Download a PDF copy of the weekly economic commentary here.

Markets

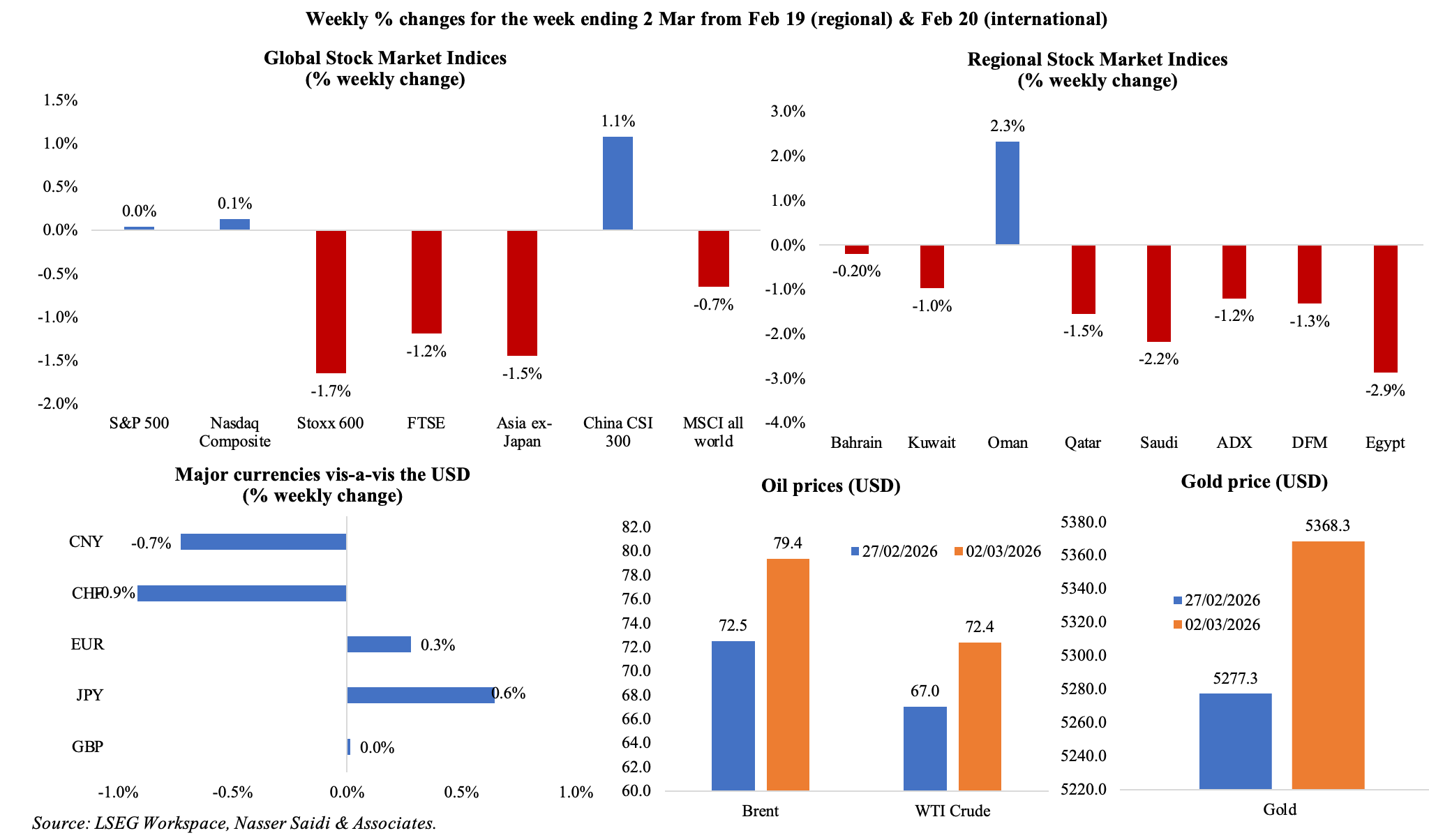

The US-Israel-Iran conflict dominated market performance on Monday, after the attack was launched on Saturday (and spilled over into the wider the Gulf and Middle East). Even though oil prices surged and stocks declined (across continents, as well as across sectors including banking, tech and airlines among others) in initial hours of trading, US markets recovered by afternoon on expectations of a swift resolution. Major markets in Europe, wider Asia and the Middle East ended in the red. Oil price rose to a high USD 82.37 a barrel (highest since Jan 2025) before settling lower (below USD 80). The USD grew stronger and held near a six-week high, as it resumes a “safe haven” role, while US rhetoric about the conflict’s end goals and objectives continue to shift. For now, there is no clear end date for the conflict and uncertainty will drive energy, financial and currency markets. Prior to the onset of war last week, major markets had ended on a positive note other than in the US where AI valuations continued to worry investors; South Korea’s KOSPI crossed the 6000-mark (after doubling in value in 2025). Regional markets were down given the US-Iran negotiations and potential for a conflict.

Global Developments

US/Americas:

- The US and Israel initiated attacks on Iran over the weekend: the conflict has since killed Iran’s supreme leader, spilled over into a wider regional conflict and will affect the oil markets (already shipments via the Strait of Hormuz have been affected). While various GCC ports and airports were hit during the attacks, more than 3k flights from the region were delayed / cancelled during this period, disrupting international air traffic given the global hubs in Qatar and the UAE. The longer it continues, the increased likelihood of higher oil prices (given the current disruption on the Strait of Hormuz) and once again affecting inflation across the globe. Crude oil was already near a 7-month high on expectations of a US-Iran conflict.

- US factory orders fell 0.7% mom in Dec (Nov: 2.7%), as commercial aircraft bookings dipped (-24.8% vs Nov’s 98.2% surge). Non-defence capital goods excluding aircraft inched up by 0.8% (from the initial estimate of 0.6%).

- Producer price index in the US accelerated by 0.5% mom and 2.9% yoy in Jan (Dec: 0.4% mom and 3.0% yoy). Services prices ticked up 0.8% mom, thanks to a 2.5% jump in trade services while core PPI jumped to 3.6% yoy (Dec: 3.3%).

- S&P Case Shiller home price index rose 1.4% yoy in Dec, following a similar gain in Nov. According to S&P, national home prices grew just 1.3% for the year: the weakest full-year gain since 2011.

- Chicago Fed national activity index moved into positive 0.18 in Jan (Dec: -0.21), the highest reading since Feb 2025, with production-related indicators driving the increase.

- Richmond Fed manufacturing index slipped to -10 in Feb (Jan: -6) – this is the 12th consecutive month of negative readings, with both shipments and new orders declining even further and prices remaining elevated. Dallas Fed manufacturing business index climbed to 0.2 in Feb (Jan: -1.2): company outlook and employment held steady (at 3.1 and 7.5 respectively) while uncertainty rose to 6.5 (below average).

- Kansas Fed manufacturing activity rebounded in Feb, rising to 10 (Jan: -2), thanks to increase in output growth, higher future activity expectations and improvements in employment outlooks. Separately, Chicago PMI rose to 57.7 in Feb (Jan: 54.0), the most since May 2022.

- Initial jobless claims increased by 4k to 212k in the week ended Feb 21, with the 4-week average inching up by 750 to 220.25k. Continuing jobless claims fell by 31k to 1.833mn in the week ended Feb 14.

Europe:

- Economic Sentiment Index in the eurozone slipped to 98.3 in Feb (Jan: 99.3). Business climate improved slightly to -0.36 (Jan: -0.38). Declines were recorded across both industrial confidence (-7.1 from -6.8) and services sentiment (5 from 6.8).

- The harmonised index of consumer prices in Germany decreased to 2.0% in Feb (Jan: 2.1%), according to preliminary estimates.

- The GfK consumer confidence index for Germany fell further to -24.7 in Mar (Feb: -24.2). Economic expectations weakened (4.3 from Feb’s 6.6) and willingness to buy sharply dropped (-9.3 from -4.0). Rising prices and economic-political uncertainty has raised respondents’ willingness to save by another point to 18.9 – the highest reading since 2008.

- German Ifo business climate index increased one point to 88.6 in Feb, indicating “the first signs of recovery”. The current assessment and expectations rose to 86.7 and 90.5 respectively (from 85.7 and 89.6). This is in line with the manufacturing PMI reading released last week that showed the first expansion in over 3.5 years.

- Unemployment rate in Germany stood unchanged at 6.3% in Feb though the number of unemployed persons ticked up by 1k to 2.977mn.

- UK’s GfK consumer confidence dropped to -19 in Feb (Jan: -16), reversing gains from the previous two months, partly due to the jump in unemployment in Q4; perceptions of people’s own finances dropped four points both for the past year and year-ahead views. Despite the low inflation readings, the index of willingness to make major purchases dropped four points to -14. This contrasts with recent signs of improvement in PMI for Feb (fastest growth since Apr 2024), a record budget surplus in Jan and a sharp uptick in Jan retail sales.

Asia Pacific:

- The People’s Bank of China (PBoC) held interest rates unchanged at 3% at the meeting last week. Later in the week, the PBoC removed the risk reserve requirements for forex forward contracts, in a bid to support the yuan’s value, encourage dollar buying, and by making the CNY less expensive to hold. The CNY had hit a near 3-year high versus the greenback on Thursday. The apex bank also stated that it would remove the reserve requirement of 20% on forex forward contracts from Mar 2.

- Inflation in Tokyo ticked up to 1.6% in Feb (Jan: 1.5%). Excluding fresh food and energy, prices inched up to 2.5% (Jan: 2.4%). Excluding just fresh food (core CPI), prices slipped to 1.8% (Jan: 2.0%), falling below 2% for the first time since Oct 2024. Weakness in inflation could potentially allow the BoJ not to increase rates – a stance preferred by the current PM.

- Industrial production in Japan grew by 2.2% mom and 2.3% yoy in Jan (Dec: -0.1% mom and 2.6% yoy). The monthly gain was the first in three months, supported by a double-digit increase in car output while the wider motor vehicles production grew by 9.1% (Dec: 1.4%).

- Japan’s leading economic index increased to 111 in Dec (prelim: 110.2, Nov: 109.9), the highest reading since May 2024, supported by improving labour market conditions even though consumer sentiment weakened (after touching a 19-month high in Nov) Meanwhile, the coincident index moved to a 4-month low of 114.3 (prelim: 114.5, Nov: 114.9) on ongoing trade and tariff uncertainty affecting autos and related sectors.

- Retail trade in Japan rebounded in Jan, up 1.8% yoy (Dec: -0.9%), posting the fastest increase since Jun 2025 thanks to the stimulus measures including consumption vouchers to encourage spending. The monthly gain of 4.1% (Dec: -2.0%), was the fastest uptick since Sep 2019. Large retailer sales grew by 3%, quicker than the 2% gain in Dec.

- GDP in India grew by 7.8% yoy in Oct-Dec or Q3 of the fiscal year 2025-26 (Jul-Sep: 8.2%), as per the new series of national accounts with a base year of 2022-23. Growth was supported by strong services sector performance (in line with the PMI readings), double-digit growth in manufacturing, rationalisation of indirect taxes as well as festival demand. For full year 2025-25, growth was raised to 7.6% (from 7.4% before) and from 7.1% in the 2024-25 fiscal year.

- India’s fiscal deficit widened to INR 9.8trn in Jan (Dec: INR 8.6trn), accounting for 63% of the estimate for the financial year. Net tax receipts increased to INR 20.94trn (Apr 2024-Jan 2025: INR 19trn) while capex grew to INR 8.4trn (from INR 7.6trn).

- South Korea’s central bank left interest rates unchanged at 2.5% last week, in line with expectations. The apex bank also signalled that it was likely to hold for the next six months, given its chips exports as well as the steady inflation print. GDP growth forecast was revised up to 2.0% (from 1.8% previously).

- Industrial production in Singapore accelerated in Jan, up by 5.3% mom and 16.6% yoy (Dec: -0.3% mom and 10.9% yoy), supported by the surge in electronics output (44% yoy vs Dec’s 19.6%) as semiconductors surged (52% from 20.5%). This was accompanied by a sharp decline in the volatile biomedicals output (-33.1% from -10.9%). Excluding the biomedical manufacturing, manufacturing grew 24.1% yoy in Jan.

Bottom line: As the US-Israel attacks on Iran began, so did the retaliation attacks by the latter on Israel and its neighbouring nations including the GCC countries that are home to US military bases. Even Oman, that was mediating the nuclear deal talks, was not spared. The escalation of conflict has led to a severe maritime bottleneck, with over 150 vessels anchored as insurance risks and security threats stall energy shipments and disrupt supply chains; the Strait of Hormuz is a chokepoint through which approximately 20% of global oil and LNG supply flows, with some 80% flowing to Asian countries. Marine insurers Marsh, Skuld and Gard announced the cancellation of war risk covers for ships, taking effect from March 5th while others are raising maritime insurance premiums (up by 25% to 50% in the first 48 hours of the conflict). Brent crude is already trading at over USD 80 per barrel and could rise up to USD 100 per barrel if the situation is not resolved within the coming days and energy infrastructure damaged. Although OPEC+ has pledged to increase production, it remains to be seen how this spare capacity can be accessed – especially if the blockade at Hormuz continues.

This instability has also bled into the aviation sector, with over 3,000 flights cancelled across Middle Eastern hubs, threatening tourism and connector-hub revenues integral to the GCC. Air traffic disruption negatively affects hospitality occupancy, cargo capacity and lost retail sales. For economies such as the UAE, Qatar and Saudi Arabia, such prolonged interruptions could dent tourism revenues from lower tourist and business traffic flows.

In addition, the region is bound to further increase spending on defence and the repair of targeted civilian infrastructure, such as ports and power plants, thereby leading to wider-than-budgeted fiscal deficits for 2026. This would divert resources from development and social spending.

Furthermore, the UAE and Kuwait have temporarily closed their domestic capital markets to prevent panic-selling citing “exceptional circumstances”.

It remains unclear at this stage how long the conflict will last. The neutrality of the GCC is being tested and the path to recovery will depend on how quickly a de-escalation can reopen the Strait of Hormuz and restore the region’s air corridors to its original operational capacity. As countries attempt a re-evaluation of energy transport security, they must prioritize the development of overland pipelines, land and rail networks to offer a viable alternative to the increasingly volatile Strait of Hormuz and ensure security of energy supplies.

Lastly, thanks to lessons from the Covid closures, the countries seem to have sufficient stocks of perishable goods and pharmaceuticals; Kuwait has further announced a ban on food exports due to the regional situation.

Regional Developments

- OPEC+ announced plans to increase oil output by 206k barrels per day in Apr; the group has not raised production since Dec. However, the conflict in Iran and spillovers into the rest of the Middle East begs the question if that increase would be sufficient to offset the disruption (were it to continue for longer).

- Fitch downgraded Bahrain to “B” from “B+” citing rising debt, low foreign exchange reserves and widening deficits making the country increasingly vulnerable to external shocks. Bahrain’s fiscal vulnerability reflects structurally higher break-even oil prices and limited buffers relative to GCC peers while elevated interest costs add to debt sustainability concerns.

- Egypt achieved a major milestone with the IMF completing its 5th and 6th reviews, unlocking USD 2.3bn in critical funding as part of its Extended Fund Facility. This fiscal anchor is bolstered by record-breaking inflows, including an all-time high of USD 41.5bn in remittances (+45% yoy) and record food exports in 2025 (+12% yoy to nearly USD 7bn). The Central Bank of Egypt now expects GDP growth to accelerate to 5.1% and 5.5% in the fiscal years 2025-26 and 2026-27 respectively, supported by a 3-year economic action plan and a rebound in Suez Canal activity. Separately, the finance ministry disclosed that payment for interest on Egypt’s debt soared by around 40% to around EGP 1.48trn in the first seven months of the fiscal year 2025-26.

- Egypt’s decision to operate ports and customs year-round – export procedures 24 hours a day and import inspections till 6pm – aims to reduce clearance times and boost trade efficiency. In addition, this is expected to lower handling and storage costs, reduce financing burdens on businesses and enhance export competitiveness.

- Kuwait’s economic activity has rebounded (+1.7% yoy in Q2 2025) and is making significant strides in its “the transition from an oil dependent welfare state towards a dynamic and diversified economy”, according to the IMF’s Article IV consultation. The IMF urged Kuwait to accelerate fiscal reforms – such as implementing tax reforms and subsidy rationalisation – to reduce its long-term dependence on hydrocarbons: while large sovereign assets provide exceptional buffers, political gridlock has historically delayed structural reform. More: https://www.imf.org/en/news/articles/2026/02/23/pr-26061-kuwait-imf-executive-board-concludes-2025-article-iv-consultation

- The IMF issued a stark call for Lebanon to modernise its tax regime – “more modern and effective income tax law” – to improve revenue collection and transparency. This remains a prerequisite for any broader recovery package; reform sequencing and political consensus remain decisive variables for recovery. The IMF also called for the parliament to discuss and approve amendments to the Bank Resolution Law “in the coming months”.

- Oman’s annual inflation eased to 1.4% in Jan 2026 (Dec: 1.6%), the lowest since Sep 2025, driven by a deceleration in food and beverage prices (0.9% from 1.1% in Dec) while transport prices declined 0.3% (Dec: 2.8%). Simultaneously,FDI stocks surged 16.2% yoy to OMR 30.948bn by end-Q3 2025, reflecting investor confidence in Oman’s regulatory reforms and its “Oman Vision 2040” roadmap. Oil and gas exploration (OMR 24.9bn), manufacturing (OMR 2.715bn) and financial intermediation (OMR 1.483bn) sectors accounted for the largest shares of foreign investment.

- Oman ports reported a robust 21.6% growth in container volumes to 5,178,622 TEUs in 2025, underscoring the success of the Duqm and Salalah port expansions. This logistics momentum is matched by a growing service economy, with over 137,000 cruise tourists visiting in 2025, signalling Oman’s rising status as a boutique destination for high-value international tourism (especially port cities such as Salalah, Khasab and Muscat).

- Qatar’s FDI increased by 7% yoy to QAR 157bn at end-Q3 2025, with the mining and quarrying sector (including LNG) drawing the largest share of capital (44%), followed by financial and insurance (32%) and manufacturing (15%).

- Qatar ranks sixth globally in the Islamic Fintech sector, according to the Global Islamic Fintech Report 2025-2026, thanks to a sophisticated regulatory framework and a surge in digital banking adoption. The size of Qatar’s Islamic fintech market stood at USD 3.1bn in 2024-2025 and projects a compound annual growth rate of 9% to USD 4.8bn by 2029.

- The formal launch of negotiations for a Free Trade Agreement between the GCC and India marks a strategic move toward a South-South economic corridor.This agreement aims to build on the success of the UAE-India CEPA, targeting the removal of barriers for energy, food security, and technology services. Focus should also be on harmonizing standards for digital trade and sustainable finance to ensure the agreement serves as a blueprint for future transcontinental partnerships.

Saudi Arabia Focus

- Saudi Arabia recorded a budget deficit of SAR 276.6bn for the full year 2025, its largest since the pandemic era and more than double the shortfall recorded in 2024. Non-oil revenues reached SAR 505.3bn in 2025, accounting for a historic 45.45% of total government income (supported by a 2.2% jump in tax revenues to SAR 388.9bn). Oil revenues comprised 54.55% of total receipts despite falling about 20% yoy, highlighting the challenge and gradual progress of revenue diversification.

- Total reserve assets in Saudi Arabia surged to SAR 1.78trn in Jan 2026, the highest since Apr 2020. Net foreign assets grew 3.6% mom and 9.9% yoy to SAR 1.696trn while M3 growth accelerated (8.5% yoy) alongside a rise in deposits (8.8%) and bank credit (10.0%). GRE deposits continue to be a sticky funding source. Private sector credit growth on the other hand remains resilient while the mortgage boom has normalised.

- Tadawul’s first IPO of the year saw the retail tranche of Saleh Abdulaziz Al Rashed & Sons being 16.1 times oversubscribed, with orders touching SAR 122mn. Furthermore, four additional major companies are reportedly exploring IPO plans for H1 2026. The consistent high oversubscription levels demonstrate deep domestic liquidity and robust investor confidence. Companies raised USD 4.2bn in Saudi Arabia in 2025, though only two of the 10 largest IPOs are currently trading higher than the offer price, according to Bloomberg. More: https://www.bloomberg.com/news/articles/2026-02-23/saudi-firms-advance-ipo-plans-in-boost-for-flagging-local-bourse

- Saudi Arabia’s non-oil exports (including re-exports) surged by 18.6% in Q4 2025, though when excluding re-exports non-oil exports dipped 1.5%. The overall growth is supported largely by the machinery, electrical equipment and parts (78.5% yoy in Q4) – benefiting from enhanced regional trade integration and industrial zones. China held its position as Saudi Arabia’s largest trading partner in both exports and imports.

- PIF-owned Lucid Motors saw its deliveries surge 55% yoy to close to 16k units in 2025. When fully operational, the company is targeting the production of 155k electric cars per year annually at its plant in King Abdullah Economic City; it currently assembles 5k vehicles.

- The new Qiddiya Bullet Train, linking the entertainment and tourism hub to King Salman International Airport and the King Abdullah Financial District, aims to drastically reduce travel times to around 30 minutes from nearly two hours currently. This reduction will result in a multiplier effect on the domestic tourism and entertainment sectors in addition to raising land values and improving labour mobility.

UAE Focus

- UAE’s real GDP expanded by 5.1% yoy to approximately AED 1.4trn in Jan-Sep 2025, thanks to a 6.1% surge in non-oil sector (to over AED 1trn). Growth is now more broad-based, with thelargest growth rate clocked in by financial & insurance (+9%), followed closely by construction (8.7%) and real estate (7.9%). The financial sector has benefitted from the performance of its financial centres DIFC and ADGM as well as the seamless integration of fintech. Manufacturing also showed resilience, growing by 6.9% and contributing nearly 14% to the non-oil economy, reflecting the success of the “Operation 300bn” industrial strategy. The strong non-oil performance and supportive policy landscape (in addition to the uptick in oil production) will enable growth to remain robust at around 5.5% for full-year 2026.

- Dubai reported a 6% yoy increase in tenancy contract volume to 1.38mn in 2025 alongside a 17% surge in its total value to AED 126.4bn. New tenancy contracts rose by10% (to 513k contracts) while renewals increased by 3% (to over 514k contracts), indicating a healthy balance between new population inflows and long-term resident stability. Policymakers should focus on the 25% increase in projects under construction (to 937) to ensure supply remains elastic to demand and prevent overheating. Sustained rental increases can tighten cost-of-living conditions and feed into wage expectations.

- The Abu Dhabi real estate market saw more than100 nationalities investing AED 8.2bn in 2025, up 13% yoy. Russians, Chinese, Britons, Americans, French and Kazakhs were designated the top buyers though no further breakdowns were provided. This degree of diversification mitigates concentration risk and underscores Abu Dhabi’s growing profile, underscoring recent policy reforms such as long-term residency and ownership liberalisation.

- According to the Dubai International Chamber, about 46.9% of the new MNCs that registered at the Dubai Chamber last year originated from Asia, followed by the Middle East/CIS region at 20.3%. Asia also dominated the SME influx, representing 49.8% of the 309 new SMEs established through the chamber. Amidst global trade uncertainty, the South-South trade corridor is likely to expand further. In this backdrop, expect a surge in trade-finance demand and logistics requirements as these Asian firms use Dubai as a connecting hub to build operations into Africa and Europe. Enhancing bilateral agreements, digital trade facilitation and visa mobility will sustain and boost such inflows from Asia.

- The UAE raised AED 5.88bn from its first7-year Islamic Treasury Sukuk auction, that was oversubscribed 5.3 times. Recent sovereign and quasi-sovereign sukuk issuances have attracted strong demand, reinforcing investor confidence in UAE’s credit profile, UAE’s status as a global Islamic finance hub and sustained global appetite for high-grade GCC credit. Improving the depth of the local-currency Sukuk market can lead to the creation of a robust domestic yield curve, which can become a funding source for future developmental projects.

- Abu Dhabi’s first bond sale of 2026 saw orders exceed USD 11bn, reflecting massive oversubscription for its 5 and 10-year tranches.

- Dubai awardedAED 2.5bn in contracts for stormwater drainage, benefiting 30 key areas as part of a broader AED 30bn stormwater drainage upgrade (a climate resilience initiative following the floods in Apr 2024). While this will ensure long-term urban sustainability, such infrastructure projects also lead to increased employment opportunities, protect property values, reduce insurance risk and sustain investor confidence.

- UAE and South Korea signed a landmark USD 35bn defence cooperation MOU; the defence pact can open high-margin opportunities in R&D and aerospace. From a macro perspective, such agreements contribute to technology transfer, advanced manufacturing capacity as well as domestic industrial development – all supporting knowledge-intensive employment growth.

- A joint venture between the Egyptian General Petroleum Corporation (EGPC) and Dubai’s Dragon Oil – Gulf of Suez Petroleum Company (Gupco) – is investing USD 516mn in 2026–27 to boost crude production by nearly 15%, targeting 75,000 barrels per day. The company focuses on offshore production in the Gulf of Suez; for the UAE, such outbound investment on hydrocarbons diversifies upstream exposure while reinforcing geopolitical partnerships (such as with Egypt).

Media Review:

Weaponisation of the dollar marks the end of an era: Dr. Nasser Saidi’s op-ed for AGBI

https://www.agbi.com/opinion/finance/2026/02/nasser-saidi-the-dollars-weaponisation-marks-the-end-of-an-era/

Interview with Dr. Nasser Saidi on Al Arabiya Business – the weaponisation of the dollar

https://nassersaidi.com/2026/02/21/interview-with-al-arabiya-on-the-weaponisation-of-the-dollar-19-feb-2026/ or Direct link to Al Arabiya Business

Stock-Bond Diversification Offers Less Protection from Market Selloffs: IMF

https://www.imf.org/en/blogs/articles/2026/02/18/stock-bond-diversification-offers-less-protection-from-market-selloffs

India is in the midst of a data-centre investment boom

https://www.economist.com/business/2026/02/19/india-is-in-the-midst-of-a-data-centre-investment-boom

Behind Trump’s truce with China: FT

https://www.ft.com/content/12a6a1d0-383f-4b24-8d16-7af763ba56f2

Powered by:

![]()