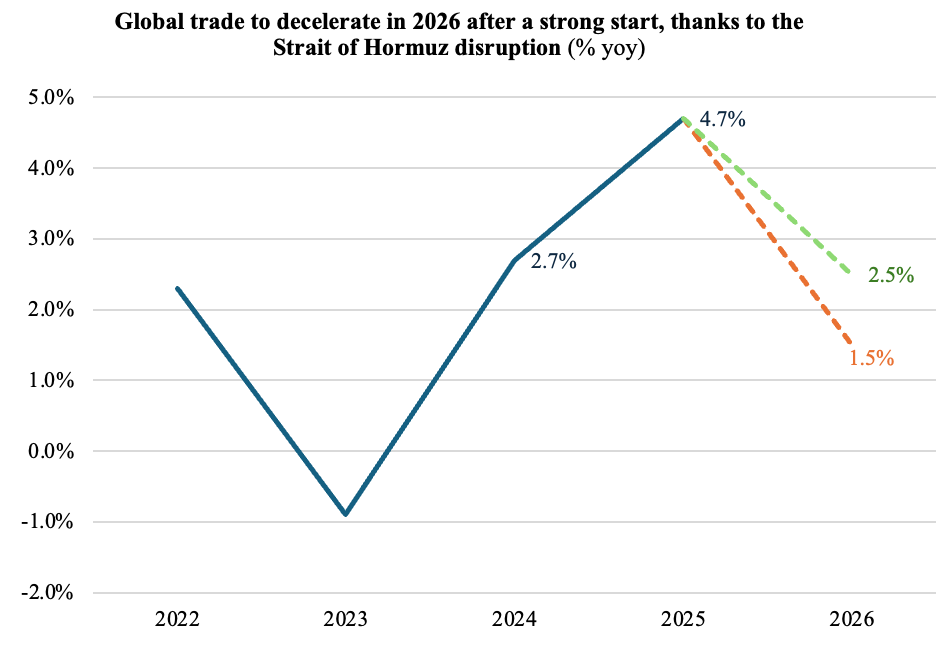

- According to UNCTAD estimates, growth in global merchandise trade is projected to decelerate from 4.7% in 2025 to between 1.5% and 2.5% in 2026 (depending on the duration, depth & breadth of the conflict).

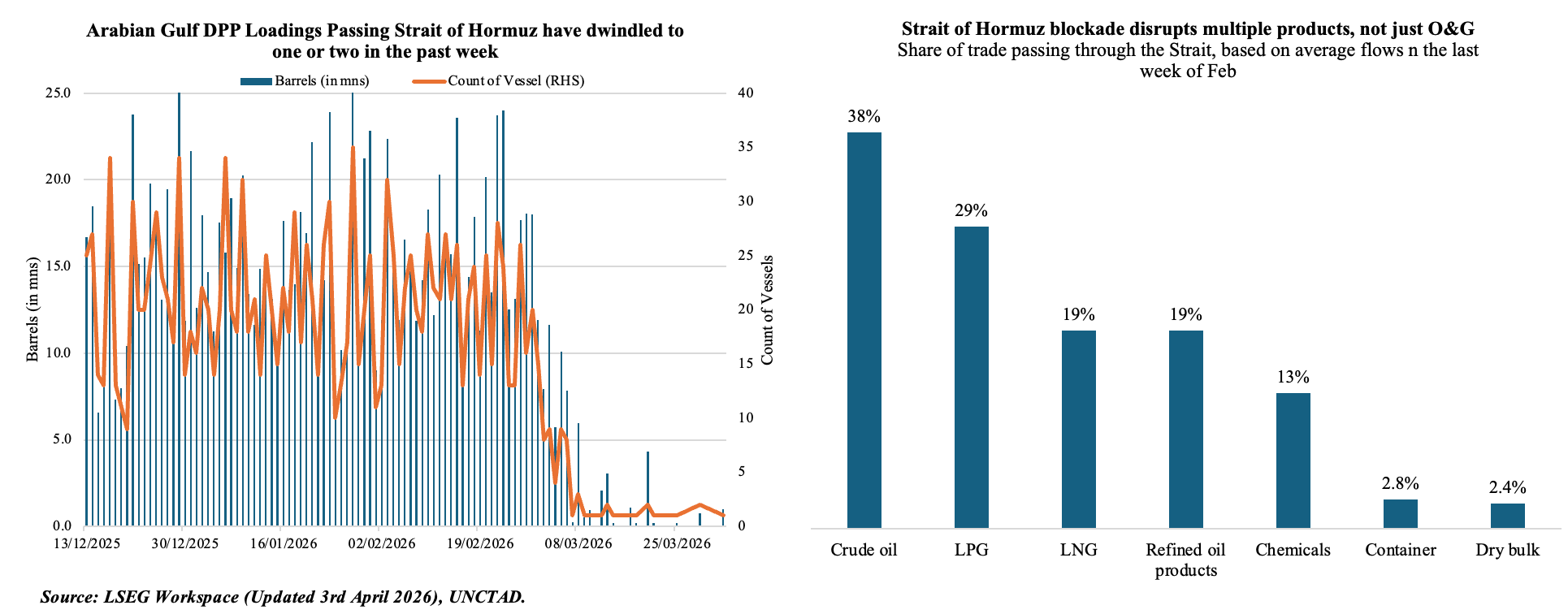

- With the Strait of Hormuz blocked, daily transits have dropped sharply. Though oil and gas flows are discussed in this context, the route also accounted for significant volumes of chemicals (including fertilisers) and grains (dry bulk).

2. The Strait of Hormuz Blockade the main point of contention in the Iran war & wider conflict in the Middle East

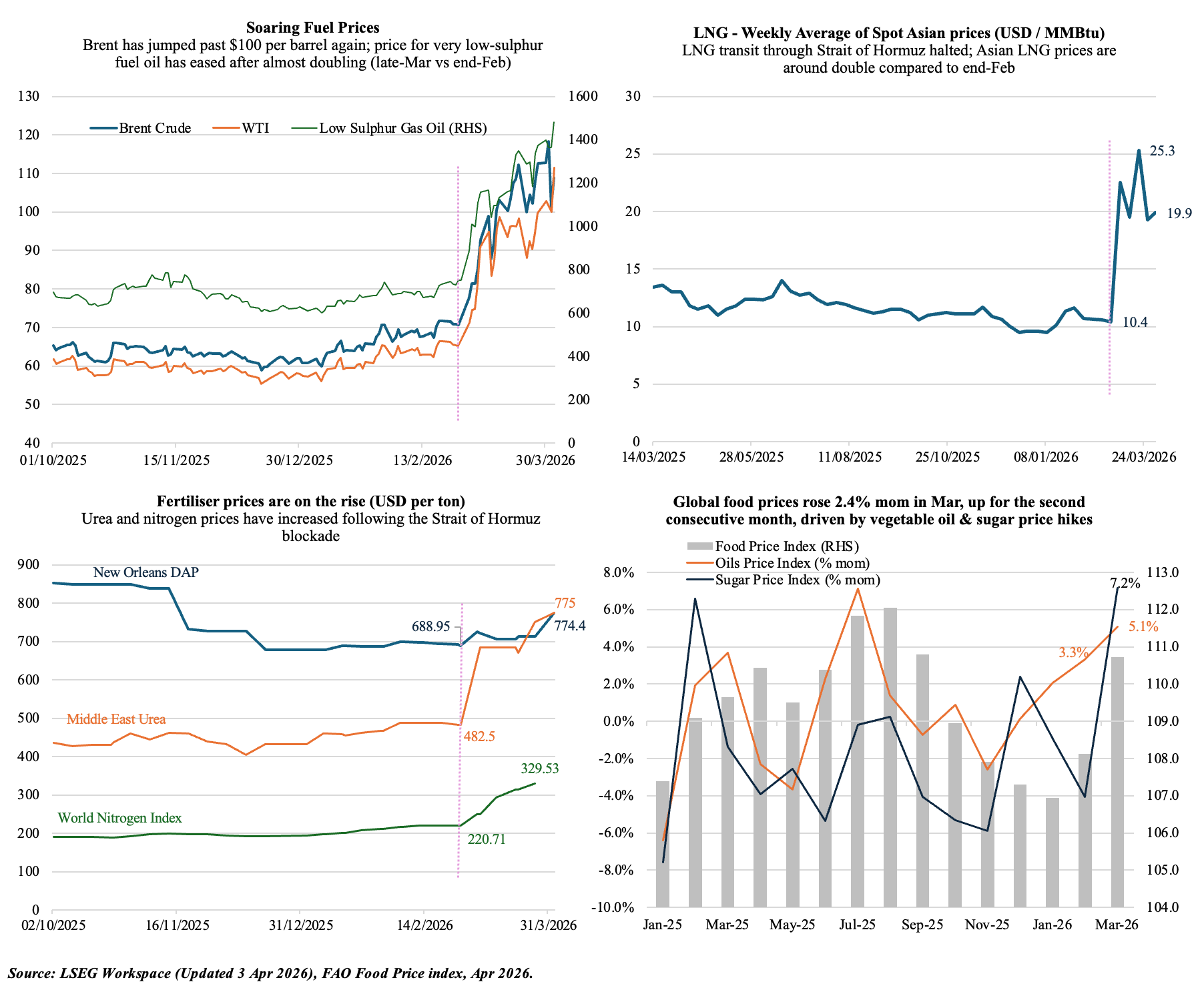

- Beyond oil, supplies of critical inputs from aluminium to helium, sulphur and fertilisers (urea, ammonia, phosphates) are being disrupted leading to price hikes and spilling over into the agricultural and food markets, vehicles, semi-conductor and AI industries.

- Fuel-related pressures are visible in FAO’s food price index for Mar: it is up 2.4% mom, driven by increases in vegetable oil (5.1% mom and 13.2% yoy) & sugar (7.2% mom & -21% yoy)

3. For the GCC, the shocks are unprecedented – but governments are pro-actively rolling out measures to counter the effects of war

- Governments, Ministries of Finance and central banks are rolling out measures and pursuing policies to maintain and support economic, banking and financial market stability; SOEs & GREs are adopting and developing new industrial policies.

- Transport and logistics are being facilitated via alternative routes given the near-closure of the Strait of Hormuz (Saudi’s Yanbu port, a Saudi-Jordan railway freight corridor, new shipping lines, expanded land transport connections etc).

- The central bank of the UAE set out a five-pillar banking and financial resilience framework: access to reserve balances (up to 30% of the cash reserve requirement); availability of term liquidity facilities; temporary relief in liquidity and stable funding ratios; Capital Buffer Relief; flexibility to banks to postpone loan classification. Qatar and Kuwait central banks also announced measures such as new repo facilities, short-term funding tools and deferring of loan payments.

- Dubai government’s announced AED 1bn support package for the private sector includes deferral of government fees, liquidity support for hospitality & tourism, extension of customs data grace periods and streamlining the issuance & renewal of residency permits.

- While the Central Banks provides monetary and exchange rate stability, ensuring liquidity and credit flow through the banking system as a lender of last resort, Dubai’s package provides the necessary fiscal policy support. This will also boost investor confidence and support capital markets performance.

- For energy and food importers of the region (notably Egypt, Jordan, Lebanon, Morocco, Syria and others), the war impact includes exchange rate depreciation, higher inflation, capital outflows, reduced remittance and capital inflows, all leading to lower GDP and potential credit and balance of payments crises.

- Power and fuel subsidy bills will strain fiscal space; high levels of debt & tighter financial conditions may likely raise debt financing costs. Such countries will require external intervention and access to liquidity & financial facilities from the IMF, WB & AMF.

- ESCWA estimates that around 5 million additional people in the region’s middle‑ and low‑income countries could fall into food insecurity if global food prices increase by 20%.

- Destruction in Lebanon and the massive, forced displacement is multiple the damage and displacement of 2024. Initial estimates amount to around 10-15% fall in GDP.

- Damage to infrastructure will require substantial reconstruction investments along with new investments in pipelines and transport corridors to avoid Hormuz.

- IEA, IMF and the World Bank plan a coordination group: “to monitor developments, align analysis, and coordinate support to policymakers to navigate this crisis”.

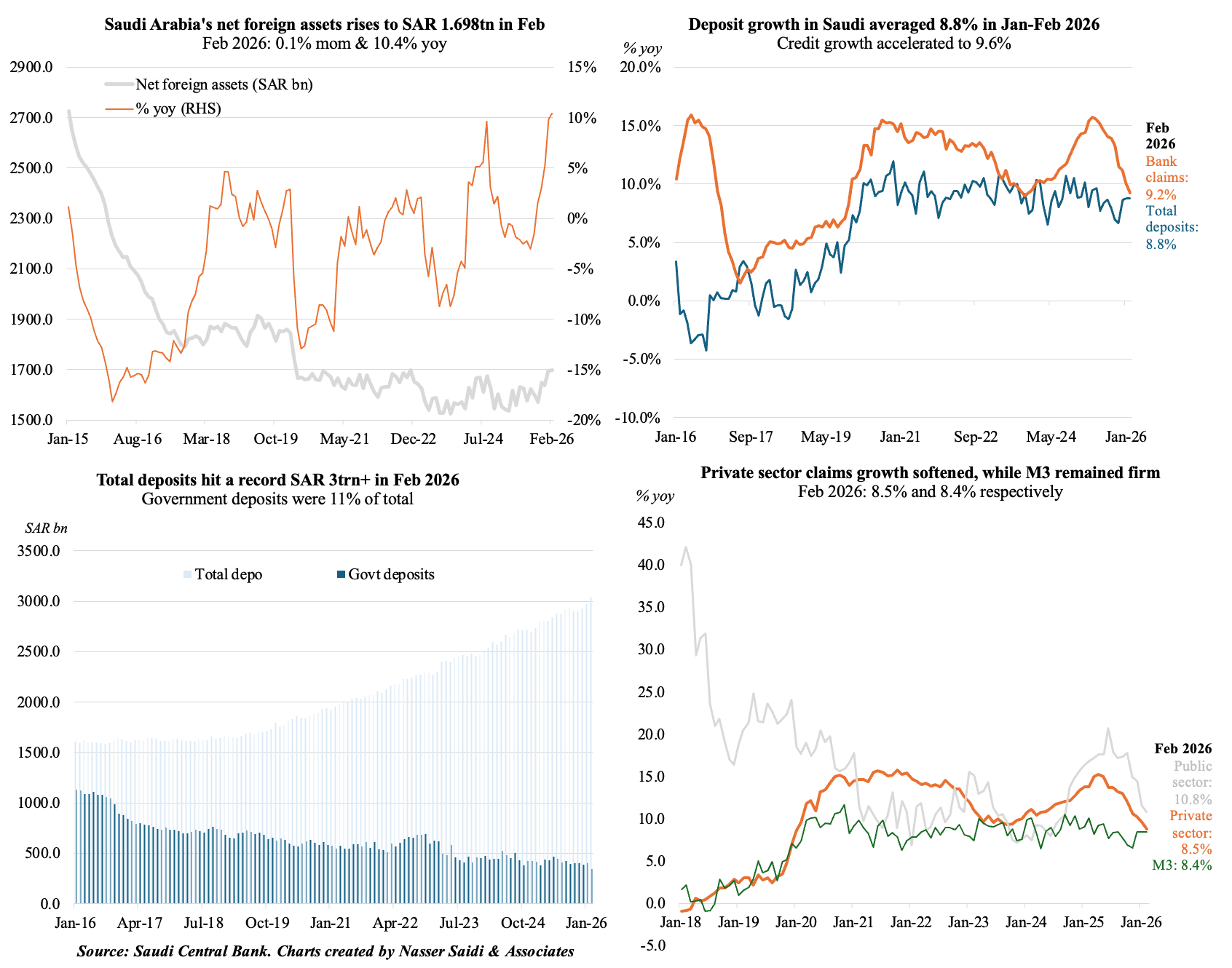

4. Saudi banking liquidity remained strong in early 2026, with deposit and credit growth still robust despite softer government deposits

Feb 2026 – Net foreign assets: SAR 1.698trn; Total deposits growth: 8.8% yoy; Credit growth: 9.2% yoy; M3 growth: 8.4% yoy

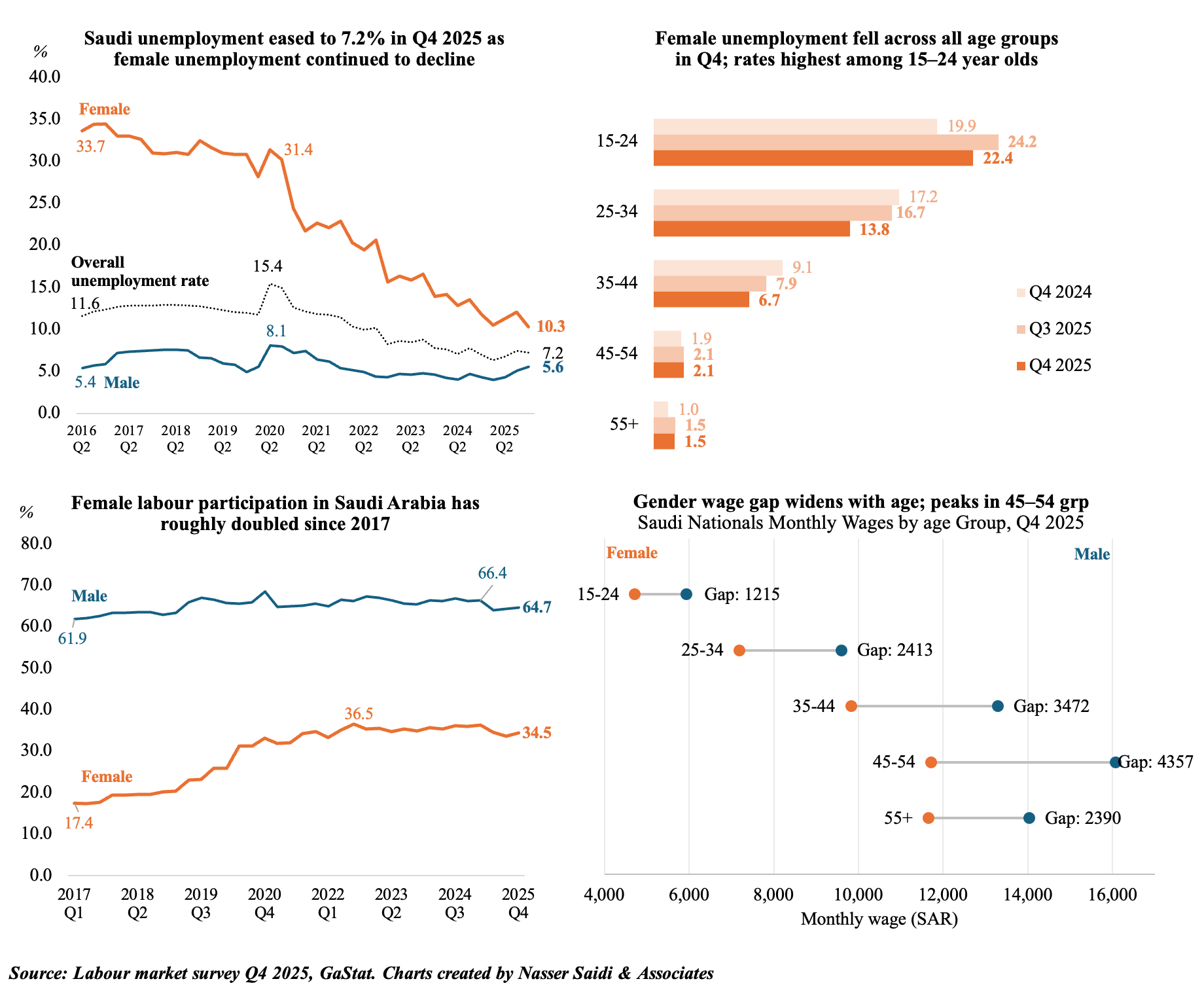

5. Saudi labour market improved further in Q4 2025, with female unemployment falling and participation remaining elevated; wage gaps persist across age groups

Powered by:

![]()