Download a PDF copy of the weekly economic commentary here.

Markets

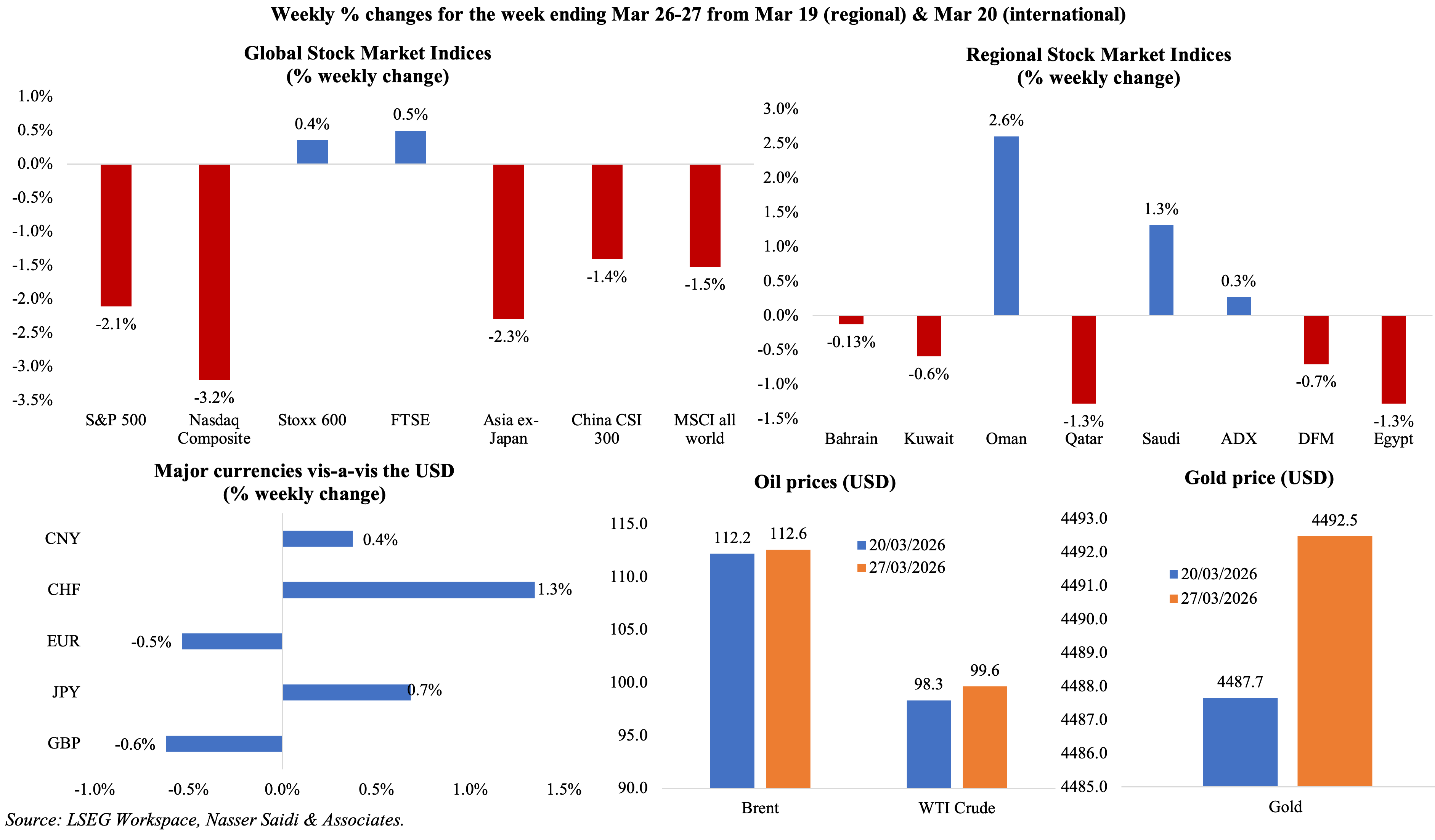

Global equities remained volatile and slid amid rising geopolitical uncertainty and shifting rate expectations. Regional markets were mixed amid the 4-week long war with Iran: Oman is relatively unaffected, supporting its equity index performance, while news of a potential ceasefire supported Saudi markets (though this became more uncertain on Friday, leading to DFM’s weekly drop). The USD continued to play a safe-haven role; GBP posted its worst monthly loss since Oct 2025 and USD rose to its highest level against the JPY since July 2024; in emerging markets, the INR hit a record low of 94.84 per dollar, its most severe drop since 2011-12. Oil prices softened following a pause in US actions against Iranian energy infrastructure but ended the weekly slightly higher on lingering doubts of de-escalation; prices have surged to over USD 115 earlier today (Mar 30th). Gold prices rose last week after falling to a four-month low on Monday.

Economic Consequences from the conflict in the Middle East & Policy Responses

As the war enters its fifth week, President Trump said (in an interview with FT over the weekend) that he wanted to “take the oil in Iran” and could seize the export hub of Kharg Island. The US president also said he was “pretty sure” of making a deal with Iran, even as he warned “it is possible we won’t” reach an agreement.

Iran is currently reviewing a ceasefire proposal, while President Trump announced a temporary pause on energy infrastructure strikes. Even with a tactical pause, the deployment of thousands of US troops suggests a high probability of escalation. Iran is pushing to include Lebanon in any ceasefire framework, complicating negotiations. Furthermore, the conflict seems to be broadening, with Yemen’s Houthi forces entering the war, increasing the risk of a multi-front regional confrontation and raising the likelihood of prolonged instability.

The disruption of traffic in the Strait of Hormuz has ignited international efforts to launch maritime security mechanisms. The UAE indicated willingness to participate in this international effort to reopen Hormuz, signalling a proactive approach to protect trade flows and energy security. Meanwhile, Iran’s decision to allow Malaysian and Thai vessels to transit the Strait of Hormuz after diplomatic talks shows that passage is conditional amid rising tensions; India has also resumed LPG imports from Iran following eased US sanctions. Iran could be planning to use access to the Strait as a strategic bargaining tool.

The conflict is reducing Gulf oil production capacity, with output cuts reflecting both physical disruptions and logistical constraints. Saudi Arabia’s finance minister has warned that a prolonged Iran conflict could further exacerbate oil supply disruptions while the IEA has already labelled this “the largest supply disruption in the history of the global oil market”. The oil shock has led Philippines to declare a national emergency due to the energy shortage, other countries implementing shorter work weeks, work from home policies and a ban on refined fuel exports. Qatar faces rising risks to LNG exports given Ras Laffan shutdown, which also threatens around 11% of global helium supply. US helium distributors are already facing supply shocks that could affect industries from electronics to automobiles.

The latest preliminary PMI data are also highlighting delivery delays and a steep increase in price pressures. Surgingfertiliser input costs are already altering global planting schedules and have farmers worried about harvests, given rising fertiliser costs. This highlights the global spillover of geopolitical shocks into agricultural markets.

Furthermore, tourism-dependent economies like Cyprus and Greece are reporting a 40–45% surge in early summer cancellations, as security concerns and rising airfares (due to fuel and rerouting costs) deter travel. The World Travel & Tourism Council estimates that the conflict is costing the sector at least USD 600mn per day in international visitor spending across the Middle East (via disruptions to air travel, traveller confidence and regional connectivity affecting demand).

Lastly, emerging markets are experiencing a sharp slowdown in debt issuance amid the Iran conflict. Looking ahead, financing constraints could weigh on growth prospects across vulnerable emerging market economies.

Regional Developments Post-conflict

- Regional efforts to repair damaged energy infrastructure could cost at least USD 25bn, according to Rystad Energy, highlighting the extent of disruption caused by the conflict.

- Strikes on Aluminium Bahrain (Alba) in Bahrain that operates the world’s latest single-site smelter and UAE’s Emirates Global Aluminium’s (EGA), the Middle East’s largest producer, highlight the widening economic footprint of the conflict, with critical infrastructure increasingly targeted. Both entities are also major suppliers to the global aerospace and automotive sectors, and aluminium prices climbed around 6% after the attacks.

- Supply-side shock to global energy markets: Iraq’s oil production has declined sharply amid limited storage and as exports via Hormuz remain constrained. Output from Iraq’s main southern oilfields has declined by about 80% to around 800k barrels per day (bpd), according to energy officials; pre-conflict, production was 4.3mn bpd. In this backdrop, Iraqis exploring the revival of an oil pipeline to Syria, to diversify export routes away from chokepoints such as Hormuz.

- Kuwait Petroleum Corporation expects to restore full oil production capacity within four months after the war ends, according to the CEO. This reflects strong recovery capabilities among producers in the GCC; many have reduced production due to disruptions to navigation.

- Lebanon has seen significant infrastructure damage, with up to one million being displaced, highlighting the economic and social cost of conflict spillovers across energy, transport, agriculture and civilian assets. This underscores the risk of prolonged reconstruction burdens and disrupted regional connectivity.

- Oman is experiencing rising import volumes at its ports as trade reroutes away from Hormuz disruptions, underscoring the country’s growing role as a regional logistics alternative.At the Sohar port, ships have increased by 40% since the war and cargo handling capacity was up by 55%. According to Oman’s ministry of transport, communication and information technology, food accounts for half of the imports handled by the port, followed by medicine and industrial materials for general manufacturing

- QatarEnergy has declared force majeure on some LNG contracts due to the Iran conflict, including for customers in Italy, Belgium, South Korea and China. This war has negatively affected production and disrupted supplies.

- Saudi Arabia and Ukraine have signed a defence cooperation agreement, underscoring Saudi’s expanding geopolitical and strategic engagement beyond the region as well as the diversification of security partnerships.

- Saudi Arabia is scaling services to strengthen its position as a regional logistics hub amid the conflict and shipping disruptions. (a) Bloomberg reported that Saudi Arabia’s East-West pipeline is pumping oil at 7 million barrels per day (i.e. full capacity) and has successfully ramped up crude oil exports through the Yanbu port on the Red Sea to 5mn bpd. (b) Saudi Arabia Railways launched a 1,700-kilometer international freight corridor linking the Eastern Province ports (Dammam and Jubail) directly to the Al-Haditha border crossing with Jordan. This link, capable of carrying over 400 containers per train, halves transit times compared to other land transport methods and establishes a critical land-based bypass for goods that previously relied on the Strait of Hormuz. (c) The Saudi Ports Authority inaugurated a new maritime link with Bahrain’s Khalifa Bin Salman Port. Operating through King Abdulaziz Port in Dammam, this feeder connection with up to a 3,000-TEU capacity is designed to alleviate land-border congestion. (d) Multiple GCC logistics initiatives are in place, with Saudi announcing new initiatives to boost supply chains including new storage and redistribution zones in Dammam, allowing for up to 60 days of fee-free storage and a 30-day waiver on maritime documentation requirements for vessels in Gulf waters among others. (e) Saudi is now actively redirecting cargo from the Eastern Region to Jeddah Islamic Port and other Red Sea facilities. It has also added new shipping lines and expanded land transport to over 500k trucks. The Red Sea is emerging as a critical alternative trade route amid Hormuz disruptions, with increased shipping activity and strategic focus. Deeper intra-GCC connectivity should be prioritised post-war to mitigate external trade disruptions and support regional supply chains.

- DP World added three new quay cranes at Jeddah port to support Red Sea trade flows, reflecting infrastructure upscaling and more efficient handling amid shifting trade routes. This underscores the adaptability of regional logistics networks.

- The Dubai World Cup was held over the weekend despite regional conflict, highlighting the resilience of high-profile global events in the UAE. This reflects strong institutional capacity to maintain normalcy and will be critical to maintain Dubai’s status as a global events hub.

- Shipping firm Maersk reported that it has been using a “land-bridge” system in the GCC to deliver critical goods, namely food and medicines, indicating adaptive logistics responses to maritime disruption. It was using ports in Saudi Arabia (Jeddah), Oman (Salalah and Sohar) and UAE (Khor Fakkan) to transport cargo before moving it by land to GCC destinations.

Macroeconomic Developments in the MENA region

- Egypt’s cabinet approved an expansionary EGP 5.1trn (USD 96.7bn) budget for 2026-27, targeting a 27.6% yoy increase in revenues, a primary surplus of 5% and overall deficit of 4.9%. The budget also includes targeted wage increases alongside ambitions for 5.4% GDP growth and improved social spending efficiency. Public debt is expected to decline to 78% of GDP though interest payments is expected to still account for roughly half of spending.This underscores a consolidation strategy anchored in revenue mobilization, particularly tax intake (estimated 79% of revenue), while maintaining fiscal discipline. This will likely be updated and/ or revised given the current ongoing war.

- The Ministry of Finance in Egypt announced the successful recovery of roughlyEGP 1.2bn in state assets and allocated an additional EGP 1.4bn for the treasury, directly boosting revenues and signalling tighter enforcement of public asset management.

- Egypt is prioritizingenergy efficiency and securing financial resources for energy imports to counter regional shocks, according to the PM. Egypt’s decision to raise train and metro ticket prices by up to 25% reflects the pass-through of higher global energy prices and the government’s continued commitment to subsidy rationalization despite the regional crisis.

- Exceptional customs facilitation measures are being offered by Egypt for returned export shipments. Such shipments will be treated as domestic goods and reflects a policy shift toward improving trade logistics and competitiveness while supporting exporters facing blockades.

- Egypt’s manufacturing and extractive index declined by 2.0% mom in Jan,highlighting the short-term weakness in non-oil industrial activity. Production of food products and beverages increased (by 19.4% and 37.6% respectively) ahead of Ramadan while other sectors posted sharp declines.

- Egypt is discussing enhanced cooperation with theWorld Bank and International Finance Corporation (IFC) to expand MSME financing and industrial development, thereby boosting private-sector-led growth. This recognises the constraint of credit access (especially to SMEs) and its effect on productivity and export diversification.

- Remittances into Egypt grew by 21% yoy to USD 3.5bn in Jan, with cumulative inflows reaching USD 25.6bn in the first seven months of FY 2025-26. This provides a critical buffer for Egypt’s external accounts, supporting foreign currency liquidity and consumption.

- A significant gas discovery was revealed in Egypt’s Western Desert, adding to the country’s efforts to bolster domestic energy supply and reduce reliance on imports, which in turn would support both fiscal and external balances. Tests indicate output of about 26mn cubic feet a day of gas and 2,700 barrels a day of condensate from the new gas discovery.

Macroeconomic Developments in the GCC

- Real GDP in Oman grew by 2.4% yoy to OMR 39.3bn in 2025, with the non-oil sector supporting the increase (3.1%) and accounting for more than 70% of total GDP. Among non-oil sectors, services and industry activities grew by 3.1% and 2.4% while agriculture & fishing surged 10.2%. Key drivers included hospitality (+12.3%), agriculture and fisheries (+10.2%), financial (3.7%) and transport/logistics (+3.6%) sectors. Petroleum sector activity rose by 1.1% (Q4: a very strong 3.4% uptick), with natural gas and crude petroleum growing 0.6% & 1.2% respectively. Unlike regional peers facing double-digit GDP contractions due to shut-ins, Oman’s relative safety will likely see growth supported by trade & logistics during Q1.

- Non-oil exports from Oman rose 15.3% yoy to OMR 613mn in Jan, with re-exports up 9.7% to OMR 109mn, underscoring strengthening trade integration and logistics capacity. The UAE remained Oman’s largest market for non-oil exports (54.8% to OMR 141mn), followed by Saudi Arabia (OMR 92mn) and South Korea (OMR 77mn).

- Oman’s government has acquiredSalamAir: the CEO believes this to be supportive of the low-cost airline’s growth trajectory, particularly in fleet expansion and route development.

- Qatar’s industrial producer price index declined by 4.03% mom and 14.9% yoy in Jan, largely reflecting lower prices of the crude oil and natural gas extraction group.

- Strong staycation demand during Eid has lifted domestic tourism and hotel occupancy in Qatar, according to anecdotal evidence, thanks to a long holiday break, competitive hotel offers and resilient consumer spending.

- Non-oil exports (including re-exports) in Saudi Arabia accelerated1% yoy to SAR 32.57bn in Jan 2026. While national non-oil exports saw a slight contraction, re-exports surged by a staggering 95.5% to a record-high SAR 15.8bn. Machinery was the largest segment of total non-oil exports (24.2%), followed closely by chemicals & its products (19.2%) and plastics, rubber and their articles (16.0%). UAE accounted for 36% of non-oil exports; share of non-oil exports to GCC was 44.1%. Overall exports grew 1.6% mom and 1.4% yoy to SAR 98.7bn in Jan, though the share of oil exports continued to decline (67%). Imports fell by 3.3% mom to SAR 81.4bn in Jan, resulting in a narrower trade surplus, SAR 17.3bn.

- NEOMterminated a steel works contract with Eversendai and contracts with Webuild for the construction of three dams and a freshwater lake at The Trojena, highlighting geopolitical developments and execution challenges.

- Saudi Aramcois investing in a major supercomputing initiative with Arabian Internet and Communications Services Co. (known as solutions by stc) to enhance data processing and exploration efficiency to support production.

- Saudi Public Investment Fund’s governor assured that the PIF portfolio is “well diversified and structurally resilient” highlighting their role as a “long-term, patient investor” at the recently held FII summit.

- Point-of-sale transactions in Saudi Arabia continue to expand touching the USD 4bn mark in the week ended March 21st, with value of transactions at SAR 14.79bn. Transactions at restaurants, cafes and bakeries reported some of the highest increases in terms of both value and number of transactions.

- UAE gross banking assets grew 1.4% mom and 18.7% yoy to AED 5.41trn in Jan 2026, indicating strong credit expansion and financial sector resilience. According to the central bank, banks’ gross credit expanded by 1.1% mom to AED 2.598trn in Jan. Growth was primarily domestic, led by a 2.5% monthly surge in government sector credit and a 0.6% rise in private sector lending. Total deposits in Jan rose 0.9% to AED 3.337trn. Notably, resident deposits grew by 1.2% (to AED 3.046trn), successfully offsetting a 2.4% decline in non-resident deposits, demonstrating strong domestic confidence. The CBUAE’s own foreign assets crossed the AED 1.084trn threshold by end-Jan, providing a massive external backstop against currency or liquidity shocks.

- India extended gold import authorisations under the India-UAE trade agreement to June 2026, extending the Mar 31st deadline in view of “prevailing geopolitical developments affecting global trade and logistics”.

- Dubai advanced to 7th place in the Global Financial Centres Index, its highest ranking to date, thanks to the strong financial infrastructure, regulatory environment and appeal to international investors.

- The UAE ranked first in the Arab world and 21st globally in the World Happiness Index, reflecting strong socio-economic outcomes and public service delivery. Kuwait and Saudi were ranked 29th and 31st respectively while Lebanon lagged its regional peers ranking 144th (out of a total 146 countries).

- Dubai Municipality reported a 12% yoy increase in building permits to 10,776 in Q1, signaling robust construction activity and real estate demand. The total permitted built-up area reached close to 3.9 million square metres, up 48% from 2025.

- Mubadala Energysecured a new gas block offshore Indonesia, expanding its upstream portfolio internationally. The first exploration well is expected to be drilled in 4 to 6 years.

- Dubai awarded the first contract on its “20-minute city” masterplan, aiming to enhance urban liveability and reduce commute times through integrated infrastructure. Neither the contract’s value nor the timeline for completion was revealed.

- Food security is becoming a top policy priority: Oman has invested in nine projects worth over OMR 2.3mn in Sohar, targeting enhanced food security through local production and agri-industrial expansion. Qatar aims to reach 120,000 tonnes of local vegetable production by end-2026, achieving over 70% self-sufficiency. This reflects a broader GCC trend of reducing import dependence and strengthening supply chain resilience.

Global Macroeconomic Developments

US/Americas:

- US non-farm productivity was revised down in Q4, up 1.8% qoq (from the preliminary estimate of 2.8%) while unit labour costs jumped 4.4% (vs 2.8%). This – i.e. where workers are producing less per hour while costing much more – is a cautionary signal suggesting that the labour market remains structurally tight. Meanwhile, there was a slight uptick in initial jobless claims (up 5k to 210k) in the week ended Mar 21, with the 4-week average down to 210.5k (from 210.75k) while continuing jobless claims fell by 32k to 1.819mn in the week ended Mar 14. Together, it suggests the Fed may hold interest rates steady while observing inflationary pressures stemming from the war in Iran.

- Current account deficit in the US narrowed to USD 190.7bn in Q4 (Q3: USD 239.1bn), the lowest level since Q1 2021, thanks to primary income balance moving to a surplus (USD 23.92bn) after a deficit in the previous quarter; goods trade deficit also narrowed thanks to a record-high goods exports (USD 563.6bn). Deficit for the full year narrowed to USD 1.12trn or 3.6% of GDP (2024: 4.0% of GDP).

- Richmond Fed manufacturing index moved up to 0 in Mar (Feb: -10) as shipments contracted less and new orders rebounded despite the surge in energy prices since the war started. The Chicago Fed national activity index, in contrast, plunged to -0.11 in Feb (Jan: 0.2), highlighting the regional divergence in industrial performance.

- S&P Global’s US manufacturing PMI jumped to 52.4 in Mar (Feb: 51.6), thanks to an uptick in production alongside new orders rising at the fastest pace since Oct. Even though employment growth slowed and input and output prices surged, business confidence jumped to a 13-month high as tariff worries eased.

- The University of Michigan consumer sentiment index slipped to 53.3 in Mar (Feb: 56.6), reflecting the impact of rising gas prices and financial market volatility, alongside a drop in consumer expectations index (51.7, foreshadowing softer consumption ahead).

Europe:

- Manufacturing PMI surprisingly edged up in Mar in both Germany (51.7 from 50.9) and the eurozone (51.4 from 50.8). German PMI was the strongest reading since Jun 2022 thanks to new orders (fastest in 4 years) and production (quickest rise since Feb 2022). In the eurozone, it was the strongest growth in 45 months thanks to new orders and purchasing activity expanding for the first time in 44 months. UK manufacturing PMI edged lower to 51.4 from 51.7 as respondents expected global demand to slow due to the war. In all three countries, supply chain disruptions were oft-cited and inflationary pressures increased (both input costs and prices charged) given the ongoing conflict in the Middle East.

- In stark contrast to the industrial recovery, consumer confidence in the eurozone declined further to -16.3 in Mar (Feb: -12.3), the lowest since Oct 2023 and the German GfK consumer confidence index dropped to -28 in Apr (Mar: -24.8), the weakest since Mar 2024. The declines reflect concerns over rising energy prices because of the war in Iran.

- Germany’s Ifo business climate index slipped to 86.4 in Mar (Feb: 88.4), the weakest since Feb 2025, with the conflict in the Middle East dampening sentiment. The current assessment stayed put at 86.7 while future expectations were lower (falling to 86 from 90.2).

- Inflation in the UK stood unchanged at 3.0% in Feb, with services inflation easing to 4.2% (the lowest since Mar 2022) while core inflation ticked up to 3.2% (from 3.1%). Producer price index on the input side rose by 0.5% in Feb (Jan: -0.4%) while factory gate prices eased (1.7% from 2.5%). OECD expects UK inflation to average 4.0% this year and BoE predicts a rise to 3.5% by mid-2026 given repercussions from the war in Iran.

- Retail sales in the UK slipped in Feb, down by 0.4% mom (Jan: +2% mom), the first drop since Nov. Looking ahead, the war in Iran and its ripple effects are likely to be felt in the coming months’ sales. Already, GfK consumer confidence fell in Mar (-21 vs Feb’s -19) to its lowest since Apr 2025, with households 12-month ahead assessment of the economic situation declining by 6 points.

Asia Pacific:

- Inflation in Japan eased to 1.3% in Feb (Jan: 1.5%), largely due to the 9.1% drop in energy costs. Excluding food and energy, prices were up 2.5%, moderating slightly from Jan’s 2.6% gain. Excluding only fresh food prices eased to 1.6% (Jan: 2.0%), staying below the BoJ target for the first time since Mar 2022.

- The BoJ Meeting Minutes from Mar reveal a central bank caught in a dilemma: while most members agree that real interest rates are “significantly low” and warrant further hikes toward 75–1.0%, there is growing concern that a rapid pace could stifle the moderate recovery. The risk from the closure of the Strait of Hormuz could reignite cost-push inflation especially should the conflict drag on longer. Markets see a 60% chance of an Apr rate hike.

- India’s decision to slash excise duties on petrol and diesel(effectively cutting INR 10 per litre) is an aggressive fiscal intervention to safeguard consumers from global oil prices (which have almost touched USD 120 per barrel). By pairing this with windfall taxes on fuel exports, the government is ensuring that domestic refineries prioritise the domestic market over high-priced international exports.

- The preliminary manufacturing PMI readings across Asia were consistently lower in March driven by uncertainty over Middle East trade routes: Japan PMI slipped to 51.4 (Feb: 53.0) and in India it fell 3.1 points to a 4.5-year low of 53.8. India posted the fastest rise in input costs in 45 months and manufacturers are turning “cautiously optimistic” from purely bullish, as delivery times lengthen and the cost of petrochemical-based raw materials surged.

- Inflation in Singapore eased to 1.2% yoy in Feb (Jan: 1.4%) thanks to a moderation in housing and utilities prices (0.3% from Jan’s 1.7%) though it masks a more concerning trend: core inflation (ex-transport and accommodation) rose to a 14-month high of 1.4%. While the war is likely to leave an impact on import costs in the coming months, core and overall inflation are currently forecast to average 1.0-2.0% in 2026.

Media Review:

Donald Trump says US could ‘take the oil in Iran’: FT

https://www.ft.com/content/3bd9fb6c-2985-4d24-b86b-23b7884031f5?syn-25a6b1a6=1

Iran Thinks It Can Win a Long War

https://www.nytimes.com/2026/03/28/opinion/iran-war-hormuz-cost.html

Israel’s campaign to sever southern Lebanon in a new “buffer zone”

https://www.reuters.com/graphics/IRAN-CRISIS/LEBANON-ISRAEL-INFRASTRUCTURE/gkvlklaxypb/

The nightmare scenario for global trade: The Economist

https://www.economist.com/interactive/briefing/2026/03/27/the-nightmare-scenario-for-global-trade

Powered by:

![]()