Download a PDF copy of the weekly economic commentary here.

Markets

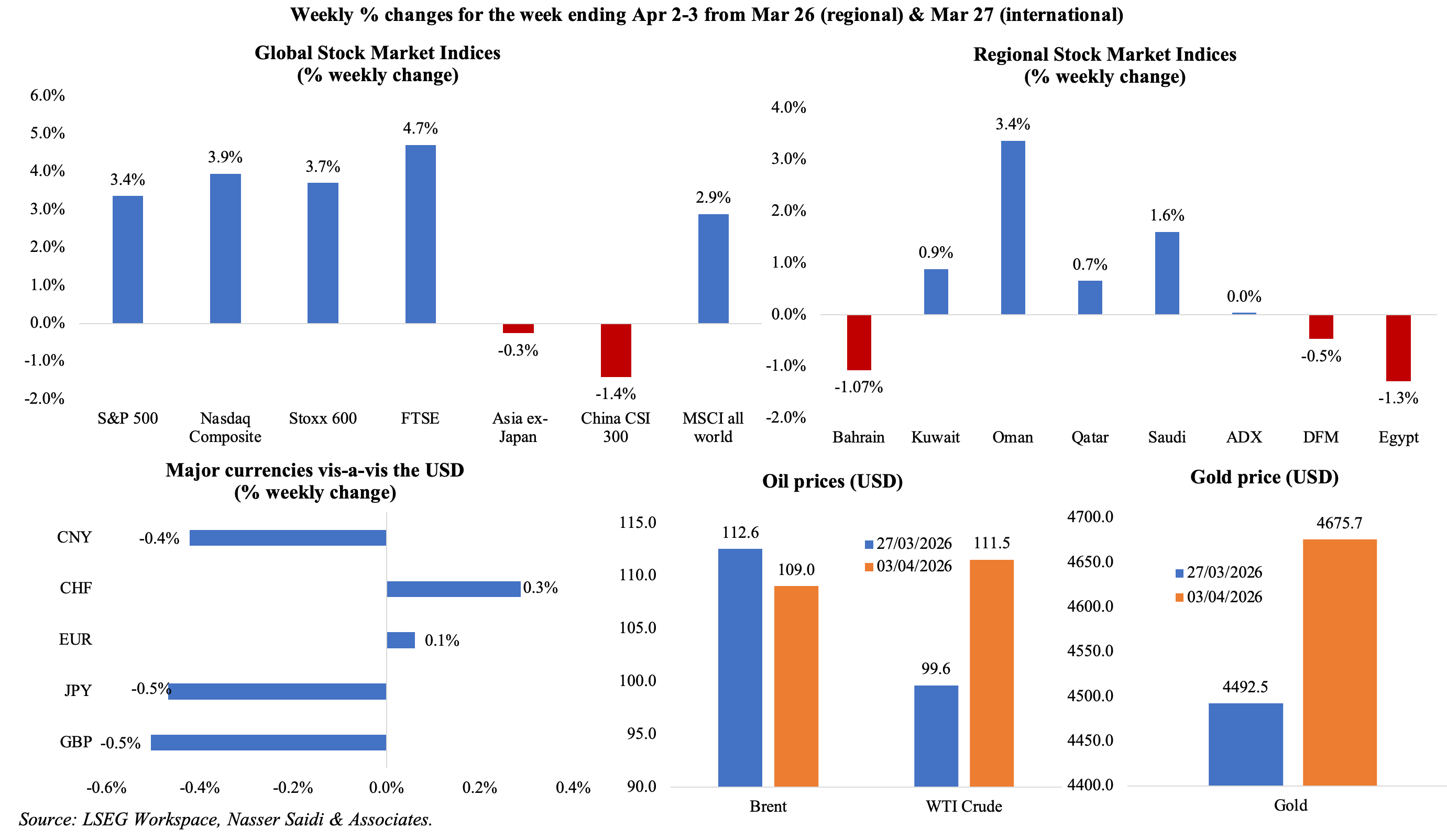

Global equities have been highly volatile with the many (sometimes threatening) war-related messages and headlines. US and European markets closed higher last week (before breaking for the Easter holidays); all markets remain on edge, though Asian markets (including China and Japan) are feeling the weight of potential supply chain disruptions given high dependence on Gulf for energy, fertilisers and petrochemicals. GCC equity markets and investors are weighing the risks of a prolonged Middle East conflict and waiting for clarity on ceasefire talks; less-affected Oman outperformed its peers last week, while UAE equities closed mixed despite news of fiscal support. The dollar continues to behave as a safe haven, while the INR stabilised post its record low after the RBI intervened to curb speculation; the JPY is back near intervention territory. Oil prices are still hovering around the USD 110 mark, while gold prices climbed last week.

Economic Consequences from the conflict in the Middle East & Policy Responses

The broad picture is a war shock that continues to disrupt energy and shipping, but with some selective workarounds rather than a full normalization (for now; a potential 45-day ceasefire has been shared with all parties involved). The IEA, IMF and World Bank have formed a coordination group, warning that the war has already driven one of the largest energy supply shortages on record and is feeding through into oil, gas, fertilizer, food, tourism and broader supply-chain stress, with energy importers most exposed. The FAO in a recent report stated that if the conflict lasts beyond about 40 days, higher energy and fertilizer costs could lead farmers to cut fertilizer use, reduce plantings or switch crops, which would push the consequences further into next year. For import-dependent economies such as Egypt, Jordan and Lebanon and for policymakers across the Middle East trying to prevent another inflation wave, this makes the food channel almost as important as the oil channel.

A limited number of Omani-, French-, Japanese-, Turkish-, Iraqi- and Malaysia-linked vessels have crossed the Strait of Hormuz under Iranian exemptions (about 5% of the pre-war volume of shipping is getting through the strait); India has resumed buying Iranian crude for the first time since 2019 – both situations reduce risk but it is still far away from restoring normal shipping conditions. Across the GCC and many Middle East & Asian emerging market economies, the policy mix is a combination of logistics rerouting and port expansion, liquidity measures and temporary fee reliefs or energy-demand restraint. This matters because it suggests governments are now managing for a longer disruption, not a brief shock.

Global PMIs show a still expanding activity (only 12 of the 33 countries’ readings were contractionary in Mar), but more slowly and with signals of rising inflationary pressures. The latest JP Morgan global manufacturing PMI eased to 51.3 from Feb’s 44-month high (of 51.8) but remained the second-strongest reading since Jun 2022. Meanwhile, country PMIs show a common pattern of expansions in many developed economies but with sharply higher input costs and longer delivery times. The important takeaway is that the war has not yet pushed the world into broad contraction, but there is evidence of slowing momentum and rising cost pressures across regions. Middle East PMIs show that the regional shock is already biting harder than the global average. From the region, Saudi Arabia and the UAE can still emerge as relative logistics and policy winners, because ports, trucking corridors and support packages are helping them absorb and redirect trade, but the PMI data show they are not insulated from the shock. Qatar’s very weak PMI reinforces the view that direct energy-asset disruption is translating into a wider domestic slowdown, while Egypt’s sub-50 reading fits the story of an energy-importing economy already under immediate pressure from higher fuel and power costs.

The most important near-term question is whether the current exemptions for selected vessels broaden into a more durable shipping corridor. If crossings remain small and selective, the shock will continue. The IEA has warned that April disruptions could be worse than March, so the next few weeks will determine whether governments need to rollout further demand-curbing steps (options so far include rationing, remote work or broader fiscal support). Investors should watch whether damage remains contained or spreads further (in LNG, petrochemicals, aluminium and downstream manufacturing). The market impact will rise sharply if damage to infrastructure assets such as Ras Laffan or Borouge results in them being out of commission for longer periods (years and months) rather than temporary.

Regional Developments Post-conflict

- OPEC+ agreed to raise May quotas by 206k barrels per day, but the increase is mostly theoretical subject to the reopening of the Strait of Hormuz (that has currently curtailed the ability of GCC producers to add barrels). This can be read more as a signal of readiness for a post-disruption reopening than an immediate relief for markets, especially with crude near USD 120 and the quota rise amounting to less than 2% of disrupted supply. For now, in the absence of a ceasefire or pause in conflict and near blockade of Hormuz traffic, oil prices are likely to stay elevated (JP Morgan forecast oil above USD 150 should the war extend into mid-May) and policy responses will keep shifting from supply expansion to demand curbs.

- Egypt is absorbing the shock as an energy importer. Egypt has imposed early shop closures and partial remote workto lower energy consumption, citing the surge in its monthly energy bill (to USD 2.5bn in Mar from USD 1.2bn in Jan). It has also raised electricity tariffs for higher-usage households (by 16%) and businesses (by about 20%) from Apr. This looks like the start of a wider energy-rationing mindset in Egypt if external energy prices remain high into the summer; also raises the risk of another inflation surge.

- Oil flows through Egypt’s SUMED pipeline have surged by about 150% since the start of the Iran war, as traders shift toward safer alternative corridors, reported Asharq Business. The core point is that Egypt’s pipeline infrastructure has become a safe corridor, gaining strategic value amid the Strait of Hormuz blockade.

- Passenger traffic at Egypt’s airports rose 8% yoy to 2.2 million passengers in Mar (as of Mar 29th), despite the regional conflict.

- The EBRD is lending USD 20mn to support Egypt’s industrial sector – the construction and operation of three interconnected plants in the Suez Canal Economic Zone, also expected to create around 300 direct jobs.

- Kuwait’s central bank introduced a support package for local banks in the backdrop of the war, while stating that that the sector remains financially strong. The measures include temporary easing of the liquidity coverage ratio, reduction of net stable funding ratio (to 80% from 100%) and lowering the minimum regulatory ratio (to 15% from 18%). Kuwait is trying to get ahead of the shock rather than react late.

- Oman’s market has remained surprisingly firm despite regional war risk given its relatively lower direct exposure vis-à-vis its GCC peers. Oman’s equity market capitalisation rose 39% mom to OMR 5.93bn in Mar, while the main index gained 11% and turnover rose 22%. The exchange is also planning three IPOs this year.

- The value of property sales in Oman rose by about a third to USD 550mn after the war began, with roughly a third of the transactions coming from UAE buyers. In 2025, UAE’s buyers in Oman’s properties accounted for a monthly average of 12%. Oman’s property market could keep benefiting while the uncertainty lasts, though some of that demand looks opportunistic rather than structural.

- In line with other central banks in the region, Qatar Central Bank announced that banks can defer principal and interest payments for affected borrowers for up to three months and boost liquidity support. The apex bank’s liquidity measures include unlimited Qatari riyal repo facilities against eligible securities, a cut in reserve requirements to 3.5% (from 4.5%) and a new term repo facility of up to three months. The authorities reassured that the banking system has strong domestic and foreign-currency liquidity and enough capital to handle short-term funding pressure.

- Fitch placed Qatar’s sovereign credit rating of “AA” on “rating watch negative” e. at risk if war uncertainty persists, especially after strikes on Ras Laffan LNG complex. The damage, which has taken roughly 17% of liquefaction capacity offline for years, is estimated to amount to USD 20bn in annual revenue losses. Qatar’s rating pressure will depend less on current buffers than on whether future damage can be contained and how quickly export capacity can be stabilised.

- The IMF, in a recent blog post, stated that the war is hurting recovery prospects across many economies, with the impact falling unevenly: energy importers, poorer countries and countries with weaker buffers are suffering most. The article highlights higher fuel, food and fertiliser prices, tighter financial conditions and the risk that all paths from here point to higher prices and slower growth. Be prepared for growth downgrades in regional and emerging-market outlooks – though this will be less about a single country shock and more about second-round inflation, trade, fiscal and financing effects.

- Saudi Arabia is strengthening its logistics position, and its overland logistics network could emerge as one of the biggest medium-term winners from the crisis. The country has introduced a new Transport Companies Database meant to connect Saudi and Gulf businesses with vetted logistics providers. It also removed bank-guarantee requirements for some transit cargo, extended port storage by 30 days and allowed 15-day entry visas for Turkish truck drivers. Reports also shows Saudi land customs processed 88,109 outbound trucks to GCC countries between Mar 1-25, underscoring the importance of land routes.

- Saudi Arabia is also accelerating port modernization given global trade route disruptions and shifting cargo patterns. Case in point are the logistics corridors redirecting cargo toward Jeddah and Red Sea facilities, more than SAR 2.2bn in private investment across eight ports, and Jubail Commercial Port’s upgraded container terminal (annual capacity rising to 2.4mn TEUs from 1.5mn TEUs under a SAR 2bn concession with Saudi Global Ports). Saudi ports could potentially capture a larger regional trans-shipment and industrial-export role, but success will depend on ease of customs procedures and inland transport links.

- Dubai approved an AED 1bn support package starting April 1 for three to six months to ease pressure on businesses and households amid regional economic disruption. This includes deferring government fees for three months, extending customs data grace periods from 30 to 90 days and streamlining residency permit issuance and renewal. Dubai will also defer collection of hotel sales fees and the Tourism Dirham for three months from April 1. The package is particularly vital for SMEs, which are more sensitive to negative demand shocks and liquidity crunches. While the Central Bank previously announced resilience package ensures liquidity and credit flow, Dubai’s package provides the necessary fiscal policy support. This is a prime example of pro-active government policies and well-structured economic stress management, designed to absorb shocks from the regional conflict.

- Abu Dhabi government entities and logistics firm 7X launched ADEED, an artificial intelligence-powered platform designed to strengthen trade continuity and business resilience. It is meant to coordinate logistics solutions across air, road and sea transport and provide actionable supply-chain insights for businesses and government.

- UAE raised April fuel prices sharply: the month-on-month rise ranges from just over 30% for petrol grades to more than 70% for diesel, making it one of the steepest monthly increases. This hike will feed through into transport, logistics and consumer costs quickly; it could become a significant driver of inflation if prices stay high into May as well.

- UAE continues to pursue overseas energy investing despite the war: 2PointZero stated that its subsidiary ePointZero will acquire a 100% stake in Traverse Midstream Partners for about USD 2.3bn, subject to regulatory approvals. The broader message is that the UAE is not retreating into defensive capital preservation and is using the crisis as an opportunity to deepen long-term control over energy infrastructure and resilient cash-generating assets.

- The International Energy Agency, IMF and World Bank are forming a coordination group to respond jointly to the war’s economic and energy fallout. With the conflict having caused major global disruptions and one of the largest energy supply shortages in history, possible support will range from policy advice to financing needs assessments and even low- or zero-percent funding.

- The attacks on major aluminium smelters in Abu Dhabi and Bahrain will result in a direct production shock. The US relies on imports for about 60% of its aluminium needs, and the attacked smelters each produce more primary aluminium than the US does domestically. The sharp jump in aluminium prices highlights this issue. Spillover effects could extend into packaging, autos and industrial manufacturing costs. Separately, Abu Dhabi authorities said debris from an air-defence interception ignited fires at Borouge’s petrochemicals plant, damaging the site and forcing operations to be suspended. The incident underscores how even successful interceptions can still impose costs on critical industrial infrastructure.

- Omani-operated tankers, a French-owned container ship and a Japanese-linked gas carrier crossed the Strait of Hormuz under Iran’s policy of allowing vessels without US or Israeli links. This is an important signal that partial movement/ re-opening is possible, helping ease supply chains even though many ships remain stranded.

- India’s refiners have bought Iranian oil for the first time since May 2019: the oil ministry also stated that there are no payment hurdles. If the disruption drags on, more buyers may test previously dormant supply channels, which could reshape energy trade patterns and partners.

Macroeconomic Developments in the MENA region

- Egypt’s non-oil private sector contracted sharply in Mar, with PMI falling to 48.0 (Feb: 48.9), the weakest since Apr 2024, as regional conflict and elevated costs weighed on business confidence. Output and new orders were both at nearly two-year lows, input costs rose the most in 1.5 years, selling prices were up the most in 10 months and business expectations slipped into negative territory.

- Egypt’s central bank left interest rates unchanged at the latest meeting, reflecting a cautious stance. The overnight deposit rate was left at 19%, the overnight lending rate at 20% and the main operation & discount rates at 19.5%, reflecting inflation concerns and a more uncertain external outlook.

- At the same time, fiscal and social policy is trying to cushion households in Egypt. The decision to raise the minimum wage to EGP 8,000 from Jul and additional increases for teachers and healthcare workers represent an expansionary fiscal measure. While socially necessary, the move risks adding to fiscal and inflationary pressures.

- While Egypt reported strong increase in tax revenues – which grew 30.8% to EGP 1.614trn in the first eight months of 2025-26 – thanks to administrative reforms and nominal growth effects, the debt servicing burden remains acute. Interest payments reached EGP 1.63trn during the same period, more than half of public expenditure (which grew 28% to EGP 2.954trn). This underscores fiscal vulnerabilities despite ongoing debt management efforts, better revenue collection and expenditure rationalization.

- Plans to temporarily list around 20 state-owned enterprises on the Egyptian Exchange by end-April (with the first 10 to happen within the first two weeks) mark an acceleration of the government’s privatization and asset monetization agenda. This initiative aims to deepen capital markets, attract foreign inflows and reduce fiscal pressures through non-debt financing. The IMF in a recent report expects four major transactions to reach financial closure under the state-ownership program and raise USD 1.5bn.

- A UAE-UK joint investment (to the tune of USD 500mn) in an Egyptian gas field highlights continued foreign interest in Egypt’s energy sector, particularly upstream gas development. The project is expected to produce nearly 150 million cubic feet of gas and 3,300 barrels of condensate per day when completed (scheduled for by 2028).

- Egypt’s push to raise the share of renewables in its energy mix by 2028 (ahead of 2030 aimed for before) reflects a strategic pivot toward energy diversification and sustainability. This aligns with efforts to reduce import dependency and attract green investment flows.

Macroeconomic Developments in the GCC

- Kuwait’s non-oil PMI plunged to 46.3 in Mar (Feb: 54.5), its first move below 50 in 19 months, with firms reporting the first decline in output and new orders in 38 months and the sharpest since May 2021 (due to disrupted flights and shipping). Responses also pointed to weaker export demand, the first drop in employment in about a year as well as a pessimistic outlook for the first time in 26 months.

- In contrast to the drop in private sector confidence due to the ongoing war, Kuwait approved its FY 2026-27 budget capital spending of about KWD 3.0bn (or USD 10bn), up 33.3%+ yoy, with allocations focused on 117 new projects and 551 projects under construction (including airport, water, power and port projects). This is likely to support non-oil growth and crowd in private sector participation but watch out for execution risks and bureaucratic delays. The finance minister revealed revenues under the 2026-2027 budget to be KWD 16.3bn and expenditure at KWD 26.1bn, with a projected deficit of KWD 9.8bn.

- In the backdrop of the war, Oman still stands out as the most stable macro story in the GCC, though not immune. Consumer prices rose 2.0% yoy in Feb, before the war, with average inflation at 1.7% for Jan–Feb. The largest increases were noted in miscellaneous personal goods and services (13.4%), restaurants & hotels (5.7%), furniture, household equipment & maintenance (3%) and food & non-alcoholic beverages (2.8%).

- International firms began bidding for about USD 1.5bn of mineral projects in Oman despite regional instability, highlighting investor confidence in its resource diversification strategy. The Minerals Development Oman (MDO) had offered five mines to investors in Feb.

- GDP in Qatar grew by 2.0% yoy in Q4 (Q3: 2.9%), as the mining and quarrying activities declined by 2.4% while non-hydrocarbon activities were up 4.5%. Among the latter, the fastest growth rates were recorded in accommodation and food services (+12.8%), construction (12.6%) and transportation & storage (10.6%).

- PMI in Qatar plunged to 38.7 in Mar, the second lowest reading on record and from Feb’s 50.6, affected by the war in the Middle East. Almost two-thirds (64%) of firms reported lower new orders than in Feb and the decline in total output was the fastest since May 2020. While input price inflation accelerated to a 15-month high, weak demand and challenging market conditions saw firms cut charges to retain customers.

- Saudi Arabia’s non-oil PMI plunged to 48.8 in Mar (Feb: 56.1), as regional conflict shrank output and new orders – all reporting the first contraction since Aug 2020. Export orders posted their steepest decline in almost six years amid dampened demand and disrupted business activity; future expectations weakened to the lowest since Jun 2020.

- Saudi unemployment rate eased to 7.2% in Q4 2025 (Q3: 7.5%), reflecting continued labour market absorption driven by private sector expansion and localization policies: total working-age unemployment stood at 3.5% and female Saudi unemployment was down to 10.3% (the lowest level in more than 25 years). Separately, Saudi women’s private-sector employment exceeded 1mn in Q4, accounting for 66% of new citizen jobs added in the sector since the start of the Vision 2030 reforms.

- Saudi banks’ assets reached SAR 5.07trn at end-Feb (8.98% yoy) while private-sector claims rose to SAR 3.19trn (8.8% yoy) and deposits exceeded SAR 3trn for the first time.

- Saudi net FDI inflow surged 90% yoy and 82% qoq to SAR 48.4bn (USD 12.9bn) in Q4 2025 underscoring rising investor confidence and the effectiveness of ongoing regulatory reforms. Separately, services exports reached SAR 66.1bn in Q4, led by travel (SAR 39.5bn) and transport services (SAR 10.5bn) while service imports reached SAR 119.6bn.

- Reuters reported that SpaceX held talks with Saudi Arabia’s PIF over a potential USD 5bn anchor investment in its planned IPO, which would add to PIF’s existing stake (under 1%) and signal that Saudi capital remains active in global deals. Reuters also reported that the Middle East conflict is causing companies globally to delay IPOs and suspend dividend plans.

- Saudi IPO activity declined to an eight-year low in Q1 2026, reflecting weaker market sentiment amid heightened geopolitical uncertainty. This slowdown contrasts with prior years of strong issuance linked to reform momentum and is largely expected to stay so in H1 2026.

- Saudi Arabia issued 38 new mining licenses in Feb, taking the total number of valid mining licenses to 2,963 at end-Feb. Building materials quarry licenses topped the list (1,566 licenses) followed by exploration licenses (1,036).

- Lending to the industrial sector in Saudi Arabia increased significantly in 2025, up 36% yoy to SAR 774mn, reflects policy-driven credit allocation toward strategic sectors and aligns with efforts to expand manufacturing and localize production.

- The entertainment sector in Saudi Arabia recorded more than 89mn visitors in 2025 across 1,690 events, with a total of 75,661 event days and 6,778 participating companies. While 6,490 licenses were issued in the sector last year, there was a 12% rise in entertainment destinations licensed in 2025 (to 472).

- UAE PMI slipped to 52.9 in Mar (Feb: 55.0), the lowest since Jul 2025, with softer output (slowed to its weakest pace since Jun 2021) and new orders reflecting geopolitical tensions. Despite the slowdown, UAE remains more resilient than its regional peers with activity still in expansion territory, supported by domestic demand and business-friendly conditions.

- Fitch Ratings highlights UAE banks’ exposure to real estate as a potential vulnerability amid regional conflict – identifying it as the most likely source of asset-quality stress if the conflict worsens, with weaker activity, slower population growth and softer tourism putting extra pressure on residential and commercial property markets.

Global Macroeconomic Developments

US/Americas:

- US data show a slower and more selective hiring environment. Non-farm payrolls rebounded to 178k in Mar(Feb: -133k), the most since Dec 2024, while average hourly earnings eased (3.5% in Mar vs Feb’s 3.8%), labour force participation inched lower (61.9% vs 62%) and unemployment rate slipped to 4.3% (Feb: 4.4%). ADP employment was softer in Mar, adding 62k jobs (Feb: 66k) and JOLTS openings fell to 6.88mn in Feb (Jan: 7.24mn).

- Initial jobless claims fell 9k to 202k in the week ended Mar 28, with the 4-week average down to 207.75k (from 210.75k) while continuing jobless claims rose to 1.841mn, suggesting firms are still hiring (but more cautiously) and displaced workers are taking longer to find new jobs.

- Consumer demand remains strong. On one hand, retail sales in the US rebounded in Feb, up 0.6% mom (Jan: -0.1%), with sales rising the most at department stores (3%). In yoy terms, sales grew by 3.7% (from 3.2%). Meanwhile, goods trade deficit widened to USD 84.6bn in Feb (Jan: USD 81.8bn) and the overall goods-and-services trade deficit to USD 57.3bn (Jan: USD 54.7bn), pointing to firm domestic demand but also a continuing drag from external trade. Goods exports grew by 5.9% to an all-time high of USD 206.9bn while overall exports also increased to a record high USD 314.8bn (+4.2% yoy).

- On the production side, the picture is mixed. ISM manufacturing PMI increased to 52.7 in Mar (Feb: 52.4), despite slight drops in new orders (53.5 from 55.8) and employment (48.7 from 48.8) while prices paid jumped (78.3 from 70.5). Regional indicators were softer, with the slide in the Dallas Manufacturing Index (-0.2 from Feb’s 0.2) and the Chicago PMI (52.8 from Feb’s 57.7) underscoring an uneven and fragmented manufacturing activity.

- S&P Case Shiller home price indices slowed in Jan, rising by 1.2% yoy (the smallest annual change since July 2023; Dec: 1.4%), showing that higher mortgage rates are continuing to cool price momentum.

Europe:

- While manufacturing activity is holding up better than expected in Europe and the UK, the shock is turning more inflationary. Manufacturing PMI surprisingly edged up in Mar in both Germany (52.2 from preliminary reading of 51.7 and Feb’s 50.9) and the eurozone (51.6, from prelim 51.4 & Feb’s 50.8). German PMI was the strongest reading since May 2022 thanks to new orders and production. In the eurozone, new orders and purchasing activity expanded for the first time in 44 months but job cuts accelerated and business confidence slipped. In both countries, part of the uptick came from longer supplier delivery times and stock-building, which can raise PMI readings even when the underlying story is less healthy. UK manufacturing PMI edged lower to 51.0 from Feb’s 51.7 as respondents expected global demand to slow due to the war. In all three countries, supply chain disruptions and inflationary pressures rose (both input & prices charged) given the Middle East conflict.

- Inflation is where the war shock is already showing up most clearly. Euro area headline inflation jumped to 2.5% yoy in Mar (Feb: 1.9%) while Germany’s harmonised inflation rate jumped to 2.8% yoy in Mar (Feb: 2.0%). Core inflation in the euro area eased to 2.3% (from 2.4%). That mix strongly suggests the current inflation jump is being driven mainly by energy and imported cost pressures, not by demand-driven price pressure.

- EU economic sentiment index slipped to 96.6 in Mar (Feb: 98.2). Businesses were slightly more optimistic about the business “climate” (-0.27 from -0.36), likely due to full order books, while consumers remain deeply pessimistic at-16.3.

- German retail sales fell 0.6% mom in Feb (Jan: -1.1%) and rose just 0.7% yoy (Jan: 1.0%). Themonthly drop suggests that consumers are retreating in the face of these higher price prints. High-frequency data shows a clear shift toward “precautionary saving” as households brace for sustained cost-of-living pressures. Unemployment rate in the EU inched up to 6.2% in Feb (Jan: 6.1%). The overall picture hence says firms may still be busy coping with disrupted supply chains, but households are becoming more cautious and the labour market is no longer improving.

- The UK was a weak link even in pre-war Q4 2025. GDP grew by 0.1% qoq and 1.0% yoy in Q4 while current account deficit had widened to GBP 18.39bn in Q4 (Q3: GBP 10.69bn).

Asia Pacific:

- China’s NBS manufacturing PMI rebounded to 50.4 in Mar (Feb: 49.0) while non-manufacturing PMI also rose to 50.1 (from 49.5) suggesting that large, state-linked firms are seeing a marginal recovery in demand. In contrast, the RatingDog (smaller private sector firms) manufacturing PMI slipped to 50.8 and there was a significant cooling of the services PMI to 52.1 post CNY-holidays (from 56.7).

- Across Asia more broadly, March PMIs point to a region that is still growing but now facing a sharper cost-and-logistics shock from the Middle East conflict. Japan PMI slipped to 51.6 (Feb: 53.0) and in India it fell 3.0 points to a 4-year low of 53.9. India still looks stronger than most peers in absolute terms, but the tone has clearly shifted from straightforward optimism to a more cautious expansion. Separately, industrial output in India grew by 5.2% yoy in Feb (Jan: 4.8%) and cumulative industrial output grew by 4.1%.

- Japan’s labour market is holding up. The Tankan large manufacturers’ index rose to 17 in Q1 (prev: 16), unemployment eased to 2.6% in Feb (from 2.7%) and the jobs-to-applicants ratio edged up to 1.19 (from 1.18).

- However, activity indicators in Japan are mixed. Industrial production fell 2.1% yoy (from Jan’s 4.3% gain), retail sales fell 0% mom and 0.2% yoy and Tokyo headline inflation eased to 1.4% in Mar (Feb: 1.5%), with core inflation excluding fresh food at 1.7% (Feb: 1.8%). High imported energy costs could squeeze margins quickly in the coming months.

Media Review:

How the War in the Middle East Is Affecting Energy, Trade, and Finance: IMF

War: a perfect storm is brewing – op-ed by Dr. Saidi in CNN Business Arabia

Dubai’s Dh1 billion stimulus: What it means for companies and jobs (including Dr. Saidi’s comments)

Inflation or recession? The tug of war in bond markets

Gulf states consider new pipelines to avoid Strait of Hormuz

https://www.ft.com/content/880664d8-e110-4760-8b00-aa3141a770ff?syn-25a6b1a6=1

Powered by:

![]()