Download a PDF copy of the weekly economic commentary here.

Markets

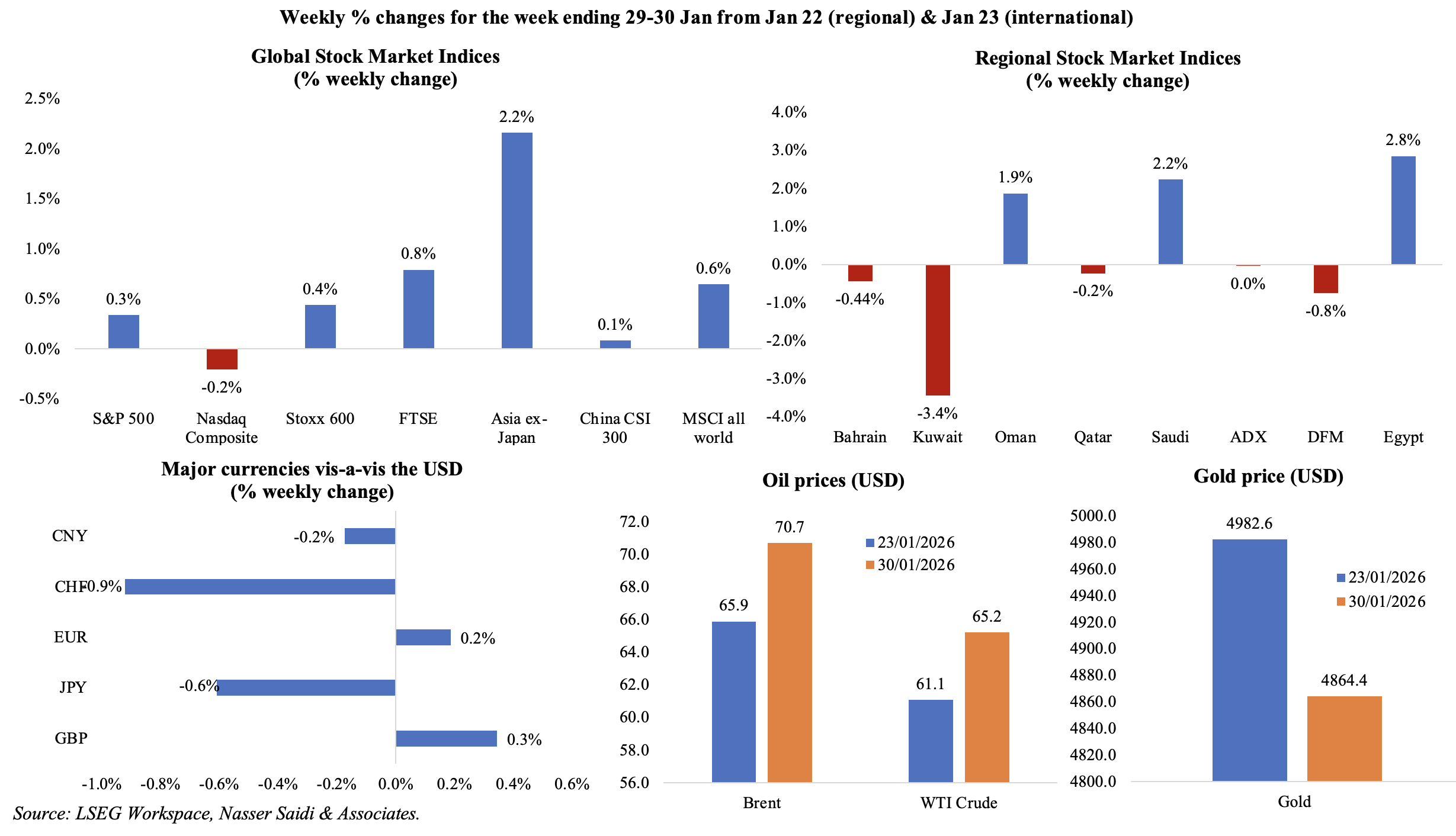

Global equities declined on Friday, but most ended the week on a positive note including the S&P 500 (the first in 3 weeks) and MSCI global stocks index gained 0.6%. Regional markets were mixed amid geopolitical worries namely, a possible US attack against Iran. The new Fed Chair announcement saw the USD gain, as concerns eased about Fed independence, while the yen was impacted by the threat of official intervention (after it came close to the 160-per-dollar mark). Oil prices neared a 6-month high on Friday, with Brent settling around the USD 70 a barrel mark. Gold hit a record of nearly USD 5,600 an ounce on Thursday before plunging almost 9% on Friday. Silver prices slumped over 26% bringing prices to around USD 85 an ounce.

Global Developments

US/Americas:

- The Fed kept its lending rate unchanged between 3.5% and 3.75% at the latest meeting following three straight rate cuts; two Fed officials had voted in favour of an interest rate cut. The Fed chair noted that tariffs were leading to the recent uptick in inflation, while also stating that “there’s an expectation that sometime in the middle quarters of the year we’ll see tariff inflation topping out”. Separately, President Trump nominated Kevin Warsh as the new Fed Chair subject to confirmation by the US Senate.

- Durable goods orders in the US accelerated in Nov, up 5.3% mom from Oct’s 2.1% dip, thanks to the rebound in transport equipment (14.7% from -6.3%). Excluding transportation, new orders increased 0.5% (Oct: 0.1%) while orders excluding defence surged 6.6% (Oct: -1.3%). Non-defence capital goods orders excluding aircraft ticked up 0.7% (Oct: 0.3%).

- Factory orders rebounded in Nov, up 2.7% mom (Oct: -1.3%), while the orders increased 3.4% yoy. This was partly due to the higher demand for commercial aircraft (97.6%).

- US goods trade deficit widened to USD 86.9bn in Nov (Oct: USD 59.1bn), as exports plummeted 5.6% (to USD 185.6bn) and imports advancing 6.6% (to USD 272.5bn). Goods deficit with China declined by about USD 1bn to USD 13.9bn. The goods and services trade deficit also widened by 94.6% mom to USD 56.8bn – this was the largest gain since Mar 1992.

- Producer price index in the US ticked up in Dec, up 0.5% mom, thanks to a 0.7% rise in services (the most gained since Jul). In yoy terms, PPI rose 3.0% in Dec, following the same reading in Nov; for the full year 2025, PPI increased 3.0% (2024: 3.5%).

- S&P Case Shiller home price index rose 0.5% mom and 1.4% yoy in Nov (Oct: 1.3% yoy).

- Chicago Fed national activity index improved to a 10-month low of -0.04 in Nov (Oct: -0.42), with an increase in the contribution of production, employment and housing.

- Dallas Fed manufacturing business index jumped to -1.2 in Jan (Dec: -11.3), thanks to a rebound in the outlook index (2.9) in addition to the increase in indices of production (11.2), new orders (11.8) and shipments (12.0). The Richmond Fed manufacturing index rose one point to -6 in Jan, the 11th consecutive month of pessimism. Slower declines were seen across shipments (-5 from -11 in Dec), new orders (-6 from -8) and employment (-6 from -7) while prices paid for inputs rose faster (7.06 vs 6.53).

- Chicago PMI surged to 54 in Jan (Dec: 42.7), following 25 consecutive months of decline. New orders rose to the highest level since Mar 2022 and employment ticked up to the highest since Dec 2024.

- Initial jobless claims declined by 1k to 209k in the week ended Jan 24, with the 4-week average inching up to 206.25k (prev: 204k). Continuing jobless claims increased by 38k to 1.827mn in the week ended Jan 17.

Europe:

- GDP in the EU grew by 0.3% qoq and 1.4% yoy in Q4 (Q3: 0.4% qoq and 1.6% yoy), according to preliminary estimates. Germany’s GDP grew by 0.3% qoq and 0.4% yoy in Q4 (Q3: 0% qoq and 0.3% yoy).

- EU economic sentiment indicator ticked up to 99.4 in Jan (Dec: 97.2), the highest level since Jan 2023. Sentiment of manufacturers and service providers rose to -6.8 (the most since May 2023) and 7.2 (the most since Jan 2024). Business climate improved (-0.41 from -0.56) while consumer confidence, at -12.4, was the highest since Feb.

- Unemployment rate in the euro area eased to 6.2% in Dec (Nov: 6.3%), as unemployment decreased by 61k compared to Nov.

- The harmonised index of consumer prices in Germany ticked up to 2.1% yoy in Jan (vs previous reading of 2.0%).

- The German Ifo business climate index held steady at 87.6 in Jan, the lowest reading since May 2025. The current assessment sub-index ticked up to 85.7 (from 85.6) while expectations slipped (89.5 from 89.7). By sector, the service industry dipped (-2.6 vs -2.1) while gains were registered in manufacturing (-12.2 from -14.6) and construction (-14.2 from -14.9).

- Germany’s consumer confidence increased to -24.1 in Feb (Jan: -26.9, almost a 2-year low). Economic expectations rose strongly (6.6 vs 1.2), willingness to buy improved (-4.0 from -7.5) while the propensity to save slipped from its highest level since mid-2008 (17.9 vs 18.7).

Asia Pacific:

- China’s NBS manufacturing PMI slipped to 49.3 in Jan (Dec: 50.1), the new orders moving to contraction (49.2 from 50.8) amid declines in foreign sales (47.8 from 49.0) and employment (48.1 from 48.2). Input prices rose for a sixth consecutive month (up three points to 56.1) while selling prices moved to expansionary territory (6 from Dec’s 48.9).

- Non-manufacturing PMI in China declined to 49.4 (from 50.2), the lowest reading since Dec 2022 as new orders and foreign demand contracted more sharply (to 46.1 and 46.9 respectively) while employment was weak (steady at 46.1).

- The BoJ meeting minutes showed a hawkish view among members, with most calling for continued and steady rate hikes on rising price pressures (from a weak yen) while some cautioned the risk of being “behind the curve” in dealing with inflation.

- Tokyo CPI eased to 1.5% in Jan (Dec: 2.0%). Excluding food and energy, prices eased to 2.4% (from 2.6%). Excluding fresh food, prices slowed to 2% (from 2.3%), the lowest since Oct 2024 partly due to a base effect. Food prices eased for the fifth month in a row (5.6% from Dec’s 6.2%) while energy prices fell 4.2%.

- Japan’s consumer confidence index inched up to a 21-month high of 37.9 in Jan (Dec: 37.2. All components rose: employment (42.4 from Dec’s 41.5), income growth (42.0 from 41.3), willingness to buy durable goods (30.4 from 30.2) and overall livelihood (36.8 from 35.9).

- Unemployment rate in Japan stood at 2.6% in Dec for the fifth consecutive month, with the number of unemployed up 50k to 1.86mn; this remains the highest since Jul 2024.

- Japan’s industrial production inched lower in Dec (-0.1% mom) though slower than Nov’s 2.7% drop. Output grew for general-purpose & business-oriented machinery (7.3% from -0.3%), electrical & electronics equipment (2.7% from -10.1%) and motor vehicles (1.4% vs -6.7%) while production machinery fell (-1.9% from 5.1%). IP grew by 2.6% yoy (Nov: -2.2%).

- Retail trade in Japan unexpectedly fell by 2.0% mom and 0.9% yoy in Dec (Nov: 0.6% mom and 1.1% yoy). This was the first yoy decline since Aug, with sales declining across clothing & personal goods (-11.6%), non-store retailers (-5.8%) and food & beverages (-0.4%).

- India’s 2026-27 budget, announced on Sunday, estimates a fiscal deficit of 4.3% of GDP and aims to lower debt-to-GDP to 55.6% (2025-26: 56.1%). Federal government revenue is expected to increase 5.7% in 2026-27, with net tax revenue seen growing 7%. The budget sees record spending on capex (up 9.0% to INR 12.2trn) and defence (up 21.8% to INR 7.85trn) amid a push to build “rare earth corridors” in four mineral-rich states. The budget proposed a tax holiday up to 2047 for foreign cloud companies making data-centre investments.

- Industrial output in India grew by 7.8% yoy in Dec (Nov: 7.2%), the fastest pace in more than two years, while manufacturing growth eased (8.1% from 8.5%). Output of consumer durables and non-durables grew by 12.3% and 8.3% respectively while capital goods output accelerated 8.1%. Cumulative industrial output increased to 3.9% (Nov: 3.3%).

- Industrial production in Singapore grew by 8.3% yoy in Dec (Nov: 18.2%), with pharmaceuticals the main drag (-69.7%) while electronics and semiconductors surging by 30.8% and 32.4% respectively. Excluding the volatile biomedical manufacturing sector, manufacturing output increased 16%.

Bottom line: Though the ECB and Bank of England are expected to hold rates at the meetings this week, the latter is expected to signal a further fall in rates in the near-term. With the Trump administration continuing to stoke trade uncertainty (latest tariff hike threat was to South Korea last week, accusing it of not complying with the trade deal) and geopolitical worries (threats of military action on Iran before signalling diplomatic talks to avoid conflict), its allies are expanding their economic horizons. This includes EU’s trade deal with India (already signed), Canada’s limited trade deal with China (on EVs and canola oil) as well as Canada’s ongoing talks with India to expand trade in oil and gas. The EU-India deal is expected to double EU goods exports to India by 2032 by eliminating or reducing tariffs.

Regional Developments

- OPEC+ left its oil output unchanged for March, reaffirming production quotas agreed in late-2025, despite the Brent crude trading near six-month highs (it touched USD 71.89 on Thursday). The lack of forward guidance beyond March reflects continued uncertainty over global demand and tensions involving Iran, which have contributed to recent price support.

- Egypt’s non-oil exports climbed 17% yoy to about USD 48.57bn in 2025, helping narrow trade deficit by roughly 9% to USD 34.45bn despite a modest increase in imports (5% to USD 83.014bn). Growth was broad-based across building materials (USD 14.88bn), chemicals (USD 9.42bn) and food industries (USD 6.8bn); key non-oil exports markets were UAE, Turkey, Saudi Arabia, Italy and the US underpinning external demand. UAE was the largest destination for Egypt’s non-oil exports in 2025, highlighting bilateral trade linkages and the UAE’s role as a regional re-export hub.

- Total trading value at Egypt’s capital market jumped to EGP 15.7trn in 2025, up from EGP 2.3trn in 2024, driven by strong activity in T-bills and T-bonds (EGP 13.1trn) and stocks (EGP 2.4trn). Regulatory reforms and new financial products expanded investor participation significantly, with close to 300k new investors entering the market last year.

- The Central Bank of Egypt disclosed the repayment of USD 39bn in external debt service in fiscal year 2024-25. External debt rose to USD 161bn in Jun 2025 (end-Mar: USD 157bn).

- Egypt’s free zones attracted capital investments worth USD 14.3bn across 1,237 projects by Oct 2025, also creating around 245k direct jobs. This reflects renewed investor interest in export-oriented production (e.g. EVs and components) and logistics platforms in Egypt.

- Kuwait is preparing to finalise a USD 7bn pipeline stake sale, potentially this month, reflecting a broader strategic pivot among GCC oil & gas producers towards offering foreign investors access to critical infrastructure. Reuters reported that Saudi Aramco was planning to sell some gas-powered power plants in the coming weeks to raise around USD 4bn.

- Kuwait conducted a limited cabinet reshuffle, appointing new finance and foreign ministers, a modest political adjustment reflecting an intent to accelerate fiscal and diplomatic strategies.

- The World Bank approved a new USD 200mn financing package to support poor and vulnerable groups in Lebanon. The funding will provide cash transfers to stabilise living standards, addressing gaps in social safety nets amid the ongoing economic and fiscal crisis. Separately, Qatar’s Fund for Development pledged USD 434mn in financial support to Lebanon, mostly aimed at the energy sector.

- Oman’s inflation edged downto 1.5% in Dec (Nov: 1.6%), staying higher than 1.0% for the fourth month in a row, as transport costs plunged (0.19% from 4.36%) while prices of food & beverages ticked up (1.2% from 0.8%). The average inflation rate for the full year 2025 was 0.85% (2024: 0.6%), reflecting an environment of subdued price pressures aided by stable housing and utilities costs (vs 0.39% in 2024) while food & beverages costs were negative.

- Oman’s bond and sukuk issuance grew by 14.1% yoy to OMR 4.916bn by end-2025, reflecting investor appetite for fixed-income instruments. This accounted for 15.3% of the Muscat Stock Exchange’s total market value, highlighting deeper financial intermediation and diverse fiscal financing options.

- Passenger traffic in Oman increased by 5.0% yoy to 689k+ in Dec 2025, with hotel guests at 3 to 5-star hotels up 10.8% to 2.4mn and hotel revenues surging 22% to OMR 297mn –underscoring a resurgence in tourism and travel activity. Rising tourism demand has bolstered related sectors such as transport, hospitality & retail, contributing to non-oil economic growth.

- Oman unveiled plans for a 400 km hydrogen pipeline, with the project supporting logistics for green hydrogen and derivatives – across production sites and to industrial hubs and export terminals – complementing domestic decarbonisation objectives and potential export corridors to Asia and Europe.

- Qatar’s banking sector posted robust growth in total assets, up 1.0% mom to QAR 2.15trn as of Nov 2025, supported by expanding loan books (0.5% mom and 6.6% yoy to QAR 1.435trn) and healthy liquidity ratios (liquid assets to total assets stood at healthy 30%). Over the past five years 2020-24, loan growth (average 5.4%) has outpaced deposit growth (3.9%) while capital adequacy and provisioning metrics remained strong.

- Trade surplus in Qatar narrowed by 23.6% yoy to QAR 14.1bn in Dec, as exports dipped by 13.7% to QAR 26.9bn alongside a modest increase in imports (0.6% to QAR 12.8bn). Qatar’s top export markets were China (QAR 5.2bn), followed by India and South Korea (QAR 3.8bn and. QAR 2.1bn respectively). China was also the top import partner (18.8% of the total), followed by the US and Italy (13.5% and 7.5% of the total respectively).

- Venture capital investment inQatar surged 81% yoy to QAR 214mn in 2025, according to a report by MAGNiTT, driven largely by early-stage deals (61% of investment value), while fintech was the busiest sector by volume (33% of transactions). Qatar ranked 4th in the MENA region in deal count and venture funding, representing about 5% of regional transactions.

- Syria is seeking roughly USD 100bn for infrastructure and USD 300bn for real estate development over the next decade, as more than 180 industrial zones resume operations. This push is part of broader attempts to rebuild Syria’s war-damaged economy and restore productive capacity.

Saudi Arabia Focus

- GDP in Saudi Arabia grew by 4.5% yoy in 2025, according to Gastat, supported by oil sector activity (5.6%) and broader non-oil sector growth (4.9%). Separately, Saudi Investment Minister highlighted that real GDP has more than doubled since Vision 2030 was launched, reaching about SAR 4.7trn by end-2024, with strong job creation and growing foreign investment licenses evidence of deep structural change; furthermore, non-oil activities now account for over half of the economy. The regional HQ target of 500 under Vision 2030 was surpassed with Saudi hosting over 700 HQs, signifying enhanced competitiveness and attractiveness as a regional business hub.

- Broad money supply in Saudi Arabia grew by 8.3% in 2025 (slower than ‘24’s 9.0%). Pace of credit growth increased in 2025 (14.1% vs 11.3% in ‘24) and it outpaced deposit growth (which eased to 8.4% in ‘25 vs 9.1% in ‘24). Government deposits’ growth fell quicker in ’25 (-7.6% from the 6.4% drop in 2024). Claims to the private and public sector grew by an average 13.3% and 17.2% respectively in 2025. SAMA net foreign assets increased by 5.3% yoy to SAR 1.637trn at end-2025.

- Saudi Arabia’s overall exports declined by 4.4% mom in Nov,with monthly declines across oil (-4.4%), non-oil (-7.0%) & re-exports (-0.9%). Share of oil exports to overall exports held at 67.2%. Total non-oil exports (i.e. including re-exports) increased by 20.7% yoy to SAR 32.7bn in Nov, reflecting broadening external demand beyond hydrocarbons. A breakdown shows that re-exports and domestic non-oil exports (i.e. excluding re-exports) grew by 52.1% yoy and 4.7% yoy to SAR 13.7bn and SAR 18.97bn respectively. Imports fell by 6.9% mom and 0.2% yoy to SAR 77.4bn in Nov, resulting in a wider trade surplus, SAR 22.4bn. China was the largest trade partner for Saudi in Nov: it received 13.7% of Saudi exports and was source nation for 26.7% of imports.

- Reuters reported that Saudi Arabia suspended work on the Mukaab “The Cube” megaproject, reassessing its funding and feasibility, and redirecting PIF resources in the meantime toward projects related to the World Expo 2030 and the 2034 World Cup among others. This reassessment of mega-project capital allocation is a positive move amid shifting global oil market dynamics and a focus on projects with clearer near-term impact.

- Saudi Arabia will deliver an additional 300k housing units over the next three years working with the private sector. This will help meet rising demand, restore market balance and support rising homeownership (66% at end-2025 from 47% in 2016).

- Saudi Arabia is planning to broaden its premium residency program to attract wealthy individuals (with net worth of close to USD 30mn), ultra-wealthy individuals who moor superyachts in Saudi waters as well as top performing students and entrepreneurs, reported Bloomberg.

- Aramco’s first bond issuance of 2026 (USD 4bn) attracted around USD 21bn in orders, underscoring robust investor appetite for high-quality sovereign-linked instruments. Strong subscription levels point to Saudi’s creditworthiness and such issuances are likely to rise.

- Saudi Arabia plans to set up a cloud computing Special Economic Zone (SEZ) from April, aiming to attract cloud service providers and data centre operators. Details of tax relief and qualifying conditions for the SEZ are not yet published.

- A new National Privatization Strategy was unveiled by Saudi Arabia, designed to broaden the role of public-private partnerships (PPPs) in delivering large-scale infrastructure and services. This aims to mobilise more than USD 64bn in private capital investments and create tens of thousands of quality jobs by 2030.

- Saudi Arabia’s air passengers exceeded 140mn in 2025, up 9% yoy, as international destinations rose to 176 and new carriers like Riyadh Air expanded operations.

- Saudi Arabia approved a company to offer non-residents and foreign individuals fractional home ownership property via a digital platform, with the minimum investment set at SAR 1000, days after the new real estate ownership rules were rolled out.

UAE Focus

- Dubai unveiled a landmark USD 27.2bn expansion of the DIFC freezone. The district, to be expanded by 17.7mn square foot, will include new commercial and residential zones as well as a dedicated space for future technologies and AI. The expansion could strengthen Dubai’s role in regional capital markets, boost financial services exports and attract deeper FDI flows from Asia and Europe.

- Dubai’s GDP grew by 4.7% yoy to AED 355bn in Jan-Sep 2025, driven by finance (+8.5% yoy, accounting for 12% of GDP), real estate (+6.7%) and construction. (+8.5%) while health & social work activities were the fastest growing (15.4%), reflecting broad-based momentum across key economic engines. Q4 performance will likely be supported by Dubai’s strong global connectivity (reflected in the performance of the trade and hospitality sectors) alongside elevated activity in other non-oil sectors.

- Abu Dhabi’s newest sovereign wealth fund L’imad Holding is taking control of peer ADQ, marking a major reshuffle of investment vehicles, with the merged entity managing around USD 300bn in assets.

- Overnight visitors to the Ras Al Khaimah emirate rose 6% yoy to more than 1.4 mn in 2025 and the aim is to attract 3.5mn tourists by 2030. Separately, the Ras Al Khaimah Airport welcomed 1mn passengers in 2025 (up 51% yoy) and aims to receive 1.5mn passengers by end-2027, thanks to infrastructure upgrades and airline partnerships.

- UAE is among the world’s most air-connected countries, revealed the Minister of Economy and Tourism. UAE accounts for about 2.3% of global international passenger traffic and 32.2% of international passenger traffic at the regional level. High connectivity supports tourism, trade and business travel, reinforcing UAE’s competitiveness as a regional economic hub.

- Outstanding debt in the UAE grew 9.3% yoy to USD 325bn+ at end-2025 and is positioned to cross USD 250bn this year, according to Fitch Ratings. This is underpinned by strong sukuk issuance (UAE’s DCM saw record high sukuk issuance last year, the highest-ever annual issuance) and funding diversification alongside regulatory reform. UAE was the second-largest USD sukuk issuer and third-largest issuer of ESG-linked sukuk globally in 2025.

- The Stargate UAE campus will cost more than USD 30bn (up from the initial projections of USD 20bn), according to UAE’s AI minister, and is designed to position UAE as a leading regional hub for cloud computing, AI and digital infrastructure. The project’s first phase is expected to be completed by Q3 2026.

- Abu Dhabi Airport welcomed more than 33 million passengers in 2025, doubling over the past three years, underscoring the expansion in international air travel. The Zayed International Airport, which accounted for almost 98% of passenger traffic and 73% of aircraft movements, also added 39 new routes and 7 more airlines last year.

- ADNOC is leasing fuel oil storage capacity in Singapore, its first such move, allowing it to strengthen supply chain flexibility and access key Asian bunkering markets directly. Expanding strategic storage abroad may improve refining margins and mitigate inventory risk amid shifting global energy patterns.

- Emirates NBD received a licence to participate in India’s rapidly growing IPO market, allowing it to offer equity and debt capital market services. This aligns with regional banks’ broader strategies to capture fees and cross-border financing opportunities in high-growth economies while also enhancing financial linkages with South Asia.

Media Review:

Traffic congestion tightens grip on Dubai and Riyadh

https://www.agbi.com/infrastructure/2026/01/traffic-congestion-tightens-grip-on-dubai-and-riyadh/

Trump Wants a “Hot Hot Hot” Economy

https://www.project-syndicate.org/commentary/trump-bet-on-rapid-growth-without-inflation-likely-to-fail-by-kenneth-rogoff-2026-01

How steep is Trump’s democratic backsliding?

https://www.ft.com/content/b474855e-66b0-4e6e-9b73-7e252bd88938

Why software stocks are getting pummelled

https://www.economist.com/business/2026/02/01/why-software-stocks-are-getting-pummelled

Powered by:

![]()