Radio interview with Dubai Eye’s Business Breakfast on UAE’s Ministry of Foreign Trade & Economic Outlook, 23 Jun 2025

Dr. Nasser Saidi spoke with Dubai Eye’s Business Breakfast team on 23rd June 2025 about the UAE adding a Ministry of Foreign Trade, if there would be any competition with SaudiArabia for tourism & also the outlook for economic growth in the UAE.

Listen to the full radio interview at the link below (from 5:48 to 12:26):

Transcript below:

Dr. Saidi, good morning.

Good morning to you.

Dr. Saidi, a quick word first of all on the evolving situation in the region. I don’t want to get drawn on political or security speculation, but a quick word on the economics, if you will.

You mentioned the energy sector, and oil prices have risen a little bit. What’s surprising actually is that they haven’t risen any more. So the anticipation and expectation in the markets is that most of it is already done and we can continue.

So probably the impact will be less tourism for a few weeks, but it will come back to normal. That’s what the markets seem to be saying.

Dr. Saidi, thank you very much indeed for that. Now, the reason we’ve asked you to come on was to talk about some significant changes here in the UAE announced over the past 72 hours or so. We have a new ministry here in the UAE, a Ministry of Trade for the first time.

“Not a new minister though, Dr. Thani El-Zayoudi has been heading up trade for the UAE for some time now. First of all, your reaction to the new Ministry of Trade.

I think the important thing is that it’s a strategic signalling and positioning. At a time where the rest of the world is talking about greater protectionism, tariffs, tromponomics and the rest, the UAE is saying, I’m creating this trade ministry, foreign trade ministry, and I want to open up to the rest of the world. So the strategic positioning is extremely important from that point of view.

The other thing that’s important is that we need to remember that trade policy is a major tool of economic diversification.

In terms of the work that Dr. Al-Zayidi has done already with the SEPA trade deals, now we get quite excited about them in the Business Breakfast Studio and we see the impact that things like the SEPA deal with India, for example, have had over the past three years. But what’s your objective assessment as an economist?

“The first point to note is that the UAE is now the most diversified economy in the GCC. Seventy-five percent of output is now non-trade. And if you look at India in particular, this was one of our biggest trade partners apart from China.

And opening up, and what Dr. Zayidi has done, is that you’re opening up not only to your existing trade partners, but you’re lowering barriers across the board. So amazing achievements over a short space of time. 24 SIPAs, you’re going to reach easily 1.1 trillion dollars worth of trade way before 2031.

So I think very much to the credit of the Minister.

The other change that we’ve had, not quite as significant, is the Ministry of Economy. Now that’s an existing ministry. It is now the Ministry of Economy and also Tourism.

Why the need to do that, do you think?

Well, because tourism, because first, services have become much more important for the UAE. Tourism, trade, commerce, all the rest, wholesale and retail trade are a major fraction of the economy. So focusing on tourism is also saying, I’m going to become a global hub for tourism.

“And UAE is well on its way. And importantly, I think transport and logistics, your airports, ports and facilities really make it much easier. It’s one of the easiest places to get into.

We do have, of course, emerging competition here in the UAE as a tourism hub for the Gulf region and that is in Saudi Arabia. Embryonic stages yet, but their ambitions are significant. How seriously should the UAE take Saudi Arabia as a tourism competitor?

I think they’re largely complimentary. UAE is way ahead in terms of being integrated into global tourism. Saudi has obvious strengths in terms of religious tourism, environmental tourism, et cetera.

But I think they will complement each other. What Saudi and the UAE have done over the past few years is grow their soft power. Look at their hosting of international events, World Cups, et cetera, exhibitions and all the rest.”

“And what you have is greater integration of transport services, air, road and rail. That will mean that you’ll open up the whole market of the GCC. So I’m very positive in terms of the complementarity of the two.

And why not? If there is competition, so be it. It will mean lower prices and more attractive to tourists from across the world.

We just had a message in. Someone’s correcting me, Dr. Saeedi. Aruba has written in saying, it’s not the first time there’s been a Ministry of Foreign Trade in the UAE.

Aruba’s memory is strong. Back in 2010, she said, Her Excellency Lubna Al Qasimi was Minister of Foreign Trade.

Yes, that’s true. That’s true.

Thank you, Aruba, for pointing that one out. That is a good memory. Finally, Dr. Saeedi, it’s almost time for the half-time report for the UAE economy in 2025, June the 23rd, almost at the end of the first half.

Most of the reports we’re reading, World Bank, IMF, points to 4 or 5% growth for the UAE economy this year. What’s your reading?

“I think the readings will be correct. We’ll have a slowdown probably in the second quarter. It’ll pick up rapidly in the third and fourth quarter.

I’m pointing to the fact that digital economy is rapidly growing, clean energy, clean technology are rapidly growing. So all the tech sectors are really going to be a major factor of growth. Take fintech, for example.

We’ve become a global hub of fintech. So all of that, and I really want to focus on the tech sector because I think it’s really going to be an engine of growth and job creation, but more important, attracting foreign direct investment and people to come and live here. Look at the influx of people coming in for the golden visas, professional visas and all the rest.

So forget the traditional sectors, focus on the tech sectors because I think that’s where we’re going, e-commerce, digital trade and the like.

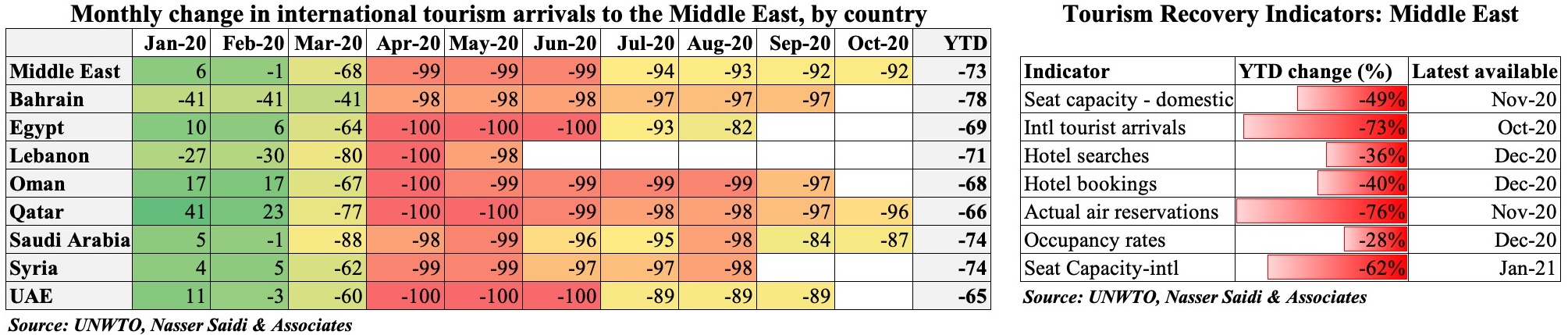

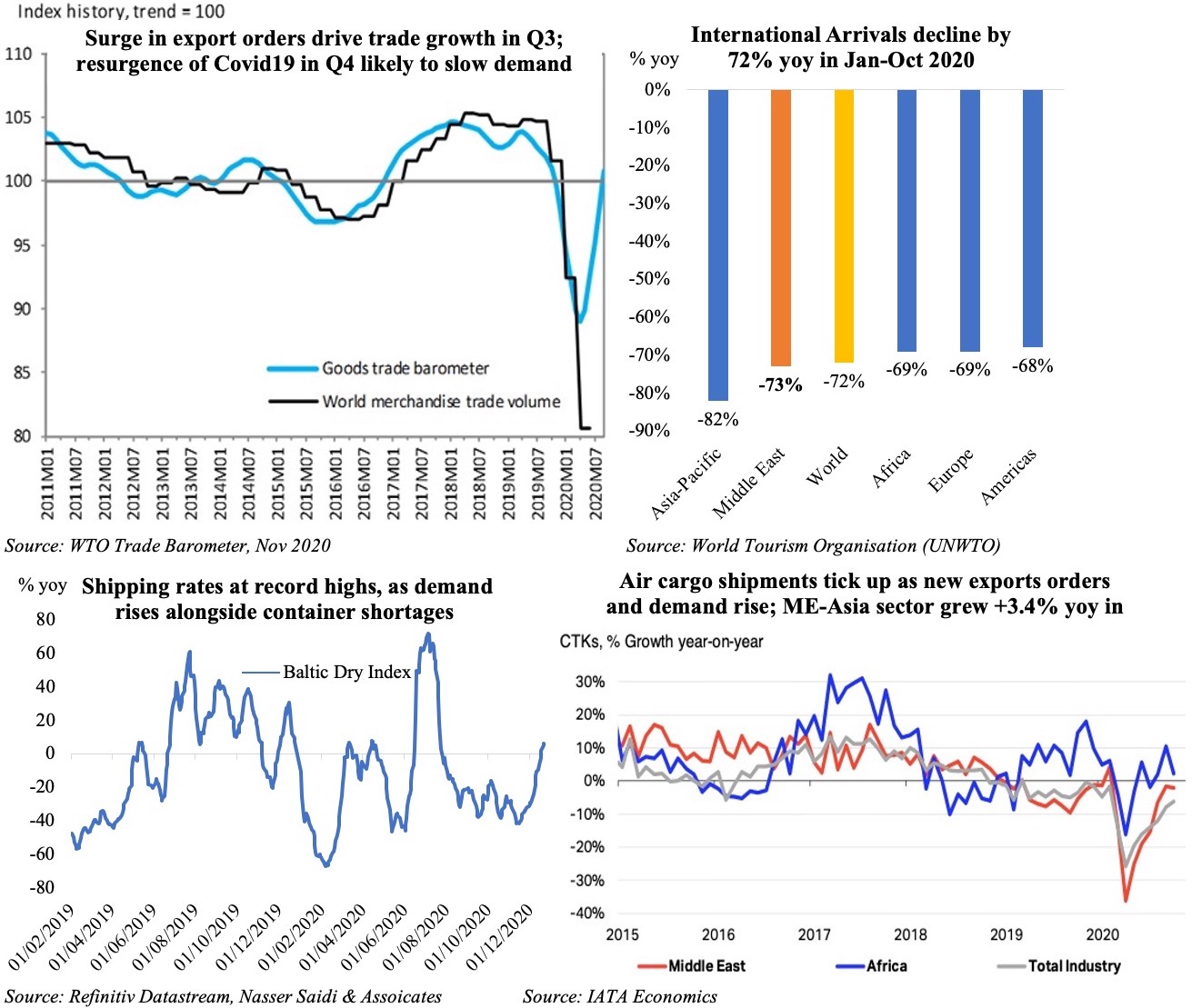

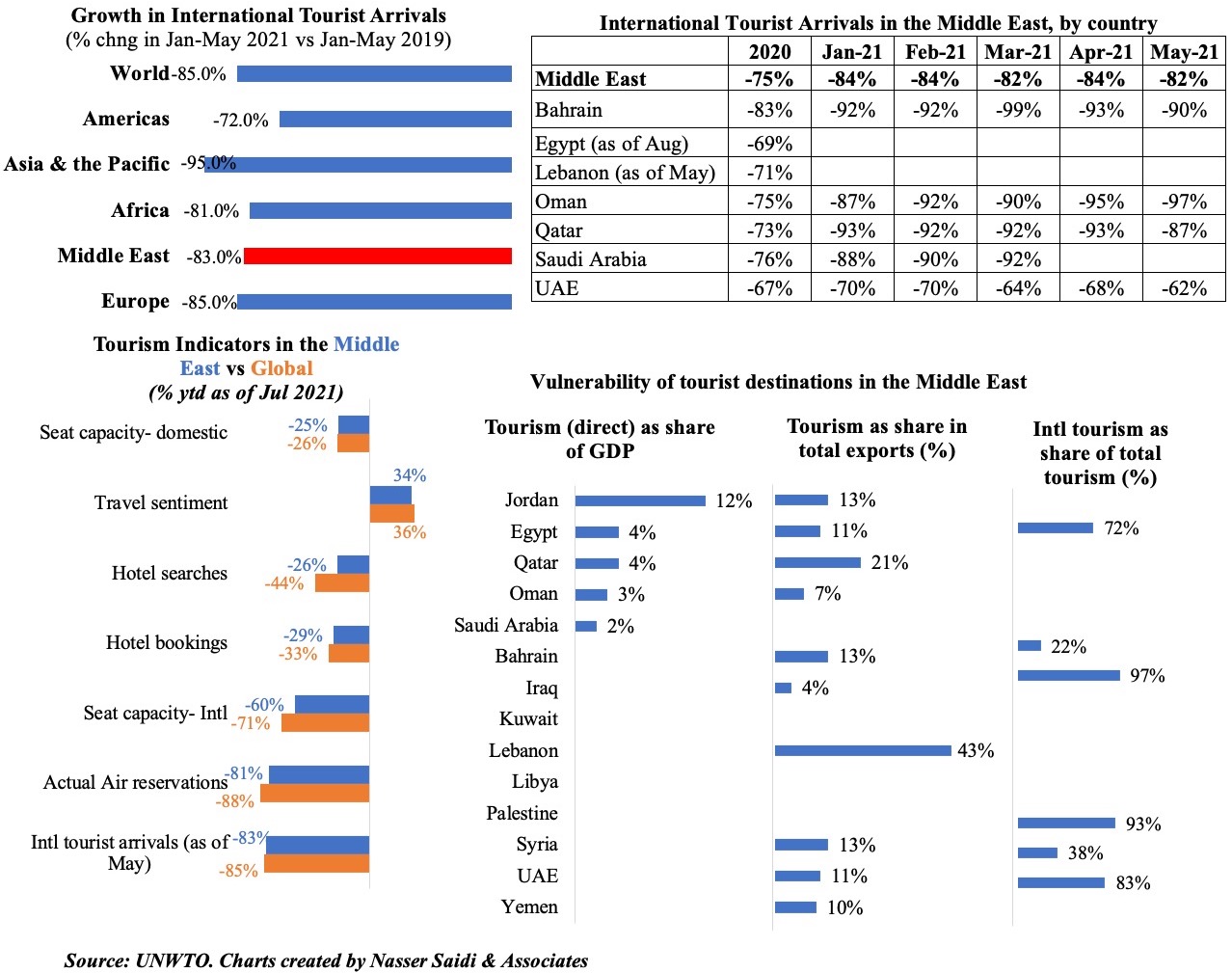

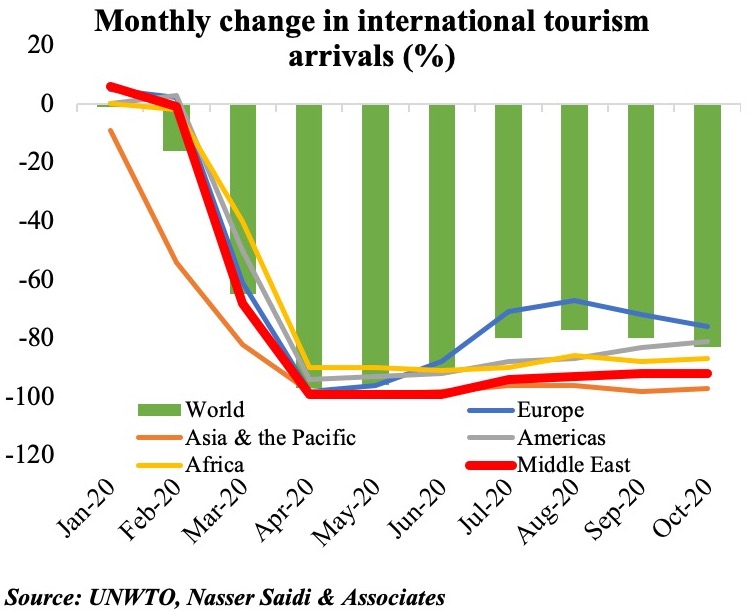

The UNWTO reported a 72% drop in international tourist arrivals during the Jan-Oct period, with the Middle East region continuing to lag its global counterparts in tourism arrivals (-73% year-to-date). International tourism as a share of total tourism is significantly high in Bahrain (97%) and UAE (83%), making these nations more vulnerable than say, Saudi Arabia, with its share at 26%. With air travel restrictions still in place in many nations, and hotels either closed or open at lower capacity, the road to recovery will be long.

The UNWTO reported a 72% drop in international tourist arrivals during the Jan-Oct period, with the Middle East region continuing to lag its global counterparts in tourism arrivals (-73% year-to-date). International tourism as a share of total tourism is significantly high in Bahrain (97%) and UAE (83%), making these nations more vulnerable than say, Saudi Arabia, with its share at 26%. With air travel restrictions still in place in many nations, and hotels either closed or open at lower capacity, the road to recovery will be long.