GCC macro story is strong even as Trump tariff hikes bring about global uncertainty – Weekly Insights 14 Mar 2025

1. Trump’s trade tariff hikes: initial thoughts + impact on the GCC

- In the 50 days+ since President Trump took office, there have been multiple announcements / roll backs / postponements of tariff hikes, leading to a period of high uncertainty that is affecting business and consumer sentiment as well as capital markets performance. So far, China, Canada and Mexico have been the most targeted, while the recent 25% tariff hike on all aluminum & steel imports will negatively impact GCC producers.

- In 2024, Canada, UAE, and Mexico were the top 3 countries from where US imported aluminum and bauxite and Bahrain was the sixth largest. Together, all GCC nations accounted for 12.2% of US aluminum and bauxite imports last year. None of the GCC countries featured in top 10 countries of origin for US iron and steel imports –together they accounted for only 1.4% of total iron and steel imports last year.

- Market performance has been dismal, with the S&P 500 entering a correction yesterday (i.e. down by more than 10% from its Feb 19 closing high) after the Nasdaq index went into correction the week prior.

- As it stands, we believe it unlikely that Trump will back down on tariffs, even at a rising risk of recession. This is the President’s second-term, with the Republic Party having majority in both Houses and with the Supreme Court comprised of his nominees.

- What could be the impact of the tariff hikes? Rapidly rising global economic uncertainty; 2. Already seeing the evidence of greater EU unification (higher defence spending, issuance of common debt etc); common debt could also allow support the role of euro as an alternative global reserve currency (and lower USD’s importance) 3. Could bring the EU and UK closer again (post-Brexit) 4. As more products and countries are included under tariff hikes, major trade partners will diversify trade & investment linkages to the rest of the world including India, China & the Middle East; 5. Expect rate cuts to be delayed given greater uncertainty about the impact on the real economy and inflation.

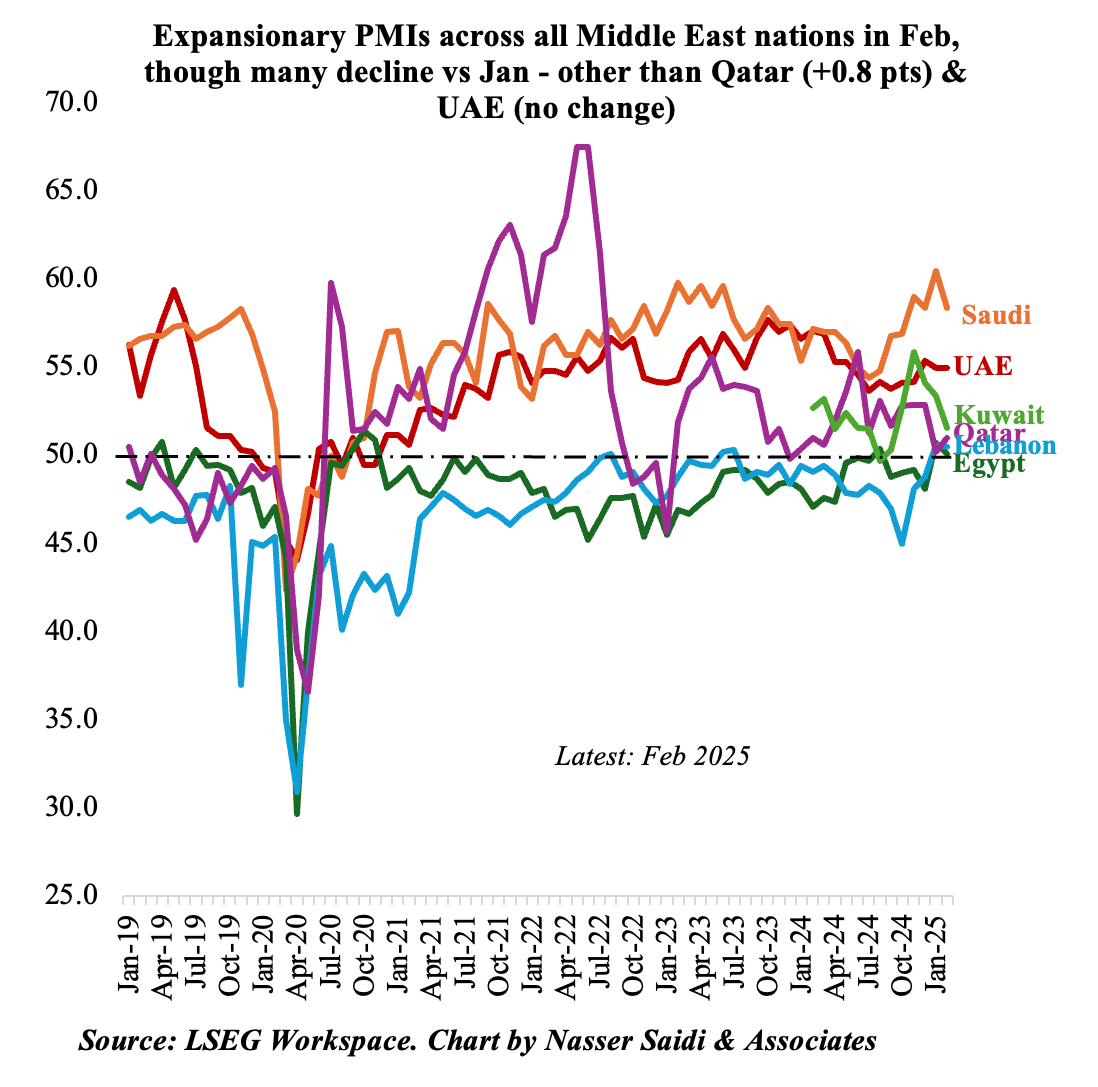

2. PMIs remain on an expansionary trajectory across the Middle East

- Even though Middle East nations’ PMI readings continued to be expansionary, four posted declines in Feb while UAE remained unchanged, and Qatar rose by 0.8 points to 51.0.

- Saudi PMI clocked in the highest PMI: at 58.4 in Feb, the reading was supported by expansions in output, export sales and orders. Upturns in output was reported in UAE, Dubai and Kuwait. The latter revealed that aggressive marketing campaigns and price discounts led to the upticks. Meanwhile, Qatar reported weaker activity in construction sector even as financial remained strong.

- Employment growth showed a divergence across the GCC. It hit a survey record-high in Qatar and a 16-month high in Saudi while in Kuwait firms lowered staffing levels; though employment increased in the UAE, job creation was limited.

- Egypt recorded its first consecutive expansionary PMI readings since Sep-Nov 2020, thanks to increasing demand and stable output. Lebanon reported stronger foreign sales and firms increased staffing for the first time since Nov 2023.

- Cost pressures were different across countries. Egypt businesses reported muted input cost inflation while in Lebanon it ticked up to the highest in 4 months. It eased in Saudi while ticking up in UAE (up for the first time since Jul 2024) and in Qatar salaries grew at the 2nd-quickest rate on record. Selling prices fell in Qatar (for the 7th month in a row), ticked up in UAE (5-month high) and Lebanon (23-month high).

- Business confidence increased to a 15-month high in Saudi Arabia supported by domestic demand and mega projects, while Egypt saw a decline (to the lowest since Nov). Global uncertainty is ticking up, and there could be a spillover effect on PMI in the coming months.

3. In line with PMI responses, inflation rate plunges in Egypt & eases in Lebanon: supported by lower food prices

- Egypt’s annual urban inflation eased to 12.8% in Feb (Jan: 24%), the lowest reading since Mar 2022. It is partly a base effect as the increases seen for the past two years fade. While food prices also plunged in Feb (to 3.7% from 20.8%), transportation costs remained relatively high (34.3% from 35.9%). Core inflation also fell to 10.0%, the lowest since Feb 2022, and from 22.6% in Jan.

- The IMF approved its USD 2.5bn loan for Egypt this week, including USD 1.3bn for climate resilience. High debt levels and large financing needs were highlighted by the Fund, which has laid one of the main conditions as the elimination of fuel subsidies by Dec 2025. Uncertainty is high in the near to medium term: from the impact of US tariffs hikes, potential uptick in prices as subsidies are phased out and regional conflicts.

- Inflation in Lebanon inched lower to 16.1% yoy in Jan 2025 (Dec: 18.1%), tumbling from the 177.3% clocked in Jan year ago. Food and beverages costs declined sharply to 20.9% (from Dec’s 22.2%) while transport costs inched up to 10.3% (from 9.0%).

4. GCC headline inflation is relatively low vs Egypt & Lebanon: Kuwait’s 2.5% in Jan was the highest across GCC. Costs of food declined in both Bahrain and Qatar, while it was higher in Kuwait and UAE.

5. Saudi Arabia GDP grew by 4.5% yoy in Q4 2024, with non-oil sector growing at a faster 4.7% rate alongside an increase in oil sector activity

- GDP in Saudi Arabia expanded by 4.5% yoy in Q4, highest in 2 years, and up from the preliminary estimate of 4.4% and Q3’s 2.8%. Growth was evident across the board, rising fastest in non-oil sector (4.7%), followed by the oil (3.4%) and government (2.2%) sectors.

- Real GDP rebounded in 2024, up by 1.3% yoy, supported by the expansion in non-oil (4.3%) and government (2.6%) sectors while oil activity declined 4.5%. This follows the 0.8% dip in 2023, which was dragged down by the oil sector (-9.0%).

- Mining and quarrying sector was the dominant sector in Q4, accounting for 23.2% of total output while manufacturing had a significant 11.4% share alongside real estate & construction (11.5%). Share of non-oil activities clocked in at 50.2% of overall GDP in Q4.

- By expenditure components (at current prices), final consumption expenditure accounted for more than two-thirds of overall GDP in Q4 2024. Gross fixed capital formation (GFCF) clocked in at SAR 283bn in Q4 – both government (14.4% share of GFCF, declined by 27.2% yoy) and non-government (85.6% share, growing by 6.7% yoy).

6. Saudi Arabia’s year-on-year industrial production and manufacturing grew by 1.3% & 3.8% respectively in Jan 2025

- Industrial production in Saudi Arabia grew for the seventh consecutive month in Jan 2025, up by 1.3% (slightly lower than Dec’s 1.8% gain) and oil activities posting modest gains (0.4% in Jan vs 0.5% in Dec 2024). In month-on-month terms, IP was flat (Dec: +0.6%). Overall manufacturing inched up by 0.4% mom and 3.8% yoy.

- Non-oil activities grew by 3.6% yoy in Jan 2025. Within manufacturing, the manufacture of electrical devices and food products grew the fastest growing (9.2% and 8.4% respectively) alongside manufacture of non-metallic products (6.9%) and manufacture of paper and paper products (5.0%).

- Positive signs for industrial/ mining activity in the future. The Saudi Ministry of Industry & Mineral Resources disclosed that 1346 industrial licenses were issued in 2024; 1,075 factories began production last year, with investments worth SAR 48bn+ and a workforce of about 39k employees. Saudi also launched this week applications for mining licenses / mineral exploration.

Powered by:

![]()