Saudi Arabia: Growing and Resilient Despite Lower Oil Prices, Weekly Insights 2 May 2025

1. GCC to grow by 3.0% in 2025, recovering from a modest 1.7% in 2024; inflation remains a muted 1.9% in 2025-26; GCC non-oil budget deficits are improving: IMF

- Economic growth is forecast to edge up to 2.6% in the MENA in 2025 and rise further in 2026 (+3.4%). There is a divergence within groups of oil exporters.

- The GCC is projected to drive growth, thanks to robust non-oil sector activity & gradual phase-out of oil production cuts.

- Inflation is projected to ease in 2025-26, running at 1.9% in the GCC versus just over 10% in the wider MENA region.

- Given global uncertainty, softer oil prices could result in some prioritising of projects in GCC.

- Break-even oil prices are inching lower, though Qatar and UAE will be better placed than Bahrain (breakeven price of $137.0 this year) or Saudi Arabia ($92.3) to prolonged period of lower oil prices.

- Non-oil fiscal balances (as % of non-oil GDP) are estimated to improve, as GCC nations introduce non-oil revenue measures (minimum tax for MNCs, tax administration reforms, discussions around carbon tax in Bahrain, income tax in Oman etc).

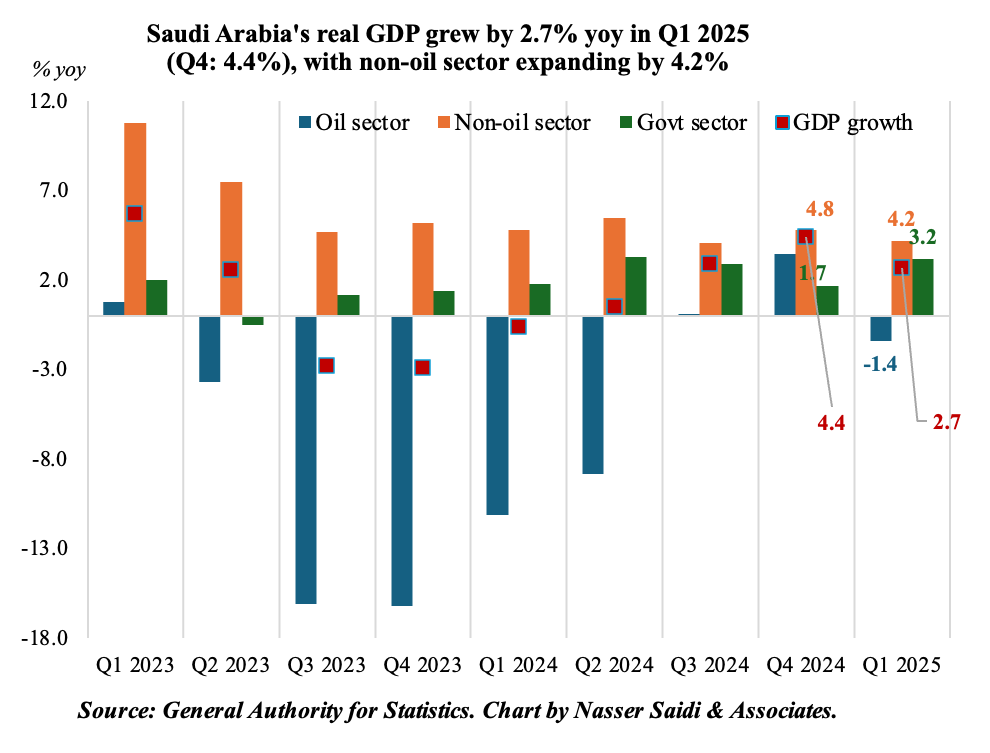

2. Saudi Arabia GDP grew by 2.7% yoy in Q1 2025 (Q4 2024: 4.4%), supported by non-oil activities

- Saudi Arabia’s real GDP grew by 2.7% in Q1 2025, according to preliminary data, thanks to a boost from the non-oil sector (4.2% from 4.8% the quarter before) while the oil sector posted a decline after two quarters of growth (-1.4% yoy from Q4’s +3.5% gains).

- Non-oil sector growth remained resilient: growing by 4.2% in Q1, from the previous quarter’s 4.8%. Furthermore, the government sector grew by 3.2% in Q1 (Q4: 1.7%).

- The IMF forecasts overall GDP to recover in 2025 (+3.0% yoy, down from 3.3% before) and further in 2026 (to 3.7% from 4.1% prior), with the gradual unwinding of oil output cuts. Non-oil GDP is projected to grow by a robust 2.0% and 5.0% in 2025 and 2026 respectively.

- Non-oil sector growth is driven by robust domestic demand. But an important question is whether the recent decline in oil prices (touching a 4-year low of USD 61 on Wednesday) would affect growth forecasts: the budget breakeven price projected for Saudi is USD 92.3 this year. There has been reports of some spending cuts/ prioritisation of projects to keep spending in check; additionally, public sector entities are likely to tap the debt/ Sukuk markets for financing (PIF this week raised USD 1.25bn from its second debt sale this year). With low levels of government gross debt (29.9% of GDP in 2024), and ample reserves (USD 437.2bn in 2024), this would not be a significant burden on the economy.

- Risks to the forecast include persistent low oil prices (as an indirect impact of tariffs), slower implementation of reforms (leading to lower growth) and geopolitical fragmentation among others.

- However, Saudi Arabia could use the opportunity (along with other GCC nations) to diversify / strengthen trade and investment relations as well as lean towards greater regional integration. Read more: https://www.agbi.com/opinion/markets/2025/04/nasser-saidi-trumponomics-tariffs-and-the-global-flight-from-the-us/

3. Overall deposits in Saudi Arabia grew an average 9.0% in Q1 2025; govt deposits surged 15.4% mom in Mar. Credit growth has consistently outpaced deposit growth for 14 months. Net foreign assets ticked up in Mar, up 5.2% mom to SAR 1.62trn. Consumer spending accelerated in Mar, given the month of Ramadan & Eid break

4. Saudi Arabia’s FDI inflow climbed to SAR 23.8bn in Q4 2024; sum of 4 quarters takes total FDI in 2024 (to SAR 85.3bn) short of the NIS target of SAR 100bn+

- FDI inflows into Saudi Arabia touched SAR 23.8bn in Q4 2024: this was up 16.7% qoq but down by 11.5% when compared to Q4 2023. Net FDI inflows stood at SAR 22.1bn in Q4.

- FDI inflow totalled SAR 85.3bn in 2024, down by 11.1% yoy; this amount is short of the annual National Investment Strategy target (of over SAR 100bn). FDI inflow in 2023, at SAR 95.9bn (USD 25.6bn), exceeded the NIS target of USD 22.13bn.

- Investment licenses issued by Saudi is also rising. It expanded by 59.2% yoy to 4597bn in Q4 2024. Three sectors – construction, manufacturing, and wholesale & retail trade – accounted for more than 55% of total licenses issued in Q4 2024 (Source: MISA)

5. Saudi exports drop 4.5% yoy in 2024 despite robust non-oil exports growth

- Saudi exports declined by 4.5% yoy to SAR 1.145trn in 2024, according to GaStat.

- By region, Eastern Asia was the largest export destination (36.5% of total) in 2024, followed closely by Western Asia (17%).

- By country, China, South Korea and Japan topped the list, together accounting for one-third of total exports.

- Imports grew by 12.5% to SAR 873bn, resulting in a trade surplus of SAR 272.6bn.

- Eastern Asia was the largest source region; China alone accounted for 23.9% of overall imports in 2024.

Powered by:

![]()