Comments on strikes on GCC energy infrastructure in The National, 7 Apr 2026

Dr. Nasser Saidi’s comments on strikes on GCC energy infrastructure appeared in an article in The National titled “Strikes on Gulf energy sites stoke global and regional stagflation fears” published on 7th April 2026.

The comments are posted below.

Facilities recently attacked include Kuwait’s Shuwaikh oil sector complex, which houses the oil ministry and Kuwait Petroleum Corporation headquarters, two power and water desalination plants in the country, a fuel storage facility run by Bahrain’s Bapco Energies, and the Borouge plant and Adnoc’s Hashan gas plant in the UAE. Many of them have reported significant damage, with assessments still underway.

“Hits to infrastructure will have more permanent effects on prices, the ability to recover energy supply and overall economic recovery; it is more likely to result in stagflation,” said Nasser Saidi, president of Nasser Saidi and Associates and former economy minister of Lebanon.

Stagflation refers to an economy facing a combination of slowing growth, rising unemployment and high prices (inflation).

When infrastructure is damaged or destroyed, it leads to reconstruction costs as well as the need to develop alternative lower war risk infrastructure such as new pipelines and transport routes. This in turn implies higher deficits and use of fiscal buffers, Mr Saidi said.

“Destruction of energy and related infrastructure (pipelines, ports, etc) implies a larger fiscal effect: lower revenue, higher deficit and build-up of debt, since capacity has been impaired or destroyed,” he said.

“The longer the strait remains inaccessible, the greater the impact on prices, supply chains, and the regional and global economy, given the critical role of energy in all activities,” Mr Saidi said. “This will feed into producer and consumer prices, resulting in macro-effects as economies and governments adjust.”

That could mean increased working from home and e-learning, shorter work weeks, reduced travel and a hit to transport and logistics, among other things.

The hit to power and desalination plants could also lead to socio-economic and environmental effects, particularly in Gulf countries such as Bahrain, Qatar and Kuwait, Mr Saidi said.

“This can become existential and depends on the degree of dependence on desalinated water for consumption and production.”

Mr Saidi said the economic and financial impact will depend on the reaction and effects on the private sector and how quickly confidence can be re-established.

“The latter will depend on how proactive governments (via fiscal, subsidies, industrial policies) and central banks (through monetary policies) are to counter the negative effects of damage to infrastructure,” he said.

For the Gulf states, an important stabilising role can be played by state-owned enterprises and government-related entities, given that they dominate sectors such as power, water and transport, as well as by sovereign wealth funds, according to Mr Saidi. “We need a strategy reset,” he added.

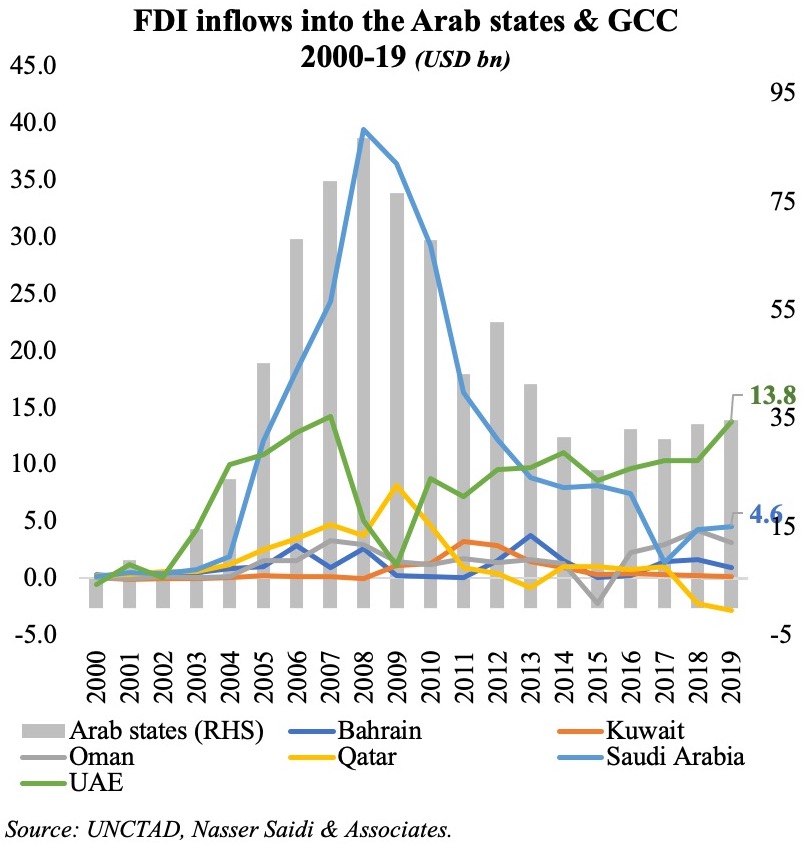

We focus on FDI in this Weekly Insight piece. FDI inflows are essential to the UAE’s diversification efforts, as it would not only create jobs, raise productivity and growth, but could also lead to transfer of technology/ technical know-how and promote competition in the market. According to the IMF, closing FDI gaps in the GCC could raise real non-oil GDP per capita growth by as much as 1 percentage point.

We focus on FDI in this Weekly Insight piece. FDI inflows are essential to the UAE’s diversification efforts, as it would not only create jobs, raise productivity and growth, but could also lead to transfer of technology/ technical know-how and promote competition in the market. According to the IMF, closing FDI gaps in the GCC could raise real non-oil GDP per capita growth by as much as 1 percentage point.

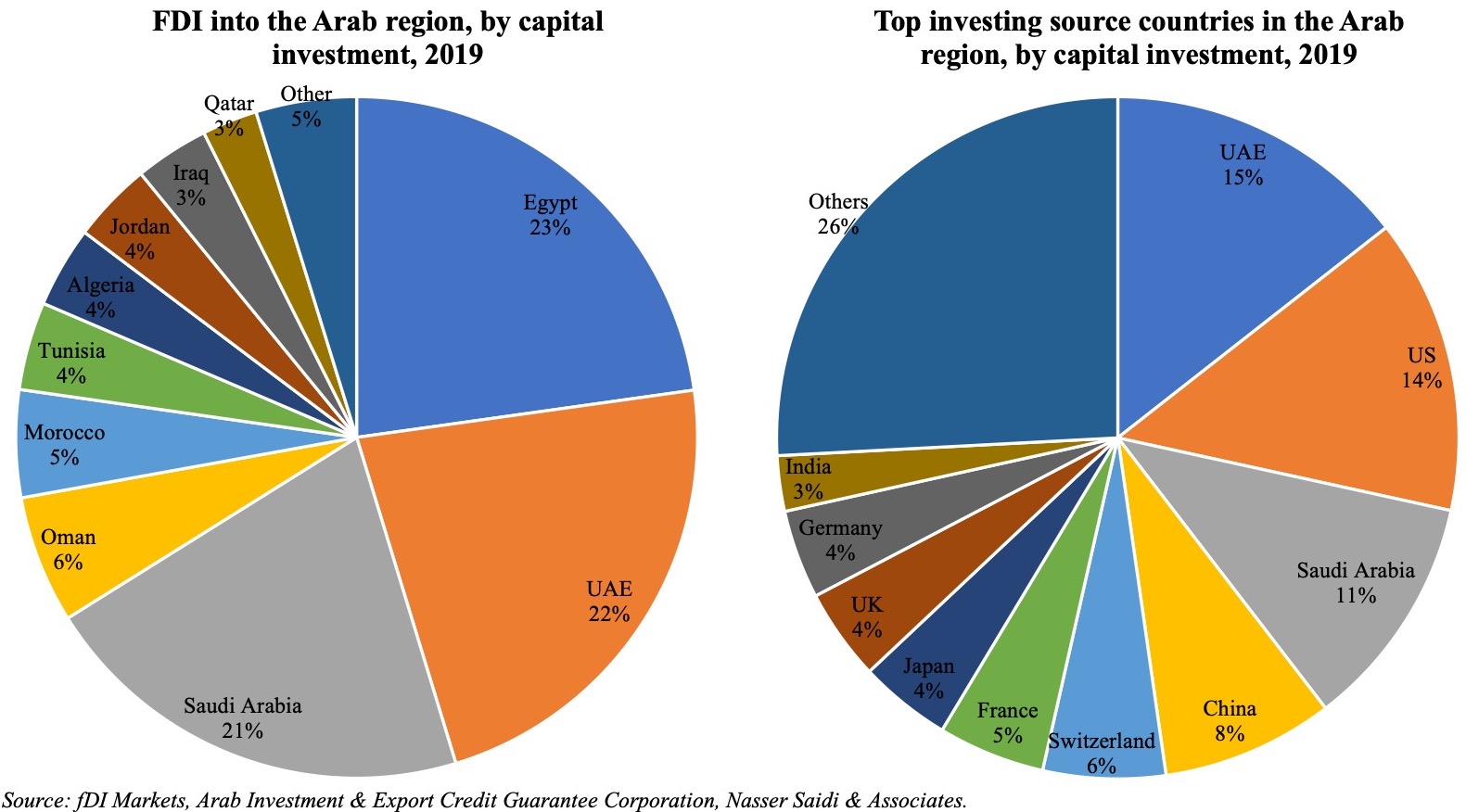

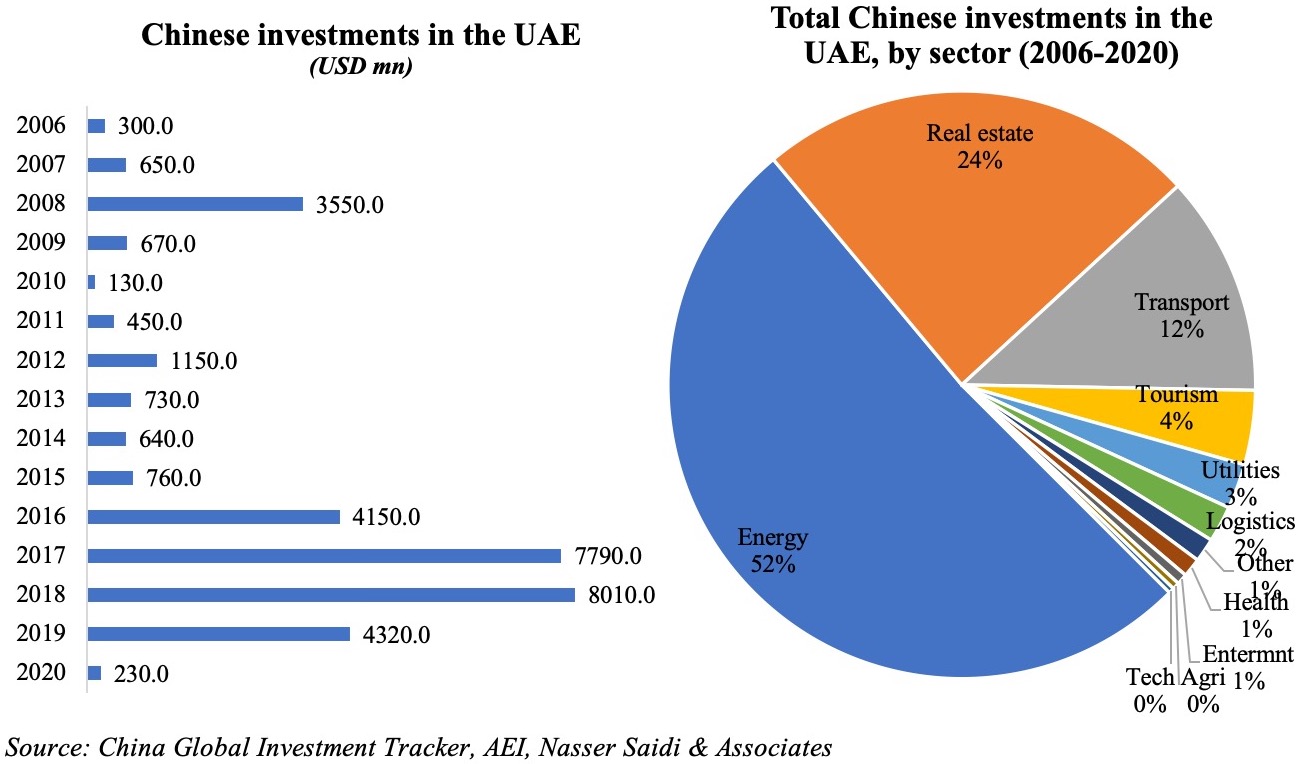

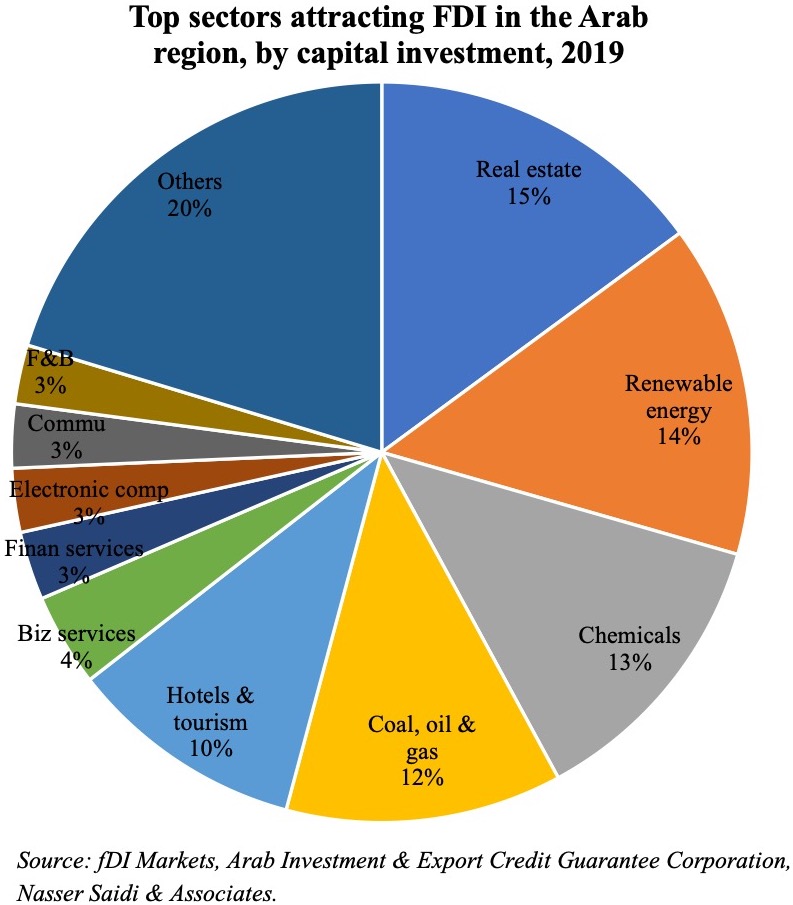

hinese projects tracked during Jan 2003-Mar 2020 (with the number of projects in double-digits in 2018 and 2019). According to AEI’s China Global Investment Tracker, the value of Chinese investments touched a high of USD 8bn in 2018, thanks to a handful of large projects (including with ACWA Power and Abu Dhabi Oil). Sector-wise, investments were concentrated in energy (both oil and gas as well as renewables), real estate and transport – together accounting for 87.8% of total investments during 2016-2020. This is largely in line with FDI inflows into the Arab region as well, with the top 5 sectors (real estate, renewables, chemicals, oil & gas and travel & tourism) accounting for close to two-thirds of total inflows in 2019.

hinese projects tracked during Jan 2003-Mar 2020 (with the number of projects in double-digits in 2018 and 2019). According to AEI’s China Global Investment Tracker, the value of Chinese investments touched a high of USD 8bn in 2018, thanks to a handful of large projects (including with ACWA Power and Abu Dhabi Oil). Sector-wise, investments were concentrated in energy (both oil and gas as well as renewables), real estate and transport – together accounting for 87.8% of total investments during 2016-2020. This is largely in line with FDI inflows into the Arab region as well, with the top 5 sectors (real estate, renewables, chemicals, oil & gas and travel & tourism) accounting for close to two-thirds of total inflows in 2019.