Comments on Saudi Arabia’s economic diversification in Al Arabiya News, 8 Apr 2024

Dr. Nasser Saidi’s comments appeared in an Al Arabiya News article titled “Saudi Arabia’s economic diversification: Driving growth beyond oil” published on 8th April 2024.

The comments are posted below.

Amidst the dynamic economic shifts within Saudi Arabia, experts underscore the essential contribution of the non-oil private sector to driving sustainable job creation and enhancing total factor productivity growth, contrasting it with the capital-intensive oil and gas sector’s limitations in meeting the demands of the burgeoning young and educated population.

“With approximately 60 percent of the population under the age of 30, there is a pressing need to pivot toward the non-oil private enterprises, rather than relying solely on the public sector, as the primary driver of sustainable job creation and heightened total factor productivity growth,” founder, president and chief economist at Nasser Saidi & Associates, Nasser Saidi, emphasized.

“Expansionary readings of the Saudi PMI for March 2024 echo the resilience and resurgence of the private sector following the challenges posed by the COVID-19 pandemic,” he told Al Arabiya English. “The spike in demand has spurred a flurry of new orders and clientele, with export orders rebounding notably after a period of subdued activity. Noteworthy is the observed rise in employment alongside mild wage pressures, positioned to bolster the financial standing of firms and listed companies, thereby fortifying the overall health of the financial markets.”

“Saudi Arabia is progressing steadily toward achieving the ambitious objectives outlined in Vision 2030, buoyed by supportive public investments and comprehensive policy and legal reforms,” Saidi explained. “The Kingdom has pursued rapid diversification across three pivotal fronts: enhancing trade diversity to elevate non-oil trade share, boosting export value-added and expanding trade partnerships; pursuing government revenue diversification through VAT and other broad-based tax measures; and broadening production horizons to lessen reliance on oil-centric industries.”

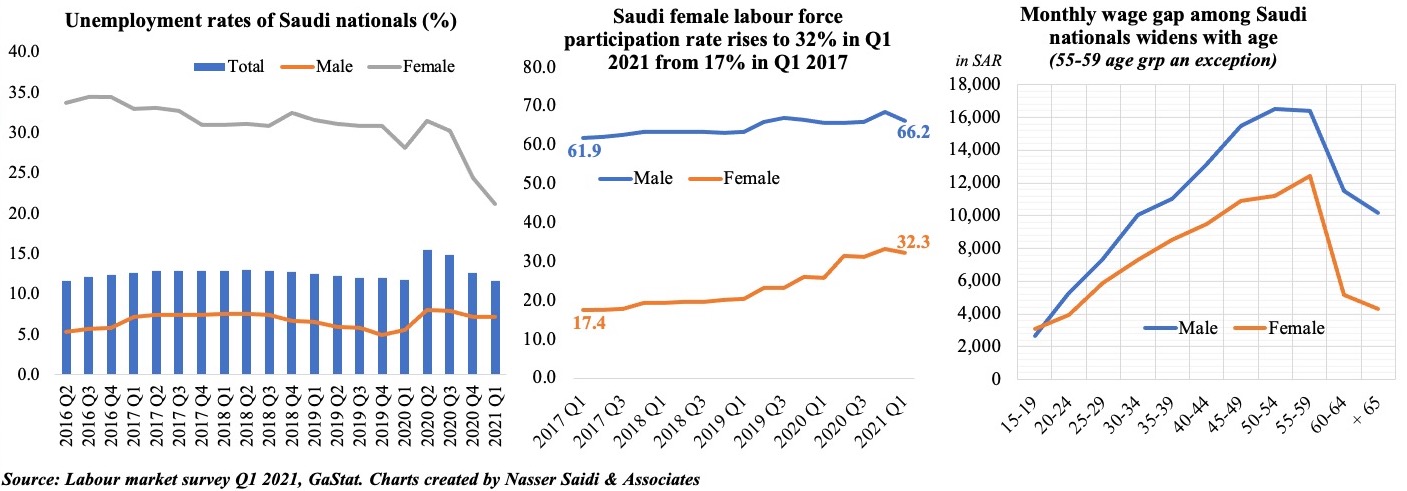

“A significant driver of this [GDP] growth, constituting 40 percent, is private consumption, fueled by the emergence of new sectors such as entertainment, hospitality and tourism,” Saidi mentioned. “Notably, social reforms have propelled a rise in female labor force participation rate, concurrently reducing the female unemployment rate to a historic low of 13.7 percent in Q4 2023. This shift towards dual-income households has not only elevated household income but has also facilitated increased consumption rates and wealth accumulation.”

He added: “These developments have been instrumental in bolstering the services sector, including retail, and catalyzing the digital economy, with women playing important roles in both arenas.”

Among the various non-oil sectors experiencing growth in Saudi Arabia, Saidi believes that tourism has strong potential, given the country’s capacity to attract cultural, historical, and religious tourists.

He noted that “Saudi Arabia made an exceptional achievement of hosting 27 million foreign tourists and 77 million domestic visitors in 2023, meeting previous targets set for 2030.”

“Strategic initiatives such as the development of resorts along the Red Sea and hosting major events like gaming conferences and concerts, coupled with facilitative measures like the unified GCC tourist visa and the upcoming Expo 2030, are projected to fortify tourism prospects,” Saidi stressed.

“Services-related industries such as financial services, wholesale and retail trade, restaurants, hotels, as well as transport and logistics, are expected to lead the upswing,” Saidi emphasized. “These sectors are anticipated to experience rapid development, reflecting a buoyant economic landscape. However, challenges may arise in the construction sector due to disruptions in Red Sea shipping, leading to increased costs of construction inputs and potential cost overruns.”

Saidi suggested a positive near-term outlook driven by several key factors. Those include the pipeline of Mega and Giga projects, preparations for Expo 2030 and the World Cup 2034, and the ongoing regional headquarters project, where licenses are being issued at a remarkable rate of ten per week.

“The Public Investment Fund’s domestic investments in new and emerging sectors are also expected to provide crucial support to non-oil activity, further fueling economic growth.”