Download a PDF copy of the weekly economic commentary here.

Markets

President Trump posted that following “productive and constructive conversations” with Iran, a decision has been taken to postpone (for five days) “any and all military strikes against Iranian power plants and energy infrastructure”. The markets have since then rebounded, with US stock futures rallying in addition to a decline in oil prices (inching closer to USD 100 a barrel). Reuters has since reported that Iran has denied any direct communication with the US or via intermediaries.

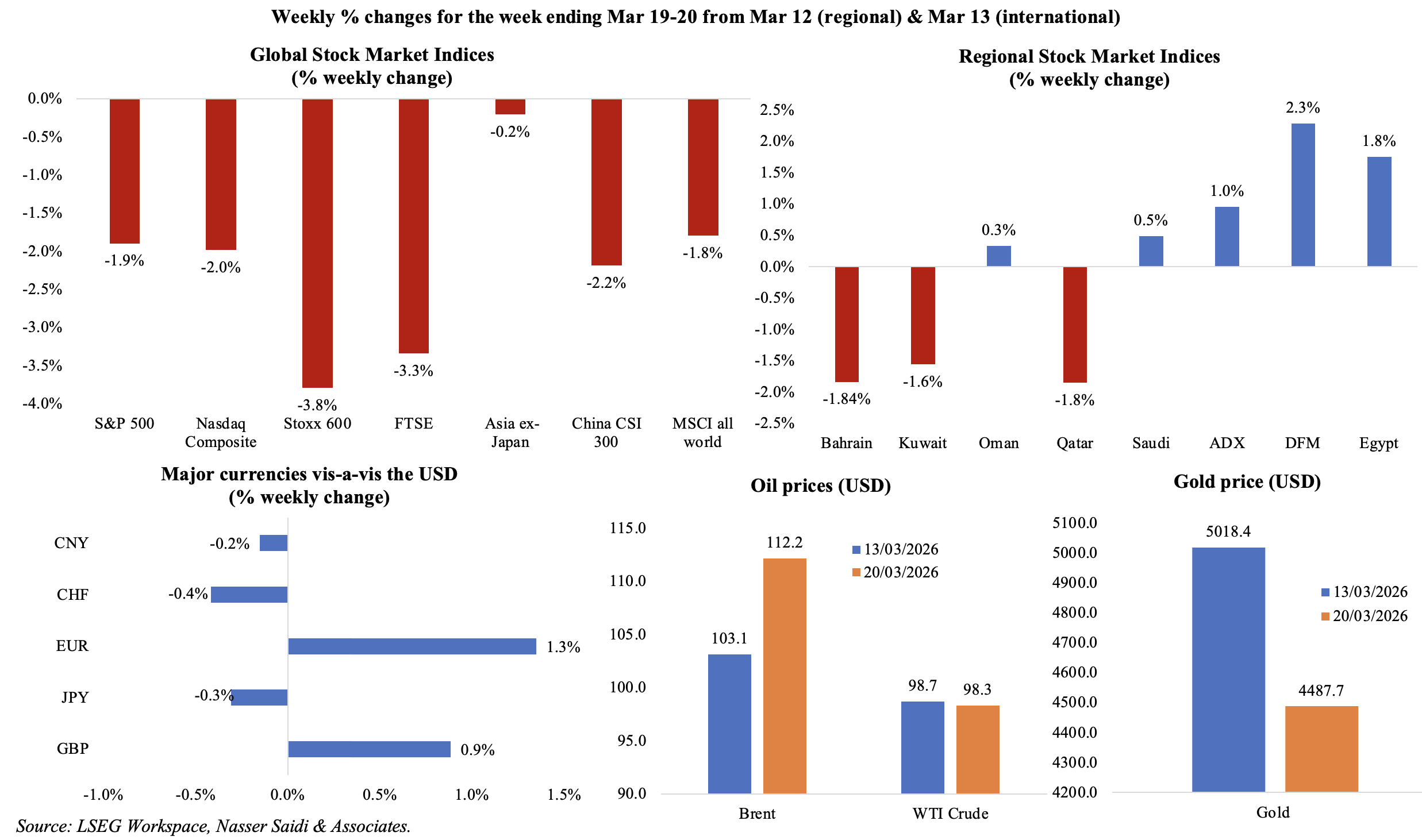

Global market indices were retreating as investor fears rise that war-driven inflation will necessitate a higher-for-longer monetary stance, effectively stalling global growth in 2026. In contrast to global weakness, Middle East equities and particularly the UAE (following its central bank’s stimulus package) ended on a positive note; Qatar, Bahrain and Kuwait fell by more than 1.5% from the week before. The USD remained a safe haven in the backdrop of the war, while the GBP and the EUR gained on hawkish rhetoric from the Bank of England and the ECB. Oil benchmarks have surged to record highs as the conflict shifts from a transport blockade to the physical destruction of oil & gas production and processing infrastructure. Brent oil price ended Friday at USD 112.19 per barrel (some 50% yoy), and the highest since Jul 2022 while the WTI’s discount to Brent hit its widest in 11 years mid-week. European natural gas prices have nearly doubled since the war started while UK gas is now at around 151pence per therm versus 80pence per therm pre-war. Gold posted a weekly decline, suppressed by a surging USD and a hawkish Fed.

Economic Consequences from the conflict in the Middle East & Policy Responses

The US-Israel-Iran conflict moves into its fourth week, transitioning from a near-closure of the Strait of Hormuz to targeting of high-value energy production and processing assets. Following strikes on Iranian energy facilities last week, retaliation was against energy infrastructure across the Gulf, moving the crisis from temporary supply disruptions (difficulty in transporting exports) to more permanent ones (difficulty in production and repair/reconstruction of infrastructure and facilities). Reuters reported that closure of Hormuz resulted in a loss of a full four days of global supply – or some 440mn barrels – during the first 22 days of the war.

The status of the Strait remains the major geo-economic lever. Over the weekend, after signalling a possible winding down of the conflict, US President Trump abruptly reversed course, issuing a 48-hour ultimatum to Iran. The threat of strikes on Iranian power and energy infrastructure should the Strait of Hormuz not be fully reopened to shipping was met with Iran warning a complete closure of the Strait in addition to targeting of US-linked energy and finance institutions and assets and that in the Gulf countries. Attacks on and partial destruction of critical infrastructure – whether it is energy fields and infrastructure, transport and logistics, desalination plants or power sector – will lead to higher prices for longer, increase reconstruction costs and further raise uncertainty of supplies across energy, fertiliser, food, plastics etc. While some major Asian importers are moving to coal to maintain power grid stability, the long-term benefits are likely to come from investing in nuclear and renewable energy assets that are immune to maritime blockades.

Meanwhile, in an extraordinary move to stabilize global prices, the US authorized the temporary lifting of sanctions for 30 days on some Iranian oil (that is currently loaded on vehicles and stranded at sea). This tactical policy reversal, designed to improve immediate supply (bringing about 140mn barrels of oil to the markets), seems to indicate that concerns of US inflationary pressure superseded the traditional pressure of sanctions in the short term. Refiners in India and across Asia moving to secure Iranian crude following US waivers reflects strong demand for discounted barrels in price-sensitive markets. This is in addition to the US lending 45.2mn barrels of crude oil from the US Strategic Petroleum Reserve (SPR) to oil companies, as part of a broader IEA-aligned release. While continued SPR releases may smooth short-term volatility, but cannot fully offset structural supply losses, implying sustained upward pressure on prices. FT reported that LNG shipments that left the Middle East prior to the missile attacks are due to arrive in 10 days after which LNG supplies will remain tight (unless ships pass through the Strait of Hormuz).

With prices hitting new thresholds, major importers (particularly in Asia) are also facing other woes – ranging from fiscal (strain on budgets; for many EMEs, the cost of paying back debt will become more difficult) to exchange rates (Indian rupee at record low, Egypt’s EGP is down nearly 9.0% since the war) and hit on remittances (especially from the GCC) to name a few. Europe is also scrambling for quick fixes to surging gas prices (up 60%+ since the war started). Proposed policy responses, including subsidies, changes in rules on free carbon permits and other market interventions, highlight the trade-off between fiscal costs and social stability. This supply-driven inflation is causing central banks to rethink forecasts, as the costs of alternative logistics is being passed through the global value chain.

Regional Developments Post-conflict

- Disruption at Aluminium Bahrain (Alba) shutdown 19% of its production capacity amid ongoing disruptions at the Strait of Hormuz. Bahrain’s rerouting of aluminium exports via Jeddah (between 40-60%) and through Egypt by air reflects rapid regional logistical adaptation to the Strait of Hormuz disruption, albeit with increased transport time and cost (which will compress margins). The company has about one month worth of raw materials left and has received additional supply from Saudi’s Ma’aden (which owns 20.62% stake in Alba) but are “looking at other channels to extend that period”, according to the CEO.

- Egypt’s monthly gas imports bill more than doubled to USD 1.65bn since the start of the conflict in the Middle East (when it was USD 560mn); diesel costs jumped to USD 1604 per tonne (from USD 665) and butane was up 34%. According to the IIF, the rising cost of oil could result in an increase in Egypt’s expenditure - to the tune of 0.2%-0.55% of GDP. The IIF also revealed that the country saw net capital outflows of EGP 210bn during the first two weeks of Mar, the most since 2022.

- Though the attack on Iran’s main gas field South Pars halted gas flows last Wednesday, flows to Iraq resumed towards end of the week at a rate of 5mn cubic metres per day. Though volumes will rise gradually, how long it will take to reach the contracted 50mn mark remains unclear.

- Crude production at Iraq’s Basra Oil Company has been cut to 900k barrels per day (bpd) from 3.3mn bpd after exports from the southern ports were halted. With storage capacity at its limits and supply risk escalating, Iraq declared force majeure on foreign-operated oilfields, shielding operators from contractual penalties while reflecting the severity of export constraints and operational uncertainty.

- The agreement between the Iraqi federal government and Kurdish authorities to resume exports viaTurkey marks a critical step toward restoring northern export capacity. The deal – which sees pumping at an initial rate of 170k bpd and gradually rising to 250k bpd – will reduce internal fragmentation in Iraq’s oil sector. Post-crisis, Iraq could benefit from restructuring and reconstructing the Gulf energy infrastructure: by rehabilitating the Kirkuk-Baniyas (Syria) and Kirkuk-Tripoli (Lebanon) pipelines, Iraq could facilitate the transit of not only its own crude but also Qatari LNG and Saudi oil to the Mediterranean. This could happen in parallel to land routes from the Gulf through Iraq and Syria for trade.

- Lebanon’s infrastructure is under attack: a main power substation was put out of service in the south on Thursday (19th Mar; though not acknowledged by Israel’s military) and on Sunday (22nd Mar), the main bridge linking Lebanon’s south to the rest of the country was destroyed, with the latter strike seen as a “prelude to a ground invasion”, according to Lebanon’s President. Such hits on infrastructure will add to overall losses (estimated currently at around USD 8-14bn; to give a comparison, the World Bank estimated last year’s conflict losses at nearly USD 11bn).

- France’s decision to double humanitarian aid toLebanon (to the value of EUR 17mn) and the UK’s emergency funding package (of over GBP 5mn) underscore the scale of the humanitarian and economic crisis in Lebanon. Such aid flows help alleviate immediate pressures but does little to address underlying fiscal and governance challenges.

- Oman crude crossed USD 150 for the first time on March 17th, driven by global supply constraints and geopolitical tensions. The increase supports fiscal revenues and external balances in the short term though volatility remains elevated given global uncertainty.

- Qatar. The attack on Ras Laffan that wiped out roughly 17% of Qatar’s LNG capacity represents a major shock to revenues (USD 20bn in lost revenues) and global gas markets. The projected recovery timeline of up to five years implies a prolonged supply gap, tightening LNG balances and elevating spot prices, particularly in Asia and Europe. The damaged units had cost approximately USD 26bn to build, according to QatarEnergy CEO, who also stated that no work is currently taking place on Qatar’s massive North Field expansion project (which could be delayed more than a year).

- Saudi Arabia’s ports stepping in to support regional trade flows demonstrates the strategic importance of Red Sea and alternative export infrastructure. Saudi’s ability to absorb diverted cargo reinforces its role as a regional logistics anchor though capacity limits and geographic constraints remain binding.

- Increased oil exports bySaudi Aramco via Saudi Red Sea ports demonstrates adaptive supply responses: AGBI reported Saudi maybe exporting four times as much oil via the Red Sea compared to last month. This shift helps partially offset regional disruptions, supporting global supply continuity. However, rerouting entails higher costs and logistical complexity.

- The five-pillar Financial Institution Resilience Package launched by UAE’s central bank underscores proactive financial stabilization measures amid geopolitical stress. Though it has not been quantified, proactive liquidity injection and facilities provided by the central bank are necessary and appropriate to maintain orderly and stable conditions in the banking, money and financial markets given the ongoing war conditions which are reverberating globally.This reflects lessons learned from past crises in managing systemic risk (during the 2008 crisis) and the anticipatory move in 2020 when a AED 100bn comprehensive Economic Support Scheme was announced (specifically for retail & corporate customers affected by the pandemic).

- The sharp decline in UAE crude output (by more than half) due to forced shut-ins reflects the direct production impact of export bottlenecks. Even with available capacity, the inability to move crude constrains output and revenue generation.

- UAE’s alternative routes for trade: The Oman-Dubai green corridor initiative and the new Sharjah-Saudi Arabia (Dammam) trade bridge initiative to expedite diverted cargo reflects rapid policy innovation to maintain trade continuity. Streamlined customs and logistics processes can partially offset the inefficiencies created by rerouting. Such corridors could become permanent features, enhancing regional trade integration and resilience.

- Average jet fuel prices were USD 175 a barrel last week, according to IATA, the highest in a decade and up from USD 94 in mid-Feb. This will have an impact on airlines operating margins (fuel had accounted for 31% of Emirates total operating costs in the 12 months to 31 Mar 2025). Furthermore, the jet fuel premium over crude has jumped to nearly four times its mid-Feb level given the supply shortage; this gap is expected to continue until shipping resumes. Separately, IATA’s warning that there are no winners in the Middle East crisis underscores the broad-based economic fallout across aviation and trade. Airspace disruptions increase costs, extend flight times and reduce efficiency for global carriers – with ripple effects through tourism, cargo logistics and business travel.

- The World Food Programme warned that conflict could push an extra 45mn people into acute hunger. The current level is already at a record high 319mn persons. Food insecurity on this scale extends beyond immediate conflict zones; it can destabilize labour markets, increase migration pressures and strain public finances across affected regions.

- US approval of more than USD 16.5bn in arms sales to Middle Eastern countries (UAE and Kuwait at USD 8.4mn+ and USD 8bn respectively) and Germany’s easing of arms export restrictions to Gulf states highlight a rapid militarization response, also signalling expectations of prolonged instability.

- S&P Global Ratings estimate that banks in the GCC could face domestic deposit outflows of USD 307bn – given heightened financial contagion from a prolonged conflict. Capital outflows could tighten liquidity, raise funding costs and constrain credit growth.However, banks currently hold around USD 312bn in cash or at central banks to absorb such outflows.

Macroeconomic Developments in the MENA region

- Egypt’s petroleum ministry stated that it will settle USD 1.3bn in arrears to international oil companies by Jun. This signals an effort to restore investor confidence in its hydrocarbons sector and might encourage foreign companies to resume drillings and/ or invest more.

- Egypt plans to privatise the operation of desalination plants, aiming to leverage private sector efficiency and financing to meet rising water demand. There was no mention of how many facilities would be offered (these would be located along the northwestern coastline), but the initiative aligns with broader structural reforms and efforts to reduce fiscal burdens and is likely to attract international investors, particularly amid increasing water scarcity risks.

- Ongoing conflict risks are undermining Lebanon’s already fragile plan to return bank deposits, exacerbating depositor uncertainty. Political instability and ongoing security concerns (which has seen over 1mn people displaced this month) continue to delay reforms required for banking sector restructuring.

Macroeconomic Developments in the GCC

- Inflation in Kuwait eased to 1.99% yoy in Jan (Dec: 2.07%), the lowest since Jul 2020, as food inflation slowed to 5.33% (Dec: 5.42%).

- Kuwait’s new decree authorises theKuwait Investment Authority and Central Bank of Kuwait to conduct borrowing on behalf of the Ministry of Finance, marking a shift toward more flexible fiscal management. This mechanism may help bridge funding gaps in the backdrop of years of legislative gridlock and delayed debt law reforms.

- Oman’s real GDP grew by 2.4% yoy to OMR 39.3bn in 2025, with growth supported by non-oil sector expansion (3.1%) and an uptick in petroleum activities (1.1%). Among the fastest growing sectors were refined petroleum products (13.5%), accommodation & food services (12.3%), agriculture & fishing (10.2%) and information & communication (5.3%). Overall services activities grew by 3.1% and manufacturing by 2.5%. Oman’s relative safety amid the Middle East conflict will likely see the country growth remain stable during Q1: trade and logistics will support growth.

- Inflation in Oman edged up to 2.0% in Feb (Jan: 1.4%), driven by increases in food costs (2.8% from Jan’s 0.9%) and a rebound in transport costs (0.2% from -0.3%). Though headline inflation remains moderate, domestic demand recovery is leading to gradual upticks.

- Oman’s producer price index fell in Q4 (-3.3% yoy from Q3’s 4.3% drop) due to declining oil and gas prices (-6.0%), highlighting the economy’s exposure to energy market fluctuations.

- Rising geopolitical tensions during the Middle East conflict could delay the implementation of the Oman-India Comprehensive Economic Partnership Agreement (CEPA) as trade and investment flows stand partially disrupted by heightened regional uncertainty and logistical risks. Timely execution of this CEPA (scheduled to take effect on Apr 1st) will depend on geopolitical de-escalation and secure trade corridors.

- Oman’s tourism sector experienced a surge in hotel bookings during Eid, demonstrating resilience despite regional geopolitical tensions. Domestic and regional travel demand remains strong, with 70% of its nearly 64k guests (+60% yoy) coming from the Gulf.

- Inflation in Qatar increased to 2.5% in Feb (Jan: 2.28%), driven by higher prices of miscellaneous goods & services (21.16%), recreation & culture (4.92%) and food (2.05%) while transport costs eased (1.7%).

- Qatar reaffirmed that it holds strategic water reserves sufficient for four months of consumption and food reserves for up to 18 months, underscoring resilience. The Minister of Interior disclosed that these food reserves have not been used yet and that additional supply lines had been opened to stabilise food supplies.

- Saudi Arabia’s producer price index for Jan reflected easing cost pressures (0.4% yoy vs 1.0% in Dec), given a 0.1% uptick in the manufacturing prices and a 1.8% increase in electricity, gas, steam and air conditioning supply prices.

- NEOM terminated a USD 1bn tunnel contract that was central to The Line due to “business restructuring”, underscoring challenges in mega-project delivery. Settlement for work completed had been finalised, according to Hyundai that was part of the consortium.

- Saudi Arabia’s holdings of US Treasuries grew by 6.22% yoy to USD 134.8bn in Jan, though in monthly terms it dipped by USD 14.7bn. Saudi ranked 18th globally, falling one place as South Korea increased its holdings (to USD 141.3bn). The UAE increased its holdings to USD 112.4bn (17.6% mom and 21.4% yoy), the highest since Apr 2025, to become the 20th largest holder globally.

- The Crown Prince of Abu Dhabi approved a housing benefits package worth AED 4.21bn for citizens in the emirate, reinforcing social welfare and domestic demand.

- The UAE launched phase one of its R&D tax incentives programme, aimed to encourage innovation and private sector investment in technology. Under this, businesses will be able to benefit from a non-refundable R&D tax credit of up to 50% on qualifying expenditure of up to AED 5mn.Over time, effectiveness will depend on uptake rates and integration with broader industrial policy frameworks.

- ADNOCand OMV are set to complete a USD 60bn joint venture by end-Mar (first announced in Jul 2023), creating the world’s fourth largest by nameplate production capacity. While this reflects global consolidation trends and ambitions to scale downstream operations, integration execution and market conditions will determine the JV’s long-term value creation.

- Starlinkbegan operations in the UAE, expanding high-speed satellite internet access. The rollout comes amid heightened regional tensions, highlighting the importance of resilient communications infrastructure. The platform introduces new competition in the telecom sector but its future adoption will depend on pricing, regulation and domestic competition.

- UAE reaffirmed that capital flows remain unrestricted following rumours that stated the opposite, underscoring UAE’s commitment to economic openness and the free movement of capital. This assurance, significant amid regional geopolitical tensions, supports investor confidence and financial market stability.

- S&P Global validated Gulf sovereign ratings. Ras Al Khaimah’s A/A-1 credit rating with stable outlook was affirmed, reflecting solid fiscal performance and manageable debt levels. Qatar retained its AA/A-1 rating with a stable outlook, supported by strong hydrocarbon revenues and fiscal buffers.

Global Macroeconomic Developments

US/Americas:

- The US Fed left rates steady at 3.5-3.75% given expectations of higher inflation because of the war in the Middle East; the inflation print for Feb was already ticking up, prior to the conflict, amid a cooling labour market. By Friday, the sell-off in bonds implied that investors were preparing for a more hawkish Fed and possibility of no more rate cuts this year; a one-in-five chance of a Jun rate hike is being priced in according to the CME FedWatch tool.

- US Producer Price Index (PPI) and core PPI jumped to 3.4% yoy and 3.9% in Feb (Jan: 2.9% and 3.5% respectively); in monthly terms, PPI ticked up 0.7%, thanks to higher services costs (0.5% mom following Jan’s 0.8% gain) and a rebound in food (1.1%) and energy (2.3%) prices. Conflict-related surging energy and logistics costs are likely to lead to higher energy prices and food costs in the coming months. US average retail gas prices have jumped more than 30% since the start of March (quicker than during the 2022 Russia-Ukraine invasion).

- US industrial production inched up marginally in Feb, up 0.2% mom (Jan: 0.7%), with manufacturing up 0.2% and durable and non-durable manufactured goods production up 0.1% and 0.2% respectively. Meanwhile, the sharp divergence between the NY Empire State Index (Mar: -0.2 vs 7.1 in Feb) and the Philadelphia Fed Survey (Mar: 18.1 vs 16.2 in Feb) suggests a fragmented manufacturing sector and uneven supply-chain pressures as firms start to price in the Strait of Hormuz blockade.

- In the US housing market, a 1.8% growth in pending home sales in Feb (partly thanks to the slight decline in mortgage rates) stood in contrast to a 17.6% plunge in new home sales (the slowest pace since 2022, to 587k). The housing affordability crisis seems likely to worsen in the months ahead as geopolitical uncertainty keeps Treasury yields elevated (mortgage rates track the benchmark 10Y-Treasury yield) amid higher input costs (including labour).

- Initial jobless claims slipped by 8k to 205k in the week ended Mar 14, with the 4-week average down to 210.75k. Continuing jobless claims rose by 10k to 1.857mn in the week ended Mar 7.

Europe:

- Both the ECB and BoE held rates steady at their respective meetings last week, as policymakers braced for the inflationary impact from the closure of the Strait of Hormuz. Like the Fed, markets are pricing in rate hikes this year to dampen price pressures.

- Inflation in the euro area stood at 1.9% yoy in Feb (Jan: 1.7%) while core inflation clocked in at 2.4% (Jan: 2.3%).The current blockade at the Strait of Hormuz and the related risk premium is threatening a new wave of imported cost-push inflation: the ECB raised its inflation forecast to 2.6% this year in a “baseline” scenario (vs 1.9% in its Dec forecast) and predicts higher uptick in case of a prolonged war in the Middle East. Growth was lowered to 0.9% (from 1.2% forecast in Dec).

- Producer price in Germany fell 0.5% mom and 3.3% yoy in Feb, with lower energy prices the main reason for the drop (-1.8% mom and -12.5% yoy).

- The German ZEW economic sentiment plummeted to -0.5 in Mar (from 58.3 in Feb)and the Eurozone to -8.5 (from 39.4), representing a historic reversal of optimism. Though the current situation improved to -62.9 in Germany (Feb: -65.9), investors are rapidly pricing in the risks from the disruption of critical energy pipelines, which will negatively impact Europe’s growth.

- UK unemployment remained unchanged at 5.2% in the three months to Jan and the easing of average earnings to 3.9% (including bonus) suggests that the labour-market-driven inflationary impulse is cooling just as energy-led inflation is starting to increase.

Asia Pacific:

- The PBoC left interest rates unchanged last week while the Governor revealed (at the China Development Forum 2026) that the apex bank will “continue to implement a moderately loose monetary policy”.

- The 6.3% yoy growth in China’s industrial production during Jan-Feb (Dec: 5.2%) and the unexpected recovery in fixed asset investment (1.8% yoy in Jan-Feb vs a 3.8% drop in 2025) suggests that the domestic manufacturing sector is slowly recovering, offsetting external vulnerabilities. Retail sales grew 2.8% in Jan-Feb (from Dec’s 0.9%) while the 5.7% drop in FDI into China reflects a cautious approach from investors (ahead of the Trump-Xi Summit).

- The Bank of Japan left interest rates unchanged and did not commit to an Apr hike but announced that a new indicator on inflation would be introduced and that the neutral rate of interest estimate would be updated. This will enable the BoJ to understand the price movements emerging from domestic demand.

- Export growth from Japan moderated in Feb (4.2% yoy vs Jan’s 16.8%) while imports accelerated by 10.2% (Jan: -2.6%), moving the trade balance to a surplus JPY 57.3bn from a deficit of USD 1.1635trn in Jan.

- Industrial production in Japan grew by 4.3% mom and 0.7% yoy in Jan (Dec: 2.2% mom and 2.3% yoy); core machinery orders fell 5.5% mom in Jan reversing Dec’s 16.1% gain.

- WPI inflation in India ticked up to 2.13% yoy in Feb (Jan: 1.81%), the fastest rise since Feb 2025, with increases in food (2.19% from 1.55%) and non-food articles (8.8% from 4.97%) while prices for fuel and power continued to decline (-3.78% from -4.01%). Given India’s80-85% dependency on Qatar for LPG and its reliance on fertilizers from the Middle East, any prolonged production halt will likely move this inflation higher – in both wholesale to retail (also given the impact of the latter on the upcoming agriculture season).

Media Review:

How LNG strikes on Qatar could reshape global energy markets (with Dr. Saidi’s comments)

https://www.agbi.com/analysis/oil-and-gas/2026/03/how-lng-strikes-on-qatar-could-reshape-global-energy-markets/

Iraq faces polycrisis as Iran war grinds its oil exports to a halt (with Dr. Saidi’s comments)

https://www.thenationalnews.com/business/energy/2026/03/18/iraq-faces-polycrisis-as-iran-war-grinds-its-oil-exports-to-a-halt/

Iran war is a risk to the flow of Gulf funds around the globe

https://www.ft.com/content/bdc2ad8c-d22f-44b5-aec4-14740f810a66

There is plenty of scope for the Iran war to intensify

https://www.economist.com/briefing/2026/03/19/there-is-plenty-of-scope-for-the-iran-war-to-intensify

Who controls the global petrochemical industry, and how might that change?

https://www.piie.com/publications/working-papers/2026/who-controls-global-petrochemical-industry-and-how-might-change

Powered by:

![]()