The oped titled “UAE’s Leap Into Energy Independence & the New Oil Order” was published as part of the Clean Energy Business Council’s newsletter issued 1st May 2026.

UAE’s Leap Into Energy Independence & the New Oil Order

Nasser Saidi

The UAE announced it would withdraw from the OPEC and OPEC+ this week, after nearly six decades (it joined in 1967). This move will allow the UAE to operate independent of OPEC’s production quotas and fully monetize its massive investment in capacity, targeting 5mn barrels per day (bpd) by 2027 – a significant jump from its pre-war level of 3.4mn bpd – enabling the country to become one of the top five largest producers. The UAE’s decision is strategic: with its increased energy production efficiency and energy diversification, it cannot continue accepting OPEC quota were increasingly binding constraints on energy policy.

A major driver of the OPEC exit is the UAE’s renewable energy success story. Over the past two decades, the UAE has transformed into a highly efficient and increasingly diversified energy producer. The story is no longer about oil. UAE is home to the Barakah Nuclear Power Plant which generates up to 25% of the country’s electricity needs. The UAE is also home to the Mohammed bin Rashid Al Maktoum Solar Park (the largest single-site solar park using the Independent Power Producer model) and the Al Dhafra Solar PV (the largest single-site solar power plant currently in operation). These projects have consistently delivered record-breaking efficiency, most recently achieving a global-low tariff bid of USD 0.01622 per kilowatt-hour for Phase 6 of the Solar Park. The OPEC exit can accelerate ADNOC’s expansion as a global, integrated energy company operating across the full energy value chain: think reinvesting hydrocarbon revenues into the hydrogen and green data infrastructure required for a greener future and underlying the growing digital economy.

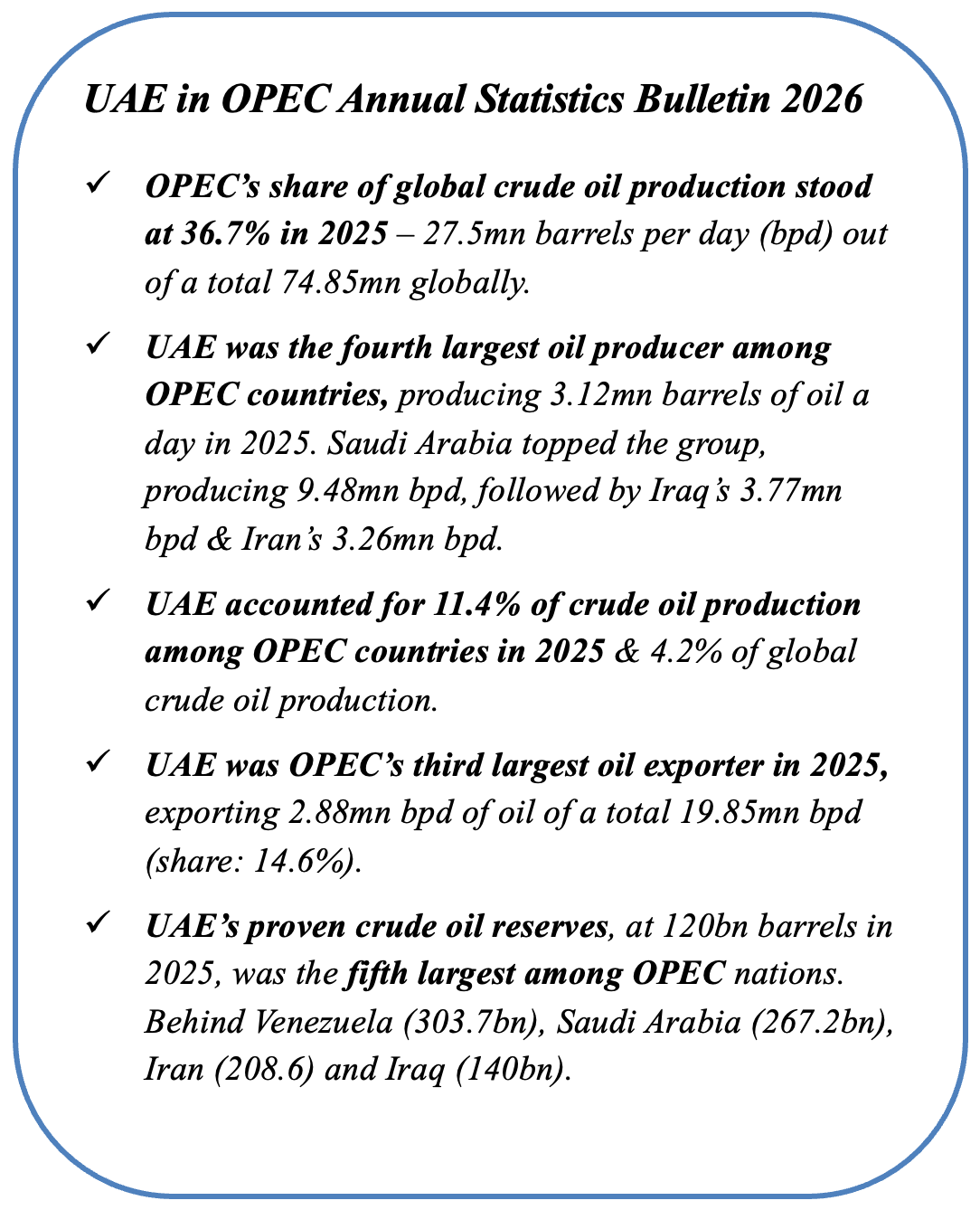

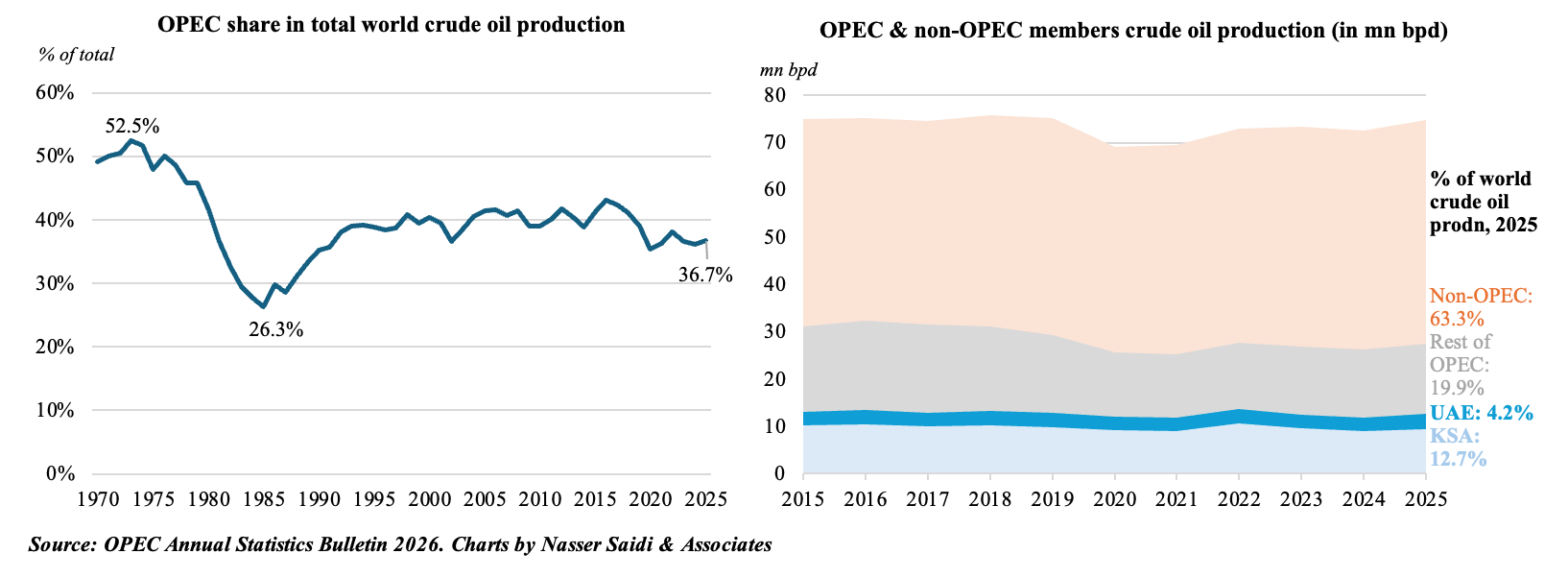

Now, consider the strategic position of OPEC: its share of global crude oil production has been declining over time, from 52.5% in 1973 to around 36.7% last year; without the UAE, this will fall below 30%.

On the supply side, this loss in share stems from the growing competition of non-OPEC members in addition to the widespread availability alternative options to oil & gas (namely renewable energy sources and nuclear power). The shale revolution in non-OPEC member US has allowed it to dominate the supply side: it was one of the top crude oil exporters in 2025 (supplying a record 3.9mn bpd and leading global production with 13.58mn bpd). With oil in Venezuela now being controlled by the US, the potential for a US-pressured Venezuelan exit threatens the power of OPEC+ and OPEC as an organisation. Global solar and renewable energy’s shares have been on the rise: according to IRENA, renewable power accounted for almost 50% of the world’s electricity capacity in 2025, traced back to a record increase in solar installations.

There is also a demand side contraction. As the world’s largest consumer, China’s steady reduction in oil and gas dependence is a signal that the era of peak fossil fuel demand is on the horizon. A growing shift to services, along with increased investment to lower the energy intensity of industry, reduced overall energy intensity. Through the rapid, state-led adoption of EVs and electric transport, combined with massive urban retrofitting programs, Beijing is signalling that the era of peak oil demand is no longer a future projection. As more countries improve energy efficiency – through technological innovation, sustainability policies, along with the rapid adoption of EVs, electric transport and urban retrofitting – the demand for fossil fuels is declining, diminishing OPEC’s leverage.

As both supply and demand dynamics shift, the ability of OPEC+ to artificially support prices will be compromised. Member quotas created space for non-members to take a larger share of the market. With the closure of the Strait of Hormuz, OPEC’s crude oil production[1] already contracted to 20.79mn bpd in Mar from about 28.67mn bpd in Feb.

In the short-term, the effects of UAE’s departure will likely be muted – regional oil flows via the Strait have been throttled. But when the Strait of Hormuz eventually reopens, the world will not return to the “normal” of past years. Instead, it will face a market where OPEC+’s share has dwindled to roughly 28% in real terms. With the market facing a synchronised surge in non-OPEC supply and relatively diminished demand, expect a significant downward repricing of crude which will favour energy diversified oil economies that can survive comfortably in a lower-price regime.

The UAE is uniquely positioned in this regard. With its fiscal break-even estimated at close to USD 45 per barrel and a more-diversified economy, UAE will be able to withstand volatile oil prices better than its GCC peers. The UAE is likely to pursue long-term, bilateral supply contracts to secure future volume, modelled after its CEPAs and Qatar’s recent LNG agreements. In the age of greater weaponisation of the USD, the UAE could even opt to price its oil in Chinese yuan and develop the PetroYuan market in partnership with China and other oil importers especially if the dollar liquidity remains tight. Additionally, the UAE’s sovereign wealth funds (with deep pockets and global investments) can act as automatic fiscal and economic stabilisers using their deep pockets and global investment portfolios to absorb the shock to government spending if oil revenues fall sharply.

Geopolitically, UAE’s OPEC exit registers as a big win for the US, which has called for the breakup of the OPEC+ for many years now. The UAE’s departure could be the first major domino in OPEC’s architecture: other members such as Kazakhstan and Iraq may find production quotas increasingly incompatible with their domestic fiscal needs and past overproduction challenges (though neither of them have UAE-level spare capacities). Remember that Qatar, Ecuador and Angola had chosen to leave the OPEC in recent years. A US controlled Venezuela will likely follow suit and quit OPEC, further weakening OPEC’s market power.

The bottom line is that the UAE’s economic and energy diversification -as a global hub for both Oil & Gas and renewable energy-, growing industrial strength, supported by internationally focused infrastructure, will serve as strategic drivers as the UAE pivots toward a new era of energy autonomy.

[1] Source: OPEC Monthly Oil Market Report, April 2026.

Nasser Saidi is the Chairman of the Clean Energy Business Council.