UAE GDP. Saudi monetary stats, fiscal deficit. Middle East 2025 airlines performance & tourism.

Download a PDF copy of this week’s insight piece here.

GCC Growth Driven by Boom in Tourism & Aviation, Weekly Insights 27 Feb 2026

1. UAE GDP expanded by 5.1% yoy in Jan-Sep 2025, with non-oil sector growing at a faster 6.1% pace

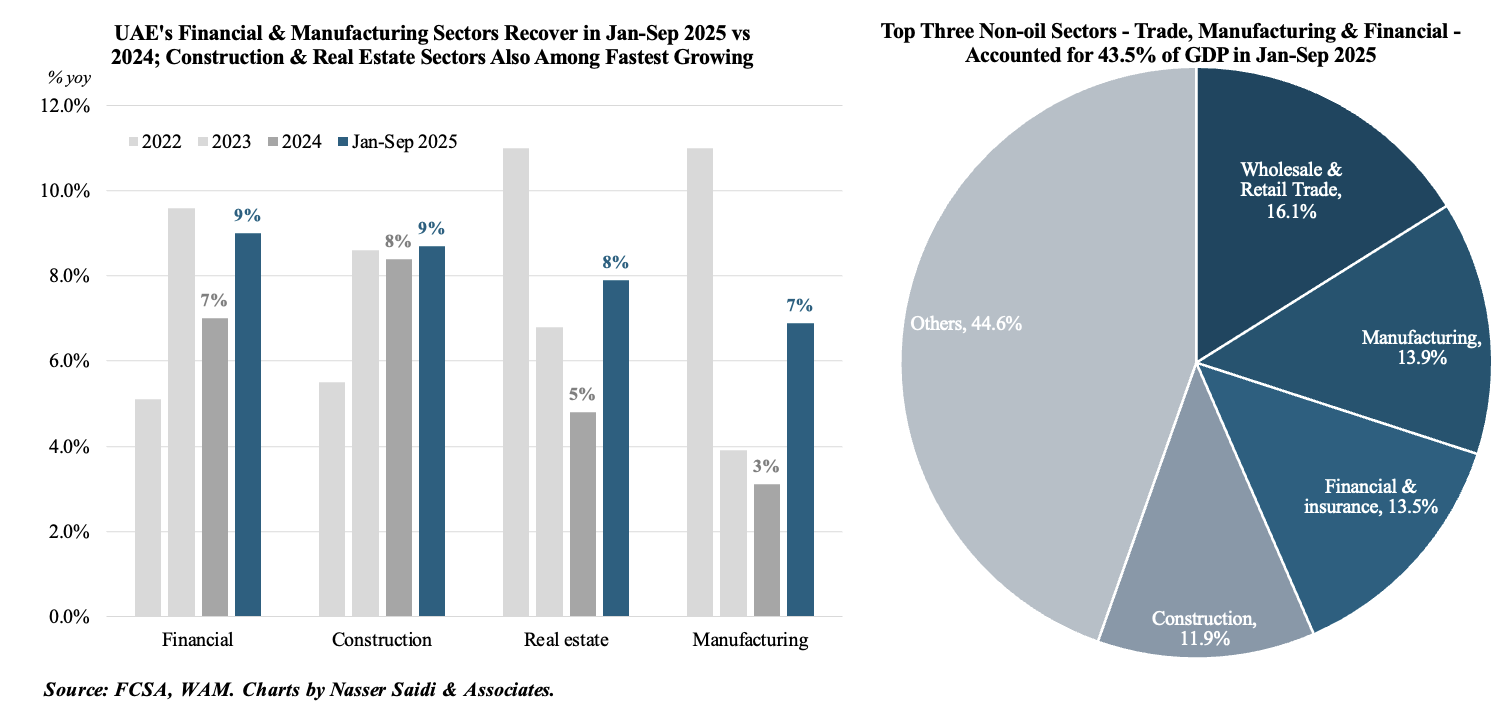

- UAE’s real GDP expanded by 5.1% yoy to approximately AED 1.4trn in Jan-Sep 2025, thanks to a 6.1% surge in non-oil sector (to over AED 1trn).

- Growth is now more broad-based, with the largest growth rate clocked in by financial & insurance (+9%), followed closely by construction (8.7%) and real estate (7.9%). The financial sector has benefitted from the performance of its financial centres DIFC and ADGM as well as the seamless integration of fintech. Manufacturing also showed resilience, growing by 6.9% and contributing nearly 14% to the non-oil economy, reflecting the success of the “Operation 300bn” industrial strategy.

- Services-led diversification is also reaping benefits: Dubai welcomed 13.95mn international visitors in Jan-Sep 2025 (5.0% yoy) while combined passenger traffic during the period at UAE’s major airports (Abu Dhabi Airports, Dubai International and Sharjah) crossed 108.6mn. These correlate with the 16.1% contribution of the wholesale & retail sector to total non-oil GDP.

- The strong non-oil performance and supportive policy landscape (in addition to the uptick in oil production) will enable growth to remain robust at around 5.5% for full-year 2025. With the “We the UAE 2031” vision targeting AED 3trn GDP, the focus is shifting toward digital infrastructure as well as AI-led initiatives – to maintain this growth trajectory.

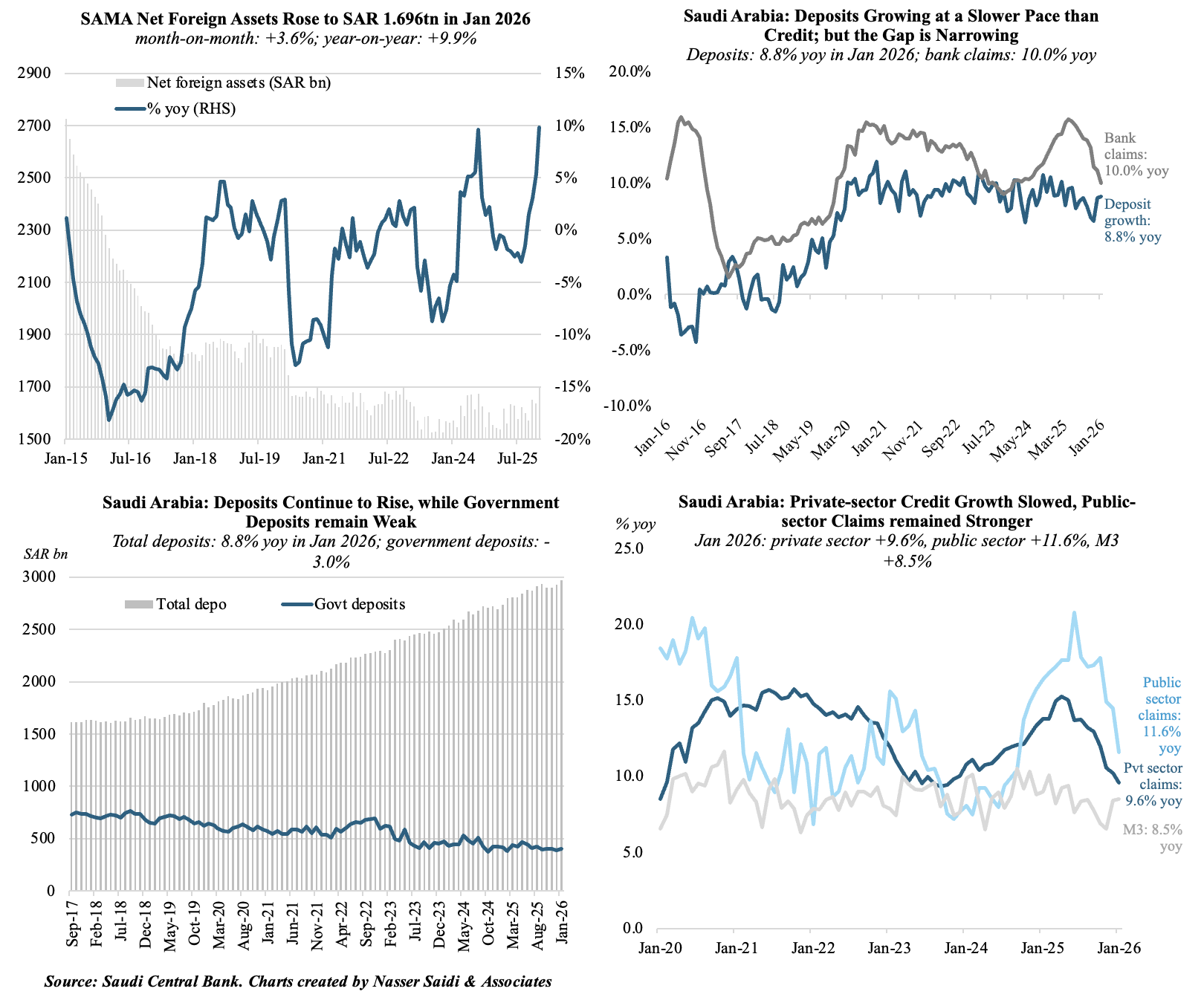

2. Total reserve assets in Saudi surged to SAR 1.78trn in Jan 2026, the most since Apr 2020; NFA grew to SAR 1.696trn. M3 accelerated, driven by a rise in demand deposits & bank credit; GRE deposits will continue to be a sticky funding source. Private sector credit growth is resilient; mortgage boom has normalised.

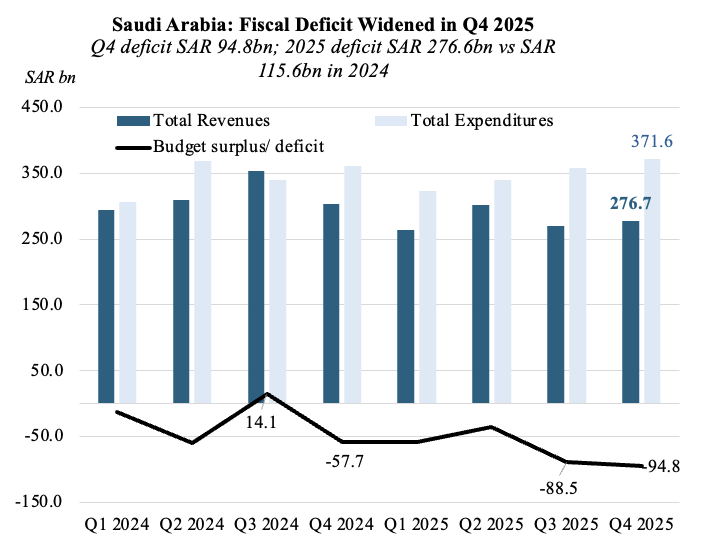

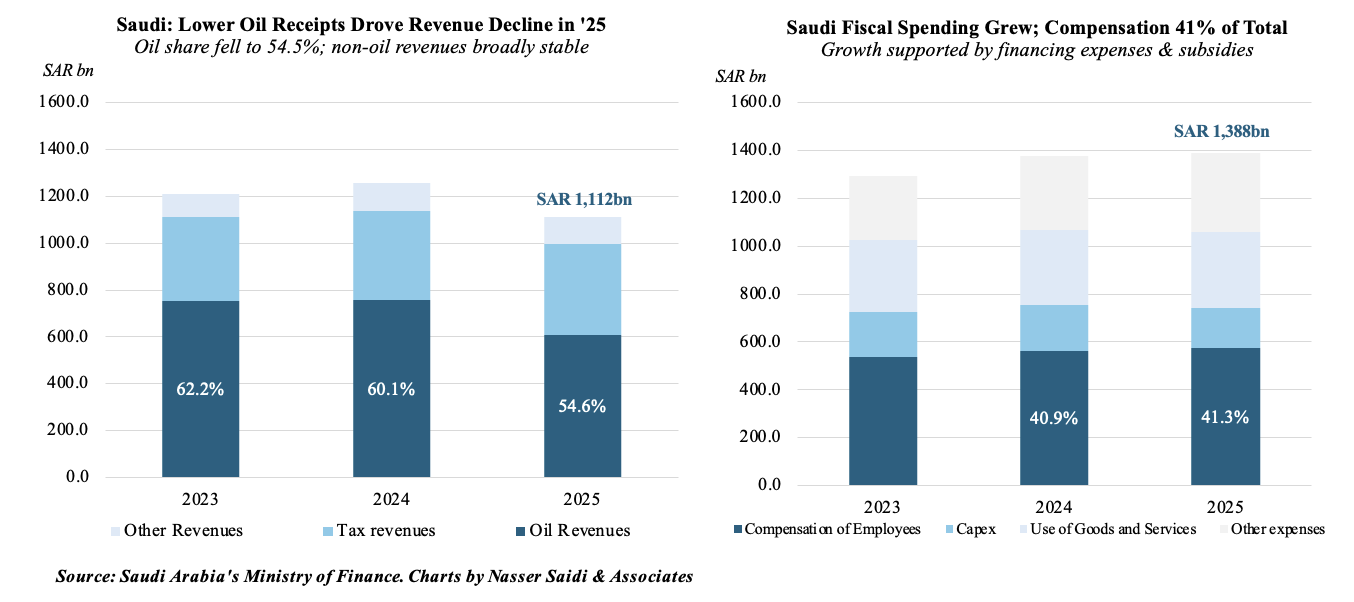

3. Saudi Arabia deficit in 2025 more than doubles to SAR 276.6bn, as spending inched up by 1.0% amid a 20% plunge in oil revenues

- Saudi Arabia recorded a budget deficit of SAR 276.6bn for the full year 2025, more than double the shortfall in 2024. This exceeded budget forecasts and was driven by a 1% increase in total expenditure to SAR 1.39trn.

- Non-oil revenues reached SAR 505.3bn in 2025, accounting for a historic 45.45% of total government income (supported by a 2.2% jump in tax revenues to SAR 388.9bn). Oil revenues comprised 54.55% of total receipts despite falling about 20% yoy, highlighting the challenge and gradual progress of revenue diversification.

- Human capital and social stability received the lion’s share of spending in 2025 (35.4% of total). Notably, capex surged 18% in Q4 alone, as infrastructure works accelerated ahead of upcoming major events such as Expo 2030.

-

Will Saudi meet its 2026 budget deficit goals? Unlikely. Why? One, in the current uncertain & volatile geopolitical & economic environment, any drop in oil prices towards the USD 60 mark will push deficit higher, leading to further sovereign debt issuance or a drawdown from reserves. Two, spending is unlikely to face meaningful cuts given fixed deadlines of events such as Expo 2030 and the 2034 World Cup.

-

What needs to be done? Improve efficiency. This means optimising tax collection (improve compliance, better enforcement); rationalising untargeted energy subsidies; tighter prioritisation of capital projects; implementing performance-based budgeting for government entities; and reduce the SAR 574bn public wage bill (the largest recurrent expense).

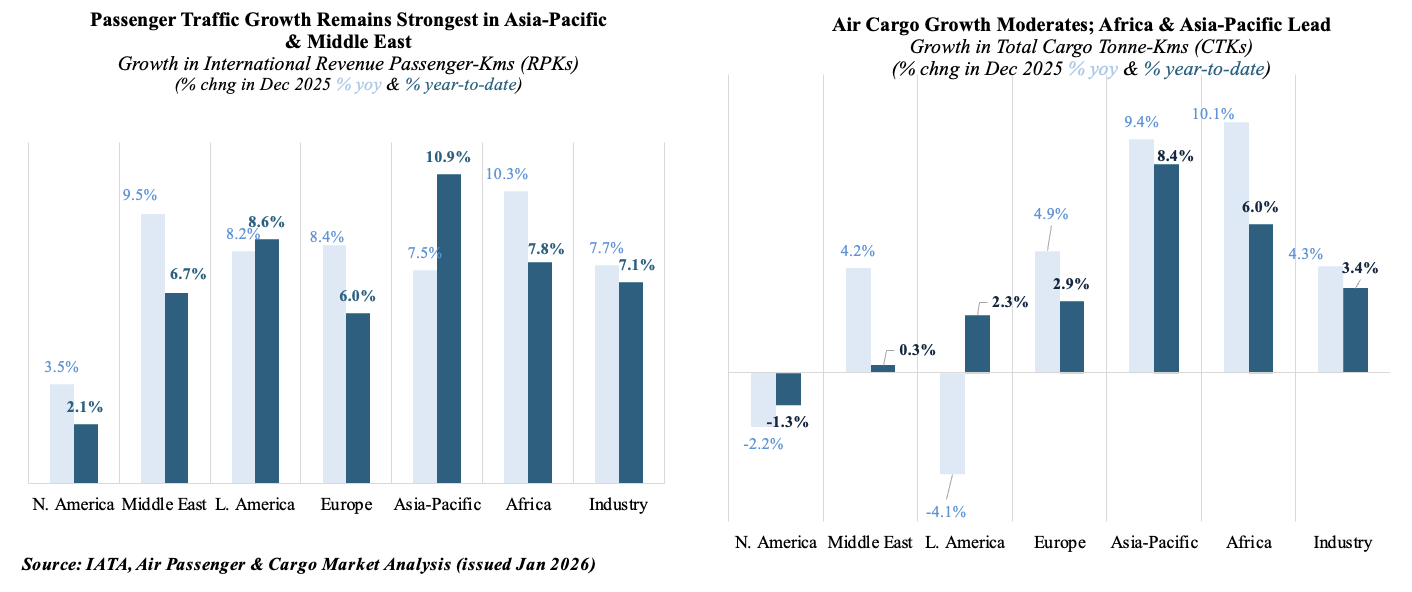

4. Middle East airlines strong 2025 performance; to continue into 2026

- Full-year 2025 global air passenger demand (RPK) climbed 5.3% yoy, with international travel (7.1%) outpacing domestic traffic growth (2.4%). Middle Eastern carriers reported a 6.7% year-to-date (ytd) rise in Dec, while Asia-Pacific saw higher volume growth (10.9%).

- Global air cargo demand (measured in cargo tonne-kilometres) grew by 3.4% ytd in 2025 (reaching record volumes in late Q4), defying pessimistic trade outlooks. Asia-Pacific and African carriers led cargo growth (8.4% and 6.0% respectively) whereas Middle East carriers posted a modest 0.3% rise in cargo demand (albeit with capacity increases and stronger performances later in 2025).

- 2025 was a year of regional contrast. North America saw a contraction in domestic passengers (-0.6% ytd in Dec) and the only regional decline in air cargo (-1.3%), largely due to uncertain US tariff policies. On the other hand, Africa emerged on top reporting a 9.4% spike in overall passenger demand. The Middle East-Asia cargo corridor expanded by 9.5% yoy in Dec, reflecting the South-South pivot (the strongest after Europe-Asia corridor’s 12.2% growth).

- The Middle East is set to continue its robust performance in 2026, with a projected 6.1% passenger growth outpacing capacity expansion (5.4%). It is also expected to be the most profitable region, with a projected net margin of 9.3% in 2026, more than double the global average of 3.9% (anchored by the performance of GCC hubs – UAE, Saudi Arabia & Qatar). The region’s massive airport expansions (e.g. King Salman International, DXB/DWC) can absorb the growth.

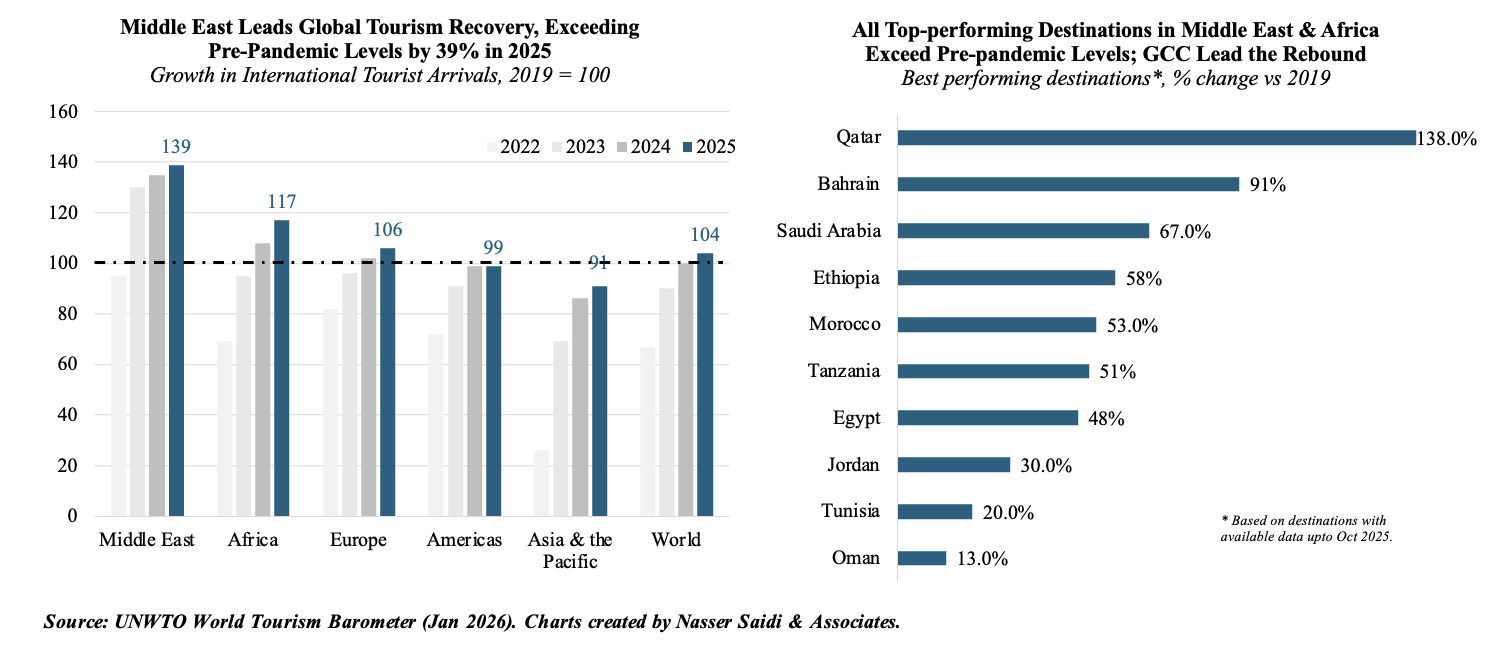

5. Middle East international tourist arrivals surged 39% in 2025 vs 2019: most destinations cross pre-pandemic levels

- According to UN WTO, international tourist arrivals grew to a new record 1.52bn in 2025, fully recovering to pre-pandemic levels and marking a 4% increase over the 2019 baseline. While Europe remained the most visited region (793mn), its growth stood at 6% above 2019 levels, contrasting with the much higher expansions clocked in emerging markets.

- The Asia-Pacific region continued its steady climb, reaching 91% of its pre-pandemic volume in 2025. Conversely, Africa saw a robust recovery, with arrivals 17% higher than in 2019, driven by strong demand for North African destinations like Morocco and Tunisia.

- Middle East was the clear global leader, with international arrivals surging 39% above 2019 levels (close to 100mn visitors). This exceptional performance was anchored by the GCC, which have successfully utilised mega-events and simplified visa regimes to transform from being just transit hubs. Tourism’s contribution to GDP in the Middle East outpaced global averages, reflecting high-spending traveller patterns and success of diversification strategies. Kuwait, Saudi Arabia and Morocco were also among the global best-performing destinations by earnings in Jan-Nov 2025.

- Looking ahead, the Middle East is projected to maintain its lead as regional connectivity improves (as the GCC Unified Tourist Visa launches) and new giga-projects (such as the Red Sea Project) begin to scale their commercial operations. This will support spillovers into hospitality, retail, cultural and creative sectors.

Powered by:

![]()