Markets

S&P 500 touched another record high last week on upbeat US jobs reports (https://on.ft.com/2PH139z), but world equity markets dipped after news broke of concerns regarding trade talks and “phase one” pact (Pompeo’s verbal attacks on China, Beijing’s doubts on ability to reach a comprehensive long-term deal). Regional markets were mostly down towards end of the week amidst falling oil prices. The dollar fell to a 10-day low after the Fed rate cut, supporting a rise in the gold price while oil prices dipped.

Global Developments

US/Americas:

- US real GDP growth slowed to 1.9% in Q3 (Q2: 2%), thanks to personal consumption expenditures growing at 2.9% (decelerating from 4.6% in Q2) while gross private domestic investment slipped by 1.5% (though better than the 6.3% drop in Q2).

- The PCE price index ebbed to 1.3% yoy in Sep (Aug: 1.4%).Excluding food and energy, the core PCE index remained unchanged in Sep from the month before but slowed in yoy terms to 1.7% (Aug: 1.8%).

- Fed cut interest rates by 25 bps for the third consecutive time, while signaling a pause. The Fed chair stated during the press conference that central bank officials “see the current stance of monetary policy as likely to remain appropriate”.

- Non-farm payrolls added 128k in Oct, following an upwardly revised 180k reading in Sep. Unemployment rate ticked up to 3.6% while the average hourly earnings remained unchanged at 3%. Employment in the private sector increased by 125k in Oct following Sep’s downwardly revised reading of 93k.

- ISM manufacturing improved to 48.3 in Oct, after the sharp drop to 47.8 in Sep, supported by new orders (+1.8 points) and new export orders (+9 points) while output fell 1.1 points.

- US goods trade deficit narrowed by 3.6% to USD70.4bn in Sep, as exports declined by 1.6% (on lower shipments of soybean and automobiles) while imports were lower by 2.3% (on drops in capital and consumer goods, automobiles, industrial supplies and others).

- Pending home sales gained 1.5% mom in Sep (Aug: 0.8%). S&P Case Shiller home price indices ticked up by 3.2% yoy in Aug, up from Jul’s 3.1% while average rates for a 30-year mortgage fell to 3.75% last week after hitting nearly 5% last Nov.

- Initial jobless claims increased by 5k to 218k in the week ended Oct 26; the 4-week moving average of claims slipped 500 to 214,750.

Europe:

- EU’s preliminary GDP grew by 0.2% qoq and 1.1% yoy in Q3 this year (Q2: 0.2% qoq and 1.2% yoy). Inflation fell to 0.7% (Sep: 0.8%) while unemployment rate ticked up to 7.5%.

- German inflation remained unchanged at 0.9% yoy in Oct, and unemployment rate dropped to 4.8% – the lowest level since Nov 2018. Retail sales grew by just 0.1% mom in Sep (after a revised 0.1% drop in Aug), while in yoy terms it was up 3.4% (Aug: 3.1%).

- EU economic sentiment indicator fell to 100.8 points in Oct (Sep: 101.7) while the business climate indicator rose to -0.19 points in October from -0.23 a month earlier.

- With the new Jan 31 Brexit deadline, and ongoing parliamentary deadlock, the UK will hold elections on 12 Dec, 2 weeks before Christmas: this will be the fourth time the country heads to polls in less than 5 years.

Asia Pacific:

- China’s Caixin manufacturing PMI edged up to 51.7 in Oct (Sep: 51.4) – the highest since Feb 2017 – thanks to an increase in output and new orders; exports orders posted the first increase in 5 months.The official NBS manufacturing PMI showed that activity contracted for a 6th consecutive month, with the reading at 49.3 in Oct (Sep: 49.8). Non-manufacturing PMI fell to 52.8 in Oct (Sep: 53.7), the lowest level since Feb 2016.

- The Bank of Japan left rates unchanged at the meeting last week and hinted at its willingness to cut rates further. Inflation forecasts for 2020 were lowered to 0.5% from 0.8%.

- Core inflation in Tokyo rose by 0.5% yoy in Oct; excluding the impact of the tax hike and the childcare discount, core inflation hit 0.34% – the slowest pace in more than two years.

- Industrial production in Japan ticked up by 1.4% mom in Sep, following Aug’s 1.2% fall. Retail sales grew at the fastest pace since Mar 2014, rising 9.1% yoy in Sep vs Aug’s 2%, as consumers spent more ahead of Oct’s sales tax hike to 10% from 8%.

- South Korea’s industrial production declined by 0.4% mom in Sep (Aug: 0.2%), with the 2% expansion in manufacturing and mining output being offset by a 1.2% and 2.9% decline in the services industry and the wholesale and retail sector production respectively. Retail sales shrank by 2.2% in Sep – the fastest fall since Dec 2017 – following Aug’s 3.9% jump.

- Hong Kong fell into its first recession in 10 years, with the Q3 GDP shrinking by 3.2% qoq and 2.9% yoy. Q2 GDP was revised down to 0.4% yoy (from 0.6% previously) and a contraction of 0.5% qoq (from 0.3%).

- India’s fiscal deficit in Sep touched 92.6% of the 2019-20 budget estimate, supported by the transfers from the central bank earlier this year. In the Apr-Sep period, government spending stood at 53.4% of full year estimates.

Bottom line: A week of mixed news – the temporary trade truce seems to be in trouble following rhetoric from China while in the UK, Brexit uncertainty drags on with elections coming up (again). Jobs growth in the US and China’s PMI numbers provided relief towards the end of the week which saw weak GDP numbers in the US and EU alongside a recession in Hong Kong while the Fed and BoJ meetings sprung no surprises. The trade tensions and its impact continue to be evident: latest UNCTAD data revealed that global FDI flows – at USD 640bn in H1 – remained below the average level of the past decade; the IIF reported a slowing of portfolio inflows to emerging markets to USD 22.5bn in Oct from Sep’s USD 37.7bn.

Regional Developments

- Saudi Crown Prince gave the green light for the Aramco IPO, and the official intention to float was approved by the Saudi Capital Market Authority. The approval is valid for 6 months, and the shares are likely to start trading in Dec.The valuation is likely to have been lowered to around USD 1.2-1.5trn, and next year’s dividend likely to be boosted by USD 5bn to USD 80bn to woo investors. Bloomberg reported that IPO investors have been guaranteed that the dividend won’t fall until after 2024, regardless of oil price moves.

- The IMF issued the Regional Economic Outlook for the MENA region:oil exporters’ growth is expected to soften to 1.3% this year on lower and more volatile global oil prices, geopolitical tensions, and the global slowdown while oil importers’ growth is higher at 3.6%.

- GCC central banks lowered interest rates last week, mirroring the Fed’s 25bps rate cut.

- Bahrain’s money supply increased by 8.4% yoy to BHD 13.5bn (USD 35.9bn) as of Sep 2019. Outstanding loans and credit disbursed by banks grew by 5.6% to BHD 9.8bn.

- Bahrain’s national exports declined by 6% yoy to BHD 584mn (USD 1.55bn) in Q3 2019; Saudi Arabia was the top importer of Bahraini exports (BHD 112mn), followed by the US and UAE at BHD 74 and 57mn respectively.

- Foreign investment in Bahrain edged up by 1% qoq to BHD 10.9bn (USD 29.25bn) in Q2, according to the initial Foreign Investment Survey results. FDI flowed most into the financial and insurance sector (+1.2% to BHD 7.9bn) while FDI from Kuwait topped the list (+1.3% to BHD 3.6bn).

- Bahrain’s Economic Development Board set up a fast-track process for global and regional startups to use Bahrain as their launchpad: the process covers residency, visa requirements and business registration as well as access to grants and financial support.

- The number of Bahraini citizens working in the public sector declined by 13% to 46,712 in H1 this year, as many citizens chose the option of voluntary retirement. Bahrianis working in the private sector increased to 105,158 in H1 (from 104,884 in H1 2018).

- Egypt’s GDP grew by 5.6% yoy in the Jul-Sep quarter, according to the planning minister. The target is 6% growth in the 2019-20 fiscal year.

- Money supply in Egypt moved up by 13% yoy to EGP 4.01trn (USD 249.22bn) in Sep. Separately, external debt jumped by 17.3% yoy to USD 108.7bn as of end-Jun, resulting in external debt-to-GDP ratio at 36%.

- Non-oil exports from Egypt increased by 3% yoy to USD 19.2bn in Jan-Sep 2019. About 37% of Egypt’s exports went to the US (USD 1.64bn), followed by UAE and Saudi Arabia at USD 1.4 and 1.3bn respectively.

- Egypt’s industrial production accelerated by 21.6% yoy to EGP 188.8bn in Q4 2018.

- Egypt attracted FDI flows worth USD 3.6bn in H1 this year, according to UNCTAD, and was the largest FDI recipient in Africa (which witnessed inflows of USD 23bn).

- Egypt’s finance ministry disclosed the selection of five international lenders for a new dollar-denominated bond offering to be made in the 2019-20 financial year (no dates were specified).

- Japanese tourists into Egypt increased by 38.2% yoy in Jan-Sep this year, according to the latter’s minister of tourism.

- Egypt’s unemployment rate fell to 7.5% in Q2 2019, recording the lowest level in 30 years, according to the cabinet’s media centre.

- Jordan’s central bank lowered interest rates by 25bps for the third time this year, given low inflation rates amidst rise in tourist incomes and remittances.

- Kuwait’s central bank sold bonds and related tawarruqworth KWD 200mn, with a 3% return. The 3-month bonds were oversubscribed by 13.25 times.

- Bilateral trade between Kuwait and China grew to USD 7bn (excluding petroleum products and derivatives); China was also Kuwait’s top trading partner in 2018.

- Reuters reported that the US White House budget office and National Security Council had decided to withhold USD 105mn in security aid for Lebanon. No reason was provided for the decision.

- Lebanon’s President called for the formation of a new government of technocrats, after Tuesday’s resignation of Saad Hariri and asking the cabinet to continue in a caretaker role. Banks, which were shut for more than 10 days, reopened on Fri. Dollar bonds and CDS spreads recovered on Thurs after being under selling pressure during the anti-government protests.

- Lebanon is delaying a planned Eurobond issuance of up to USD 3bn given the unrest but will repay debt maturing in Nov, reported Bloomberg, citing people familiar with the matter.

- Oman’s non-oil exports grew by 18.3% yoy to USD 9.7bn in 2018, providing employment to over 240k persons, according to a senior Ithraa Oman official.

- Over 202k Omanis were registered with public sector pension funds at end-Aug (-0.2% yoy).

- Saudi Arabia expects its 2020 budget deficit to widen to SAR 187bn (USD 49.86bn) or 6.5% of GDP, from an estimated SAR 131bn this year (4.7% of GDP), according to the finance minister. Revenues are expected to dip to SAR 833bn next year from a projected SAR 917bn this year, on lower oil prices and revenue. The minister also added that real GDP growth is estimated at 2.3% next year, from 0.9% this year (IMF estimates 2.2% growth next year from this year’s 0.2%).

- Saudi Arabia closed 24 investment deals worth a total of USD 20bn at the Future Investment Initiative held last week. The largest deals included the USD 5bn mixed-use real estate Arabian Dream project and USD 11.45bn Air Product Qudra project.

- The Public Investment Fund (PIF) in Saudi Arabia has successfully raised a USD 10bn bridging loan to cover its general corporate expenses and investment requirements; the loan will be repaid following the completion of the SABIC-Aramco transaction.

- New residential mortgage contracts jumped by 353% to 16,816 in Sep; value of residential loans surged by 249% to SAR 7.125bn. Mortgage loans have jumped more than 3 times over this year, according to SAMA.

- Saudi Arabia’s foreign reserves declined by 1.3% yoy and 1.4% mom to SAR 1.877trn (USD 500.59bn)in Sep – recording the lowest level since Mar 2019. General reserves declined by 13.5% yoy to SAR 496.04bn by end-Sep.

- Saudi Arabia launched an export bank with a capital of SAR 30bn (USD 8bn), in a bid to support local producers and develop international relations to support foreign and national investors. The minister of industry and mineral resources also disclosed that 3 industrial free zones were ready to be launched.

- The Saudi Arabian General Investment Authority (SAGIA) announced a 30% yoy increase in new foreign investor licenses to 251 in Q3 this year.Total licenses touched 809 in Q3.

- Saudi Arabia’s Ministry of Foreign Affairs revealed that 77,069 tourist visas were issued since the launch, of which a total 28,190 persons had arrived during the period between Sep 27-Oct 30. In terms of nationality, about 17,988 Chinese tourists had secured visas followed closely by the British at 17,777.

- Saudi Arabia plans to launch a carbon trading scheme, revealed its energy minister at the FII conference. It operates the largest carbon capture and utilization plant in the world, turning half a million tons of CO2 annually into products such as fertilizers and methanol.

- Saudi Arabia’s construction sector expanded, growing by 3% this year, from a 2.8% contraction last year.

- Saudi Arabia and UAE are planning to issue a joint visa enabling visitors to UAE to visit Saudi and vice versa. The visa is likely to come into force in 2020.

UAE Focus

- UAE cabinet approved a zero-deficit federal budget of AED 61bn (USD 16.61bn) – the largest budget ever recorded – for the fiscal year 2020 (2019: AED 60.3bn). A third of the budget is allocated for social development, one third for government affairs and the rest to infrastructure, economic resources and living benefits.

- Total re-exports from the UAE amounted to AED 1.046trn over the past three years, together accounting for 1/4thof UAE’s total trade volume during the period.

- Non-oil exports through Abu Dhabi’s ports touched AED 136.3bn in Jan-Aug 2019; total trade declined by 17.5% yoy in Aug, with exports and imports down by 14.7% and 26.4% respectively. Saudi Arabia, US, Kuwait, Japan and UK were the top trade partners.

- Dubai Economy’s Composite Business Confidence Index of local businesses increased 14.9 points (from Q2) and reached 129.8 in Q3 this year. Large companies are more optimistic than SMEs about their outlook and the main challenges firms face include delays in payments (as cited by 43% of firms), followed by competition (34%) and insufficient demand (17%).

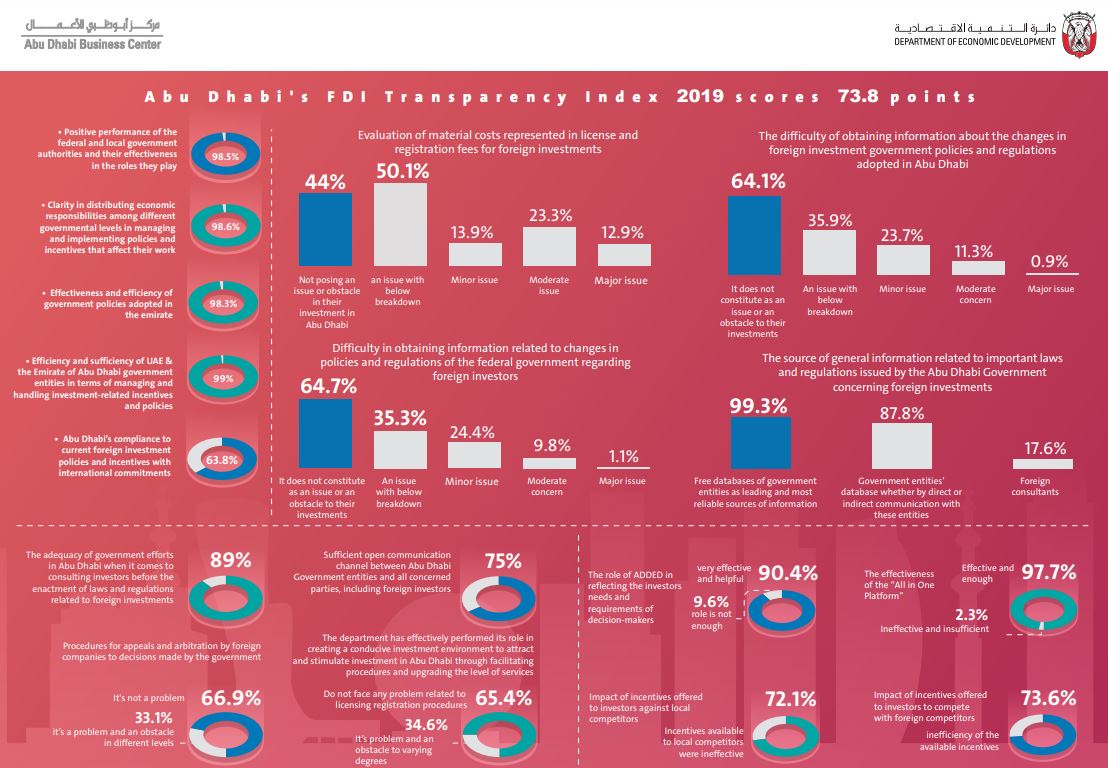

- The Foreign Direct Investment Transparency Index in Abu Dhabi touched 73.8 points a 100-point scale in 2019, reflecting the responses to key topics including the efficiency of government policies to attract FDI as well as incentives provided to foreign investors. More: http://imgs.syndigate.info/320/1058/18/157226439249.jpg

- Fitch affirmed Abu Dhabi’s rating at AA with a stable outlook, reflecting the emirate’s strong fiscal and external metrics and high GDP per capita.

- S&P affirmed Sharjah’s ‘BBB+/A-2’ long- and short-term foreign and local currency sovereign credit ratings, with a stable outlook.

Media Review

IMF issues Regional Economic Outlook for the MENAP region

https://www.imf.org/en/Publications/REO/MECA/Issues/2019/10/19/reo-menap-cca-1019

Trump’s whims stoke Middle East fears of instability

https://www.ft.com/content/cc040f18-f987-11e9-a354-36acbbb0d9b6

Key Takeaways from the FII 2019 conference

https://www.zawya.com/uae/en/business/story/From_Aramco_IPO_to_sustainability_five_key_takeaways_from_Saudi_Arabias_FII_2019_conference-SNG_158337665/

A week in charts: The Economist

https://www.economist.com/graphic-detail/2019/11/01/a-british-election-and-other-uncertainties

The Allure and Limits of Monetized Fiscal Deficits

https://www.project-syndicate.org/commentary/limits-of-mmt-supply-shock-by-nouriel-roubini-2019-10

Powered by:

{kind=link}