UAE banking stats. Dubai tourism. Saudi inflation & fiscal performance. GCC US Treasury holdings.

Download a PDF copy of this week’s insight piece here.

Weekly Insights 21 Feb 2025: Non-oil sector gains – robust performance in UAE banking & tourism; Saudi non-oil fiscal revenues rise

1. UAE gross assets rise 9.3% ytd to AED 4.45trn in Nov; deposits surge 11.2% ytd

- UAE’s gross bank assets grew by 10.6% yoy and 9.3% year-to-date (ytd) to AED 4.451trn in Nov. It edged down by 0.1% from Oct 2025

- The central bank’s total assets inched up by 1.2% mom to a new record-high AED 861.5bn in Nov.

- UAE banks’ deposits increased by 0.1% mom and 14.7% yoy in Nov, driven by a 0.5% mom uptick in resident deposits while non-resident deposits ticked up by 0.1% (its share was just 7.6% of overall deposits).

- Private sector deposits account for two-thirds of total deposits and 71.4% of total resident deposits in Nov. Government and GREs together accounted for over ¼-th of total deposits; these grew by 7.3% & 15.3% ytd.

- The rapid growth in population in the UAE, combined with the steady increase in loan growth will support banking sector performance.

2. Domestic credit growth in the UAE rises by 6.8% ytd as of Nov 2024

- Gross credit in the UAE grew by 8.5% yoy and 8.6% year-to-date (ytd) to AED 2.163trn in Nov. This was driven by growth in domestic credit (6.0% yoy amd 6.8% ytd to AED 1.857trn in Nov) and foreign credit (26.6% yoy to AED 306.9bn). Foreign credit also includes loans and advances to non-residents, which grew by 4.1% mom and 22.8% yoy to AED 25.3bn.

- Within domestic credit, the share of loans to the private sector stood at 72.7% in Nov. Loans to the government and GREs increased by 3.9% and 2.6% year-to-date to AED 191.4bn and AED 300.1bn respectively as of end-Nov.

- Loans disbursed to business and industrial sector (at AED 863.1bn) accounted for 64% of credit to the private sector. Credit disbursed to the private business and industrial sector grew by an average 4.7% yoy in Jan-Nov 2024 while in contrast, private sector retail credit grew at a much faster pace of 13.2%.

- Separately, capital and reserves of banks operating within the UAE climbed to a new high of AED 528.6bn, up 1.1% mom & 9.8% yoy.

3. International visitors to Dubai surge 9.1% yoy to 18.71mn in 2024

- Visitors into Dubai increased by 9.1% yoy to 18.71 million in 2024. Western Europe and South Asia accounted for the largest shares of visitors at 10.0% and 16.7% in 2024 (3.74mn and 3.3mn respectively) while GCC & MENA together accounted for 4.74mn visitors (or 25.3% of the total).

- Annual gains were highest in North and South-East Asia (+24.2% yoy to 1.8mn), followed by Africa (19.8% to 903k). Tourists from China surged by 31% yoy to 824k in 2024.

- Growth in tourism is also supported by the tourism infrastructure: there were 154,016 hotel rooms (+2% yoy) across 832 establishments (+1% yoy) in Dubai. Dubai hotels saw record-highs (with available data) amongst multiple indicators: hotel occupancy rate at a robust 78.2%; revenue per available room of AED 421 (+1.4% yoy) and room rates were at AED 538 (+0.4% yoy). However, length of stay has edged down to 3.7 (from 3.8 last year), but higher than the pre-Covid 3.4 in 2019.

- Passengers passing through the Dubai International Airport touched a record high of 91.9mn passengers this year (vs 86.9mn in 2023 and the previous pre-pandemic record of 89.1mn in 2018). Dec 2024 was the busiest month, with the airport handling 8.2mn passengers.

- 2025 is shaping up to be another eventful year: Dubai International airport is scheduled to handle 2.5mn passengers in the week 20-28 Feb, given a mix of school holidays and events such as the Dubai Duty Free Tennis Championships and UAE Cycle Tour among others.

4. Consumer prices in Saudi Arabia starts 2025 with a slight increase while producer price inflation eased

- Consumer price inflation in Saudi Arabia inched up to 2.0% in Jan (Dec: 1.9%), with housing & utilities clocking in the largest increase (8.0% in Jan vs 8.9% in Dec). Rentals for housing stood at 9.68%, down slightly from Dec’s 10.63% reading: rents paid for housing by 9.7% and increase in villa rental prices by 7.7% during Jan 2025.

- Food & beverage costs were up by 0.8% while prices at restaurant & hotels eased slightly (0.8% from 0.95% in Dec). Miscellaneous goods and services prices accelerated: by 3.3% in Jan 2025 versus 2.2% in Dec 2024.

- Wholesale prices in Saudi Arabia eased in Jan to 0.86% from Dec’s 1.2% gain. This was the lowest reading since Sep 2023.

- Deflation eased in ores & minerals (-2.2% from -2.6%), increased in food products, beverages, tobacco and textiles (-0.26% from -0.14%) while metal products prices fell in Jan (-0.24% from Dec’s 0.04%). Prices of agriculture & fishery products grew by 4.63% yoy in Jan (Dec: 3.22%).

- The PMI readings highlight the increase in costs: input costs jumped at the steepest rate in nearly 4.5 years in Jan & contrary to previous months, output prices also rose at the quickest pace in a year.

5. Saudi Arabia posts a wider deficit of SAR 115.6bn in 2024, as spending surged by 6.3% versus a modest 3.9% rise in revenues

- A breakdown of Saudi Arabia’s fiscal deficit in 2024 showed a narrowing in H2 (SAR 27.7bn, less than one-third the deficit of SAR 87.9bn in H1). The 2025 budget forecasts fiscal deficit to narrow further to SAR 101bn in 2025.

- The 6.3% yoy increase in spending contributed to the widening of deficit last year. Compensation of employees & subsidies together accounted for just over 43% of total expenditure (& 50% of total opex) and grew by 6.8%. Capex accounted for just 14% of total spending and grew by 2.2% to SAR 190.7bn (capex is budgeted to drop in 2025). With multiple gig-projects underway in the country, infrastructure investments are expected to rise further and reach USD 1trn by 2030 (according to the economy minister) .

- Revenues grew by 3.9% yoy to SAR 1259.1bn in 2024, thanks to a 9.8% increase in non-oil revenues to SAR 502.5bn. Oil revenues, which accounted for 62% of overall revenues, grew by a modest 0.3% to SAR 756.6bn.

- Total debt stood at SAR 1.2trn at the end of 2024 from SAR 1.05trn at the start of the year. Domestic debt accounted for 60.7% of overall debt at end-2024.

- Saudi needs an estimated total funding of SAR 139bn in 2025 to cover both deficit and SAR 38bn in debt servicing.

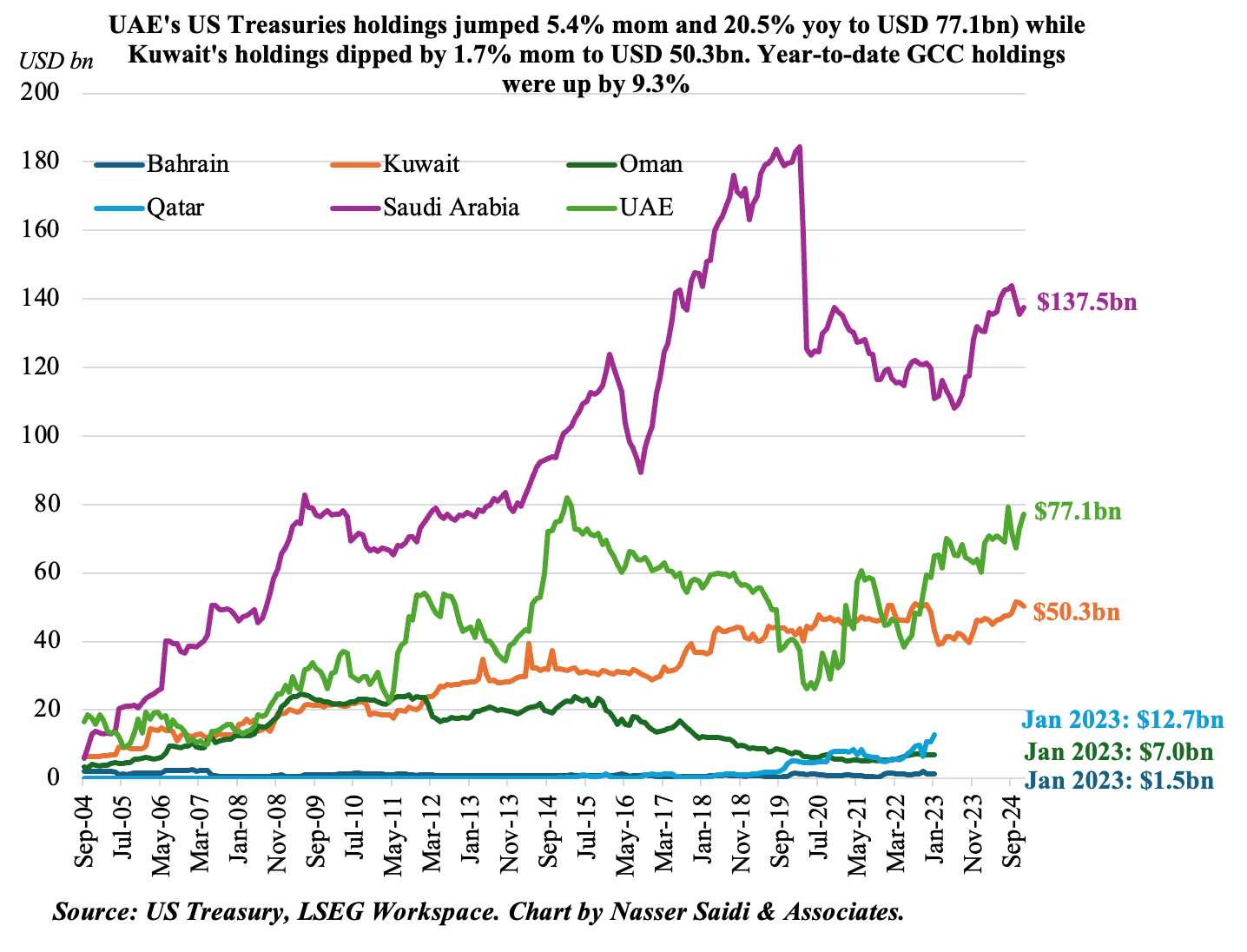

6. GCC nations increase holdings of US Treasuries in 2024; UAE’s holdings surge close to its record high (from Feb 2015)

- Foreign holdings of Treasuries fell to USD 8.513trn in Dec (Nov: USD 8.633trn).

- Japan and China continued to reduce US Treasuries holdings in Dec. Japan is still the largest foreign holder of US government debt – USD 1.06trn at end-2024. China reduced its holdings to USD 759bn, the lowest level since 2009. Some nations increased their holdings including Luxembourg, Canada and Belgium.

- Many central banks have been increasing exposure to assets such as gold: China was the third-biggest buyer of gold in Q3 2024, adding 15.24 tonnes to its reserves.

- From the region, Saudi Arabia and UAE posted monthly increases of 1.44% and 5.4% respectively in US Treasury holdings, with Saudi the 17th largest investor globally.

- GCC nations have been increasing US Treasuries holdings in 2024. At end-Dec, Kuwait, Saudi and UAE posted annual gains of 8.7% (to USD 50.3bn), 4.2% (to USD 137.5bn) & 20.5% (to 77.1bn).

- Saudi holdings are 25% lower than its peak in Feb 2020 while UAE’s is inching closer to its record-high of USD 80.1bn (in Feb 2015).

Powered by:

![]()