Charts of the Week: Saudi inflation numbers (consumer & wholesale prices) show the impact of the tripling of VAT. For now, a proxy indicator of cement sales is showing a pickup post-lockdown, in spite of the VAT hike. We also track the recent changes in Saudi exports, also to understand the impact on government revenues.

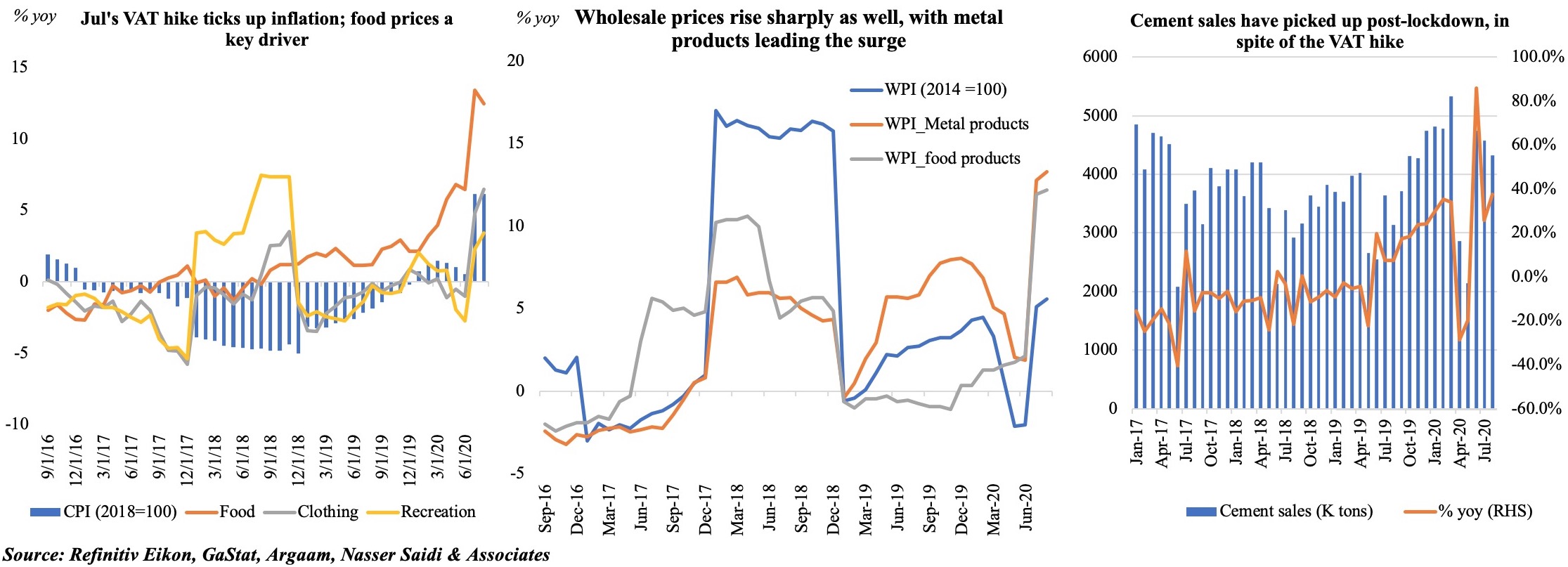

- Saudi inflation picks up post-Jul’s VAT hike

Headline inflation has been climbing in Saudi Arabia from Jul, not surprising given the VAT hike to 15% (from 5% before). The VAT effect is seen across multiple sub-categories, but note that food prices have been ticking up for many months now. Wholesale prices have also increased, similar to when VAT was initially rolled out in 2018, with metal product prices leading the way: these hikes will also filter down to the end-user.

Household spending will be negatively impacted by the VAT hike (as seen from recent SAMA data), there seems to be an increase in cement sales – a proxy for the construction sector spending – after the expected dip during the lockdown period. This could be a result of work continuing on mega-projects like NEOM in addition to a boost from the housing market. The surge in mortgage loans this year (+94.4% year-to-date, with the value in Jun 2020 more than three-times compared to Jun 2019) and the announcement that homes priced at SAR 850k and below will not be subject to VAT will support the housing market. Risks of a severe slowdown in government spending and/or delayed payments could however affect near-term demand.

- Oil sector in Saudi Arabia

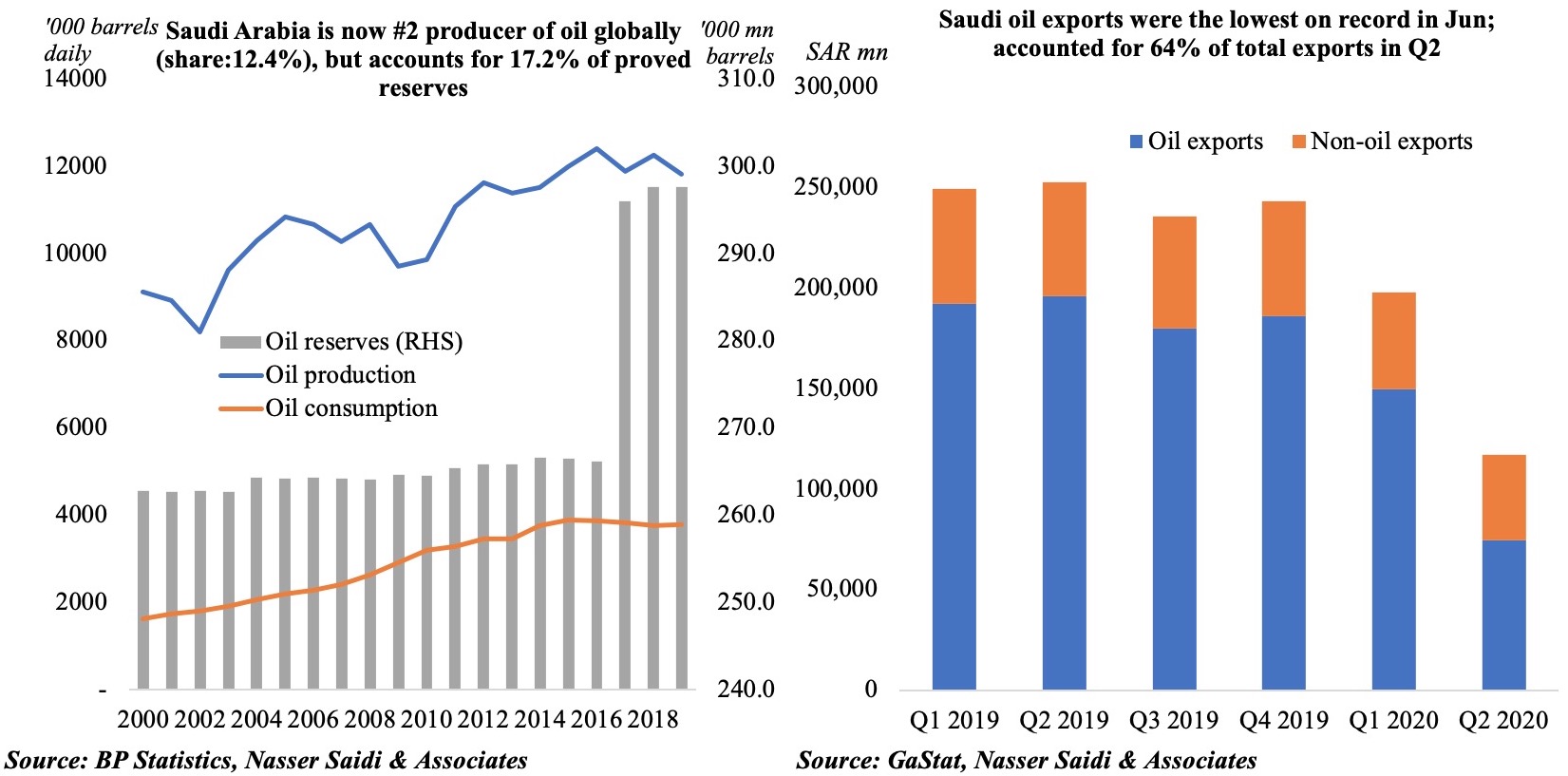

The latest trade data from Saudi Arabia shows a drop in overall exports in Q2 this year (-53.6% yoy): oil exports were down by 61.8% yoy, and the share of oil exports fell to 64% in Q2 2020 vs 77.5% in Q2 2019. Partly attributable to the OPEC+ cuts and overall weak global demand for oil (given Covid19), this implies a substantial reduction in government revenues from oil (in 2019, an estimated 63% of total revenues was derived from oil). At the same time, non-oil revenue will also have declined: government’s postponement of some taxes and fees will bite into revenues and lockdowns would have negatively affected private sector activity.

Q1 has already posted a budget deficit of SAR 34.1bn, and the IMF estimates (as of June 2020) overall fiscal deficit to widen to 11.4% of GDP this year from 4.5% a year ago. Fiscal consolidation efforts have been a cornerstone of every reform discussion and will likely continue to be – removal of subsidies, reducing public wage bills, raising non-oil revenues – at least in the near-term. This will likely be accompanied by more international debt issuances to finance the deficits, in addition to developing its fledgling local debt market.

The recently released data on world energy from BP shows that though Saudi Arabia is now the second-largest producer of oil globally (behind the US), its proven reserves still account for 17.2% of overall global reserves. But, with the rising rhetoric that oil demand may already have peaked, the pertinent question is whether oil could end up being a stranded asset sooner than later. In this backdrop, with the Covid19 pandemic and a resultant push for climate change policies (before it is too late), it is imperative that the recovery model for Saudi Arabia (and rest of the fuel-exporting nations) includes a strong clean energy policy component within overall reforms, alongside a recasting of its economic diversification model and social contracts.

Powered by: