1. Immediate shocks from the Iran Conflict. Disruption at the Strait of Hormuz could lead to Energy, Trade and Inflation Spillovers

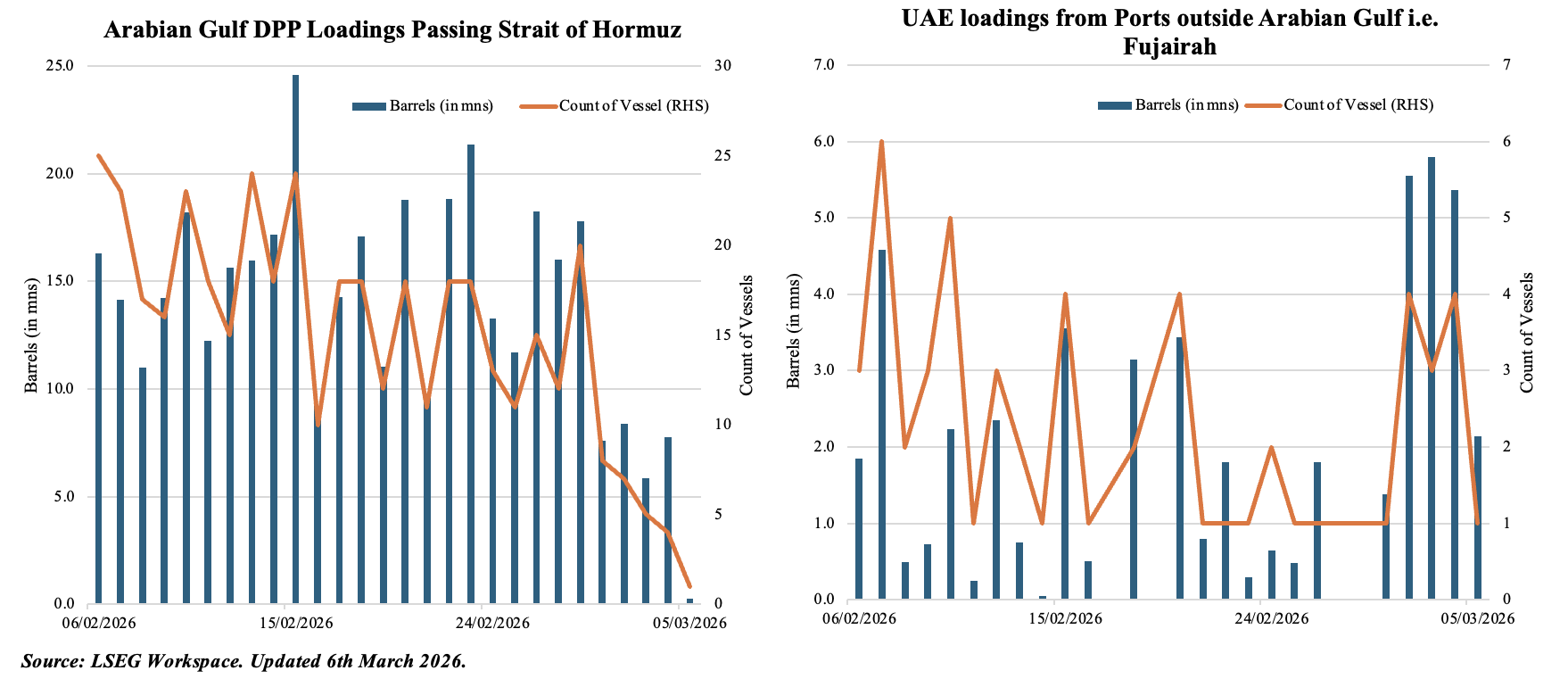

- Strategic chokepoint disruption: The Strait of Hormuz, through which flows about 20% of global oil and major LNG flows, faces severe disruption, with tanker traffic slowing or rerouting or vessels anchoring. Affected countries have been exploring alternative routes.

- Energy market volatility: Impact on oil supply from two fronts: (a) inability to transport oil from recent hikes in production due to the impact on Strait of Hormuz; (b) if Middle East energy infrastructure are targeted and hit, production could stop + it will also delay how quickly production can come back online when a ceasefire is declared. Both Brent & WTI have crossed USD 85 per barrel as of Mar 6th (3pm UAE time), but prolonged disruption could drive oil closer to USD 100 per barrel.

- Shipping and insurance shock: War-risk premiums and insurance costs have surged, forcing some shipowners to avoid Gulf routes and increasing global freight rates. Premiums have jumped to about 1% of hull value from about 0.2% last week (Source: Beinsure). Tanker freight rates are also increasing, with average spot rate to charter super tankers (or Very Large Crude Carriers / VLCCs) crossed USD 300k per day (vs a daily rate of around USD 63k a day in later Dec).

- Trade and logistics disruption:Delays in shipping, port congestion, and rerouting of vessels increase global supply chain costs and delivery times. Air traffic disruption (11k+ in the region) negatively affects hospitality occupancy, cargo capacity & lost retail sales.

- Inflation: Higher energy, fertilizer and transport costs feed into food prices and broader consumer inflation.

- Bottomline: it remains unclear at this stage how long the conflict will last. The path to recovery will depend on how quickly a de-escalation can reopen the Strait of Hormuz & restore the region’s air corridors to original operational capacity.

2. Immediate shocks from the Iran Conflict: Markets

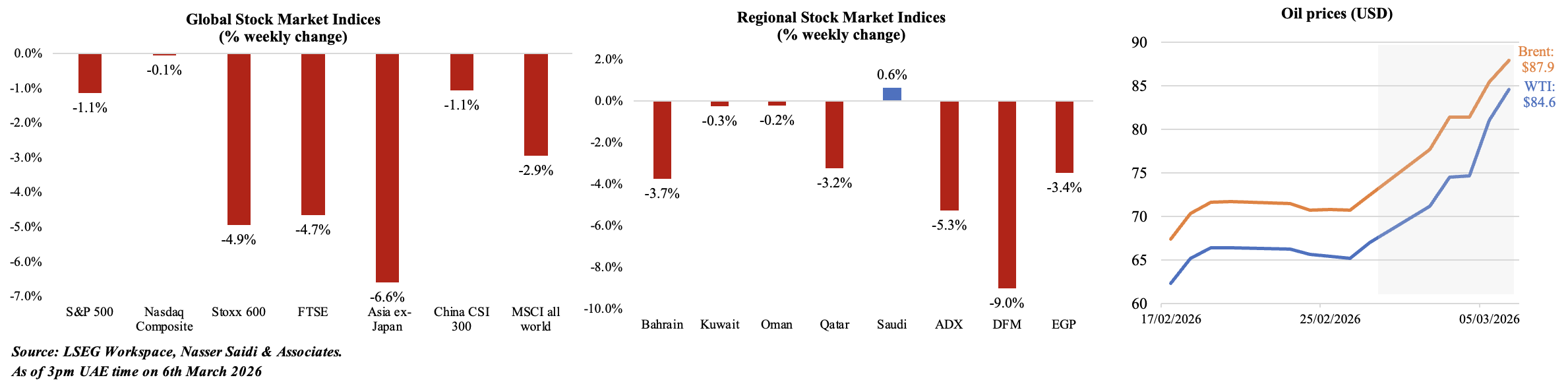

- Crude oil prices surged as fears of supply disruptions intensified, also weighing on fuel-intensive sectors (airlines, transport & manufacturing).

- Shipping, insurance & logistics sectors have also come under pressure due to rising freight costs and risk premiums, while industrial metals (especially aluminium) have been disrupted by shutdowns in the GCC, tightening global supply. In contrast, energy, aerospace & defense sectors have outperformed.

- Equities markets saw declines across several major European, Asian and emerging market indices. In the Middle East, banking and petrochemical sectors faced initial volatility due to “shut-in” production risks, industrial and telecom stocks have remained stable.

- Furthermore, only modest global equity fund outflows were recorded (about USD 1.44bn after weeks of inflows). There is no evidence (yet!) of large-scale capital flight from the GCC & its financial centres.

3. A Macro Overview of Regional & Global Economic Spillovers from the Conflict in the Middle East

GCC Economies

- Short-term oil revenue gains from higher prices.

- But a protracted war could be a threat to oil production, delay hydrocarbon exports & pause revenues.

- Export and logistics disruptions due to tanker delays and higher insurance costs.

- Potential pressure on aviation (UAE & Qatar airport hubs have seen nearly 90% flight cancellations), trade, retail, tourism, transport & logistics and maritime sectors.

Wider MENA (Energy Importers)

- Higher fuel import bills and fiscal pressure.

- Potential energy shortages

- Conflict reduces tourism inflows.

- Rising food and transport costs, intensifying inflation and cost-of-living pressures.

- Increased external vulnerabilities for already fragile economies (e.g. higher borrowing costs, less capital inflows).

Global Economy

- Energy price shocks affect major importers in Europe & Asia.

- Higher global shipping costs and supply chain disruptions.

- Middle East-based carriers account for about 13% of global air cargo capacity

- Rising food costs through fertilizer and transport channels. Middle East accounts for 45% of global supply of fertiliser (urea prices surged 25% since the war began).

- Financial market turmoil

- Risk of renewed global inflation and slower economic growth.

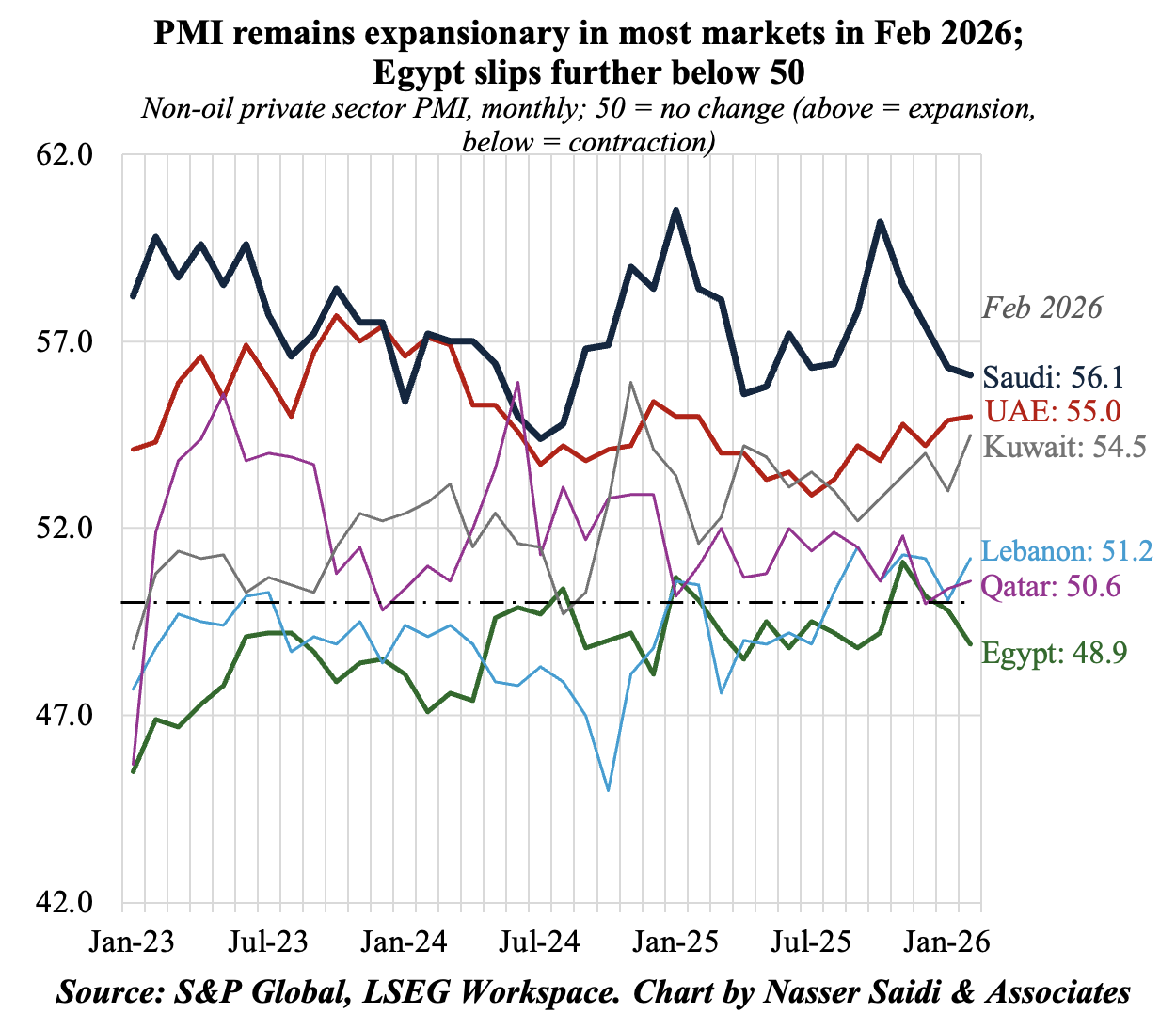

4. Pre-War: Diverging Non-oil Sector Activity in the Middle East

- Pre-war, most GCC countries continued to post robust growth in new orders, supported by population growth, infrastructure investment and upticks in services and construction. UAE’s respondents reported favourable tourism, e-commerce and technology (AI) demand. While Lebanon saw a domestically driven rebound in new orders, Egypt and Qatar saw order books decline.

- Export orders remained weak across the region, reflecting weak external demand conditions. Lebanon reported a 3rd consecutive month of decline while it grew slower than total orders in most GCC countries. Expansion hence is being driven by internal demand & government investment than export-led growth.

- Labour market expansion was strongest in the GCC: Kuwait posted an increase for the 12th month in a row alongside Saudi’s 4-month high and UAE firms hiring the most since Nov. Lebanon clocked in its first employment increase since Nov while Egypt firms cut jobs for the 3rd straight month.

- Input price inflation rose with Kuwait and Qatar at 9- and 14-month highs respectively while Saudi posted a survey-record jump in wages. Egypt and Lebanon’s purchase price inflation rose to the highest since May and Sep 2025, due to higher import costs (for both) and petrol taxes (for LB); UAE input prices rose at the slowest pace since Oct.

- There was only a partial pass-thorough of output prices. Firms in Kuwait and Lebanon passed on part of the higher costs via higher selling prices; in UAE it rose marginally & in Saudi it accelerated to the most since May 2023.

- The conflict in the Middle East stemming from the US-Israel-Iran war will throw a spanner into the works should it continue for weeks. This is likely to affect business and consumer sentiment and create short-term uncertainty.

- For the GCC, the main concern would be the supply side disruptions and logistical delays that could result in higher input prices. Sectors such as tourism, retail and hospitality will be most affected. It is possible that countries with land-based export alternatives or a route bypassing the Strait of Hormuz could benefit during this period.

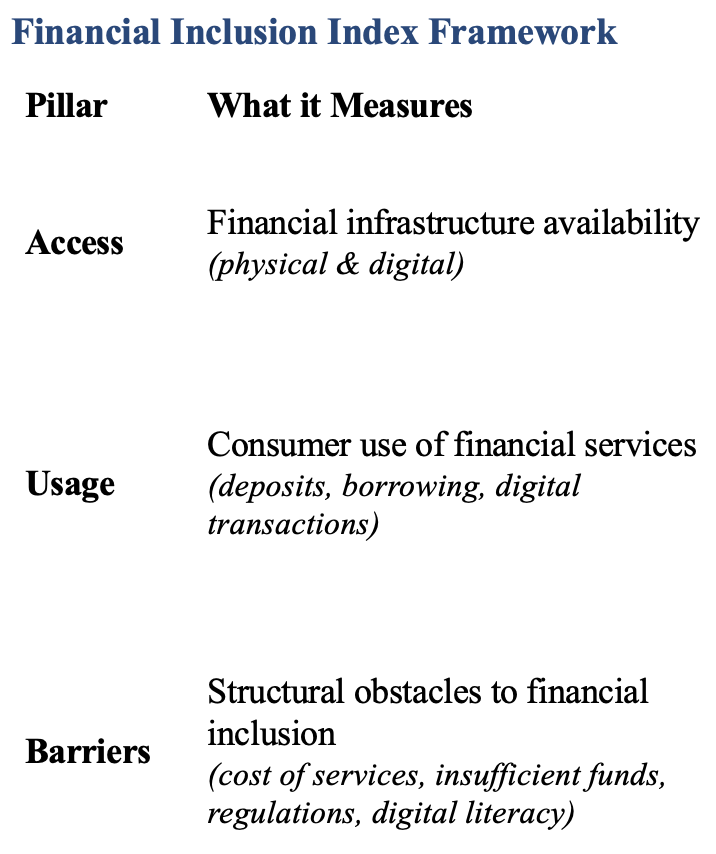

5. Digital Infrastructure is Expanding Financial Inclusion, but adoption remains uneven due to affordability, infrastructure reliability & digital capabilities

Key findings from various indicators within pillars

Access Insights

- Significant global digital divide

- Digital infrastructure > traditional infrastructure (bank branches)

- Arab region lowest account ownership; gender gap: 15ppts

Usage Insights

- Global shift toward digital payments, Covid-accelerated

- Adoption rates are highly uneven

- Infrastructure (electricity networks, internet & mobile connectivity) and human capabilities (education, digital & financial literacy) critical enablers for digital payment adoption

Barriers Insights

- Most significant obstacle in Barriers pillar: “insufficient funds”

- Smartphone internet access costs & regulatory quality important

- Mobile money can serve as a vital tool for promoting FI

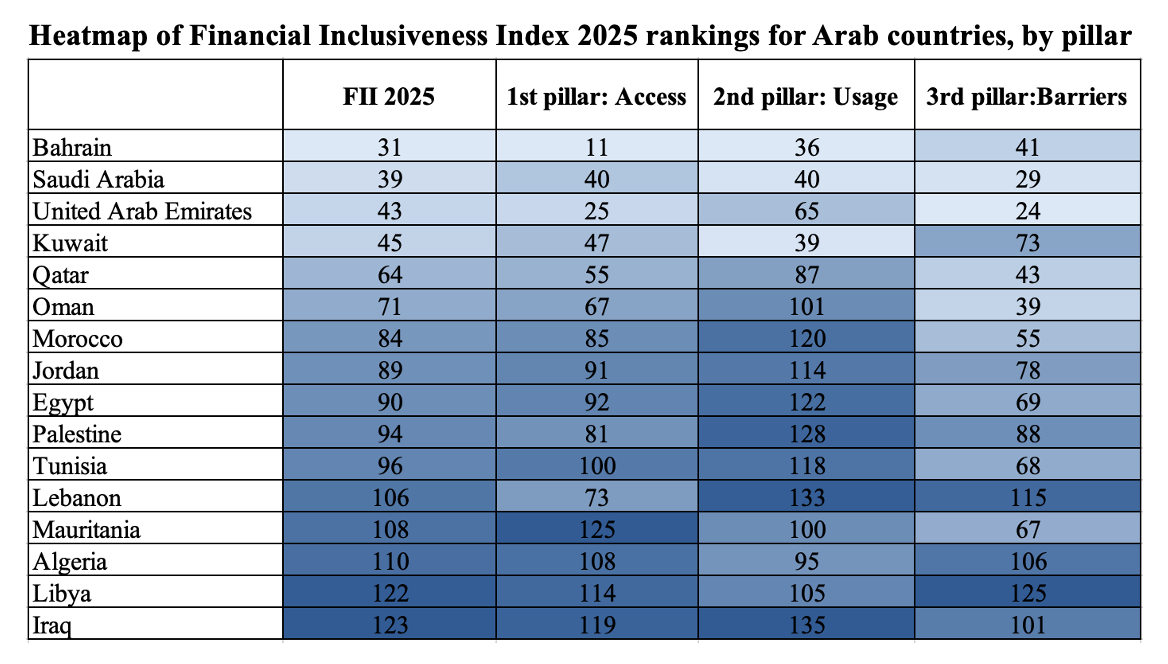

6. Financial Inclusion in the Arab Region is Improving Through Digital Infrastructure, But Remains Constrained By Low Usage & Persistent Barriers

Access: Digital infrastructure rising, but gaps persist

Access: Digital infrastructure rising, but gaps persist

- Shift away from ATMs and bank branches toward mobile & internet banking

- High-income ESCWA countries have strong infrastructure but lower “ease of access” than global peers

- Upper-middle-income countries (Iraq, Libya, Algeria) perform worst in the Access pillar

Usage: Persistent regional lag

- Arab region lags all other regions in the Usage pillar across every income group

- Indicates a gap between service availability and actual usage

- Digital infrastructure strongly correlated with higher financial service usage

- Risk: rapid technology adoption may widen gaps without supporting infrastructure

Barriers: Worsening trends

- Barriers decrease as income rises (-ive correlation with income level)

- High-income countries face lowest traditional barriers

- Most common reason for being unbanked: “insufficient funds”

- Digital divide remains significant within the Arab region

- Unlike other regions, barriers rose in Arab region between 2023–25

7. Key Recommendations to Advance Financial Inclusion

- Expand Access

Scale agent banking and mobile money using the region’s 90%+ mobile coverage.

Reduce gender gaps by removing discriminatory laws and simplifying account opening (e.g., ID-based accounts).

- Drive Usage

Digitise payments (government transfers, wages) to reduce cash reliance and improve transparency.

Remove regulatory barriers restricting mobile money and access for non-nationals.

- Dismantle Barriers

Introduce low-cost, no-minimum-balance accounts.

Develop National Financial Inclusion Strategies & Digital Public Infrastructure.

Offer Shariah-compliant financial products where relevant.

- Harness Fintech

Promote fintech innovation to expand services.

Use alternative credit scoring (mobile/utility data).

Expand national eIDs to provide secure digital identity.

- Regulate & Educate

Build adaptive regulation balancing innovation with consumer protection.

Implement financial & digital literacy programs, especially for women, rural & older populations.

Powered by:

![]()