Download a PDF copy of the weekly economic commentary here.

Markets

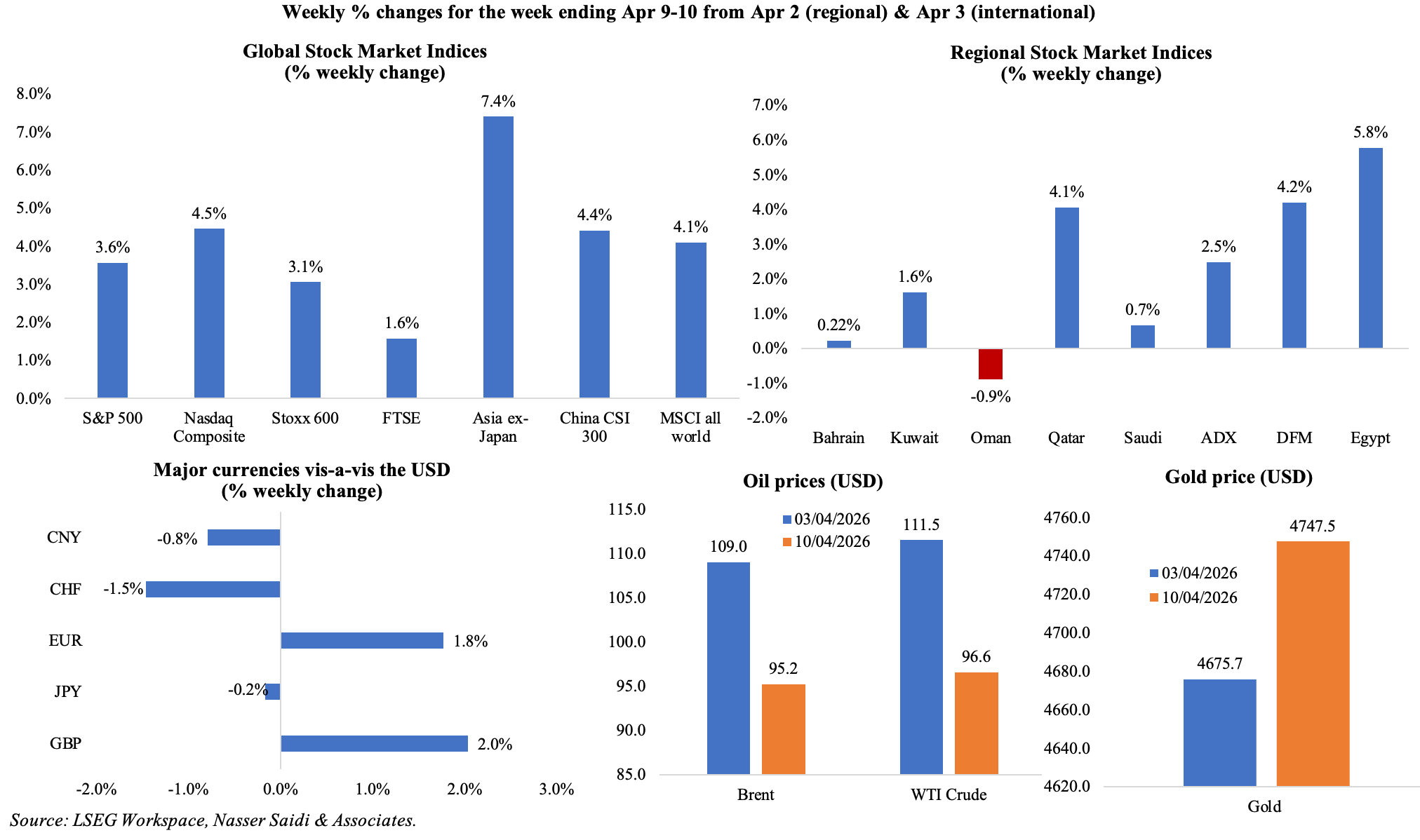

Global equity markets were navigating a landscape defined by cautious optimism last week, given the ceasefire announcement and negotiations over the weekend (which ended in no deal). US indices were also affected by the sharp rise in inflation that will in turn affect Fed rate decisions; European and Asian markets ended positive last week, despite news of a massive capital exodus pressuring regional benchmarks. GCC markets were mostly up on ceasefire optimism though overall sentiment was dampened by jitters over the fragile truce (especially in the backdrop of strikes on Lebanon); Dubai saw its highest intraday gain in 11 years last week. The USD posted a weekly decline last week on peace talk hopes, while both the GBP and EUR rallied and the CNY was trading at the strongest level since 2023. Oil prices saw a sharp drop after the ceasefire announcement, ending last week below USD 100 Brent crude was down 12.7% this week (steepest since Aug 2022) and WTI was down 13.4% (the most since Apr 2020). Gold price increased, serving as the primary hedge against regional uncertainty.

Post weekend’s “no-deal” negotiations, the US announced plans to block Iranian ports today, targeting maritime traffic entering and exiting them “regardless of flag”. This has once again led to a fall in stocks, oil prices rising to above USD 100 and USD regaining its safe-haven status.

Economic Consequences from the conflict in the Middle East & Policy Responses

The global economy is currently navigating the aftermath of the war with Iran, with a very fragile two-week ceasefire and a failure to reach a comprehensive diplomatic “deal” over the weekend.

Even with a permanent truce, the damage inflicted on regional energy infrastructure is so extensive that the recovery curve could likely be measured in years, not quarters. The strikes on critical GCC energy sites have introduced a structural supply-side shock meaning that there will be more permanent effects on prices, the ability to recover energy supply and overall economic recovery. Destruction of energy and related infrastructure (pipelines, ports, etc) implies a larger fiscal effect in these countries: lower revenue, higher deficit and build-up of debt, since capacity has been impaired or destroyed.

The fiscal fallout across the globe is uneven and severe. Emerging markets are facing their largest capital exodus since 2020, as institutional investors flee toward perceived safe havens. In Asia, the strain is manifesting in fiscal interventions: South Korea, heavily dependent on Gulf oil & gas, approved a USD 17.7bn supplementary budget to cushion the blow, while Vietnam and India have resorted to suspending fuel taxes and hiking export duties on diesel and aviation fuel to prioritize domestic availability. China capped domestic fuel price hikes to soften the impact of surging oil prices.

The transport and manufacturing sectors are at the epicentre of this demand destruction. Global airlines are facing expensive fuel costs: global jet fuel averaged USD 197.83 per barrel in the week ending 10th April, up 7.7% versus average in March. The airlines have also begun cutting outlooks and aggressively hiking fares: Indonesia is allowing increases of up to 13% just to keep carriers solvent. In China, the automotive sector has seen a decline in domestic car sales (-15.2% yoy to 1.67mn in Mar) in the face of rising operational costs (including rising fuel prices).

Confronted with a sustained energy shock, central banks are also being forced to roll out supportive measures. TheReserve Bank of India proposed easing capital adequacy requirements to ensure that banks can continue lending amidst this volatility, while Pakistan’s economy has been pushed to a corner following the unexpected repayment of a USD 3.5bn loan to the UAE. Industrial and consumer price inflation and higher core inflation will remain a primary challenge for central banks for months to come, raising the risk of higher interest rates along with lower economic growth rates. The risk of Stagflation is growing.

As the IMF and World Bank meetings convene this week, the narrative has shifted from economic recovery to resilience(our Media Review includes IMF MD’s curtain raiser speech). The global economy is entering a phase of where the cost of logistics and energy will remain structurally higher until the damaged Middle East energy, port and transport infrastructure is fully rebuilt. The ceasefire offers a tactical window, but the structural scarring (inflation expectations and a permanent shift in energy logistics) suggest that the path to recovery will be a long, challenging and potentially expensive one.

We are looking at a multi-year reconstruction phase that will act as a persistent drag on global GDP. For the GCC, an important stabilising role can be played by state-owned enterprises and government-related entities, given that they dominate sectors such as power, water and transport, as well as by sovereign wealth funds. A strategy reset is needed.

Regional Developments Post-conflict

- The World Bank sharply downgraded Middle East growth forecast (excluding Iran) to 1.8% for 2026 (2025: 4.0%),citing the triple whammy of infrastructure destruction, trade disruption and heightened risk premiums. GCC growth is projected to touch 1.3% this year, with growth in Kuwait and Qatar estimated to contract by 6.4% and 5.7% respectively while Saudi and UAE growth by 3.1% and 2.4%. For policymakers, this suggests a long-term trajectory of subdued GDP, requiring aggressive structural reforms to offset the permanent loss of productive capacity (especially in energy-sensitive sectors).

- Bahrain and the UAE signed a five-year USD 5.4bn currency swap agreement, facilitating cross-border transactions, strengthening financial ties and supporting local currency liquidity. This will enable Bahrain’s domestic banks to source AED directly, also reducing dependence on the USD for bilateral transactions.

- Faced with a USD 8bn foreign portfolio outflow (reported by Moody’s) and significant geopolitical headwinds due to the US-Israeli war with Iran, Egypt is reportedly seeking between USD 1.5 to 3bn in emergency IMF funding to stabilize its external position. The country had drawn about USD 2.3bn after three reviews were completed in Feb; the 7th IMF review is scheduled for mid-Jun (for disbursement of USD 1.7bn) and a final review in Nov.

- The approval for Boursa Kuwait to list bonds and sukuk, combined with new restrictions on cash payments (transactions for services valued over KWD 10 or USD 32 must be made via banking channels / e-payment methods and not cash), represents a push toward greater transparency and increased capital market depth. These reforms are designed to create a more resilient domestic safety net.

- Lebanon’s GDP is projected to collapse up to 16% this year, according to the IIF, reflecting the impact of the current war and institutional fragility from recent years. The damage spans tourism, agriculture and manufacturing sectors while rising import bills, supply-chain disruptions, potential lower remittances and reduced labour mobility add to the worries.

- The activation of a “Green Corridor” between Oman and Dubai is a critical logistical hedge intended to sustain global trade flows by bypassing traditional maritime bottlenecks. Prioritizing land-based connectivity to ensure supply chain continuity, this allows international sea cargo arriving at designated Dubai ports or free zones to be transported by land before being shipped onwards from Omani seaports.

- A strategic JV between QatarEnergy and Exxon Mobil – Golden Pass LNG – received US approval to export its first LNG cargoes from the US, effectively diversifying its export footprint away from the immediate vulnerabilities of the Gulf. This move will support Qatar’s strategy in becoming a long-term stabilizer in the global energy transition.

- Despite a significant 700k bpd hit to oil via the East-West pipeline and attacks on the Manifa and Khurais oilfields lowering production capacity by 300k bpd each following Iranian attacks, Saudi Arabia on 12th April disclosed that it had restored full oil pumping capacity via the East-West pipeline & recovered affected volumes from the Manifa oilfield – demonstrated remarkable agility.

- The Saudi Ports Authority and the expansion of railway corridors are being accelerated to create a robust, land-based logistics alternative. The ports reported a 6.66% yoy increase in transshipment containers to 148,192 TEUs in Mar. These integrated logistics systems are no longer just about trade efficiency; they also ensure goods flow amid the Strait blockade.

- Saudi Arabia’s foreign reserves remain a critical buffer and are sufficient to cover imports for about 22 months, according to official data.

- The Saudi construction surge continues to defy war pressures: value of new contracts totalled over USD 4bn in Mar, according to the Saudi Contractor Authority. This was double the value issued a year ago and more than five times that issued in Feb.

- UAE’s Emirates Global Aluminium (EGA) estimates a 12-month window to restore full output at its Al Taweelah smelter following recent attacks. This protracted downtime signals a persistent supply-side squeeze in high-grade aluminium – Wood Mackenzie estimates removal of 3 to 3.5mn tonnes of output this year (total global production of primary aluminium last year was just under 74mn tonnes) potentially supporting elevated prices through 2026.

- Both DIFC and DFSA have rolled out fee relief and support measures including flexible payment plans for tenants, instalments for license renewal fees and support for retailers.

- Ongoing security discussions between Ukraine and Gulf states like Oman, Bahrain and Kuwait signal a broadening of regional defence partnerships beyond traditional Western alliances. According to Ukraine’s President 10-year agreements have already been signed with Saudi and Qatar, while a deal with UAE was announced; these deals include oil and diesel supplies to Ukraine. This shift suggests that GCC are seeking diversification of military expertise to protect critical maritime and energy infrastructure.

- Solar capex across the Middle East have risen by 1-3%, according to Wood Mackenzie, due to the Iran war-related logistics disruptions and supply chain bottlenecks. Approximately 110 GW of solar capacity in the Middle East is in execution or various stages of development.

- GCC tourist inflows are expected to fall by 8 to 19 million visitors this year, according to the Secretary General of the GCC, resulting in potential revenue losses to the tune of USD 13-32bn – highlighting the vulnerability to geopolitical instability.

Macroeconomic Developments in the MENA region

- Headline inflation in Egypt accelerated to 13.5% yoy in Mar (Feb: 11.5%), signalling a renewed uptick in price pressures resulting from the Iran war, with food & beverages and housing & utilities prices key drivers (6.2% and 28.3% respectively).

- Egypt’s Ministry of Finance is recalibrating spending priorities for Q4 FY 2025-26 given the regional turmoil stemming from the war: social safety nets and essential subsidies are being prioritised over non-critical capital expenditure. Fiscal policy is being used as a shock absorber to maintain social stability while adhering to IMF-guided deficit targets.

- Egypt is set to bolster its renewable energy capacity with an additional 2.5GW, reducing the fiscal burden of oil & natural gas consumption. This expansion reinforces Egypt’s medium-term strategy to diversify its energy mix (renewable energy to account for 42% of its electricity generation mix by 2030) and reduce import dependence.

- The trade deficit in Egypt widened by 15% yoy to USD 4.8bn in Jan 2026, driven largely by a 20.3% drop in exports (to USD 3.6bn) alongside a modest 3.2% decline in imports (to USD 8.4bn). Export weakness, particularly in fertilisers (-47.1%) and plastics (-21.3%), was only partially offset by gains in food and petroleum products (+17.5%), while import compression reflected softer demand and lower energy purchases.

- A new three-year investment pact between Egypt and Morocco aims to boost bilateral ties and stimulate cross-border capital flows. Both nations stand to deepen bilateral economic ties, leading a push toward regional integration and South-South cooperation in sectors including industrial, sports and youth, investment and customs among others.

- Libya has announced significant new oil and gas discoveries in partnership with three global energy majors, marking a critical step toward its goal of producing 2 million barrels per day. This signals a potential easing of Mediterranean supply constraints, provided the domestic political environment remains sufficiently stable to permit long-term extraction.

- Syria expects a significant 149% surge in public revenues this year, thanks to oil and gas earnings. Syria’s revenues grew 120.2% to USD 3.5bn in 2025 and with spending up to USD 3.45bn, it posted the first surplus since 1990.

- The unveiling of a USD 300mn tourism project in Syria’s Damascus represents a strategic bet on the high-end hospitality sector as a driver of foreign currency inflows. The planned tourism development, a 50-year joint venture between the Ministry of Tourism and Riyadh-based Ezdihar Holding, signals an attempt to attract investment into services.

Macroeconomic Developments in the GCC

- Signing of the cooperation memorandum to launch the Oman-Japan carbon credit framework signifies a strategic alignment with Asian energy buyers in carbon reduction efforts. By institutionalizing carbon offsets, Oman is de-risking its energy exports and positioning itself as a primary partner for Japan’s 2050 net-zero goals, creating a new green revenue stream beyond traditional crude.

- The UK was Oman’s largest investor in 2025, with FDI from the country rising 11% yoy to USD 42bn, with a focus on energy and manufacturing sectors. US and Kuwait followed, with FDI at USD 22bn and USD 3.6bn respectively in 2025.

- Oman’s USD 3bn road network expansion and the USD 130mn flood repair allocation support developmental efforts in the country. While the road projects enhance the logistics backbone (linking ports like Duqm and Salalah), the flood repairs act as a localized fiscal stimulus, ensuring social resilience against climate-related disruptions.

- The Ministry of Energy in Oman launched a bidding round for five new oil and gas blocks, indicating that it continues to attract investment in its hydrocarbon sector.

- Qatar central bank foreign exchange reserves rose 2.21% yoy to QAR 261.972bn in Mar while official international reserves ticked up 2.6% to QAR 202.338bn. Separately, the industrial production index grew by 6.3% yoy in Jan, with a robust mining and quarrying sector (7.8% year-to-date and 1.4% yoy).

- The 57% surge in firm registrations at the Qatar Financial Centre (QFC) in Q1 2026 is a leading indicator of professional services growth. This influx of more than 800 new firms during the year reflects confidence in Qatar’s business environment.

- Qatar’s PMI plunged to 38.7 in war-affected Mar (Feb: 50.6), as new businesses fell (at the fastest pace in survey history), input prices rose to a 15-month high and with about 70% of respondents expecting output to decline over the next 12 months.

- Saudi Arabia’s Industrial Production Index rose 8.9% yoy in Feb 2026, led by mining and quarrying (+13.0%), while manufacturing expanded 3.6% and the oil activities index rose 11.5%; versus 2.4% growth in non-oil activities. The Feb strength was closely tied to higher crude output: Saudi oil production rose to 10.1mn barrels per day (bpd) in Feb, supporting industrial activity before the regional conflict began to weigh on sentiment and operations.

- Saudi Arabia recorded over 71k new commercial registrations to a total 1.89mn in Q1 2026, demonstrating an unprecedented level of entrepreneurial activity. This is being met by a deliberate shift in the financial sector, where SME lending is being prioritized (33% yoy to SAR 468bn in Q4 2025) to ensure these new entities have liquidity to scale. This growth, alongside a 240% surge in AI-related commercial registrations over five years (to 19,600 in 2025), suggests that the 4th Industrial Revolution is being localized within Saudi borders.

- The surge in domestic tourism in Saudi Arabia (16% yoy to approx. 28.9mn tourists and spending up 8% to SAR 34.7bn) and the strategic deployments from the Cultural Fund (more than SAR 770mn via 165 projects in Q1) are transforming Saudi into a growing leisure market.

- The Saudi Business Confidence Index remains optimistic at 52 points in Mar (Feb: 60.7): this positive reading indicates that the private sector views the internal transformation and the massive giga-projects pipeline, as a more powerful driver than external volatility.

- Abu Dhabi is scheduled to host the IMF-World Bank Annual meetings in Oct 2029, underscoring the importance of the UAE in the global financial arena. This is over 25 years since the summit was held in Dubai back in 2003.

- Mubadala’s assets under management grew 17% yoy to USD 385bn in 2025, making it the 15th largest SWF globally. This growth, backed by a domestic portfolio boost, provides UAE with a massive liquidity engine to fund strategic sectors like AI and renewable energy.

- UAE Central Bank’s 2025 report of “exceptional growth” (assets valued at AED 5.4trn in 2025, supported by a 17.9% growth in credit and a 16.2% increase in deposits) and Emirates Development Bank’s approval of up to AED 9bn in funding this year point to an active banking sector. The USD 2.5bn loan refinancing for AD Ports by local banks further demonstrates the depth of the UAE’s domestic lending markets, reducing reliance on international credit cycles.

- UAE entered the WTO’s list of top 10 global exporters in 2025, with goods and services trade crossing USD 1.637trn. It validates the aggressive CEPA strategy, proving that UAE has successfully diversified its trade basket and become a critical node in the global supply chain.

- KEZAD’s USD 40mn industrial investment and Sharjah’s issuance of nearly 19k licenses in Q1 suggest that UAE’s Operation 300bn industrial strategy is gaining grassroots traction.

- Dubai’s real estate transactions surged 31.0% to USD 68.6bn in Q1 2026 indicates that demand is surging despite regional instability. Foreign investment value also rose 36% yoy to AED 148.35bn.

- Dubai’s new guidance on virtual asset issuance (a global first) and the rollout of superfast EV charging stations (across 600 parking spaces with an investment of AED 150mn; 75 to be installed in two years) show a city-state that is “future-proofing” its regulatory and physical infrastructure simultaneously.

Global Macroeconomic Developments

US/Americas:

- US inflation surged to 3.3% yoy in Mar (Feb: 2.4%), the highest level since May 2024, as energy costs accelerated (12.5%) due to the war with Iran. In monthly terms, prices were up 0.9%, the most since Jun 2022, on higher gas prices (21.2%). Core inflation that excludes food and energy ticked up moderately to 2.6% yoy (Feb: 2.5%); inflation steadied for shelter (3%).

- GDP growth in the US was revised down to a 0.5% annualised rate in Q4 (prev: 0.7%), reinforcing the narrative of a cooling economy heading into 2026. The revision underscores weaker growth from consumer spending (1.9% from the previous 2.0% pace) and final sales to private domestic purchasers (1.8% from 1.9% rate). The core personal consumption expenditures price index rose a seasonally adjusted 3.0% in Feb.

- Personal income in the US declined 0.1% mom in Feb (reversing Jan’s 0.4% gain), the first contraction since May 2025. Disposable personal income fell by 0.1% (Jan: +0.9%) while real DPI declined by 0.5% (Jan: +0.6%). Spending ticked up 0.5% (from 0.3%). This divergence implies a declining savings rate or increased reliance on credit to sustain consumption.

- FOMC minutes reveal that though the current policy rate was seen as appropriate, some policymakers felt that interest rate hikes might be needed to counter inflation. The consensus leans toward higher-for-longer until the labour market shows more definitive slack.

- Durable goods orders fell 1.4% mom in Feb (Jan: -0.5%), the third consecutive monthly decline in orders. Non-defence capital goods orders excluding aircraft rose 0.6% (from -0.4% previously).

- The collapse in the University of Michigan consumer sentiment index to 47.6 in Apr is concerning (Mar: 53.3) as the expectations index slipped to 46.1 (Mar: 51.7) – both levels consistent with recessionary conditions. The one- and five-year inflation expectations jumped to 4.8% (from 3.8%) and 3.4% (from 3.2%) respectively.

- Initial jobless claims increased by 16k to 219k in the week ended Apr 4, with the 4-week average edging up to 209.5k (from 208k) while continuing jobless claims slowed to 1.794mn in the week ending Mar 28 (from 1.832mn); the data are consistent with a gradual cooling rather than a sharp deterioration.

- ISM services PMI slipped one point to 54.0 in Mar, as employment fell (45.2 from 51.8) and prices paid jumped (70.7 from 63) while new orders gained (60.6 from 58.6).

Europe:

- Composite PMI in the eurozone inched up to 50.7 in Mar from the flash reading of 50.5, but remained the weakest since Jun 2025, while services PMI ticked up by 0.1 point to 50.2. German composite PMI was unchanged at 51.9 – currently outperforming the regional average – despite a lower services PMI reading (50.9 from the flash of 51.2).

- Producer price index in the euro area declined in Feb, down 0.7% mom and 3.0% yoy (Jan: 0.8% mom and -2.0% yoy). This the largest yoy drop in PPI since Oct 2024; among countries Spain and Ireland posted the largest monthly declines of 3.1% and 2.6% respectively.

- Retail sales in the eurozone fell 0.2% mom in Feb, extending a pattern of subdued consumption following a flat Jan. Food and drinks sales fell 0.5% following two straight months of growth while non-food sales were flat. In yoy terms, sales grew 1.7% (Jan: 2.1%).

- German data presented a stark divergence: factory orders rebounded, up 0.9% mom and 3.5% yoy in Feb (Jan: -11.1% mom) while industrial production fell 0.3% mom in Feb (on weaker production in the pharmaceuticals and electronics industries); in yoy terms, IP was flat (Jan: -0.9%).

- Exports from Germany grew by 3.6% mom (to a 3-year high of EUR 135.2bn) and imports were up 4.7% in Feb, narrowing the trade surplus slightly to EUR 19.8bn (Jan: EUR 20.3bn).

Asia Pacific:

- China’s inflation eased to 1.0% yoy in Mar (Feb’s 3-year high of 1.3%), as food prices rose at a slower pace (0.3% from 1.7%) and non-food inflation held relatively steady at 1.2%. China had imposed controls on domestic fuel prices in Mar. Producer price ticked up 0.5% (Feb: -0.9%), after 41 consecutive months of decline as energy costs surged due to the war in Iran.

- Overall household spending in Japan fell 1.8% yoy in Feb (Jan: -1.0%), the third straight month of decline as prices remained high. Japan’s nominal wage growth was up 3.3% yoy in Feb (Jan: 3.0%), the largest increase since Jul 2025. Base pay grew by 3.3%, the most in nearly 34 years, while real wages grew by 1.9%.The strong wage data is raising expectations of a rate hike at the next BoJ meeting in end-Apr.

- Current account surplus in Japan surged to JPY 3.9327trn in Feb (Jan: JPY 931bn), the largest since Sep. This reflects a combination of narrower goods trade surplus (JPY 267.6bn) and robust primary income surplus (JPY 4.24trn) thanks to returns on overseas investments.

- Interest rates were held steady at both the Reserve Bank of India (repo and reverse repo rate at 5.25% and 3.35% respectively) and the Bank of Korea (2.5%), given the heightened global economic uncertainty stemming from the wat in Iran. Both countries expect inflation to rise due to the surge in global oil prices.

- Singapore retail sales plunged 4.1% mom in Feb, the steepest since May 2021, after the 6% gain in Jan. In yoy terms, sales rebounded 8.3% (Jan: -0.5%) thanks to higher sales in department stores (16.8%) as well as in food & alcohol (13.6%) and cosmetics (13%).

Media Review:

Cushioning the Middle East War Shock: IMF MD’s speech at the Spring Meetings

https://www.imf.org/en/news/articles/2026/04/09/sp040926-spring-meetings-2026-curtain-raiser

There is still time to resurrect talks between America and Iran

https://www.economist.com/middle-east-and-africa/2026/04/12/there-is-still-time-to-resurrect-talks-between-america-and-iran

The risks of Donald Trump’s Strait of Hormuz blockade plan

https://www.ft.com/content/54003e09-03dd-4a45-90d3-98354f8aadfb?syn-25a6b1a6=1

Dr. Nasser Saidi’s interview with CNN Business Arabic (ceasefire, unsustainable market rallies & pressure in O&G markets)

https://www.youtube.com/watch?v=ebj2jRWtjMk

Powered by:

![]()