“Digitalization, Growth, and Diversification in the Gulf”, AGSIW webinar, 11 Mar 2025

Dr. Nasser Saidi participated in the presentation and discussion hosted by the Arab Gulf States Institute in Washington (AGSIW) ahead of the publication of an IMF report on Digitalisation in the GCC – held as a webinar on March 11th, 2025.

The Gulf Cooperation Council member countries have actively embraced digital transformation, making notable progress in the extensive development of digital infrastructure, the maturity of government digitalization, and a dynamic ecosystem for financial technology activities.

In a forthcoming paper, the International Monetary Fund highlights the positive relationship between progress in digitalization and more favorable macroeconomic and financial outcomes, including economic growth, government effectiveness, financial inclusion, and private sector resilience to shock.

New analysis by the Mohammed bin Rashid School of Government (along with Nasser Saidi & Associates and Developing Trade Consultants) also emphasizes the important and growing role of digitalization in supporting growth and economic diversification.

Within the context of these two papers, what additional efforts can be made toward improving digital skills, industry, and innovation? What are the challenges raised by the broad adoption of digital technologies and artificial intelligence, especially relating to cybersecurity and the potential effect on the labor market? Could comprehensive strategies help further accelerate the GCC countries’ already impressive progress on digitalization and support their broader economic transformation agendas?

Watch the discussion below:

“China’s Rapidly Rising Innovation Capacity – Interview with Nasser Saidi” in The People’s Daily, 5 Mar 2025

The interview with Dr. Nasser Saidi titled “China’s Rapidly Rising Innovation Capacity – Interview with Nasser Al-Saidi” was published in The People’s Daily (China’s biggest daily newspaper) on 5th March 2025. The original article in Chinese can be accessed via this link & its English translation is posted below.

China’s Rapidly Rising Innovation Capacity – Interview with Nasser Saidi

Nasser Al-Saidi, an economist, is a regular presence at many of Dubai’s seminars on the topic of China. With his snow-white hair and tough frame, he speaks methodically.

‘The topic of China is one of my greatest concerns.’ In a recent interview with People’s Daily Online, he said he has been paying attention to China’s development and Arab-China co-operation, believing that China’s economy will continue to grow steadily and create opportunities for pragmatic co-operation among the vast number of developing countries.

‘I believe that China will maintain a solid growth trend this year and inject momentum for long-term sustainable economic development by further deepening reform and opening up and launching more policy initiatives.’ Nasser Saidi said the results of China’s high-quality economic development can be seen in the changes in the structure of China’s foreign trade. According to the Economic Complexity Index published by Harvard University, China’s score has improved from 0.46 in 2000 to 1.4 in 2022 (note: a higher score represents an economy’s more productive capacity), and its ranking among the world’s major economies has improved from 41st in 2000 to 18th in 2022. ‘Looking at the significant growth in China’s exports of electric vehicles, lithium batteries and photovoltaic products, we can sense the trend of China’s economy climbing up the global value and industrial chain.’

Nasser Saidi pointed out that the high priority given to research and development is driving ‘China’s rapid rise in innovation capacity.’ Statistics show that by the end of 2024, China will have about 4.76 million valid domestic invention patents, a record high, making it the first country to have more than 4 million valid domestic invention patents. ‘This marks a remarkable progress in China’s intellectual property development.’

For Nasser Saidi, the success of AI company DeepSeek is a powerful example of Chinese-style innovation and efficiency. DeepSeek has achieved performance comparable to the world’s most advanced AI models, but at a much lower cost, which in turn reduces energy consumption. What’s more, Deep Seek provides an open architecture that allows for more application access and development. ‘Similarly, China is leading the world in innovation achievements in high-end manufacturing and new energy technologies.’

Nasser Saidi, who has served as Lebanon’s Minister of Economy, Deputy Governor of the Central Bank of Lebanon, and Chief Economist of Dubai International Financial Centre, has served as an economic advisor to the International Monetary Fund and the Organisation for Economic Co-operation and Development. He emphasised that ‘the joint “Belt and Road” initiative is crucial to enhancing global connectivity.’ Citing a World Bank report, he noted that the decade of building the Belt and Road had reduced global trade costs by 1.8 per cent through infrastructure development alone, increased trade among participating countries by between 2.8 per cent and 9.7 per cent, increased global trade by between 1.7 per cent and 6.2 per cent, and increased global income by between 0.7 per cent and 2.9 per cent. It is expected that by 2030, building the Belt and Road together could lift 7.6 million people out of extreme poverty and 32 million out of moderate poverty in the countries concerned. ‘Without China’s support, infrastructure construction in many countries would not have been possible.’

Nasser Saidi is a strong supporter of the China-GCC Free Trade Agreement. He has participated in many international forums to explain the significance of signing the China-GCC FTA: ‘Against the backdrop of increased uncertainty in the global economy, the significance of China’s solidarity and co-operation with the GCC countries has come to the fore. China should become a comprehensive strategic partner of the GCC countries in their efforts to diversify their economies. As an important GCC country, the UAE should strengthen financial market co-operation with China, stimulate synergies in the fields of artificial intelligence, climate technology, and aerospace, and explore deepening regional and multilateral co-operation.’

“AI, geopolitics and the Mena opportunity”, Op-ed in Arabian Gulf Business Insight (AGBI), 27 Feb 2025

DeepSeek’s emergence has spotlighted the GCC’s role in hosting green AI infrastructure

The surprise arrival of Chinese LLM startup DeepSeek roiled global markets, wiping billions from US chipmaker Nvidia’s market cap and slashing global tech stocks.

DeepSeek’s breakthrough highlights China’s rapid innovation capabilities, as well as Washington’s struggle to contain Beijing’s rise, particularly in AI and quantum computing.

The Chinese tech firm’s emergence is attributable to its open source, cost-effective AI models, which operate with significantly lower costs and data requirements than existing models. Since DeepSeek entered into the market, global tech firms have announced even higher spending on AI infrastructure and accelerated deployment.

However, financial sustainability remains a question. There is also a long way to go to reach human-level intelligence levels or Artificial General Intelligence (AGI).

DeepSeek has challenged the belief that advanced chip hardware is necessary for better AI. This raises hope for less advanced countries to catch up in the AI race, particularly against the backdrop of greater geopolitical fragmentation and increased protectionism.

As it becomes easier and cheaper to adopt new technology this will increase the ubiquitousness of AI-based applications and services.

AI is a general-purpose technology that promises to be transformational. Its wide applicability will increase economic efficiency and reshape innovation and R&D processes, while complementing other innovations – such as in quantum computing, generative biology and robotics – leading to an upward shift in total factor productivity.

In the early 2020s, initial expectations assumed that AI tools would primarily benefit lower-skilled workers by enhancing efficiency (for example, assisting new customer support employees). However, research has since warned that AI could exacerbate socio-economic disparities.

The International Labour Organisation estimates that 75 million jobs worldwide (or 2.3 percent of global employment) are at risk of automation due to high exposure to generative AI (GenAI) technology, with the risk rising to 5.1 percent in high-income countries.

Nobel Laureates Daron Acemoglu and Simon Johnson caution that decisions regarding powerful automation tools should not be left solely to a small group of entrepreneurs and engineers, as this could deepen income and wealth inequality.

They advocate for AI policies that prioritise worker interests to prevent widespread job displacement and unemployment.

Where does the Middle East stand?

As GenAI technology becomes more mainstream, its growing adoption calls for more data centres, increased electricity consumption and higher carbon emissions.

AI is highly carbon-intensive, with ChatGPT alone generating over 260 tonnes of CO₂ emissions per month. This presents a significant sustainability challenge for tech firms and governments.

However, the GCC offers a solution: renewable energy powered data centres.

Moro Hub, a subsidiary of Digital Dewa, operates a data centre entirely powered by renewable energy (in partnership with Masdar and Acwa Power). With abundant and cost-effective renewable energy, the GCC has a strategic advantage in becoming a global hub for sustainable data centres.

Within the next five years, renewables could account for 30 percent of the region’s total energy capacity, supporting the expansion of “green” data centres.

The GCC had $3.1 billion worth of data centre projects in progress, as of November 2024, with the UAE and Saudi Arabia leading investments in this sector.

Recent partnerships with Europe, China, and the US to develop AI capacity have cemented the ambition of the region to become a prominent player in the sector.

For example the UAE plans to invest EUR 30-50 billion in building a mammoth AI data centre in France. The project is backed by a consortium of French and Emirati investors, including MGX, a major Abu Dhabi government-backed investor.

MGX is also a core stakeholder in OpenAI’s Stargate project, which aims to invest $500 billion in AI infrastructure over the next four years.

The successful adoption of AI and digital technologies requires both hard and soft infrastructure.

This includes electrification, digitalisation infrastructure, supportive policies, R&D investments, STEM education, workforce reskilling, an enabling regulatory environment, and adaptable legal frameworks.

There remains a wide technology divide between the GCC and other Mena countries, which face challenges such as a shortage of AI talent, digital illiteracy, underdeveloped infrastructure, and limited R&D investment.

While AI has the potential to be transformative, it also risks deepening inequalities due to the region’s disparities in digitalisation and AI preparedness.

As the GCC emerges as a leader in AI, it should prioritise technology sharing and capacity building across the region through investment, digital infrastructure integration, and inclusion in foreign aid programmes.

Dr Nasser Saidi is the president of Nasser Saidi and Associates. He was formerly chief economist and head of external relations at the DIFC Authority, Lebanon’s economy minister and a vice governor of the Central Bank of Lebanon

Comments on the World Governments Summit & opportunities in Arab News, 11 Feb 2024

This year’s World Governments Summit will present world leaders and delegates with a unique opportunity to combine efforts and address ongoing challenges amid rising regional tensions, organizers said ahead of the mega-event.

The three-day summit, set to kick off in Dubai on Monday, will bring together 25 world leaders and heads of state, 120 governmental delegations, more than 85 international and regional organizations and institutions, and distinguished thought leaders and experts. The participants will tackle pressing issues facing humanity across different fields, including economy, technology, artificial intelligence, sustainability, finance and education.

In a statement to Arab News, Nasser Saidi, former chief economist and strategist at the Dubai International Financial Centre, and former minister and first vice governor of the Central Bank of Lebanon, named three major challenges facing governments as they meet at the WGS: the growing visible consequences and risks of climate change, the accelerated growth of the digital economy due to the implications of using AI and related technologies, and the “New Cold War” resulting from growing fragmentation and deglobalization as the US, the EU and their allies decouple from China amid geopolitical conflicts and turmoil.

“Each of these challenges is greater for developing and poor countries,” said Saidi.

A growing multipolar world is evident in governments’ policies that are leading to increased economic and financial fragmentation. The number of global trade restrictions introduced each year has nearly tripled since the pre-pandemic period, reaching almost 3,000 last year, according to the International Monetary Fund.

This “New Cold War,” Saidi said, could result in a 7 percent loss of global gross domestic product according to the IMF, due to global supply chains becoming less efficient, and inward-looking, self-sufficiency policies being disguised as restrictions on access to tech and critical resources.

“It will be strategically important for the governments meeting at the WGS to rapidly mitigate the risks of a New Cold War and its potential consequences, including growing strategic and military confrontations,” he added.

The growing climate divide and rapid growth of AI will also affect economies, societies, politics and militaries, and lead to greater degrees of inequality within countries.

“AI magnifies the risks of under-investment in the digital economy, and the growing digital divide between advanced economies and developing countries unable to invest in digital technologies and educate their populations for the digital economy,” said Saidi.

The investments required for climate adaptation to make infrastructure services resilient will also be costly for developing countries, requiring governments to partner with the private sector, which will have to provide 80 percent or more of the financing.

“Along with the growing use of robotics, AI will have profound implications for how governments are organized, and how they will deliver goods and services in general, let alone re-educating and retraining their workforce,” said Saidi.

Comments on China-GCC economic relations, The National, 3 Feb 2023

Dr. Nasser Saidi’s comments (posted below) on the potential for the GCC-China Free Trade Agreement and beyond, appeared in the article titled “Why a China-GCC free trade agreement might be a game changer” on The National dated 3rd February 2023.

Nasser Saidi, president of Nasser Saidi & Associates and former chief economist of the Dubai International Financial Centre, says an FTA could be signed as early as this year.

“The China-GCC FTA negotiations have been ongoing since 2004. While it has taken a long time, agreements have been reached on most trade-related issues,” says Mr Saidi, who also previously served as Lebanon’s minister of economy and industry and deputy governor of the country’s central bank.

“This is the last mile for negotiations, and considering [the] GCC’s plans to increase economic diversification, the agreement is likely to focus beyond just oil, [and] into trade [and] services (including digital), tech sectors and both portfolio and direct investments.”

Chinese President Xi Jingping’s historic visit to Saudi Arabia in December heralds a “major shift” in the strategic relationship between China and the GCC.

“President Xi’s visit will give a strong impetus and I anticipate an initial FTA could be signed in 2023,” says Mr Saidi.

Mr Saidi says trade between the GCC and China has been steadily rising and doubled between 2010 and 2021, with China accounting for about 16.7 per cent of the Gulf region’s total trade in 2021.

Mr Saidi says an FTA would open new sectors such as services, technology, artificial intelligence and robotics, and strengthen linkages in infrastructure, transport and logistics, leading to a “potential doubling of non-oil trade in three years”.

Opportunities also exist in construction, manufacturing, tourism and space exploration, as well as the linking of financial markets, he says.

While China is a big export market, Mr Saidi sees many opportunities beyond trade and investment. “First and foremost, there could be significant benefits from the adoption of the PetroYuan,” he says. “Oil could continue to be priced in USD, but payment and settlement would be in Yuan. The Yuan could be used for all bilateral trade with only the net balance settled in euro or USD.”

Deeper economic ties mean that China and the Gulf region can benefit from increased co-operation on numerous fronts such as the integration of banking and payment systems, the expansion of central bank swap agreements, collaboration between special economic zones and state-owned enterprises becoming an instrument of economic and industrial policy. “Sovereign wealth funds can also be used as an instrument for co-operation — for example GCC SWFs can focus more of their portfolios on Asian economies, especially China, and vice versa,” says Mr Saidi. “In parallel, China will emerge as a geostrategic partner of the GCC in defence and security, given alignment on most political issues.”

"AI & the Digital Revolution: Implications for Regional Economies", Keynote at the Order of Engineers & Architects Beirut, 26 Feb 2019

Dr. Nasser Saidi was invited to present a keynote at the Order of Engineers & Architects in Beirut on 26th February, 2019. Titled “AI & the Digital Revolution: Implications for Regional Economies“, the presentation covered the economics of AI & digitalisation – including recommendations on how policy makers should prepare for five primary economic effects due to AI-driven automation. It looks in-depth at the performance of the Middle East region, also providing a peek at whether there is an ambition-action gap. The presentation ends with takeaways and recommendations as to what an AI strategy should include in the region.

An interview was published in Daily Star where Dr. Saidi airs his views on how AI is key to beating corruption. “Developing an integrated artificial intelligence government strategy and devoting resources to concretely implementing them is the best way to fight corruption, provided it is driven from the highest level, from our prime minister,” Saidi told The Daily Star Wednesday. Read more here.

Dr. Saidi’s keynote (from 1:41 in Video 1) and related panel discussion (Video 2) can be accessed below:

Video 1

Video 2

Speaker at the Arab Strategy Forum, 12 Dec 2018

Dr. Nasser Saidi participated in the Arab Strategy Forum, held in Dubai on 12th December 2018.

Part of the panel session discussing the State of the Arab World Economy in 2019, Dr. Saidi spoke at length about the volatile prospects for oil market, impact of US-China economic war, and how the risks of a new global financial crisis in 2019-2020 are rising (thanks to global debt, high interest and low growth rates).

Below are some key quotes from the panel session: “Arab countries should focus on digitization because it is the future of the world, infrastructure, and work to transform our economies into digital economies” “The economic war between China and America – the two biggest engines of growth globally – goes beyond just trade & will negatively affect the world” “Renewable Energy policies should be a priority: need to invest in it and export it abroad” “The Arab region needs new trade & investment agreements to reflect the shift in trade partners- “pivot East & South”

في جلسة نقاشية حول حالة العالم العربي اقتصادياً في 2019، تطرق د.ناصر السعيدي إلى موضوع الركود الاقتصادي مع العوامل المرتبطة والمهمة للمنطقة العربية، كما أشار د.ﻣﺤﻤﻮد ﻣﺤﻴﻲ اﻟﺪﻳﻦ إلى العلاقة بين معدلات النمو المتوقعة في المنطقة وأسعار النفط. #المنتدى_الاستراتيجي_العربيpic.twitter.com/53nNW2CEFG

— Arab Strategy Forum | المنتدى الاستراتيجي العربي (@arab_strategy) December 12, 2018

"The Fintech Challenge: Transforming Banking, Finance, Payments & Central Banking", Presentation to the UAE Central Bank, 20 Nov 2018

Dr. Saidi provided a keynote address on “The Fintech Challenge: Transforming Banking, Finance, Payments & Central Banking” to the UAE Central Bank on Nov 20, 2018.

The presentation, given as part of the UAE Central Bank’s Strategy Session, covered issues like why Fintech is growing globally and in the MENA region, industry trends, as well as how central banks are adapting and embracing Fintech. Developing the right ecosystem for FinTech and how central banking could change over the next generation were also key discussion points.

World Cup 2018: can anyone predict the winner? Article in The National, 2 July 2018

The article titled “World Cup 2018: can anyone predict the winner?” appeared in The National on 2nd July, 2018 and is posted below. Click here to access the original article.

World Cup 2018: can anyone predict the winner?

Alongside the animals and traditional tipsters, high tech is now being used to try to forecast the next champions

Last week there was a “Black Swan” event at the 2018 Fifa World Cup: the first time in 80 years, since 1938, that Germany, the current World Cup holder, was eliminated at the initial group level.

Other World Cup incumbent champions have been eliminated in the first round: France in 2002; Italy in 2010; and Spain in 2014. Is a champions’ curse emerging? The World Cup is one of the most-watched sporting events in TV history, with an estimated 3.4 billion people tuning in to watch the matches this year. The 32-team tournament fever is rapidly rising as the knockout stages get progress. Which teams will make it to the final?

From the deceased Paul the octopus (from excitement or exhaustion?) to Shaheen the camel, and more recently the clairvoyant deaf cat Achilles, a niche World Cup prediction industry has mushroomed. Over the past 10 years, economists (including at investment banks and academics), statisticians, data scientists, and mathematicians have joined the predictions party alongside the traditional tipsters. New tools including data mining, portfolio theory, econometrics, algorithms and machine learning are being harnessed in an attempt to predict the outcome.

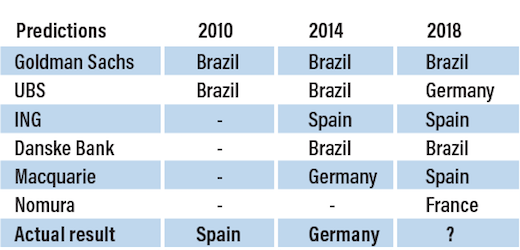

Will the economists, statisticians and algorithms be any better? Will they turn out to be more successful than the animals? Predictions are based on historical performance data that are used to estimate a set of “probability trees “of the success of teams in various rounds. This can be done with econometric tools (similar to those used to pick equities in stock markets), statistical modelling (eg Monte Carlo simulations where multiple “tournaments” are simulated to arrive at a “winner”, ie the team that wins most number of times in these simulations) and, recently, algorithmic predictions. US bank Goldman Sachs and its 1 million simulations using artificial intelligence algorithms favour Brazil to win the World Cup (Dankse Bank shares this view as to the winner), ING had its money on Spain, and Nomura and EA Sports were backing France in a France-Spain final. Before the tournament began, UBS favoured Germany after running a computer simulation of the tournament 10,000 times, (using the Elo-ranking of teams as input, with Commerzbank sharing this view). Given the elimination of Germany the model will now have to be rewired. A poor predictions record

Indeed, the predictions versus outcomes record over the past two World Cups is poor. As the accompanying table shows, none of the banks and their specialised teams were able to pick the winners. These results are not dissimilar to predicting stock markets or individual stock returns: “experts” or computer models do not outperform random, dart-throwing on a newspaper stock picking.

World Cup football remains an unpredictable tournament (hence the excitement) with the outcome of matches also dependent on factors like the fitness of star players, the weather on the day of the match, the number of coaches/managers fired before the start of the tournament, how lenient/strict referees are in one match versus another. The recent introduction of modern technology in the form of Video Assistant Referees (VAR) is making refereeing more accurate but also increasing the number of recorded faults and at this World Cup swelling the number of free kicks and penalties. Who are the real winners?

We plan to be agnostic and watch who emerges the winner on July 15 before deciding whether to endorse the prediction techniques of Achilles the cat or those of some investment bank. However, Fifa is definitely one major winner from the tournament: it is expected to gain about $6 billion in revenue from this year’s World Cup, up 25 per cent from the previous tournament, and will receive a further $3bn from broadcast revenue.

Although viewership reportedly fell a whopping 44 per cent in the US (not surprising given that the team is not among the 32 taking part, although it now pays more to Fifa for broadcasting rights than any other country), India broke the viewership record, with more than 47 million people watching the first four matches (football is now the third-most popular sport to watch in India, and in a few states the fan base even outranks cricket). The shift to emerging economies

The landscape and geography of the World Cup is likely to radically change in the coming decades. The game is slowly gaining prominence in the world’s most populous nations: China, which qualified for the tournament only once in 2002, recently announced plans to create 20,000 new training centres, the world’s biggest academy in Guangzhou (to cost about $185 million) and hopes to host a World Cup “in the future”, with 2034 considered a likely date. Indonesia, with its large population base, has the highest average Premier League audience of any country in the world, even higher than the UK.

There have been 20 World Cups with eight different countries winning with the trophy. Brazil have won the most with five, closely followed by Italy and Germany/West Germany with four. Uruguay and Argentina have both won it twice, and England, France and Spain have all won it the once. Asian nations, so far, have taken a back seat in this game: only Japan and Korea are among the 32 teams that qualified for the event this year.

This pattern will change given the power of demographics and growing incomes in the emerging economies of Asia and Africa. Economics matters. A poor country is less likely to have the infrastructure and financial capacity to support training, competing teams and be able to competitively compensate players; indeed there has been a “sports talent drain” to high-paying countries. In turn, the popularity of the game tends to be proportional to the number of “good” players a country has.

This can be reversed. A good starting point is what China is doing: start with the children and encourage them to develop the right “technical” skills (similar to their Olympics track record).

Making it Clean: Changing the Global Energy Mix, Article for Aspenia, Jul 2018

The article titled “Making it clean: changing the global energy mix” was published in the latest Aspenia Issue, July 2018, and can be downloaded in English and Italian.

The speed of transition to a new global energy mix has accelerated in the past decade. A changing global economic geography with a shift towards fast growing energy-hungry emerging economies (China specifically) as the main growth engines meant a corresponding increase in energy demand that propelled energy prices upwards. Oil prices hit an all-time high of USD 145 in July 2008 before the Global Financial Crisis, and then later in August 2013 to around USD 115. High oil prices provided an incentive for nations (especially emerging ones that ran high oil trade deficits), households and businesses to find substitutes for fossil fuels and lower energy intensity. The EU provided subsidies for renewable energy investments. Concurrently, the OECD countries implemented energy efficiency policies aimed at energy saving, leading to a trend decline in energy used to GDP ratios by some 1%-2% per annum, and breaking the historical link between economic growth and energy demand.

Two additional factors supported the acceleration in energy transition: technological innovation and growing awareness of climate change risks. Innovation in hydraulic fracturing or fracking techniques to extract “tight oil, resulted in the shale revolution and a rapid growth of on-shore oil production in the US. Fracking technology has diffused internationally and its cost has declined: the breakeven oil price for new shale oil wells ranges between USD 46-55, while an oil price between $24 and $38 would cover operating expenses in the US.[1] And the shale oil revolution is spreading internationally: Argentina’s Vaca Muerta (Spanish for Dead Cow), is a shale gas and oil formation the size of Belgium, with technically recoverable oil reserves and shale gas of 27 billion barrels and 802 billion cubic feet respectively, the second largest in the world after China’s 1.12 trillion cubic feet. Technology is changing the economic geography of energy and its global market!

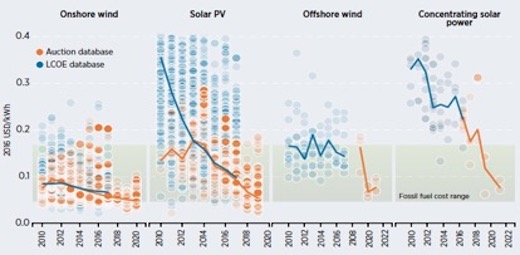

Similarly, technological innovation and investment have dramatically cut the cost of renewable energy. Since 2009, the global benchmark levelised costs of electricity (LCOE) for solar PV has tumbled by 77%, and that for onshore wind by 38%, while lithium-ion battery price index shows a fall from $1,000 per kWh in 2010 to $209 per kWh in 2017[2]. Declining battery costs means falling energy storage costs, which addresses the problem of intermittency of renewable energy. The decline in battery storage costs also means a potential revolution of international trade in renewables-based chemicals and fuels. Government policies to curb climate change alongside technological advances and rapidly falling costs for solar and wind power[3] has meant that renewables are becoming increasingly more competitive, resulting in unsubsidized clean energy world records last year. There is no longer a need to subsidise renewable energy system solutions: global renewable energy prices will be competitive with fossil fuels by 2019 or 2020.

Fig 1: Global levelised cost of electricity and auction price trends for solar PV, CSP, onshore and offshore wind from project and auction data, 2010-2022 (Source: Renewable Power Generation Costs in 2017, IRENA, Jan 2018)

There has also been a massive shift in public opinion and awareness of the implications of global warming. Addressing the risks of climate change has become a key policy priority embodied in the COP21 commitments. All nations (except the US Trump administration) have committed to reduce emissions by at least 20% compared to business-as-usual by 2030. The subsequent COP 22, 23 commitments have all seen unwavering support from countries across the globe (ex-Trump’s US). A New Oil Normal

The implication of the above trends is that there will be a permanent and persistent secular downward shift in the demand for fossil fuels, putting downward pressure on oil prices. This is the New Oil Normal. For coal producers & coal based utilities and fossil fuel producers and exporters like the GCC countries, the risk is that their vast coal and hydrocarbon reserves will become ‘stranded assets’: they will no longer be able to earn an economic return.

The bottom line is that the increasing prosperity of emerging nations, greater energy efficiency, technological innovation and policy commitments to reduce carbon emissions are resulting in a radical changes of the global energy mix and market. Looking ahead, given their size and demographics China, India and other emerging Asian countries will account for around two-thirds of the growth in energy consumption over the coming decade, to be followed by Africa. Increasingly, these emerging economies are switching to renewable energy sources, given their economic and environmental competitiveness. A New Energy World is emerging

New investment in clean energy reached USD 333.5bn in 2017, up 3% from the year before but short of 2015’s record-high USD 360.3bn, but higher in real terms. A record 157 gigawatts of renewable power were commissioned in 2017, up from 143GW in 2016, and far out-stripping the 70GW of net fossil fuel generating capacity added last year. Solar alone accounted for 98GW, or 38% of the net new power capacity coming on stream during 2017[4]. A regional comparison shows that the balance of investment has shifted from Europe as largest-investing region to Asia. China set a new record for clean energy investment in 2017, and the UAE was among those investing more than USD 1bn in clean energy along with 10 other emerging nations (from a total 20 countries). And Saudi Arabia announced a massive 200 gigawatts solar power development in the Saudi desert with Softbank that would be world’s biggest solar project and would be about 100 times larger than the next biggest proposed development!

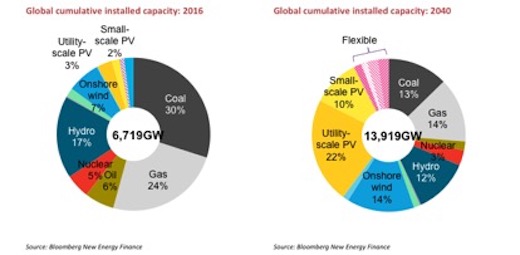

Fig. 2, Global cumulative installed capacity, 2016 and projected, 2040 (Source: Bloomberg New Energy Finance)

Renewable energy sources are set to represent almost three quarters of the USD 10.2trn the world will invest in new power generating technology until 2040, with solar and wind dominating the future of electricity (Fig 2). The world is also increasing investments in clean technologies. A transport and mobility revolution (electric vehicles) will lead to cleaner, healthier cities for increasingly urbanised populations. Not just ‘smart cities’ but also ‘clean cities’. Twin Revolutions: Renewables and AI & Blockchain

We are witnessing the birth of twin revolutions which will conflate: AI and Blockchain technologies are fusing with new energy. AI is supporting the 4th industrial revolution: think energy and water digitization, smart grids, smart meters, “deep learning”[5], demand management (i.e. manage demand response of different devices that run in parallel), and digital asset management (i.e. where machine learning algorithms collate, compare, analyze, and highlight risks and opportunities across a utilities infrastructure thereby providing an opportunity for power companies) among others. Blockchain technology has the potential to offer a reliable, low-cost way for financial and/or operational transactions to be recorded and validated across a distributed network with no central point of authority, leading to a greater decentralization of energy systems.[6] Applications lie across a vast spectrum: digital tokens to reward users for saving energy, adding smart contracts onto a blockchain, asset and inventory tracking, traceability of water, gas & electricity flows & maintenance, data sharing, fraud detection, electric vehicle charging, and so on. Peer to peer energy trading[7] , the ability of neighbouring homes, ‘prosumers’, to sell solar energy to one another as well as to a shared grid is already being tested.

The challenge to the widespread adoption of blockchain technologies will be to develop an enabling legal and regulatory framework. Country policy frameworks need to be developed to focus on cleantech investments, innovation and commercial conversion, in addition to ’soft’ and ‘hard’ investments to facilitate and integrate the twin revolutions of clean energy and AI and blockchain technologies. Clean Energy & Economic Development

Energy, water and basic infrastructure are building blocks of economic growth and development. Some 1.1 billion people, of which some 600 million in Sub Saharan Africa, do not have access to electricity. In the absence of electricity they cannot have access to the internet and the digital economy, digital services, let alone participate in the 4th Industrial revolution. The renewable energy revolution offers a new hope to spur and enable economic development of Africa (with its largely untapped hydro and solar potential), India and Asia, using off-grid power systems and decentralisation that do not require expensive, centrally administered national grids. Renewable energy can be local, at village level. A Renewable Energy Promise?

The IEA has recently warned that the world is headed for irreversible climate change in five years[8]. It is increasingly unlikely that we will be able to keep global warming below 2°C despite COP commitments. Our best hope is to accelerate the global adoption of intelligent renewable energy systems and clean tech for our cities and transport systems, to rapidly change the global energy mix and mitigate the risks of catastrophic climate change.

Enabling the transformative power of new technologies: Article in The National, 1 Jun 2018

The article titled “Enabling the transformative power of new technologies” appeared in The National on 1st June, 2018 and is posted below. Click here to access the original article.

Enabling the transformative power of new technologies

New technologies are disrupting regulated industries including finance, transport, energy, telecoms, health, defense & government

Technology has often resulted in disruptions (remember typewriters, fax machines, film cameras, desk telephones and floppy disks?) but also supported the process of globalization via digital transformations, cross-border flows of data and information, e-commerce and cloud computing.

New technologies have been disrupting many regulated industries including banking and finance, transport, energy, telecoms, health, defense & government. We now live in a world where the largest movie house no longer owns any cinemas thanks to Netflix, the largest accommodation provider, Airbnb, owns no real estate and where Skype, WeChat and WhatsApp exist without owning any telecom infrastructure.

Blockchain – which has become a buzzword and is associated by the public largely with Bitcoin – distributed ledger technology (DLT) and artificial intelligence (AI) are general purpose technologies, with widespread applicability in modern economies.

DLT applications can be used for digital identities of people and companies, maintaining patient records in healthcare, or sale and purchase of real (think property) as well as digital assets, or supply chain like IBMs’ fully transparent food system use case for instance. AI will soon become ubiquitous, with applications in national security, data science, business intelligence, healthcare, entertainment and the list goes on.

The UAE’s aspiration to support and become a leader in the 4th industrial revolution – with its blockchain and AI strategy – is likely to benefit it to help it transform and diversify its economy. Given its growing digitisation over the past decades, the banking and financial sector is a leading candidate for disruption.

Total global investment in the fintech sector was $122 billion over the past three years, with 2017 alone seeing investments to the tune of $31bn, ,according to Kpmg. The US remains the largest player, accounting for some two-thirds of the investments, but China is fast catching up in this space. As the fintech grows, increased focus should be on its economic development potential: given widespread availability of smartphones, fintech is an enabler for financial inclusion and access to finance.

The Middle East is a ripe playing field for such initiatives, especially given the relatively high mobile phone penetration: among the unbanked, 86 per cent of men and 75 per cent of women have a mobile phone but only 35 per cent of women have a bank account. Not to mention how useful it could be for creating digital identities and thereby allow for access to finance and e-services for more than 15 million Syrian, Iraqi and other refugees and displaced in the region. All of this requires investment in infrastructure and an enabling environment. Supportive Regulatory Frameworks for New Technologies

Current bank regulatory and supervisory frameworks generally predate the emergence of technology-enabled innovation. As regulators in the region start implementing new supervisory models, it is critical to avoid regulatory barriers to adoption and spread of new technologies, especially those that could stifle innovative ideas, while ensuring consumer protection and financial stability.

To facilitate innovation, regulators across the globe have focused on either building regulatory sandboxes – testing in a controlled environment, with tailored policy options – or developing accelerators or “boot-camps” for start-ups, ending with a pitch presentation, or just enabling an “innovation hub” that acts as a place to meet and exchange ideas. In the region, both the DIFC and ADGM are at the forefront with accelerators and regulatory sandboxes in place.

Given the cross-country applications of the technology like DLT and payment systems, coupled with global growth of some fintech firms, cross-country and cross-sector cooperation is essential between regulators. Ongoing discussions are needed, especially with respect to uncertainties: safeguarding data privacy, digital identity and its impact on the use of financial services, cyber security, compliance with anti-money laundering and countering financing of terrorism (AML/CFT), risk mitigation when there is a technology-governance gap and so on.

While incumbents and new entrants evolve and adjust to the disruptive potential, regulators are themselves starting to adapt within this ecosystem, leading to a branch called regtech. What is regtech? The Bank for International Settlements defines it as “any range of fintech applications for regulatory reporting and compliance purposes by regulated financial institutions. This can also refer to firms that offer such applications”.

Regtech could transform regulatory compliance by reducing its and risk management at financial institutions. It could also facilitate identity management (know your customer for onboarding, AML/ CFT checks) and improve fraud detection. Suptech – technology for supervisors – goes a step beyond and could increase supervisory effectiveness and efficiency. Some examples include algorithmic regulation and supervision (in areas such as high-frequency trading, algorithm-based credit scoring, robot-advisors) or real time supervision (look at the data as it is generated in the regulated institutions’ operational systems) or even moving towards machine-readable regulations. Together, these could result in major paradigm shifts as to how a regulator functions and a major challenge. Enabling Innovation & Fintech

A new integrated, digital financial world is emerging. The region’s policy makers and regulators should support the burgeoning, innovative start-up culture, rather than being protective of incumbents, which are typically owned by governments and have been shielded from competition. Some guidelines and principles are:

Be supportive of technologies like DLT, AI and related innovations, and remove barriers to their use by undertaking a pro-active and regular review of regulatory regimes.

Create and support innovation facilitators like hubs, sandboxes, incubators, accelerators. The best practice is to review and create structural mechanisms to enable ongoing market engagements.

Coordination, collaboration and communication between domestic regulators is necessary. The emergence of innovations such as digital money, crypto-assets, initial coin offerings (ICOs), digital financial and non-financial services, requires the development of new regulatory regimes and cooperation & coordination between regulators in different industries, such as telecoms.

Build staff capacity and knowledge of regulators and supervisors in the fast-evolving landscape

Digital finance has gone beyond cross-border to become borderless. This requires international coordination and cooperation by authorities to monitor macro-financial risks, mitigate of cyber-risks, and the managing of operational risks from third-party providers, such as cloud-based services.