Markets

Stock markets advanced last week, thanks to the Fed’s dovish statement, with US stocks closing just shy of Apr’s record-high. On the other side of the globe meanwhile, the Chinese stock market recorded double-digit weekly losses, reporting the biggest weekly drop since Oct 2008, and igniting panic over the bursting of a perceived bubble. Among regional markets, Saudi Tadawul’s opening up was touted to be a major event – however, it remained the weakest performer; with limited licenses granted, there was little activity and the index fell 0.8% on the day it opened for QFIs. In spite of the looming deadline for Greece, the euro remained resilient and was up against the greenback. Oil prices continue to display volatility, while gold closed higher compared to a week ago.

Global Developments

US/Americas:

- The Fed left its interest rate unchanged, describing the economy as expanding moderately, i.e. better compared to the assessment in April. The Fed emphasized that the rates were likely to be raised only gradually, although its projections still suggest that “lift-off” would take place this year. Fed officials forecasts are for the benchmark interest rate to rise to 0.625% at the end of 2015, while lowering it for next year and the year after.

- US inflation rose 0.4% mom in May (compared to 0.1% in Apr), the largest gain since early 2013, thanks to energy prices. Core inflation increased 0.1% last month, the smallest gain this year. The acceleration in inflation shows that deflationary fears were exaggerated.

- US industrial production fell 0.2% mom in May, with manufacturing numbers continuing to disappoint, amid a strengthening dollar and weakening global demand. Growing only a modest 1.8%yoy, output is barely above its pre-recession peak set in early 2008.

- The Conference Board index of leading indicators increased by 0.7% in May, the same figure as in Apr, lifted by building permit issuances and financial components.

- The NAHB housing market index increased by 5 points in June, moving the index from 54 to 59 – its highest point in nine months. Housing starts disappointed in May, coming in 11.1% mom below revised Apr totals, but still 5.1% yoy.

- Initial claims for unemployment insurance fell by 12k to 267k and the four-week moving average fell 2k to 276,750.

Europe:

- The Greek bailout saga witnessed another inconclusive week amid mutual accusations and stern warnings. A summit with the Eurogroup is planned for Monday, billed as yet another “last-ditch effort”, though Greece is reportedly putting together a new proposal, including elimination of many tax breaks, if not full pension reform.

- Investor confidence, measured by the ZEW index, worsened again in Germany, falling to 31.5 in Jun from 41.9 in May, while the ZEW indicator for the current situation retrenched to 62.9 from 65.7.

- Eurozone inflation accelerated in May to 0.3% yoy, following a flat reading in Apr, with more expensive food, tobacco and services outweighing the impact of lower energy prices. Core inflation was up 0.1% mom and 0.9% yoy.

- The Eurozone’s current account surplus contracted to EUR 20.4bn in Apr, from a revised EUR 24.4bn the previous month

- Germany’s CPI increased 0.7% in May, rising for the fourth consecutive month and following a 0.4% increase in Apr; Italy’s inflation accelerated to 0.2% yoy in May. UK inflation rate rose 0.1% yoy in May, the first increase in 4 months, after falling 0.1% in Apr.

- UK retail sales rose 4.6% yoy in May, the same as in Apr, underscoring robust private consumption.

- UK unemployment rate remained unchanged at 5.5% in Q1 2015. Separately, PPI fell a further -1.6% yoy in May after declining by -1.7% in Apr.

.Asia and Pacific:

- Foreign direct investment into China grew 7.8% yoy and totaled USD 9.3bn in May, marginally lower than Apr’s USD 9.6bn. Overall, FDI grew 47.4% yoy to USD 45.41bn for the Jan-May period.

- India’s WPI inflation fell -2.3% yoy in May, following a steeper -2.7% decline in Apr. However, food inflation was +3.8% in May, despite a good start to monsoon rains. This could pose a major challenge for the Reserve Bank of India, which has already cut interest rates three times this year.

- India’s trade balance widened to a deficit of USD 10.4bn in May, from Apr’s USD 11bn deficit.

- Japan’s foreign trade recorded a JPY 182bn deficit in May, after the JPY 240bn shortfall registered in Apr.

- Indonesia’s monthly trade surplus widened to USD 960mn in May, up from USD 450mn in the previous month. Meanwhile, the Bank of Indonesia maintained its benchmark policy rate at 7.5% in May’s monetary policy meeting. Given weak economic growth – Q1 GDP was the lowest in the last 6 years – pressures are mounting to respond with rate cuts.

- Singapore’s non-oil domestic exports fell 0.2% yoy in May, surprisingly decelerating from a 2.2% increase in Apr.

Bottom line: The most notable implication from last week macro data is that deflation is not a concern anymore. Dovish words from the Federal Open Market Committee and hopes that Greece and the Troika are bent on reaching an eleventh-hour deal to save the country form a catastrophe spread some optimism, but the longer-term macro picture remains clouded.

Regional Developments

- Egypt 2015-16 budget projects a 9.9% of GDP deficit, narrowing slightly from an expected gap of 10.8% in the current fiscal year, in spite of an 18.5% yoy increase in expenditure, mostly on social welfare programs. Projected public revenues stand at about EGP 599bn, up 23.2% yoy. However, the draft budget also earmarked EGP 2.2bn in foreign grants.

- Egypt’s trade minister stated that the country had reached an agreement with China over 15 projects worth about USD 10bn, mainly focused on the electricity and transport sectors, with financing agreements to be signed between late Jun and Sep.

- The legal framework for Egypt’s proposed sovereign investment fund is expected to be finalised within four months, as per quotes from the planning minister. The fund will have a board of trustees headed by the PM and will be managed by investment banks in order to attract private sector investors to the projects. It was also disclosed that there would be sub-funds for each sector, in which foreign sovereign funds will be able to take a 50% stake.

- Jordan’s finance minister revealed that the country would soon launch its first sovereign Sukuk issue (raising around JOD 400mn) to finance real estate projects.

- Bank lending growth in Kuwait was up 5% yoy in Apr (Mar: 4.4%) while M2 money supply growth rose to 5.8% yoy (Mar: 3.6%).

- MSCI Barra maintained Lebanon in its “frontier markets” category, highlighting the need to improve equal rights to foreign investors though it was given a “no major issues” rating in terms of investor qualification requirements.

- According to Lebanon’s defense minister, US weapons worth USD 462mn including missiles and 6 military aircrafts was due to arrive in the country by end of next year.

- According to the Central Bank of Oman, credit registered a double-digit growth, rising 10.6% yoy to OMR 17.5bn at the end of Apr 2015; during this period, aggregate deposits grew 5.7% to OMR 17.8bn.

- Real estate transactions in Oman topped OMR 292mn this May; there were 32,597 reported transactions through which OMR 5.79mn was collected as fees.

- The cost to the Omani government of subsidising electricity supply dipped 2.5% yoy to around OMR 302mn in 2014, from the previous year’s high of OMR 310mn, according to the Electricity Holding Company.

- Qatar inflation grew 0.87% yoy and 0.56% mom in May, thanks to higher education expenses, transportation costs and rents.

- Qatar‘s gross domestic expenditure on the research and development sector hit QAR 3.25bn, or 0.47% of GDP, as per data released by the Ministry of Development Planning and statistics.

- Saudi Arabia‘s crude exports fell by 161k barrels per day (bpd) to 7.737mn bpd in Apr, down from Mar’s near decade-high 7.898mn.

- Non-oil exports in Saudi Arabia dropped by 14.3% yoy to SAR 15.78bn while imports fell 13.6% to SAR 50.12bn in Apr. UAE topped the list of major importers of non-oil products, at 13.05% of the total value of exports, followed by China at 11.81% and India at 6.04%.

- A senior Aramco official revealed that Saudi Arabia was ready to raise oil output to a new record high to meet growing global demand, despite increased domestic use.

- Prior to the opening of Tadawul, Al Eqtisadiah daily reported that foreign investors were holding 5.1% of the market shares or SAR 108.9bn. There were 4 companies in which foreign investors held more than 40% of the total shares: SHB at 41.8%, SABB (41.6%), ANB (40.9%), and Arabia Insurance Company (40.3%). Separately, HSBC is the only foreign institution that has obtained a license to invest.

- The Global Wealth 2015 report, released by BCG, found that all GCC nations were in the top 15 countries globally in the ranking of proportion of millionaire households: Kuwait was ranked at 5th, while UAE, Oman and Saudi Arabia were ranked 10th, 12th and 15th respectively. In the Middle East and Africa region, the share of private wealth held in equities stood at 27% in 2014 – amongst the highest in the world – while the share of private wealth held in bonds was also quite high at 21%.

- Middle East’s sovereign investors have the highest return objective and the longest investment horizons (at an average of 7.8 years), making them more resilient to fund withdrawal risks, according to Invesco’s Global Sovereign Asset Management Study. Middle Eastern sovereign investors are disclosed to be keen investors in emerging market infrastructure, especially in Africa and parts of Asia.

UAE Focus

- Sheikh Mohammed bin Rashid has highlighted the need for “regional need for a real economic and developmental movement; thus, serious steps must be taken to achieve economic integration in the Gulf so as to ensure the stability of the whole region”.

- UAE’s oil minister revealed that his ministry is preparing a report on the system of fuel subsidies and that this report would be submitted soon to the government.

- Inflation in Abu Dhabi edged up by 0.2% mom in May, with the food and beverages sub-category reporting the steepest rise of 2.8% mom.

- Passenger traffic through Dubai airports were up 5.7% yoy to 6.51mn in Apr, while in year-to-date terms traffic grew 6.5% to 26.12mn people.

- The Emirates Development Bank, created by the merger of Emirates Industrial Bank and Emirates Real Estate Bank, announced its intention to allocate AED 5bn dirhams to financing housing, industrial and other schemes for UAE nationals.

Media Review

Greece’s desperate diplomacy

http://www.bloomberg.com/news/articles/2015-06-19/greece-stumbling-to-euro-exit-as-talks-end-in-frustration-ib3d3x9x

http://www.economist.com/news/leaders/21654598-greece-and-euro-zone-are-stuck-abusive-relationship-my-big-fat-greek-divorce

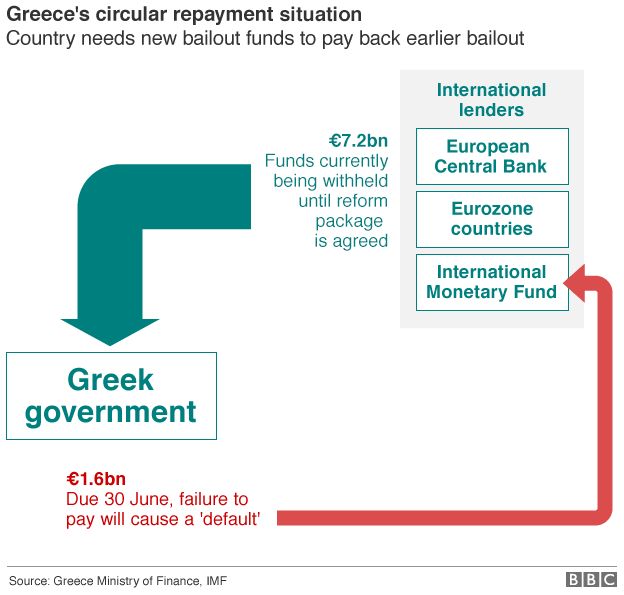

Greece’s circular repayment situation

http://ichef.bbci.co.uk/news/624/cpsprodpb/161D7/production/_83738509_greek_funding_crisis.gif

Chinese Bubble

http://www.bloomberg.com/news/videos/2015-06-19/has-the-chinese-rally-run-its-course-

The booming 18 cities in the world

http://www.bloomberg.com/news/articles/2015-06-19/these-18-cities-will-see-the-most-economic-growth-next-year

Sheikh Mohammed on the growth and prospects of the UAE economy

http://www.sheikhmohammed.com/vgn-ext-templating/v/index.jsp?vgnextoid=05ccba5b9f00e410VgnVCM1000003f64a8c0RCRD&vgnextchannel=2777bc9e88caf210VgnVCM1000004d64a8c0RCRD&vgnextfmt=default&date=1434820879190&type=sheikh

{kind=link}