Markets

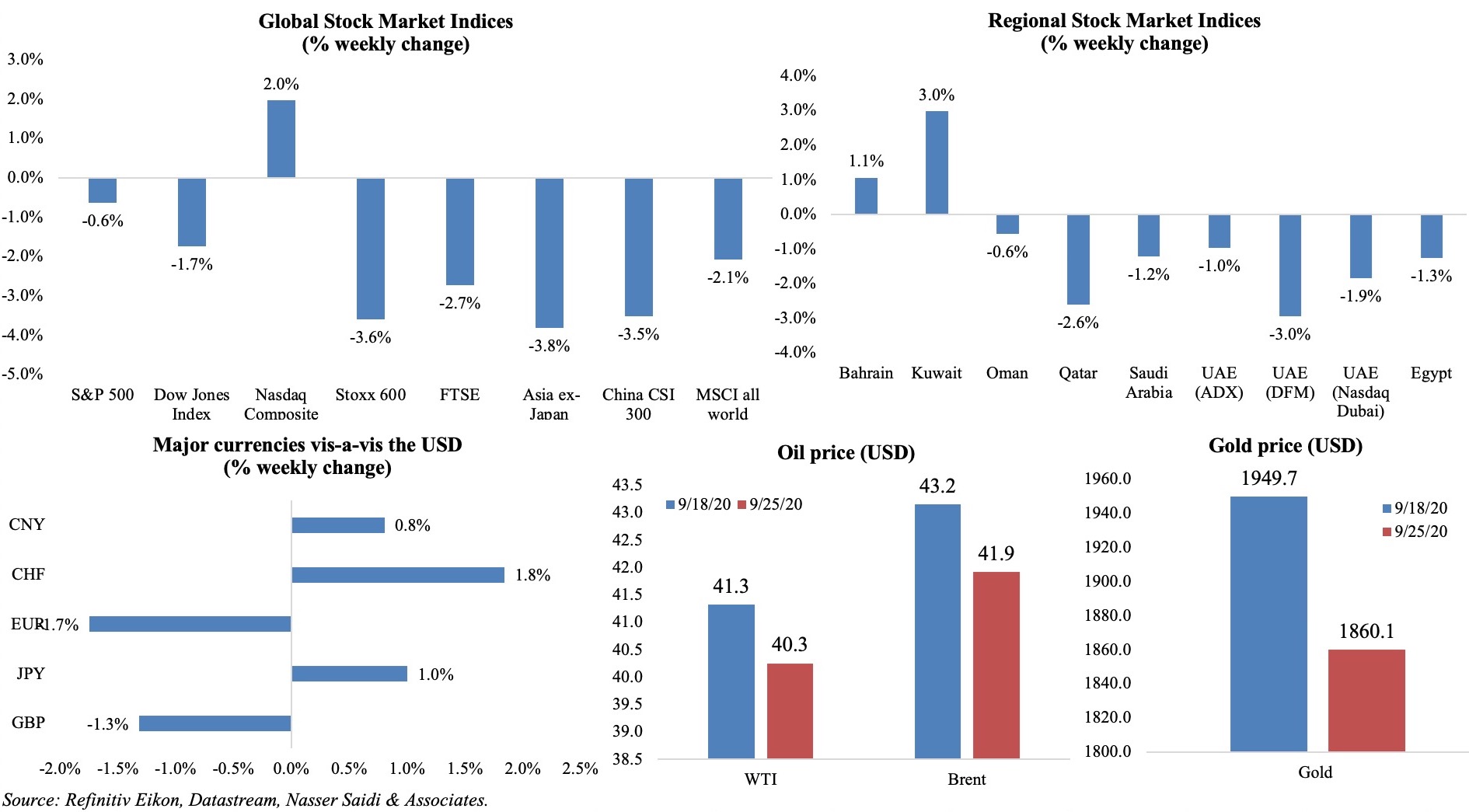

Stock markets ended in the red in across the globe: in the US, equities fell for a fourth consecutive week in spite of a tech rally, while the resurgence of Covid19 and renewed lockdowns spooked investors in Europe. In the Middle East, most equity markets were down, with the exception of Kuwait and Bahrain. Among currencies, the dollar posted its best weekly performance since Apr while the euro declined, and the yuan jumped higher following the entry of China government bonds into the FTSE Russell’s trillion-dollar World Government Bond Index (WGBI). Gold price ended 4.6% lower – the worst week in more than a month while oil prices were down by more than 2% as slowing global demand continues to be a worry.

Weekly % changes for last week (24-25 Sep) from 17th Sep (regional) and 18th Sep (international).

Global Developments

US/Americas:

- Durable goods orders edged up for the 4th consecutive month, rising by a modest 0.4% mom in Aug (Jul: +11.7%), supported by a 0.5% rise in orders for transportation equipment. Non-defense capital goods order excluding aircrafts, a proxy for business spending, increased by 1.8% following an upwardly revised 2.5% in Jul.

- The Chicago Fed National Activity Index slipped to 0.79 in Aug (Jul: 2.54), with the three-month average falling to 3.05 from 4.23 the month before. The value zero indicates an expanding economy.

- Existing home sales inched up by 2.4% mom and 10.5% yoy in Aug to 6mn (Jul: 24.7% mom). This was the highest sales pace since Dec 2006, and given tight supply and tougher competition, it took just 22 days to sell a home in Aug.

- New home sales expanded by 4.8% mom in Aug (Jul: +14.7%) to a seasonally adjusted annual rate of 1.01mn units – this was the highest since 2006. Supply constraints are emerging: the estimate of new homes for sale represent a supply of 3.3 months at the current rate of sales – the shortest period in data since 1963.

- Markit flash composite PMI in the US eased to 54.4 in Sep (Aug: 54.6), with both manufacturing and services providers reporting expansions in output. Services PMI business activity slipped to 54.6 from 55 the month before. The flash manufacturing PMI inched up to 53.5 in Sep (Aug: 53.1).

- Initial jobless claims increased by 4k to 870k in the week ended Sep 19; continuing claims fell slightly to 12.6mn from 12.75mn. Separately, talks about a new stimulus package (Democrats’ USD 2.4trn plan) has stalled given political disagreements, and the Fed Chair warned the rebound could stall if “more fiscal support” was not provided.

Europe:

- Germany’s Ifo business climate improved to 93.4 in Sep (Aug: 92.6) – the highest level since Feb – while the current assessment also inched up to 89.2 (87.9). By sector, the business climate index for services fell in Sep, after rising four consecutive times prior.

- The Markit flash composite PMI in the Eurozone eased (for a 2nd consecutive month) to 50.1 from 51.9, with divergences across sector and country. Markit manufacturing PMI increased to a 25-month high of 53.7 (Aug: 51.7), thanks to the largest rise in new orders. However, with demand affected by rising cases and social distancing measures, services PMI slipped to 47.6 from 50.5 the month before.

- A similar trend was visible in Germany’s PMI: manufacturing PMI increased to 56.6 in Sep (Aug: 52.2) while services PMI slipped to 49.1 from 52.5 the month before (on social restrictions and job security worries). Composite PMI eased to 53.7 (Aug: 54.4) and below Jul’s 2-year high.

- As UK heads into new lockdowns and restrictions, a new job support scheme aimed at “only viable jobs” (and will replace the furlough scheme) was announced by the government to support the economy. As per this plan, which will run for 6 months from Nov 1st, for every hour not worked, the employer and the government will each pay one third of the employee’s usual pay. This plan will cost the government an estimated GBP 300mn a month.

- UK lost momentum in Sep, with composite PMI at a 3-month low of 55.7 (Aug: 59.1); as both output and new business growth eased from Aug’s highs, flash manufacturing PMI slowed to 54.3 (Aug: 55.2); flash services PMI fell to 55.1 from 58.8 the month before on renewed fears about Covid19 restrictions.

- The UK government borrowed a record GBP 35.9bn in Aug, a record-high for the month. UK has borrowed a total of GBP 173.7bn since Apr, already above the USD 157.7bn recorded in the 12 months ending Mar 2010.

- The GfK Consumer Confidence Barometer in the UK rose unexpectedly to -25 in Sep from -27 in Aug; the survey however was conducted in the first half the month before the current social restrictions were put in place.

Asia Pacific:

- China’s PBoC kept benchmark lending rate steady for the 5th straight month: one-year loan prime rate remained at 3.85%, and the five-year LPR at 4.65%.

- Japan’s flash manufacturing PMI edged up by 0.1 to 47.3 in Sep, remaining below 50 for the 17th month, as both production and new orders fell further. However, business confidence strengthened, rising to a more than 2-year high.

- All Industry activity in Japan grew by 1.3% mom in Jul (Jun: 6.8%) – the second consecutive increase in activity. Both industrial production and construction outputs increased, while tertiary output fell (-0.5% from Jun’s 9%).

- Inflation in Singapore stayed flat, down by 0.4% yoy in Aug, on private transport costs (-2.3%); core inflation contracted (-0.3% in Aug) for the 7th consecutive month.

Bottom line: Q3 is drawing to an end, and there are many “events” to look forward to in Q4: round of Brexit negotiations wrap up in early Oct and an agreement needs to be in place by the EU leaders’ summit on 15 Oct, US elections in Nov (a Supreme Court nomination beforehand, and a not-so-peaceful transition should Biden win) and maybe a potential vaccine for Covid19 (cases continue to surge and new record highs are being hit in many nations leading to renewed restrictions and additional stimulus). Separately, as countries adjust to Covid19 repercussions, the G20 has called for an extension of the bilateral debt relied initiative for the poorest nations; the initiative has so far helped 43 nations defer USD 5bn in official debt service payments, but risk of defaults (foreign and domestic) loom large. Asia, especially China, seems to be on the road to recovery and export order numbers from PMI are showing signs of a revival: it was not surprising therefore that the latest WTO trade data shows Asia to be relatively less affected in Q2 (-7% yoy) as global trade value dipped by 21% yoy.

Regional Developments

- Bahrainis facing financial constraints, can submit documents to prove their status and benefit from a postponement of housing loan instalments, according to the housing minister. Separately, municipal fees were reduced for 155 Bahraini tenant families in Aug.

- Egypt’s central bank unexpectedly lowered its main overnight interest rates by 50bps: lending and deposit rates now stand at 9.75% and 8.75% respectively. The apex bank cited exceptionally low inflation as an enabling factor to lower rates and support the economy.

- Foreign holdings of Egyptian treasury bills rebounded to EGP 172.0bn (USD 10.9bn) in Jul from EGP 122.44bn at end-Jun.

- Banks operating in Egypt posted a net profit of EGP 50.04bn at end-Jun, according to the central bank. Total assets stood at EGP 6.4trn as of end-Jun, while provisions were EGP 150.07bn alongside deposits at EGP 4.68trn.

- Remittances into Egypt increased by 9.5% yoy to USD 2.9bn in Jul; total remittances this year grew by 7.8% yoy to USD 17bn.

- The manufacturing and extractive industries index in Egypt declined by 6.5% mom to 97.39 in Jul. However, manufacture of motor vehicles and basic pharma products posted increased of 8% and 3.9% respectively.

- Ration card holders in Egypt had been allocated EGP 13bn under the presidential initiative to boost local consumption (which ends on Oct 26).

- Egypt’s finance ministry plans to issue green bonds before end of this year, disclosed the minister, with the ministry currently in negotiations to agree on the proposed value.

- About EGP 160bn had been invested to develop the Upper Egypt governorates over the past five years. This accounted for 20% of total government allotment since 2015.

- Egypt will establish a department designated for the tax treatment of e-commerce companies, revealed the finance minister; it is expected to start in 2021.

- The Egyptian Natural Gas Holding Company is finalizing 6 new natural gas agreements worth USD 731mn. Currently, natural gas production stands at 7.2bn cubic feet of gas per day.

- In a bid to attract more tourists, Egypt has cut fees on airlines’ landing and parking by 50%, and ground services by 20% for all companies operating in the Red Sea, South Sinai, and Marsa Matrouh airports.

- Egypt’s Financial Regulatory Authority’s Board of Directors approved a draft law regulating and developing the use of Fintech in non-banking financial activities.

- US renewed a waiver for Iraq to import Iranian electricity for 60 days; this extension is much shorter compared to previous waivers lasting between 90-120 days.

- Iraq’s oil ministry reiterated its commitment to the OPEC+ agreement, after reports circulated about talks with the OPEC+ to increase the country’s crude oil exports.

- Exports from Jordan fell by 2% yoy in Jan-Jul while imports plummeted by 16.9%, resulting in a narrowing of trade deficit by 24.4%. In Jul alone, exports were up by 5.2% yoy and 16% mom.

- Revenues from Jordan’s tourism sector fell by 63.7% yoy to JOD 819mn in Jan-Jul 2020, according to central bank data. Revenues were JOD 4bn last year.

- Losses of restaurants and cafes in Jordan amounted to approximately JOD 20mn in the two weeks’ forced closure.

- Jordan and the Kuwait Fund for Arab Economic Development signed an agreement for two loans worth KWD 25mn (to support infrastructure development) and a grant of KWD 400k (USD 1.32mn).

- Kuwait was downgraded for the first time by Moody’s, lowered by 2 notches to A1 (the 5th highest investment-grade level), citing government’s “liquidity risks” as well as the “fractious relationship” between parliament and the government as a long-standing constraint. The ratings firm projects that the country would require net sovereign issuance of up to KWD 27.6bn (USD 90bn) to meet funding requirements between the current fiscal year till 2023-24.

- Kuwait’s National Assembly panel passed a draft law to reduce expat numbers in the country over the next five years, though without specifying related caps or percentages. It gives the government 6 months to determine the number of expats needed.

- The value of electronic payments in Kuwait surged since Jul by 25% to KWD 2bn compared to Jan-Feb when it was about KWD 1.6bn.

- Kuwait’s travel restrictions will be fully lifted only after the vaccine is widely available in the country, according to the Deputy Director General for Kuwait Airport Affairs. Currently commercial flights do not exceed 30% of the airport’s normal capacity.

- A survey of 159 companies and SMEs in Kuwait showed a drop in value of sales by a monthly average of 59%, a decline in profit margin by 66% as well as a decrease in average salaries & wages by 46%.

- Kuwait’s Ministry of Defense reduced USD 1bn from a Eurofighter aircraft deal, reported Al Rai daily. This followed a request from the finance ministry to lower spending but raised questions as to why such a move was not made earlier (if easily achievable).

- Lebanon’s PM designate resigned after a month, citing “concern for national unity”, after being unable to form a cabinet. The black market exchange rate reached around LBP 9000 for a dollar. Earlier, in a bid to end the stalemate in forming a government in Lebanon, it was proposed that an “independent” Shi’ite candidate be considered as finance minister, as a one-time exception. France had backed this proposal, but other political barriers were raised.

- Consumer prices in Lebanon increased by 58.1% yoy in Jan-Aug this year; in Aug alone, prices spiked by 120% yoy on the back of a 467% surge in food prices and a 513% uptick in clothing and footwear.

- Oman plans to issue USD-denominated bonds worth between USD 3-4bn, reported Reuters. This would follow the USD 2bn bridge loan secured last month.

- Oman will impose excise tax of 50% on sweetened drinks from the start of Oct.

- The Tax Authority in Oman has scrapped a previous ruling that required taxpayers to file a provisional return of income within three months and an annual return within 6 months of end of the accounting year; instead, taxpayers are now mandated to file only one tax return within four months from the end of the tax year.

- Oman’s ministry of commerce and industry issued more than 3,000 import permits for cars and motorcycle shipments in H1 this year.

- Expat population in Oman dropped by more than 50k in Aug, according to data from National Centre for Statistics and Information.

- Expats with valid residency can re-enter Oman from Oct 1st subject to a test on arrival and quarantine for 14 days. International flights have been given the green light for resuming operations from Oct, but will be limited at the rate of 2 flights per week for each of its previous destinations. Oman Air will start operations within the country (Muscat to Salalah & back).

- Saudi Arabia has seen a decline in FDI this year, due to the global pandemic, disclosed the investment minister, at a G20 meeting. He also stated that FDI into the country rose to USD 3.5bn in Jan-Sep 2019 from USD 3.18bn a year ago.

- The value of contracts awarded in Saudi Arabia plunged by 83.2% yoy to SAR 11bn (USD 2.9bn) in Q2, as many project awards remained suspended during the outbreak. The total value slipped to SAR 56.2bn in H1 this year vs SAR 57.8bn, thanks to a strong Q1. Water (SAR 4.3bn), oil & gas (SAR 1.8bn), and real estate (SAR 1.7bn) accounted for 70% of awarded contracts by value.

- About 38 government authorities in Saudi Arabia will be prepared for privatization within 24 months’ time, in addition to the education universities and specialist hospitals, reported Okaz.

- Saudi Arabia will resume Umrah for citizens and residents at 30% capacity (~6k persons) as part of the first stage of reopening. Starting Oct 4, each person will be given three hours to perform the Umrah.

- International travel restrictions are slowly being lifted in Saudi Arabia: patients that require to travel abroad for treatments can now do so subject to meeting certain conditions set by the health ministry.

UAE Focus

- UAE issued a new decree – which goes into effect from Sep 25 – to enforce gender equality in private sector wages e. if they are doing the same work.

- Economic growth in the UAE is forecast to contract by 5.2% this year, revealed the central bank’s latest quarterly review. Q2’s non-oil GDP is estimated to have dropped by 9.3% yoy following a 2.7% decline in Q1.

- The UAE central bank disclosed that AED 44.72bn of the AED 50bn liquidity facility had been drawn by banks until end-Jul (from AED 44.38bn drawn till end-Jun).

- Foreign currency assets of the central bank of UAE slipped by 4% yoy to AED 353.8bn in Jul this year.

- Non-oil trade between Abu Dhabi and Saudi Arabia amounted to AED 493.8bn over the past decade. This year, Saudi Arabia was the emirate’s top trading partner accounting for 22.3% of total non-oil trade. Meanwhile, non-oil trade between Dubai and Saudi Arabia amounted to AED 500bn in the 2010-2020 period and AED 24bn in H1 this year.

- Non-oil foreign trade between UAE and the US exceeded USD 11bn in H1 this year; this follows bilateral trade value of USD 26.3bn last year.

- UAE’s Federal Authority for Identity and Citizenship has started issuing entry permits into the country including tourist visas; no new work permits are being issued for now. Residents need to obtain a negative PCR test result as well as self-isolate at home. Dubai was the only emirate permitting entry of tourists since Jul 7th.

- Abu Dhabi announced more than AED 110mn in financial incentives to agricultural technology companies to start operations in the emirate.

Media Review

UNCTAD Trade and Development Report 2020

https://unctad.org/en/PublicationsLibrary/tdr2020_en.pdf

https://unctad.org/en/PublicationsLibrary/tdr2020overview_ar.pdf (overview in Arabic)

WEF’s core and expanded set of “Stakeholder Capitalism Metrics”

https://www.weforum.org/reports/measuring-stakeholder-capitalism-towards-common-metrics-and-consistent-reporting-of-sustainable-value-creation

Digital Solutions for Small Businesses in the Middle East and North Africa

https://blogs.imf.org/2020/09/22/digital-solutions-for-small-businesses-in-the-middle-east-and-north-africa/

Israel, Lebanon agree to hold maritime border negotiations

https://www.jpost.com/middle-east/israel-lebanon-agree-to-hold-maritime-border-negotiation-talks-643577

Virus prompts rethink of developing economies’ urban planning

https://www.ft.com/content/a9101163-f4e8-4bf2-a16f-2ae14d5746a3

Powered by: