The other challenge is whether the banking system has sufficient liquidity to make repayments to depositors. “The short answer is ‘no’,” said Nasser Saidi, a former economy minister and deputy governor of Lebanon’s central bank. He said it was impossible to know if banks had sufficient liquidity without a forensic audit of the lenders and the BDL.

Additionally, the draft law promises to create future liabilities without clearly specifying how these will be financed. “There is a great deal of vagueness and opaqueness in the draft law. There is uncertainty: who does what, who assesses the amount of losses, who administers etc, which opens the process to potential litigation and legal uncertainty,” Mr Saidi said.

A major issue with the draft law is that it does not add new liquidity into the banking system, but rather focuses on the balance sheets of the commercial banks and the BDL. “This is a flawed static approach. You need both solvency and liquidity and long-term sustainability requiring a dynamic analysis,” said Mr Saidi.

New capital and financial resources will need to be injected in the banks to provide credit and finance to stabilise and restore economic growth.

“This is not a zero-sum game,” he added. “The risk is that absent resolution of uncertainties, the restructuring process will end up being a failed, negative-sum game – a situation in which the total losses of all participants exceed the total gains, resulting in a net loss for everyone involved, that will not restore trust to revive a cash-based, informal economy.”

Dr. Nasser Saidi’s interview “Can Beirut’s New Reform Agenda Save the Pound?” on “You’re In Business” with Yousef Gamal El-Din, 13 May 2025

Dr. Nasser Saidi’s interview with Yousef Gamal El-Din titled “Can Beirut’s New Reform Agenda Save the Pound?” was aired on the “You’re In Business” show. The episode is published on YouTube, Spotify and Apple Podcasts

The video is available below:

“Lebanon at a crossroads: Reform or decay ahead?”, Oped in The National, 9 Apr 2025

“Lebanon at a crossroads: Reform or decay ahead?”, Oped in The National

Nasser Saidi

Lebanon is in its sixth year of a protracted financial and liquidity crisis, facing security challenges on its borders with Israel and Syria, but appears to be on the cusp of recovery.

The country is battling several economic challenges – a plunge in gross domestic product per capita by about 40 per cent, a zombie banking sector, a highly dollarised, increasingly informal, cash-based economy, high multidimensional poverty and unemployment levels, increased inequality, plunge in its currency’s value by 97 per cent, high inflationary pressures (an average of 127 per cent over the past five years) and a collapse of public finances.

The new pro-reform president and prime minister along with a cabinet that has parliament’s backing inspires confidence and appears committed to long-delayed economic reforms. Stability and recovery will require political and judicial reforms, along with institutional and structural reforms to ensure the rule of law and accountability, allowing the country to emerge from the heavy legacy of failed policies. Whether the incumbent parliament will enable the deep reforms given municipal and parliamentary elections in 2025 and 2026 respectively, adds uncertainty.

A new governor of the central bank has been appointed. Reforms are required to re-establish trust in the banking and financial sector and convince the world to risk investing in its recovery and reconstruction.

The first step should be to restructure the Banque du Liban (BDL) and its governance, appoint a new team of vice governors, restrict the powers of the governor to prevent past abuses, ensure public reporting, monitoring and accountability.

This is a unique opportunity to have a new reform-minded, effective BDL for the next six years. Given the severe monetary and real shocks Lebanon faces and the legacy of failed policies, the policy agenda should include:

Reset monetary policy to target inflation, with a unified, floating exchange rate, shifting away from the “financial engineering” that supported a disastrous fixed rate policy.

Institutional reform requires that the Banking Control Commission (BCC), Capital Market Authority and Special investigations Committee (SIC) be legally independent from the BDL, given their distinct mandates and responsibilities, along with the appointment of new boards.

The BDL should not provide any fiscal or quasi-fiscal (such as subsidies) financing. Public debt management should be the responsibility of an independent public debt management office to ensure transparency, disclosure of all public liabilities and debt sustainability.

The new governors must undertake a comprehensive forensic audit of the BDL, in an effort to underscore accountability for the banking collapse.

An independent Bank Resolution Authority (BRA) should be established – similar to what many countries set up following the 2008 global financial crisis – with a mandate to recapitalise and restructure the banking system. Bank restructuring should not reside with the BDL and BCC whose irresponsible governance led to the collapse of the banking system. The BRA should arrange for a forensic audit of the banks, while also imposing a recapitalisation – some $10 billion to $15 billion is required – a mergers and acquisitions (M&A) programme and a partial bail-in of large depositors, as part of the restructuring process. Banks have more than $86 billion in frozen deposits, largely inaccessible since 2019. Depositors with less than $200,000 represent 94 per cent of accounts and 30 per cent of the value of frozen deposits, while 70 per cent of deposits, valued at $65.5 billion, are concentrated in 87,000 accounts.

BDL assets, which include Middle East Airlines, Casino and Intra, should be audited and divested into a new, independent National Wealth Fund (NWF) – managed like Temsek in Singapore. The BDL could receive participation shares in the NWF. The NWF would restructure and manage public commercial assets for the national benefit and also manage any future oil and gas revenue.

Lebanon’s Parliament should vote to abolish its banking secrecy law or or adopt a Swiss-style system. This along with an effective SIC to enforce international anti-money laundering and counter-terrorism financing standards and an effective anti-corruption drive are critical to remove Lebanon from the Financial Action Task Force (FATF) grey list. This should be complemented by a Stolen Asset Recovery (STAR) programme to help address anti-corruption, money laundering and recover stolen assets.

Lebanon requires huge amounts – some $15 billion to $20 billion – for reconstruction and it does not have the resources. It should set up an independent reconstruction fund, with full transparency, disclosure, auditing and reporting, to ensure Lebanon is accountable for the funding of reconstruction. Donors and aid givers should be allowed to undertake reconstruction projects within an agreed plan.

Lebanon should rapidly negotiate and implement a new agreement with the International Monetary Fund based on comprehensive economic and financial reforms under five pillars – restructuring the financial sector; fiscal reforms; reforms of state-owned enterprises; strengthening governance; a credible, transparent monetary and exchange rate system. The IMF agreement and international support, mainly from the GCC, are imperativebut will be conditional on undertaking a comprehensive set of deep governance, economic, monetary, fiscal and structural reforms.

This is a moment of opportunity to undertake multipronged reforms to revive confidence and economic activity, attract back human capital, improve long-term growth prospects, and strengthen and restore linkages with the GCC. Lebanon faces reform or continued decay.

Nasser Saidi is a former economy minister and deputy governor of Lebanon’s central bank

Comments on “Can Lebanon’s new central bank governor break the cycle of economic crisis?” in Arab News, 31 Mar 2025

Echoing the prime minister’s apprehensions is Nasser Saidi, a former Lebanese economy minister and central bank vice governor, who raised concerns about the selection process for the new central bank chief, warning that powerful interest groups may have too much influence.

He told the Financial Times that the decision carried serious consequences for Lebanon’s economic future, saying that one of Souaid’s biggest challenges will be convincing the world to trust the nation’s banking system enough to risk investing in its recovery.

“The stakes are too high: You cannot have the same people responsible for the biggest crisis Lebanon has ever been through also trying to restructure the banking sector,” said Saidi, who served as first vice governor of the Banque du Liban for two consecutive terms.

“How are we going to convince the rest of the world that it can trust Lebanon’s banking system, and provide the country with the funding it needs to rebuild (after the war)?”

Lebanese economist Saidi said that the IMF “quite correctly and wisely” demanded comprehensive economic reforms.

In a March 14 interview with BBC’s “World Business Report,” he said that the government must address fiscal and debt sustainability, restructure public debt, and overhaul the banking and financial sector.

But hurdles remain. Saidi added that while Lebanon “has a government today that I think is willing to undertake reforms, that does not mean that parliament will go along.”

Lebanon also needs political and judicial reform, including an “independent judiciary,” he added.

Nevertheless, Saidi told the BBC that Lebanon, for the first time, has “a team that inspires confidence” and has formed a cabinet that secured parliament’s backing. Despite this positive step, Lebanon must still address structural failures in its public institutions, rooted in decades of opacity, fragmented authority and weak accountability.

Saidi highlighted the broader challenges Lebanon faces, cautioning that without financing for reconstruction, achieving socioeconomic and political stability will remain elusive.

“If you don’t have financing for reconstruction, you’re not going to have socioeconomic stability, let alone political stability,” he said.

“There has to be a willingness by all parties to go along with the reforms,” he added, highlighting that this is where external support is crucial, particularly from Saudi Arabia, the UAE, France, Europe and the US. Saidi said that support must go beyond helping bring the new government to power — it must include assistance, especially in terms of security.

“Lebanon’s journey to renewal starts now”, Op-ed in Arabian Gulf Business Insight (AGBI), 20 Jan 2025

Hope and optimism follow the arrival of a new prime minister and president

The nomination of Nawaf Salam as Lebanon’s prime minister under President Joseph Aoun, following more than two years of political vacuum, marks a turning point for the country.

This moment has the potential to be as transformative as the 1989 Taif agreement, which ended the civil war and restored political stability.

A major factor behind the developments in Lebanon is the significant shift in regional dynamics. This has been driven by the war in Gaza, the collapse of the Assad regime in Syria, the severe degradation of Hezbollah’s capabilities and the apparent collapse of Iran’s “axis of resistance”.

Together, these events have created a powerful impetus for change.

For the leading powers in the GCC – Saudi Arabia and the UAE – this moment provides an opportunity to displace Iran from Lebanon, Iraq and Syria while reasserting their own influence. Both regional and international stakeholders share an interest in promoting stability.

Lebanon’s political landscape has been historically paralysed by internal fragmentation. Now, at last, the country’s political class, plagued by a lack of credibility, incompetence and failure to address Lebanon’s many crises or implement long-overdue reforms, is passing on the baton.

But Salam and Aoun inherit a heavy legacy.

Since the Arab Spring in 2011, Lebanon has battled stalled institutional reforms, unsustainable fiscal and monetary policies and overvalued exchange rates. These factors contributed to significant deficits in the government budget and current account, along with massive debt accumulation.

The country’s central bank, the Banque du Liban, allegedly ran a Ponzi scheme for many years during the tenure of Riad Salameh, who was its governor for three decades. He has denied all wrongdoing and the notion that the bank was operating a Ponzi scheme.

The bank’s activities contributed significantly to Lebanon’s economic collapse, depleting international reserves, sparking a 99 percent depreciation of the exchange rate, hyperinflation, a collapse of the banking system and one of the deepest financial crises in the country’s history.

Central bank losses exceeded 200 percent of GDP. Lebanon became a cash – and increasingly dollarised – economy. The polycrisis (economic, monetary and financial, institutional, security, political and governance), along with the Beirut Port explosion and the Israel-Hezbollah war, turned Lebanon from a fragile state into a failed one.

Despite the long road ahead for Aoun and Salam, we have reasons for optimism.

The president’s inaugural speech encapsulated much promise for a new Lebanon. There were strong messages on political reform, rebuilding the state and its institutions, focusing on judicial and administrative reform, the rule of law, accountability and fighting endemic corruption.

Institutional and judicial reform will be complemented by a national anti-corruption drive and transparency initiatives while demanding accountability for multiple crises and destruction.

President Aoun’s political vision mirrors that of former President Fouad Chehab (1958-1964), who introduced reforms and built state institutions. With extensive military and security experience, President Aoun is adept at establishing domestic and external national security.

A packed agenda starts with forming a reform-centric, cohesive, competent and effective cabinet. The critical portfolios are justice, foreign affairs, defence and internal affairs, as well as finance.

With the Israel-Lebanon ceasefire agreement set to expire on January 26, the immediate need is to negotiate a permanent ceasefire to restore internal security and stability and enable the return of the displaced to the south, Bekaa and other areas.

Macroeconomic stabilisation and growth require fiscal consolidation and tax reform, modernising and digitising all government functions, administrative reform (over half of director-level posts are vacant), downsizing the bloated public sector, restructuring and effecting good governance of the state-owned enterprises (SOEs) responsible for public services.

An independent National Wealth Fund should be established to professionally manage all SOEs, commercial public assets and future oil and gas revenues.

Credible monetary reform requires a strong, professional and politically independent central bank. Monetary policy should be directed at controlling inflation and accompanied by a flexible exchange rate regime.

Additionally, a comprehensive overhaul of Banque du Liban’s governance structure is necessary to implement meaningful change and restore confidence.

To make the BDL accountable, a new governor (and deputy governors by June 2025) and radical changes to governance are required. The Banking Control Commission of Lebanon, the Special Investigation Commission and the Capital Markets Authority should also be independently governed institutions.

Furthermore, an independent Bank Resolution Authority must restructure the banking system based on recapitalisation (starting with existing shareholders), mergers and acquisitions, and bail-ins of large depositors to maximise deposit recovery.

The implementation of political reforms, a comprehensive restructuring agenda, and institutional and structural changes will pave the way for a revised International Monetary Fund programme and renewed engagement with the GCC.

These efforts can support Lebanon’s reintegration into the Arab world, facilitate funding for redevelopment and address substantial reconstruction needs, estimated at approximately $25 billion.

In essence, this is a historic opportunity for Lebanon, the GCC and the wider region.

Dr Nasser Saidi is the president of Nasser Saidi and Associates. He was formerly chief economist and head of external relations at the DIFC Authority, Lebanon’s economy minister and a vice governor of the Central Bank of Lebanon

“Time to address Lebanon’s crippling banking crisis”, guest article for Arab Banker, Autumn 2024

Lebanon has been mired in economic crisis for almost five years. A combination of acute negligence and mismanagement on the part of the government, the central bank and key institutions culminated in a series of economic and political crises that have left the banking sector on its knees and more than three-quarters of the population living in poverty.

In the guest article for Arab Banker,Dr. Nasser Saidi, founder and president of Nasser Saidi & Associates, and Alia Moubayed, emerging markets economist, analyse how the crisis unfolded and chart a proposed roadmap to recovery.

“To restore the Lebanon central bank’s credibility, independence is key”, Op-ed in The National, 15 Aug 2023

To restore the Lebanon central bank’s credibility, independence is key

Nasser Saidi

Lebanon is now dealing with the greatest financial crisis in history, the heavy legacy of Riad Salameh, the former governor of Banque du Liban. The new governor, Wassim Mansouri, has pledged that the central bank “must completely stop financing the government outside of a legal framework”, calling for a state financing law to be passed by Parliament.

This is unnecessary and a dangerous precedent that previous governors like Edmond Naim rejected. The Money and Credit Code, or MCC – Lebanon’s banking law – provides a wide measure of independence to the BDL with specific and strict conditions on financing government. The MCC legal strictures were violated, including the operating principle that the central bank does not grant credits to government and the public sector (MCC Article 90). How was this done?

The BDL financed unsustainable budget deficits (averaging 8.4 per cent of gross domestic product between 2014 and 2019) and monetised public debt, attempting to reduce the growing burden of interest payments. Wasteful government spending includes subsidising electricity generation by Electricite du Liban, which touched $1.8 billion in 2018, or 3.1 per cent of GDP. This was the biggest drain on public finances, while the company provided about three hours of electricity a day. Public debt mushroomed from 139 per cent of GDP in 2014 to 172 per cent in 2019. This accelerated to 282.3 per cent in 2022, while current account deficits widened from 26.2 per cent to 28.5 per cent of GDP between 2014 and 2019.

The BDL expanded its public sector financing through providing preferential funding at subsidised rates for housing and real estate, education, tourism, innovation and SMEs. This amounted to quasi-fiscal spending: BDL financed activities that should have been government budget financed under parliamentary scrutiny. The BDL expanded quasi-fiscal spending without public disclosure or transparency as to amounts and beneficiaries. This resulted in an absence of accountability, growing clientelism and the financing of activities at the behest of politicians and their cronies, widening the web of corruption.

Marketed under the heading of “financial engineering”, the BDL bailed out the banking system in 2015 to the tune of $5.3 billion (about 12.5 per cent of GDP) without approval from the BDL’s governing council, government or Parliament. The BDL financing was a costly and vain attempt to offset the effects of its failing exchange rate policy and overvalued parity. But the BDL financing was convenient for successive governments since they did not have to foot the bill and raise taxes.

More generally, the increasingly higher interest rates that the BDL was paying to attract deposits from commercial banks and capital inflows to increase its foreign currency reserves and defend a highly overvalued fixed parity of the Lebanese pound led to a sharp contraction of credit to the private sector. The overvalued real exchange rate acted as a tax on exports and sucked in imports, leading to a growing current account deficit. Lebanon’s productive sectors were crowded out by the BDL’s fixed exchange rate policy, unable to get access to finance from the banking sector.

The stage for economic and financial collapse was set by the BDL’s financing of the twin current account and budget deficits. The BDL-Ponzi scheme burst, triggered by bank closures in October 2019, loss of confidence and a run on the banks. Eventually, the government defaulted on the March 2020 Eurobond. The government of Hassan Diab, the prime minister at the time, prepared a financial recovery plan that comprised fiscal, banking and structural reforms. This was sabotaged by the BDL and vested political and banking interests resisting reform and the required recapitalisation and restructuring of the banking sector.

Similarly, an IMF Staff Level Agreement from April 2022 remains stalled with no sign of willingness from Lebanon’s caretaker government and politicians to implement the required reforms agreed with the Fund. With government no longer able to tap domestic or foreign debt markets, increasing recourse was made to BDL financing by drawing down foreign currency assets (in effect, customer deposits that the banks had deposited at the BDL) and printing money. This led to a collapse of the exchange rate (98.5 per cent depreciation) and triple-digit inflation rates approaching hyperinflation (296 per cent in 2023), real GDP declining by 40 per cent and an increasingly informal (non-tax paying) cash-based economy, with a growing dollarisation of transactions. The net result of the BDL’s financing activities was accumulated losses exceeding $76 billion that were offset on the BDL’s balance sheet by creating fictitious “other assets”, as mentioned in the Alvarez & Marsal Forensic Audit report.

Mr Mansouri and the newly empowered governors of the BDL have the daunting task of resolving some of the institution’s legacy issues. They have proposed rebuilding trust via proposals including budget approval and enacting financial reforms (a capital control law by the end of August, as well as a financial capital restructuring law). The BDL needs to move to a floating exchange rate regime, shift away from distortion-creating and corruption-spreading multiple rates under the existing Sayrafa platform, to a single platform (for example Bloomberg or Reuters) and adopt a monetary policy targeting inflation.

To stop financing government, the MCC provides the power to the central bank, if it decides to do so, to lend to government under the conditionality it imposes. Such a conditional loan should be in Lebanese pounds to avoid further depletion of foreign currency “reserves” (now under $6.3 billion). This will force government to tap the local foreign exchange market if it needs to fund FX spending, thereby bearing the exchange rate depreciation effects of its FX borrowing. This would impose market discipline on the government, which has been absent under existing policy.

As part of the conditionality, the BDL should request that the government undertake a shock-therapy set of policies. Restoring confidence in the economy will stem from deep and comprehensive economic reforms. These should include restructuring the public debt and the banking system (including the BDL and its losses), governance reforms and the removal of subsidies by immediately phasing out transfers to non-performing, corruption-ridden national councils, state-owned enterprises and government-related entities.

There should also be a fiscal strategy to sustainably improve the state’s finances, by reducing the size of government and revenue mobilisation (for example, by broadening the tax base and improving the efficiency of tax administration) and rationalising spending by implementing public procurement reform. While credible financial restructuring tops the list of reforms needed, this must be supported by the institution of checks and balances, public accountability as well as transparency and disclosure.

Lebanon is paying the price of years of unsustainable, fixed exchange rate, fiscal and debt policies. Outrightly refusing to fund the government will instead force its hand to go to the IMF, with its funding (as well as any international aid and financing) dependent on implementing, not empty promises, but reforms. Otherwise, the BDL will lose any remaining credibility and, once again, revert to being a government financier, thereby risking a prolonged hyperinflationary period. Restoring credibility to the BDL requires its standing firm on its independence from government and Parliament, as well as forcing politicians to be held accountable for their inaction and irresponsible policies. Absent comprehensive reforms, Lebanon will continue its descent into its infernal abyss.

Comments in The Banker article “Lebanese Financial Crisis Drags On”, Jul 2022

Dr. Nasser Saidi comments on the ongoing economic and financial crisis in Lebanon appeared in the July 2022 edition of The Banker, in an article, titled “Lebanese Financial Crisis Drags On”.

“The roots of [the crisis] can be traced to years of large fiscal deficits (current wasteful spending without any build-up of infrastructure or real public assets), leading to a growing debt burden, [and] an increasingly overvalued Lebanese pound generating persistent current account deficits,” Nasser Saidi, Lebanon’s former minister of economy and trade and a former BdL vice-governor, told The Banker.

“Malgovernance, endemic corruption, incompetence, failed policies and dysfunctional politics have tipped Lebanon from being a fragile state into a failed state.”

While political paralysis prevented the passage of capital control laws at the beginning of the crisis, banks applied sporadic controls from early to late 2019, tightening them further as time went on. Yet the patchwork system of the initial restrictions “allowed politicians and cronies, bank shareholders and bankers, the ‘privileged and connected’ to transfer over $10bn at the expense of continued depletion of international reserves and destruction of confidence in the banking system,” Mr Saidi told The Banker.

Interview with CNBC Arabia on Lebanon’s recent banking, exchange rate developments & negotiations with IMF, 17 Jan 2022

Dr. Nasser Saidi was interviewed on the recent banking and exchange rate developments in Lebanon as well as the negotiations with IMF. The CNBC Arabia TV interview, aired on 17th of January 2022, was titled “في لبنان الأزمات تلد أزمات.. تبدأ بجفاف الدولار ولا تنتهي عند الظلام! ” can be viewed directly here.

لبنان.. وكأن هذا البلد على موعد مع الأزمات والرهان .. ومن كل شكل ولون!

فما أن يحتوي أزمة إلا وتظهر أخرى اكثر تعقيدا وظنون، حتى أصبح التفريق بينها صعباً وعسيراً مع تضاؤل الآمال في العثورعلى تأمين.

تتقاطع السياسة والاقتصاد وتتعثر الدروب والمعطيات، دولار غائب عن الحضور وكهرباء متقطعة ولا نور.

ديون متراكمة تنتظر الدور ومصارف لا تكفي المودعين والحضور، وليرة تتوارى وتراجع منظور.

وسلع في الأرفف إلا لمن استطاع، عصية على الوصول، وبلد غارق في أزماته ينتظر الفرج وتقديم حلول!

Interview with Asharq Business (Bloomberg) on Lebanon, 3 Dec 2020

Dr. Nasser Saidi joined Asharq Business (Bloomberg) on 3rd Dec 2020, to speak about the Lebanon, its need for reforms and the latest aid conference. Watch the interview (in Arabic) at this link.

"Overcoming Lebanon’s economic crisis", viewpoint in The Banker, Oct 2020

This article, titled “Overcoming Lebanon’s economic crisis”, appeared as a viewpoint in the Oct 2020 edition of The Banker. The article, posted below, can be directly accessed on The Banker’s website.

Overcoming Lebanon’s economic crisis

Lebanon’s financial and economic crises can only be solved with meaningful reform, without which it faces a lost decade of mass migration, social and political unrest and violence.

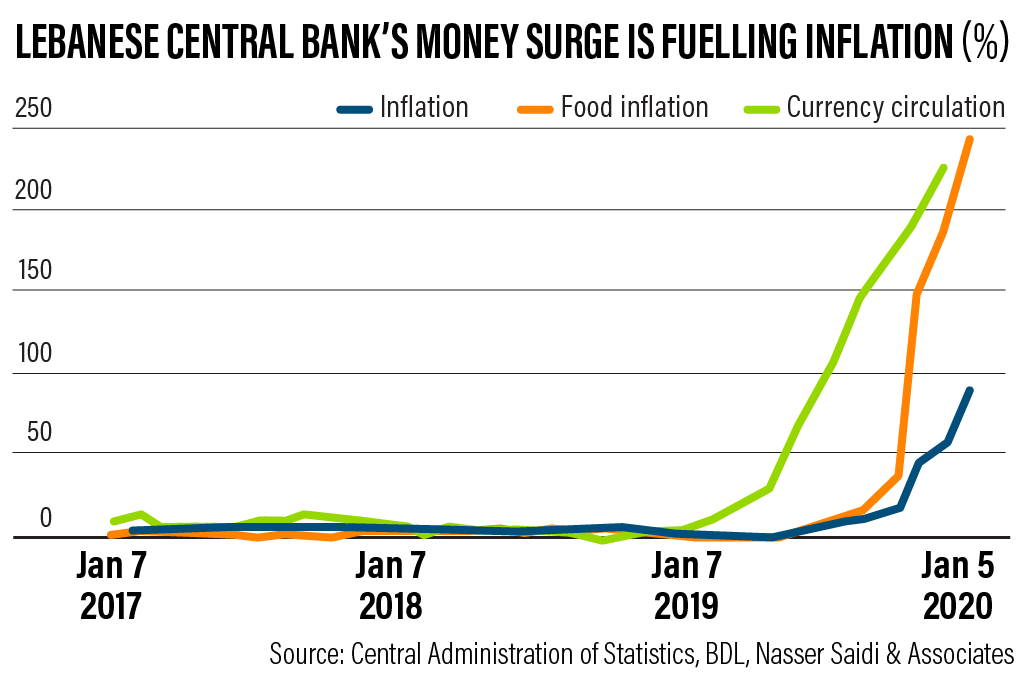

Violence and crises have shattered Lebanon’s pre-1975 Civil War standing as the banking and financial centre of the Middle East. Lebanon is engulfed in overlapping fiscal, debt, banking, currency and balance of payments crises, resulting in an economic depression and humanitarian crisis with poverty and food poverty affecting some 50% and 25% respectively of the population. The Lebanese Pound has depreciated by some 80% over the past year, with inflation running at 120% and heading to hyperinflation. A Covid-19 lockdown and the Port of Beirut horrendous explosion on August 4th created an apocalyptic landscape, aggravating the economic and unprecedented humanitarian crises. The cost of rebuilding is estimated to exceed $10 billion, more than 25% of current GDP, which Lebanon is incapable of financing.

The economic and financial meltdown is a culmination of unsustainable fiscal and monetary policies, combined with an overvalued fixed exchange rate. Persistently large budget deficits (averaging 8.6% of GDP over the past 10 years), structural budget rigidities, an eroding revenue base, wasteful subsidies, government procurement riddled with endemic corruption, all exacerbated fiscal imbalances.

Meanwhile, a monetary policy geared to protecting an increasingly overvalued exchange rate, led to growing trade and current account imbalances and increasingly higher interest rates to attract deposits and capital inflows to shore up dwindling international reserves. Deficits financed current spending, with limited real investment or buildup of real assets, while high real interest rates stifled investment and growth.

The unsustainable twin (current account and fiscal) deficits led to a rapid build-up of public debt. Public debt in 2020 is running at $111 bn, including $20 bn of debt at Banque du Liban (BdL), the country’s central bank. This figure represents more than 184% of GDP– the second highest ratio in the world behind Japan, according to the the IMF, Most of this debt is held by domestic banks and BdL, with 13% held by foreigners. Financing government spend

The BdL’s financing of government budget deficits, debt monetisation, large quasi-fiscal operations (such as subsidising real estate investment) and bank bailouts, created an organic link between the balance sheets of the government, the BdL and banks. In effect, depositors’ monies were used by the banks and the BdL to finance budget deficits, contravening Basel III rules and prudent risk management.

BdL policies led to a crowding-out of both the private and public sectors, and to disintermediation: the government could no longer tap markets, so BdL acted as financial intermediary i.e. paying high rates to the banking system, while allowing the government to borrow at lower rates. The higher rates increased the cost of servicing the public debt, with debt service representing some 50% of government revenue in 2019 and over one third of spending. Credit worthiness rapidly deteriorated, leading to a ‘sudden stop’ in 2019, with expatriate remittances and capital inflows moving into reverse.

The crisis Lebanon is now experiencing is the dramatic collapse of what economists describe as a Ponzi-like scheme engineered by the BdL, starting in 2016 with a massive bailout of the banks equivalent to about 12.6% of GDP. Ina bid to protect an overvalued LBP and finance the workings of government, the BdL started borrowing at ever higher interest rates, through so-called “financial engineering” schemes, which evolved into a vicious cycle of additional borrowing to pay maturing debt and debt service, until confidence evaporated and reserves were exhausted.

With the BdL unable to honour its foreign currency obligations, Lebanon defaulted on its March 2020 Eurobond and is seeking to restructure its domestic and foreign debt. The resulting losses of the BDL exceed $50 bn, equivalent to 2019 GDP, a historically unprecedented loss by any central bank.

With the core of the banking system, the BDL, unable to repay banks’ deposits, the banks froze payments to depositors. The banking and financial system imploded. The bubble burst in the last quarter of 2019, with a rapid depreciation of the LBP during 2020. The BDL’s costly attempt to defy the “impossible trinity” by simultaneously pursuing an independent monetary policy, with fixed exchange rates and free capital mobility resulted in growing imbalances, a collapse of the exchange rate and an unprecedented financial meltdown. Economic disaster

A series of policy errors triggered the banking and financial crisis, starting with the closure of banks in October 2019, ostensibly because of anti-government protests decrying government endemic corruption, incompetence and lack of reforms. A predictable run on banks ensued, followed by informal capital controls, foreign exchange licensing, freezing of deposits, inconvertibility of the LBP and payment restrictions to protect the dwindling reserves of the BDL. These errors precipitated the financial crisis, generating a sharp liquidity and credit squeeze, the sudden stop of remittances and the emergence of a system of multiple exchange rates.

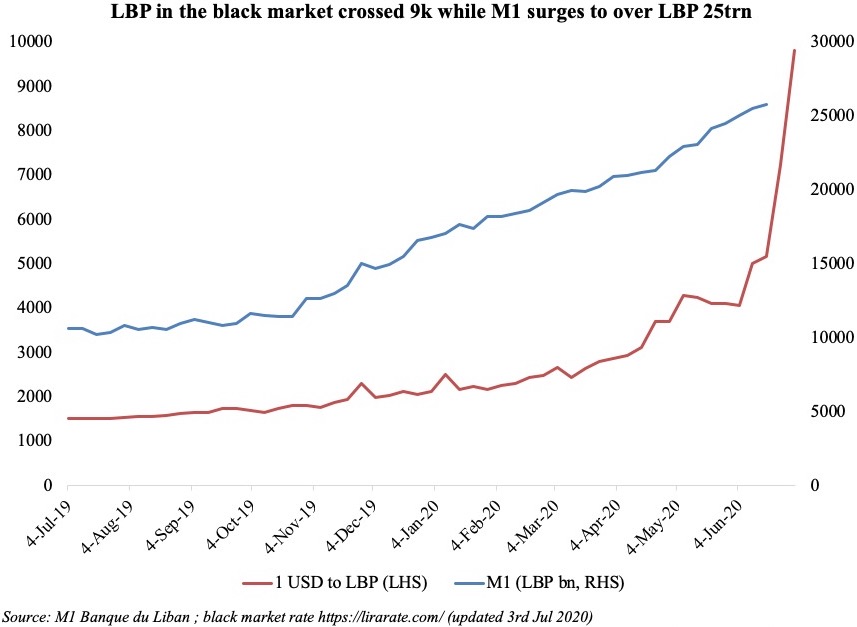

The squeeze severely curtailed domestic and international trade and resulted in a loss of confidence in the monetary system and the Lebanese pound. With the outbreak of Covid19 and lockdown measures came a severe drop in tax receipts, resulting in the printing of currency to cover the fiscal deficit, generating a vicious cycle of exchange rate depreciation and inflation. The black market exchange rate touched a high of LBP 9800 in early July, before steadying to around LBP 7400 in early September (versus the official peg at 1507). In turn these policy measures led to a severe economic depression, with GDP forecast to decline by 25% in 2020, with unemployment rising to 50%.

In response to the crisis, the government of Hassan Diab prepared a financial recovery plan that comprised fiscal, banking, and structural reforms as a basis for negotiations with the IMF. In effect, the Diab government and Riad Salameh, governor of the BDL deliberately implemented an inflation tax and an illegal ‘lirafication’ – a forced conversion, a spoliation, of foreign currency deposits into LBP to achieve internal real deflation. The objective is to impose a ‘domestic solution’ and preclude an IMF programme and associated reforms.

The apocalyptic Port of Beirut explosion on August 4, compounded by official inertia in responding to the calamity, has led to the resignation of the Diab government and appointment of a new PM, Mustafa Adib. Economic activity, consumption and investment are plummeting, unemployment rates are surging, while inflation is accelerating. Confidence in the banking system and in macroeconomic and monetary stability has collapsed. Rebuilding the economy

Prospects for an economic recovery are dismal unless there is official recognition of the large fiscal and monetary gaps, and a comprehensive, credible and sustainable reform programme is immediately implemented by a new Adib government. Such a programme needs to include immediate confidence building measures with an appropriate sequencing of reforms. The government must immediately passing a credible capital controls act to help restore confidence and encourage a return flow of remittances and capital inflows. Immediate measures need to be taken to cut the budget deficit, including by removing fuel subsidies and all electricity subsidies (which account for one-third of budget deficits). The removal of these subsidies is necessary to stop smuggling into neighbouring Syria, which has been a major drain on international reserves.

Monetary policy reform is needed to unify the country’s multiple exchange rates, moving to inflation targeting and a flexible exchange rate regime. Multiple rates create market distortions and incentivise more corruption. In addition, the BdL will have to repair and strengthen its balance sheet, stop all quasi-fiscal operations and government lending. Credible reform requires a strong and politically independent regulator and policy-maker.

There is a need to restructure the public domestic and foreign debt (including BdL debt) to reach a sustainable debt to GDP in the range of 80 to 90% over the medium term; this implies a write down of some 60 to 70% of the debt. Given the exposure of the banking system to government and BDL debt, a debt restructuring implies a restructuring of the banking sector whose equity has been wiped out.

A bank recapitalization and restructuring process should top the list of reforms, including a combination of resolving some banks and merging smaller banks into larger banks. Bank recapitalisation requires a bail-in of the banks and their shareholders (through a cash injection, sale of foreign subsidiaries and assets) of some $25 bn to minimise a haircut on deposits. As part of such far-reaching reforms, Lebanon needs a well-targeted social safety net to provide support for the elderly and vulnerable segments of the population

Crucially, the new government needs to rapidly implement an agreement with the IMF. Lebanon desperately needs the equivalent of a Marshall Plan, a “Reconstruction, Stabilisation and Liquidity Fund’ of about $30 to 35bn, along with policy reform conditionality.

A comprehensive IMF macroeconomic-fiscal-financial reform programme that includes structural reforms, debt, and banking sector restructuring would help restore faith in the economy in the eyes of the Lebanese diaspora, foreign investors/aid providers and help attract multilateral funding from international financial institutions and Cedre conference participants, including the EU and the Gulf Cooperation Council. This would translate into financing for reconstruction, access to liquidity, stabilise and revive private sector economic activity.

Without such deep and immediate policy reforms, Lebanon is heading for a lost decade, with mass migration, social and political unrest and violence. If the new government fails to act, Lebanon may turn into “Libazuela”!

"Staring into the Abyss: Where does Lebanon go from here?", Brookings Doha Centre webinar, 17 Aug 2020

Dr. Nasser Saidi joined the Brookings Doha Center webinar (held on 17th Aug 2020) for a discussion on the dire political and economic situation in Lebanon. The session addressed the following questions: Is the country on its way to becoming a failed state, or will the repercussions of the Beirut blast lead to serious reform? Does the French political initiative steered by President Emmanuel Macron have the potential to resolve the crisis? What are the prospects for economic recovery amid stalled negotiations between the Lebanese government and International Monetary Fund? And what role can the international community play in order to assist Lebanon?

Watch the webinar below:

How to save Lebanon from looming hyperinflation, Article in The National, 31 Jul 2020

The article titled “How to save Lebanon from looming hyperinflation” was published in The National on 31st Jul 2020. The original article can be accessed here & is also posted below.

How to save Lebanon from looming hyperinflation

To bring the country’s economic chaos to an end, it is important to examine how it all began

In June 2020, Lebanon’s inflation rate was 20 per cent, month-on-month. In other words, prices in the country were, on average, 20 per cent more than they were a month before. Compared to a year earlier, in June 2019, they had nearly doubled.

Lebanon is well on its way to hyperinflation – when prices of goods and services change daily, and rise by more than 50 per cent in a month.

Hyperinflation is most commonly associated with countries like Venezuela and Zimbabwe, which this year have seen annual inflation rates of 15,000 per cent and 319 per cent, respectively. Lebanon is set to join their league; food inflation surged by 108.9 per cent during the first half of 2020.

When hyperinflation takes hold, consumers start to behave in very unusual ways. Goods are stockpiled, leading to increased shortages. As the money in someone’s pocket loses its worth, people start to barter for goods.

What characterises countries with high inflation and hyperinflation? They have a sharp acceleration in growth of the money supply in order to finance unsustainable overspending; high levels of government debt; political instability; restrictions on payments and other transactions and a rapid breakdown in socio-economic conditions and the rule of law. Usually, these traits are associated with endemic corruption.

Lebanon fulfils all of the conditions. Absent immediate economic and financial reforms, the country is heading to hyperinflation and a further collapse of its currency. How and why did this happen?

Lebanon is in the throes of an accelerating meltdown. Unsustainable economic policies and an overvalued exchange rate pegged to the US dollar have led to persistent deficits. Consequently, public debt in 2020 is more than 184 per cent of GDP – the third highest ratio in the world.

The trigger to the banking and financial crisis was a series of policy errors starting with an unwarranted closure of banks in October 2019, supposedly in connection with political protests against government ineffectiveness and corruption. Never before – whether in the darkest hours of Lebanon’s civil war (1975-1990), during Israeli invasions or other political turmoil – have banks been closed or payments suspended.

The bank closures led to an immediate loss of trust in the entire banking system. They were accompanied by informal controls on foreign currency transactions, foreign exchange licensing, the freezing of deposits and other payment restrictions to protect the dwindling reserves of Lebanon’s central bank. All of this generated a sharp liquidity and credit squeeze and the emergence of a system of multiple exchange rates, resulting in a further loss of confidence in the monetary system and the Lebanese pound.

Multiple exchange rates are particularly nefarious. They create distortions in markets, encourage rent seeking (when someone gains wealth without producing real value) and create new opportunities for cronyism and corruption. Compounded by the Covid-19 lockdown, the result has been a sharp 20 per cent contraction in economic activity, consumption and investment and surging bankruptcies. Lebanon is experiencing rapidly rising unemployment (over 35 per cent) and poverty rates exceeding 50 per cent of the population.

With government revenues declining, growing budget deficits are increasingly financed by the Lebanese central bank (BDL), leading to the accelerating inflation. The next phase will be a cost-of-living adjustment for the public sector, more monetary financing and inflation: an impoverishing vicious circle!

We are witnessing the bursting of a Ponzi scheme engineered by the BDL, starting in 2016 with a massive bailout of the banks, equivalent to about 12.6 per cent of GDP. To protect an overvalued pound and finance the government, the BDL started borrowing at ever-higher interest rates, through so-called “financial engineering” schemes. These evolved into a cycle of additional borrowing to pay maturing debt and debt service, until confidence evaporated and reserves were exhausted.

By 2020, the BDL was unable to honour its foreign currency obligations and Lebanon defaulted on its March 2020 Eurobond, seeking to restructure its domestic and foreign debt. The resulting losses of the BDL exceeded $50 billion, equivalent to the entire country’s GDP that year. It was a historically unprecedented loss by any central bank in the world.

With the core of the banking system, the BDL, unable to repay banks’ deposits, the banks froze payments to depositors. The banking and financial system imploded.

As part of Lebanon’s negotiations with the IMF to resolve the situation, the government of Prime Minister Hassan Diab prepared a financial recovery plan that comprises fiscal, banking and structural reforms. However, despite the deep and multiple crises, there has been no attempt at fiscal or monetary reform.

In effect, Mr Diab’s government and Riad Salameh, the head of the central bank, are deliberately implementing a policy of imposing an inflation tax and an illegal “Lirafication”: a forced conversion of foreign currency deposits into Lebanese pounds in order to achieve internal real deflation.

The objective is to impose a ‘domestic solution’ and preclude an IMF programme and associated reforms. The inflation tax and Lirafication reduce real incomes and financial wealth. The sharp reduction in real income and the sharp depreciation of the pound are leading to a massive contraction of imports, reducing the current account deficit to protect the remaining international reserves. Lebanon is being sacrificed to a failed exchange rate and incompetent monetary and government policies.

What policy measures can be implemented to rescue Lebanon? Taming inflation and exchange rate collapse requires a credible, sustainable macroeconomic policy anchor to reduce the prevailing extreme policy uncertainty. Here are four measures that would help:

First, a “Capital Control Act” should be passed immediately, replacing the informal controls in place since October 2019 with more transparent and effective controls to stem the continuing outflow of capital and help stabilise the exchange rate. This would restore a modicum of confidence in the monetary systems and the rule of law, as well as the flow of capital and remittances.

Second is fiscal reform. It is time to bite the bullet and eliminate wasteful public spending. Start by reform of the power sector and raising the prices of subsidised commodities and services, like fuel and electricity. This would also stop smuggling of fuel and other goods into sanctions-laden Syria, which is draining Lebanon’s reserves. Subsidies should be cut in conjunction with the establishment of a social safety net and targeted aid.

These immediate reforms should be followed by broader measures including improving revenue collection, reforming public procurement (a major source of corruption), creating a “National Wealth Fund” to incorporate and reform state commercial assets, reducing the bloated size of the public sector, reforming public pension schemes and introducing a credible fiscal rule.

Third, unify exchange rates and move a to flexible exchange rate regime. The failed exchange rate regime has contributed to large current account deficits, hurt export-oriented sectors, and forced the central bank to maintain high interest rates leading to a crowding-out of the private sector. Monetary policy stability also requires that the BDL should be restructured and stop financing government deficits and wasteful and expensive quasi-fiscal operations, such as subsidising real estate investment.

Fourth, accelerate negotiations with the IMF and agree to a programme that sets wide-ranging conditions on policy reform. Absent an IMF programme, the international community, the GCC, EU and other countries that have assisted Lebanon previously will not come to its rescue.

Lebanon is at the edge of the abyss. Absent deep and immediate policy reforms, it is heading for a lost decade, with mass migration, social and political unrest and violence. If nothing is done, it will become “Libazuela”. Nasser Saidi is a former Lebanese economy minister and first vice-governor of the Central Bank of Lebanon

"Lebanon faces the abyss as political elites dither", Arab News article, 28 Jul 2020

Dr. Nasser Saidi’s interview comments appeared as part of the Arab News article titled “Lebanon faces the abyss as political elites dither” dated 28th July 2020.

The comments are posted below; access the complete news article (including sound bites from Dr. Saidi) here.

“The view of the Hirak (Lebanon’s protest movement) is that we probably need a total breakdown before we can change things,” said Nasser Saidi, Lebanon’s former economy and trade minister and founder of Nasser Saidi & Associates. “I love this quote from Giuseppe Tomasi Di Lampedusa: ‘We have to change everything if nothing is to change.’

“It’s only when it becomes practically unliveable that you are going to get change. But if you look at the experience of other countries in similar situations, two things are comparatively different. The first is that, politicians always shift the discourse to a pro-communitarian versus pro-sectarian, pro-Syrian versus anti-Syrian, pro-Iranian versus anti-Iranian, pro-8th of March versus pro-14th of March, pro-Hariri versus anti-Hariri thing,” he said.

“Once the country’s ruling elites frame the current crisis in sectarian and confessional terms, all the other initiatives concerning reform will go out the window.

“The second thing is to change the narrative. As protests amplify, the ruling elite will say that this is now a matter of national security.”

All of this may be already happening. On June 25, President Michel Aoun delivered a speech on Lebanon’s stability, in which he referred darkly to an “atmosphere of civil war” and portrayed the anti-government protests as an attempt to stir up sectarian discord.

“Ever since we have come to life in this country or in most of the Arab world, we have been told that security and stability is paramount to our survival,” said Saidi. “Any challenge to the existing order is framed as a challenge to security and stability. But once you use that argument, then you can start using the repressive forces of the state, and this is precisely what is happening today in Lebanon.

“The army and security services are quelling rising protests. Internal security services are now checking on the exchange rate prices at foreign exchange dealers.”

The breaking point, said Saidi, will come in early September. “Give it a maximum of 90 days and we will see an explosion in the streets. Hospitals will start closing, schools and universities will not be able to open. People cannot afford to send people to school. You will most likely no longer have electricity and once you no longer have electricity, everything else will break down, including communications.”

Saidi believes Lebanon’s ruling elites will try to divert attention from the increasing misery in the country.

“The misery index, which is the sum of the unemployment rate and the inflation rate, in Lebanon now is over 100 percent,” he said.

Pointing to central bank losses of $50 billion and reports of unorthodox accounting practices by the bank’s governor, Saidi said: “They are refusing to admit that they made mistakes, that there are embedded losses in the system, that there was a Ponzi scheme by the central bank — the banks benefited from this, and the shareholders of the banks and big depositors benefited from it.

“What’s most significant is that they got their money out with the connivance of the central bank. Individuals who have their deposits or income in Lebanese pounds have seen their wealth and income go down by around 70 percent. The only other cases I have seen like this are following hyperinflation after the two world wars in Europe and the end of the Soviet Union. There is now a destruction of the middle class in Lebanon, as happened in the 1980s.”

Lebanon’s only hope lies with reform, Saidi said. “There will be no help from outside, from other Arab states or Europe, or the IMF and the international community, until reforms are made internally.”

Forbes Middle East Leaders' Insights: Breaking Down The Lebanese Situation With Dr. Nasser Al Saidi, Jul 2020

Dr. Nasser Saidi was interviewed by the Managing Editor of Forbes Middle East, as part of their Leaders’ Insight series, to breakdown the factors leading up to the economic uncertainty in Lebanon and to understand the way forward.

Watch the interview below:

To halt Lebanon's meltdown it is imperative to reform now, Article in The National, 4 Jul 2020

The article titled “To halt Lebanon’s meltdown it is imperative to reform now” was published in The National on 4th Jul 2020. The original article can be accessed here & is also posted below.

To halt Lebanon’s meltdown it is imperative to reform now

The country’s currency has lost about 80% of its value against the US dollar and poverty and unemployment are on the rise

Lebanon is in the throes of an accelerating economic and financial meltdown. Unsustainable monetary and fiscal policies and an overvalued pegged exchange rate led to persistent fiscal and current account deficits.

Public debt which reached more than 155 per cent of gross domestic product in 2019, is projected rise to 161.8 per cent in 2020 and 167 per cent in 2021, according to International Monetary Fund estimates. That is the third highest ratio in the world after Japan and Greece.

Informal capital controls, foreign exchange licensing, freezing of deposits and payment restrictions to protect the dwindling reserves of Lebanon’s central bank, precipitated the financial crisis, generated a sharp liquidity and credit squeeze and the emergence of a system of multiple exchange rates.

The squeeze is severely curtailing domestic and international trade and resulted in a loss of confidence in the monetary system and the Lebanese pound. Multiple exchange rates created distortions in markets and new opportunities for corruption. The result is a sharp, double-digit contraction in economic activity, consumption and investment, surging bankruptcies, and rapidly rising unemployment rates estimated at above 30 per cent.

A dangerous inflationary spiral has gripped the country with the currency’s value against the dollar nosediving as much as 80 per cent. Inflation is on the rise and reached an annual 56 per cent in May, according to Lebanon’s Central Administration of Statistics. A Bloomberg survey of economists conducted in June, projects inflation will average 22 per cent in 2020 compared with a forecast of 7.7 per cent from a previous survey.

The minimum wage has shrunk from the equivalent of $450 per month while food prices have surged. Since the end of a 15-year civil war in 1990, extreme poverty has hovered at between 7.5 to 10 per cent, while about 28 per cent of the population is poor, according to the World Bank. In November, the World Bank warned if the economic situation in the country worsened, those living below the poverty line could rise to 50 per cent.

Given the collapse of the long-maintained peg, there is no anchor for expectations of the future value of the Lebanese pound.

The Central Bank of Lebanon does not have the reserves to support the pound. There is great uncertainty concerning the macroeconomic outlook, fiscal and monetary policies, exchange controls and structural reforms.

The government approved a rescue plan, the basis for negotiations with the IMF, but failed to set a credible roadmap for structural reforms and none of the promised reforms have been undertaken. There is a loss of confidence in the banking system and in macroeconomic and monetary stability. As a result, people want foreign currency to protect themselves, as a hedge against inflation and further depreciation of the pound.

Transfer restrictions have led to a sudden stop of capital inflows and remittances from Lebanese expatriates, who fear their transfers will be frozen. Remittances accounted for 12.9 per cent of GDP in 2019.

With capital and payment controls and lack of intervention by the central bank, the foreign exchange market became a cash market with little liquidity, therefore highly volatile and subject to large fluctuations, rumours and panic.

Two short-term factors have compounded the currency crisis. The Covid-19 lockdown meant a loss of remittances that would have come in as cash. Media reports cite an accelerated smuggling of imported, subsidised commodities like fuel and wheat into neighbouring Syria these past months due to the increasing bite of international sanctions and a failing wheat harvest.

Panic prevails because of new US sanctions targeting Syria under the Caesar Syria Civilian Protection Act (the Caesar Act) that came into effect last month. Syrians are trying to hedge against inflation and the depreciating Syrian pound by tapping Lebanon’s forex market. In effect it is one market.

More fundamentally, Lebanon’s rising inflation rates are feeding expectations of ever higher inflation rates, which along with the sharp decline in real income because of the deep recession, means a fall in the demand for money and lower demand for the Lebanese pound. As people try to shift out of the Lebanese pound, inflation rises, and the currency depreciates against the US dollar.

The vicious cycle is being fed by the monetary financing of budget deficits. Lebanon’s fiscal deficit increased 26.90 per cent in the first four months of the year to $1.75B from the year-earlier period. With the government unable to borrow from the markets, the central bank is financing the growing budget deficit and, increasingly, a growing proportion of government spending. The printing press is running, with a growing supply of Lebanese pounds on the market chasing a dwindling supply of US dollars. Hyperinflation looms.

The deepening crisis requires urgent, decisive, credible, policy action. A capital control act should be passed immediately. That will help rebuild confidence in the monetary system and restore the flow of capital and remittances.

The prices of subsidised commodities and services (fuel, electricity) should be raised to combat smuggling and stem the budget deficit. Smart and targeted subsidies are more effective. The impact of removing general subsidies is less painful than financing budget deficits that accelerate overall inflation and exchange depreciation. Exchange rates need to be unified within a central bank and bank organised market.

Most important, is rapidly agreeing and implementing a financial rescue package with the IMF. That should be based on a comprehensive macroeconomic-fiscal-financial reform programme that includes structural reforms, debt, and banking sector restructuring, which would provide access to liquidity, stabilise and revive private sector economic activity. Nasser Saidi previously served as Lebanon’s minister of economy and industry and a vice governor of the Central Bank of Lebanon. He is president of the economic advisory and business consultancy Nasser Saidi & Associates.

Comments on Lebanon’s recent BDL appointments in Reuters, Jun 10 2020

Dr. Nasser Saidi’s comments on recent appointments in Lebanon’s central bank appeared in the Reuters article titled “Lebanese government picks central bank vice governors, fills top state jobs“, published on 10th June 2020.

Comments are posted below. Nasser Saidi, a former economy minister, said the government lost credibility by approving the proposed nominations for the central bank, the banking control commission and the capital markets authority. “We missed a historical opportunity…The banking sector is at the heart of any rescue plan for Lebanon,” he said. “You need a restructuring of the debt, of the financial sector, and you need people who are not political appointees to oversee that.”

"Lebanon’s Economy: Meltdown & Redemption Through the IMF", Ana Khat Ahmar webinar, 1 Jun 2020

Interview with CNBC Arabia on restructuring of Lebanon’s banks, 4 May 2020

Dr. Nasser Saidi was interviewed on the restructuring of Lebanese banks under the government’s reform plan. The CNBC Arabia TV interview can be viewed via this tweet or directly at https://www.pscp.tv/w/1vAxRBrjOzPxl?t=34

"Lebanon's Economy: Staring into the Abyss", Presentation to the Harvard Business Club in Lebanon, 24 Apr 2020

Dr. Nasser Saidi’s presentation titled “Lebanon’s Economy: Staring into the Abyss“, was aired as a webinar to the Harvard University Alumni Association of Lebanon (HUAAL) and the Harvard Business Club in Lebanon on 24th April 2020.

Click below to access the webinar, including Q&A.

"Saving the Lebanese Financial Sector: Issues and Recommendations", by A Citizens’ Initiative for Lebanon, 15 Mar 2020

The article titled “Saving the Lebanese Financial Sector: Issues and Recommendations”, written by A Citizens’ Initiative for Lebanon was published on 15th March, 2020 in An Nahar and is also posted below.

Saving the Lebanese Financial Sector: Issues and Recommendations

In order to restore confidence in the banking sector, the government and the Banque du Liban (BDL) need a comprehensive stabilisation plan for the economy as a whole including substantial fiscal consolidation measures, external liquidity injection from multi-national donors, debt restructuring and a banking sector recapitalisation plan. Specifically, the Lebanese banking sector which will be heavily impaired will have to be restructured in order to re-establish unencumbered access to deposits and restart the essential flow of credit. A task force consisting of central bank officials, banking experts and international institutions should be granted extraordinary powers by the BDL and the government to come up with a detailed plan which assesses the scale and process for bank recapitalisation and any required bail-in; identifies which banks need to be supported, liquidated, resolved, restructured or merged; establish a framework for loss absorption by bank shareholders; consider the merits of establishing one or several ‘bad banks’; revise banking laws; and eventually attract foreign investors to the banking sector. In the meantime, we would recommend the imposition of formal and legislated capital controls in order to ensure that depositors are treated fairly and also ensure that essential imports are prioritised. How deep is Lebanon’s financial crisis? The financial crisis stems from a combination of a chronic balance of payments deficits, a liquidity crisis and an unsustainable government debt load which have impaired banks’ balance sheets, leaving many banks functionally insolvent.

Even before the government announced a moratorium on its Eurobond debt on March 7th, public debt restructuring was inevitable, as borrowing further in order to service the foreign currency debt was no longer possible and, dipping into the remaining foreign currency reserves to pay foreign creditors was deemed to be ill-advised given the priority to cover the import bill for essential goods such as food, fuel and medicine. Moreover, with more than 50 percent of fiscal revenue dedicated to debt service in 2019, debt had clearly reached an unsustainable level.

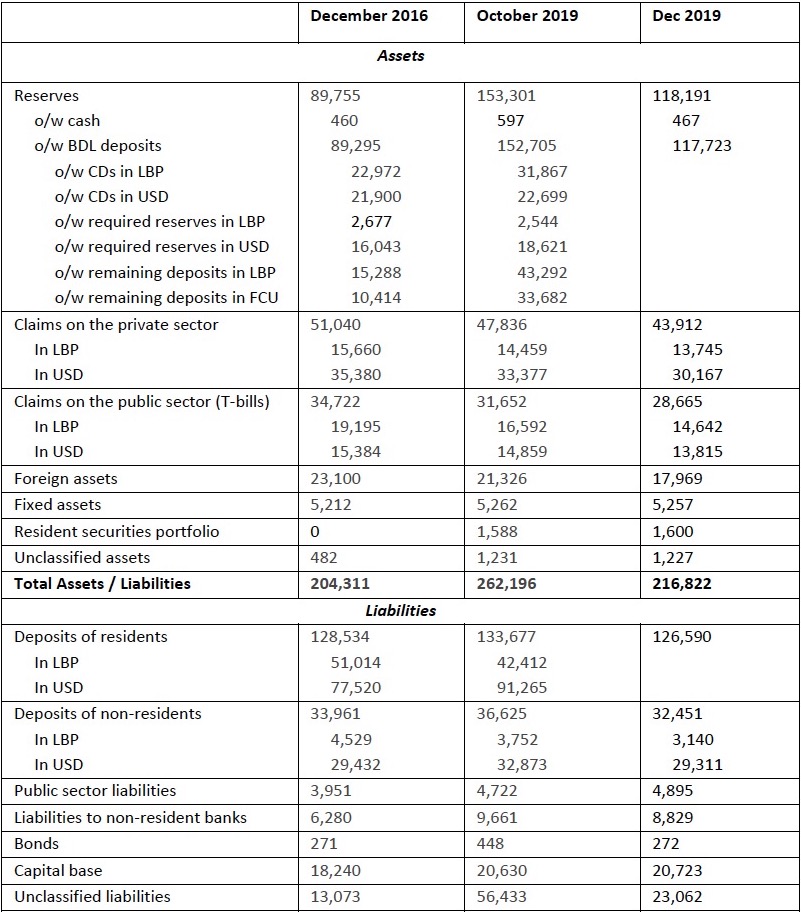

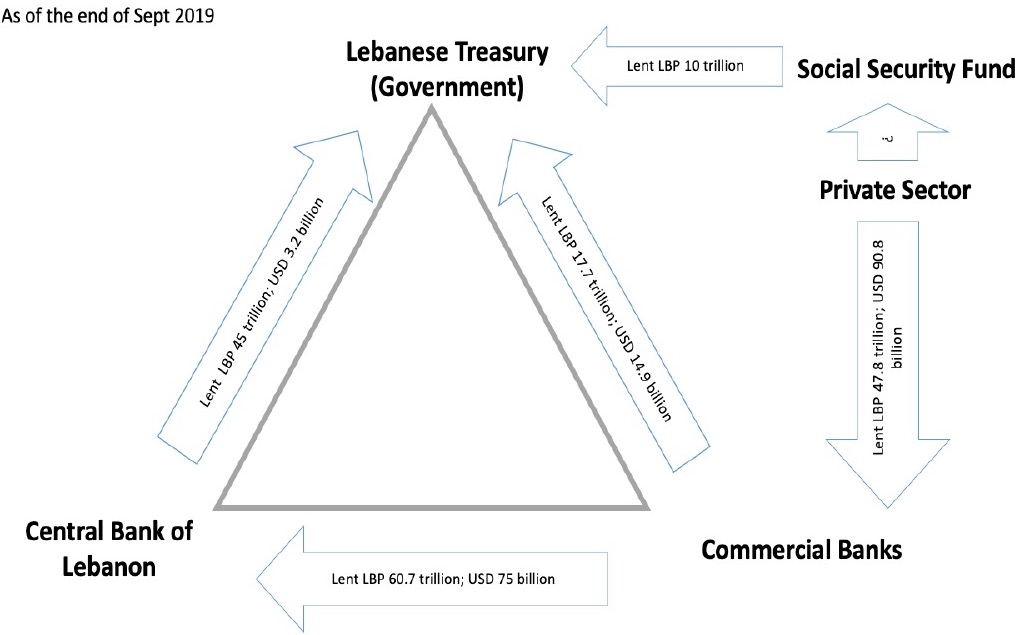

At the end of December 2019, banks had total assets of USD 216.8 billion (see Table 1). Of these, USD 28.6 billion were placed in government debt, and USD 117.7 billion were deposits (of various types) at BDL, which is itself a major lender of the government (see Figure 1 for the inter-relations between the balance sheets of the banks, the central bank, and the government). Banks also hold more than USD 43.9 billion in private loans. Already, the banking association is assuming that approximately 10 percent of private sector loans, such as mortgages and car loans, have been impaired due to the economic crisis. Other countries facing similar financial and economic crises have experienced much higher non-performing loan rates. For instance, the rate rose to above 35 percent in Argentina in 1995 and neared 50 percent in Cyprus in 2011.

Well before the decision to default however, Lebanon’s banks have had limited liquidity in foreign currency and have been rationing it since last November, as the central bank was not releasing sufficient liquidity back into the banking system. Even banks that have current accounts with the Banque du Liban do not have unfettered access to their foreign currency deposits. The BDL has had to balance a trade-off between defending the Lebanese pound peg, releasing liquidity or continuing to finance government fiscal deficits and has chosen to prioritise maintaining the peg and covering the country’s import bill. Table 1: Consolidated commercial bank balance sheet (USD million)

Source: Banque du Liban. (2019). Consolidated Balance Sheet of Commercial Banks. Retrieved from https://www.bdl.gov.lb.

Note: In December 2019, commercial banks have netted the results of the swap operations with BDL, thus explaining the large swing in Reserves (asset side) and Unclassified liabilities.

Reducing public debt to a sustainable level will require deep cuts in government and central bank debts. This in turn will have a significant impact on bank balance sheets and regulatory capital. For most banks, a full mark-to-market would leave them insolvent. To avoid falling short of required capital standards, BDL has temporarily suspended banks’ requirements to adhere to international financial reporting standards. But suspending IFRS cannot continue for a long period, as it effectively disconnects the Lebanese banking system from the rest of the world. What will be the impact of the sovereign default on the banking sector?

Today, Lebanese banks are not able to play the traditional role of capital intermediation by channelling deposits towards credit facilitation. In most financial crises, public authorities are able to intervene to recapitalise the banks and central banks are able to intervene to provide liquidity. Unfortunately, in Lebanon, the state has no fiscal ammunition and the central bank is itself facing dwindling foreign exchange reserves. This leaves the banks in a highly precarious situation.

In a sovereign restructuring scenario where we assume a return to a sustainable debt level of 60% debt to GDP ratio and a path to a primary budget surplus, depending on the required size of banking sector in a future economic vision for the country, we estimate the need for a bank recapitalisation plan to amount to $20 to $25 billion to be funded by multi-lateral agencies and donor countries, existing and new shareholders, and a possible deposit bail-in. Under all circumstances, we strongly advocate the protection of smaller deposits. In addition, special care has to be taken during any bail-in process to (i) provide full transparency on new ownership; (ii) avoid concentrated ownership; and (iii) shield the new ownership from political intervention either directly or indirectly. It is also worth noting that additional amounts of capital will be required to jumpstart the economy and provide short term liquidity.

Leaving the banking sector to restructure and recapitalise itself without a government plan would take too long and Lebanon would turn even more into a cash economy, with little access to credit, little saving, low investment, and low or negative economic growth for years to come. Economic decay would ultimately lead to enormous losses for depositors, and serious hardship to the average Lebanese citizen. What should be the goal of financial sector reforms?

The primary goal of financial sector interventions must be to restore confidence in the banking sector and restart the flow of credit and unrestricted access to deposits. In addition to rebuilding capital buffers and addressing the disastrous state of government finances, we would advocate reforming the financial sector in order to avoid banks’ over-exposure to the public sector in the future, incentivising them to lend instead to the real economy. This must include a prohibition of opaque and unorthodox financial engineering and improving banks’ capacity to assess local and global markets.

Confidence in the financial sector will also require a strong and independent regulator. Lebanon has a unique opportunity in that regard as there are 13 vacancies in the regulatory space that need to be filled by end of March: four vice governors of the Banque du Liban, five members of the Commission of Supervision of the Bank (current members due to leave by end of March), three Executive Board members of the Capital Markets Authority, and the State Commissioner to BDL. These nominations should be completed following a transparent process shielded from political and sectarian influence ensuring candidates possess the requisite competencies.

In addition to these nominations, a revamp of the governance of the regulatory institutions has to be undertaken following a thorough review. In order to enhance risk management and avoid a repeat of concentrated lending in the future, the monetary and credit law should be amended to prohibit excessive risk taking related to the government, which will have the double benefits of forcing a more disciplined sovereign borrowing program and encourage a more diversified use of bank balance sheets directed at more productive areas of the real economy. Providing a framework to curtail so-called “financial engineering” transactions should also be addressed in order to discourage moral hazard and enhance the transparency and arms-length nature of any such operations in the future.

Finally, any future model will also require a migration towards a floating currency, and revised tax and financial sector laws and regulations, encouraging greater competition including from foreign banks. It is worth noting that while a devaluation of the LBP would have a positive direct effect on the balance sheet of banks, it would hurt their private sector borrowers, as most of these loans are dollar denominated, and thus, would lead to higher level of NPLs, hurting banks through second order effects. Figure 1: Net obligations of Lebanese government, central bank, commercial banks and social security fund (as of September 2019 due to lack of some data as of December 2019).

How do we restructure the financial sector?

Saving the financial sector will require empowering a task force consisting of BDL officials, BCCL officials, independent financial sector experts, and Lebanon’s international partners, including multilateral-agencies. Bank equity should be written down to reflect the reality of asset impairment with existing shareholders being allowed to exercise their pre-emptive rights to recapitalize banks with their own resources or by finding new investors, thus reducing the burden on the public sector, multilateral agencies, donors or depositors. Certain banks could be wound down or resolved by the government. Banks that are liquidated or placed into resolution would transfer control to the government, though current bank administrators can remain in place so that regular business transactions can continue. Some banks may be too small to consider “saving’ and should go into liquidation.

The purpose of this process would be to restructure (or wind down) insolvent institutions without causing significant disruption to depositors, lenders and borrowers. The first step in the resolution process is for shareholders and creditors to bear the losses in that order. If the bank has negative equity after this stage, it can begin by selling key assets, such as real estate or foreign subsidiaries before resorting to a capital injection.

One potentially useful tool to support asset sales and re-establish normal banking activities quickly would be to create a ‘bad bank’ consisting of the bank’s non-performing loans or toxic assets. A ‘bad bank’ makes the financial health of a bank more transparent and allows for the critical parts of the institution to continue operating while these assets can be sold. Bad banks have been used in France, Germany, Spain, Sweden, the United Kingdom and the United States, among others, to address banking crises similar to the current Lebanese situation. ‘Bad banks’ can be established on a bank-by-bank basis, managed by the bank itself (under government stewardship) or by the government on a pooling basis. The challenge in Lebanon is neither the BDL nor the largest banks have sufficient capital buffers to fund the equity of such a bad bank.

If the bank equity remains in the red once key assets have been sold (or transferred to a ‘bad bank’), absent sufficient recapitalisation funds, a bail-in may be considered. A bail-in refers to shrinking of the bank’s liabilities, consisting mainly of deposits, by converting a portion into bank equity. Nationalization is impractical in the Lebanese context. While transferring control of operations away from bank management teams that have lost credibility will be necessary, nationalization is impractical in the Lebanese context since the government is effectively insolvent. Also, state-owned banks may be used to further serve political interests and can be easily misdirected and mismanaged by becoming platforms for politically motivated lending, hiring and pricing. Does Lebanon need fewer banks?

We believe that a market like Lebanon requires fewer banking institutions and a round of consolidation is imperative to make the system more robust and competitive as well as more diversified business models in order to serve a broader spectrum of economic activity. Mergers will require first full clarity on banks’ financials. As such, this crisis could be seized upon to achieve this outcome. Academic research in this area confirms that while bank consolidation can lead to higher fees and potentially higher loan rates, it also provides greater financial stability and less risk taking. Larger banks can also attract investors more easily, especially high-quality long-term shareholders.

In most countries experiencing a financial crisis, those banks that are overexposed to troubled assets have been absorbed into large healthy banks. However, in Lebanon, as most large banks are heavily exposed to central bank and government debt and non-performing loans they are unable to play the consolidator role. We therefore believe that a consolidation can be best achieved by a combination of unwinding smaller banks, resolving some banks and merging larger banks which would facilitate new equity fundraising, and cost cutting with fewer branches required in an increasingly digital world. Larger banks will also be able to afford to invest in newer IT systems and risk management systems over time and be viewed as better credits by foreign correspondents. Conclusion. The solutions exist, the time to act is now! Signatories (in their personal capacity) Amer Bisat, Henri Chaoul, Ishac Diwan, Saeb El Zein, Sami Nader, Jean Riachi, Nasser Saidi, Nisrine Salti, Kamal Shehadi, Maha Yahya, Gérard Zouein

Institutional Endorsements LIFE Kulluna Irada

Comments on Lebanon's foreign currency reserves in FT, 8 Mar 2020

Dr. Nasser Saidi’s comments on Lebanon’s foreign currency reserves appeared in the article titled “Lebanon set to default for first time as foreign currency reserves dive” published in the FT on 8th March 2020.

The full article can be accessed at: https://www.ft.com/content/bda10536-6145-11ea-a6cd-df28cc3c6a68

Comments are posted below: Nasser Saidi, a former central bank vice-governor, estimated that usable reserves had fallen to “about $3bn to $4bn”. He said this was because the gross reserves included $18bn to $19bn set against deposits for commercial banks that the BdL could not spend because of reserve requirements. In addition, the BdL has lent local institutions about $6bn to $7bn to help them cover their commitments to correspondent banks, Mr Saidi said. “It is now urgent that the government opens up negotiations with the IMF,” Mr Saidi said, “because you’re going to need help with balance of payments, even to fund your imports”.

"Capital Controls and the Stabilization of the Lebanese Economy", by A Citizens’ Initiative for Lebanon, 5 Feb 2020

The article titled “Capital Controls and the Stabilization of the Lebanese Economy”, written by A Citizens’ Initiative for Lebanon was published on 5th January, 2020 in An Nahar and is also posted below.

This note is the latest in a series of analysis by an independent group of citizens who met in their personal capacity in December 2019 to discuss the broad contours of Lebanon’s financial crisis and ways forward.

Capital Controls [1] and the Stabilization of the Lebanese Economy

Summary:

In mid-October 2019, Lebanese banks shut down their branches, imposed informal capital controls and blocked depositors’ access to their deposits. These informal capital controls are unprecedented in Lebanese banking history and are not based on legal grounds. To make matters worse, they have been applied without any transparency and in an arbitrary manner. In line with our 10-point action plan to avoid a lost decade, Lebanon urgently needs to replace these informal controls with formal (i.e., based on laws and regulations), focused and effective capital controls that are an integral part of a macroeconomic comprehensive program for monetary and financial stabilization and economic recovery. Well-designed capital controls are essential in slowing down the outflow of capital and stabilizing Lebanon’s external finances until confidence is restored in the Lebanese banking system and economy. What are capital controls?

Formal Capital controls are lawful restrictions placed by government authorities on the flow of capital, i.e. on foreign currency transactions. These restrictions are designed by governments, implemented by banks and financial institutions and are typically enforced by a central bank.

Capital controls can take many forms outright prohibition of any international transaction or, alternatively, any international transaction above a certain threshold; restriction depending on the type of the transaction debt vs equity investments, short term vs long term, or capital account versus current account. Iceland, for example, restricted capital account transactions in 2008 but allowed current account transactions in other words, no restrictions were placed on imports taxation of international transactions and, finally, requiring licenses or approvals for certain international transactions such as payments for imports of inputs to industries and other economic activity.

The type of capital controls that will be required in Lebanon will vary depending on the program for monetary and financial stabilization and economic recovery, and more specifically, the foreign exchange regime. Why are capital controls required in Lebanon?