Conflict & Reverberations Across the GCC: Industrial Strains, Financial Resilience & Emerging Strategic Realignments, Weekly Insights 16 May 2026

Conflict & Reverberations Across the GCC: Industrial Strains, Financial Resilience & Emerging Strategic Realignments, Weekly Insights 16 May 2026

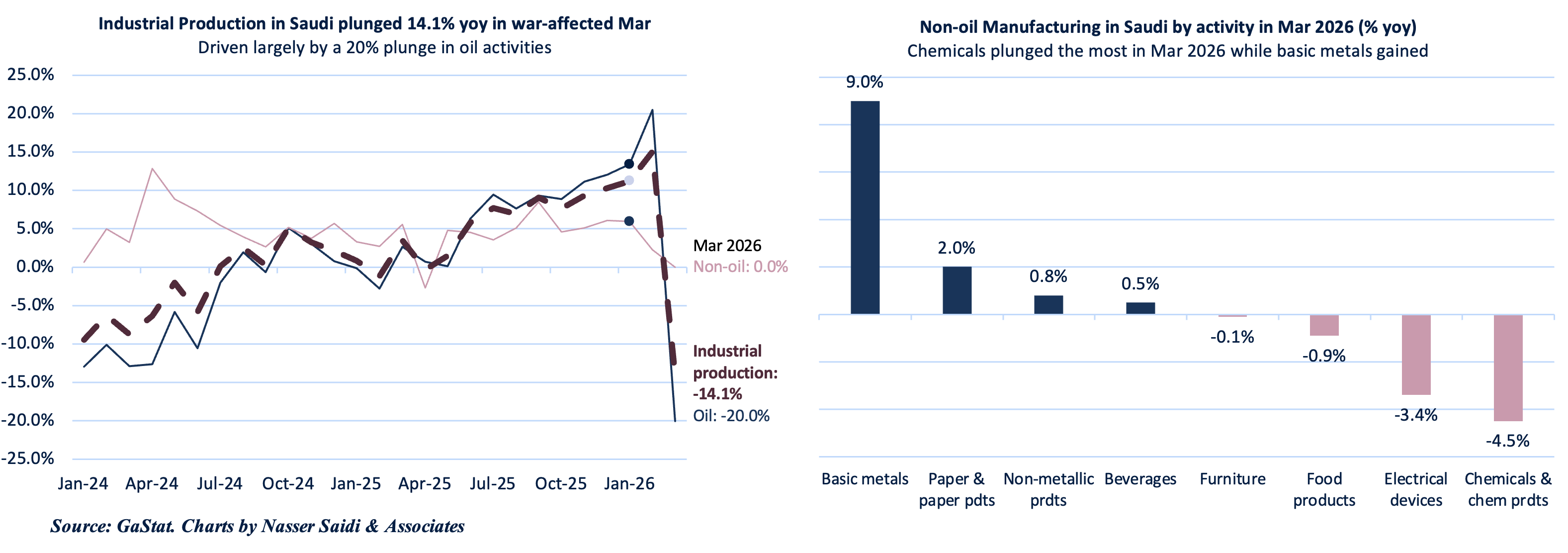

1. Saudi industrial output hit by conflict shock, but investment pipeline supports recovery

- Saudi Arabia’s Industrial Production Index decreased by 14.1% yoy in Mar 2026, a sharp reversal from Feb’s revised 15.0% surge.

- The plunge was primarily driven by a 22.2% decline in mining and quarrying activities and a 20.0% drop in overall oil activities. On a monthly basis, mining activity plunged by 36% mom.

- Manufacturing activity fell by 4.7% yoy, weighed down by an 11.6% drop in refined petroleum products and a 4.5% decline in chemicals. However, basic metals manufacturing showed resilience with a 9.0% annual increase.

- While oil activities struggled, electricity, gas, and air conditioning supply grew by 10.1% yoy and water supply & waste management rose by 1.1%. On a monthly basis, non-oil activities rose by 1.4%, signalling underlying stability.

- Despite the broader economic shock, the Ministry of Industry and Mineral Resources issued 188 new industrial licenses in Mar 2026, attracting over SAR 1.81bn in investments. This follows Feb’s strong performance (38 new mining licenses issued). 78 new factories commenced actual production in Mar, representing SAR 870mn in investment & creating nearly 1,500 new jobs.

- Industrial Production Index and the non-oil PMI (which hit a low of 48.8 in March) reflect severe disruptions from the regional conflict, including a 95% collapse in shipping transits and record-high input cost inflation. For Saudi Arabia, strategic infrastructure projects (e.g. expansion of the East-West Pipeline) are expected to mitigate maritime bottlenecks and support a rapid return to higher utilization rates once regional tensions stabilize. Expect a V-shaped recovery once the conflict ends especially given current project pipeline.

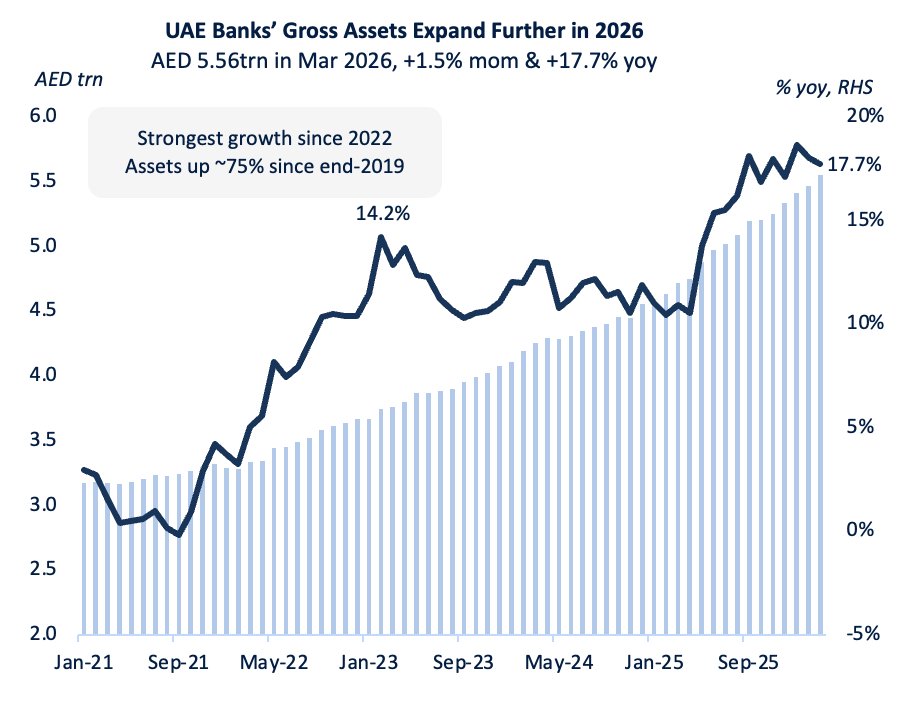

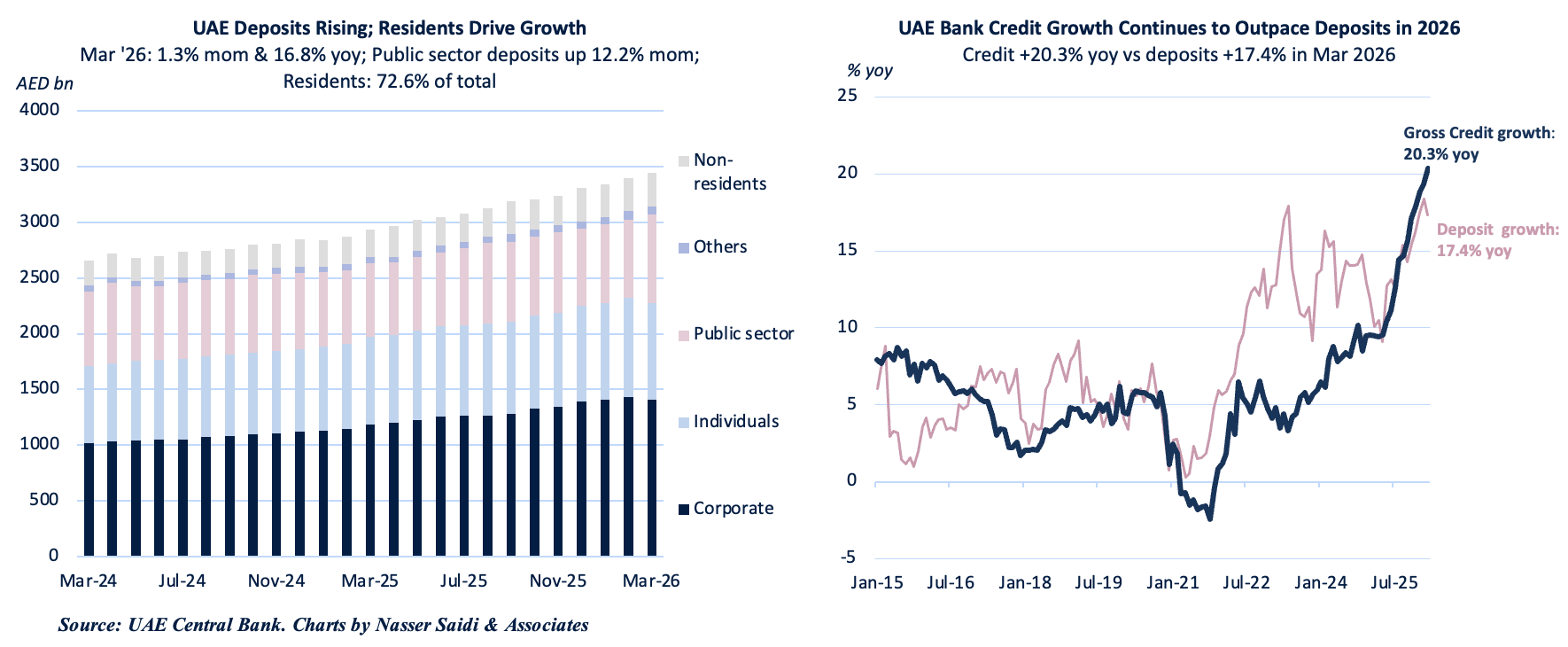

2. UAE aggregate deposits resilient in Mar, but heavily public-sector linked

- UAE gross banking assets grew by 1.5% mom and 17.7% yoy to AED 5.56trn at end-Mar 2026.

- Resident deposits increased 1.3% mom to AED 3.13trn & non-resident deposits also rose by 1.8% to AED 307.2bn: important because non-resident deposits are often more sensitive to geopolitical risk.

- Within resident deposits, largest contribution came from GREs (+16.3% mom to AED 363.1bn); govt sector also rose (+9.0% to AED 427.3bn) => deposit expansion was significantly supported by public-sector balances.

- Private sector deposits weakened despite headline growth. Private-sector deposits fell 1.9% to AED 2,278.2bn, while deposits of other financial corporations declined 2.5% to AED 70.2bn.

- Money supply indicators were up yoy, though M1 fell 2.5% mom, dragged down by a 4% drop in monetary deposits (to AED 903.6bn). Could be due to a preference to hoard cash or drawdown by corporates to manage higher working-capital needs; for now, the CB’s Financial Institutions Resilience Package has provided support to those in need 60.6k individuals, 4,335 SMEs & 485 corporates.

- In the months ahead, keep close track of (a) composition of deposits (i.e. public-sector strength vs private-sector weakness); (b) money supply indicators; and (c) uptake of the Central Bank’s Comprehensive Proactive Financial Institutions Resilience Package.

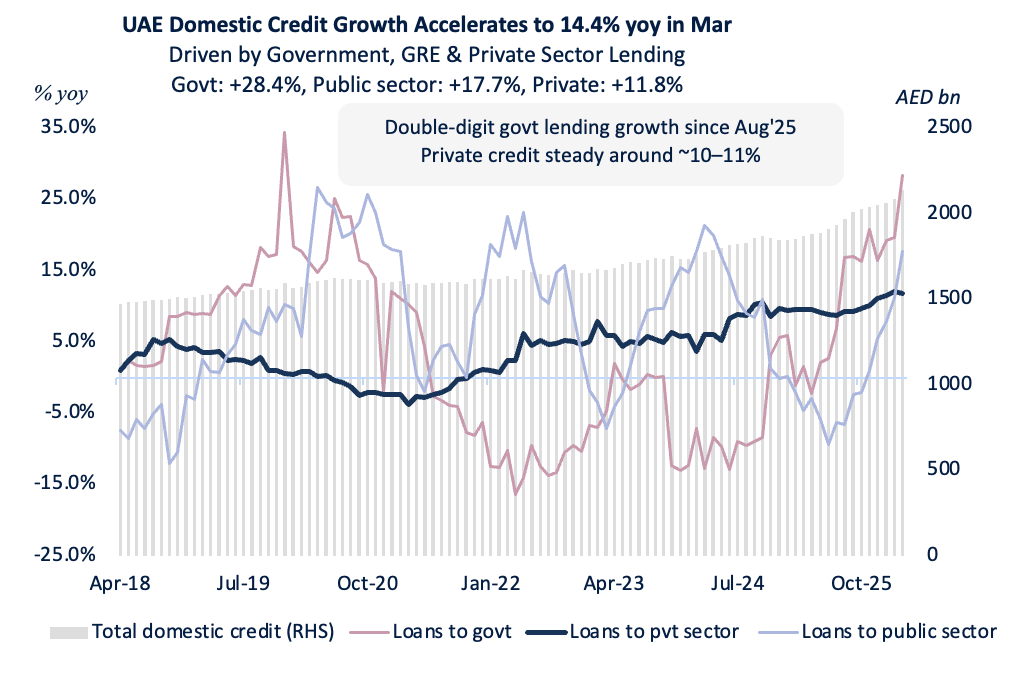

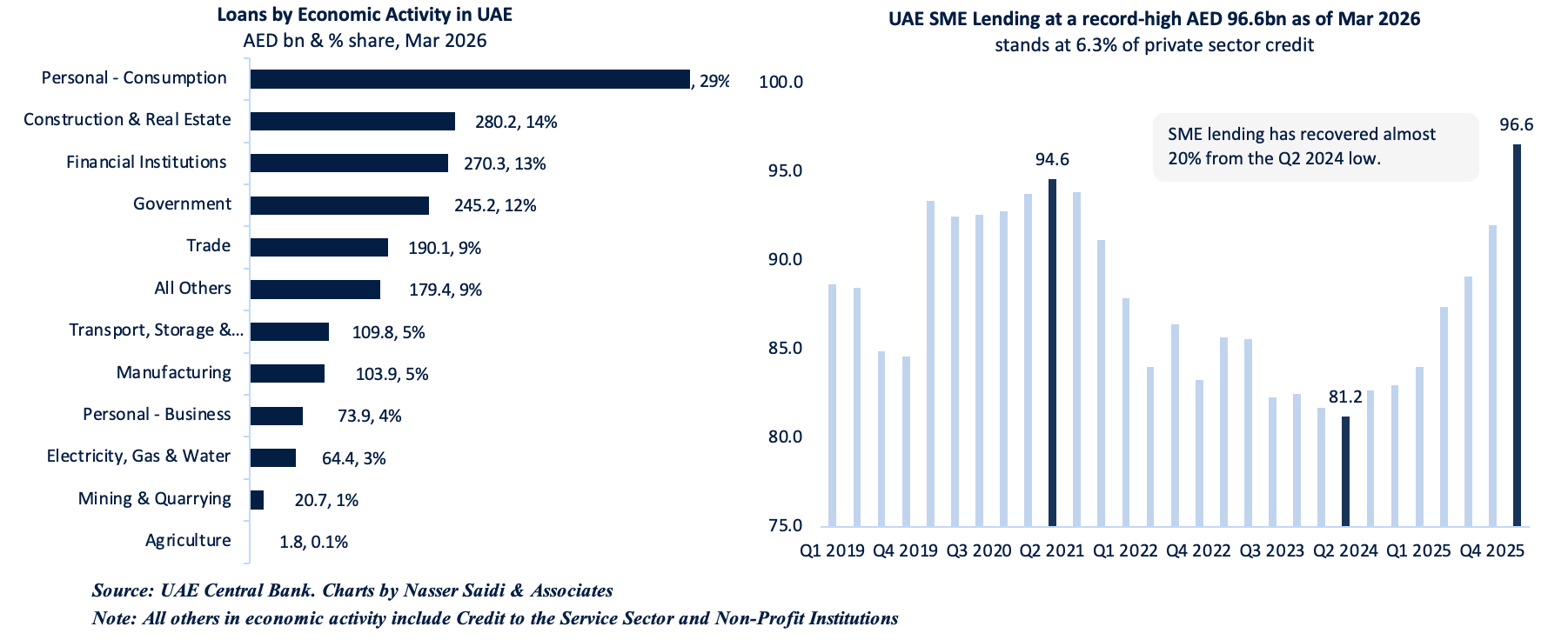

3. UAE headline credit growth strong in Mar, with prominent public-sector borrowing; SME lending at a record-high

- Gross credit expanded 2.5% mom to AED 2.7trn in Mar 2026, suggesting no immediate credit freeze despite the conflict-related uncertainty. Domestic lending was the main driver primarily supported by a 2.5% mom rise in domestic credit (rather than only external or non-resident lending).

- A stabilising public sector role was visible. Credit to the government sector rose 6.9% mom while lending to GREs were up 6.0%; private-sector credit in contrast rose just 1.1% – could be that firms may already be more cautious on borrowing, investment & capital commitments amid higher logistics and input-cost uncertainty.

- The war impact is not yet visible as an aggregate credit contraction. gross credit increased 4.9% qoq and 20.3% yoy in Q1 2026 while personal loans to residents rose 2.1% qoq & 14.6% yoy.

- Real estate & construction accounted for 13.7% of total lending in Dec 2025 (vs. 20% in 2021); fastest loan growth was reported in credit disbursed to the government (+33.6% yoy), financial services (33.2%), utilities (31.9%) & trade (10.1%).

- SME financing jumped by 5.0% qoq and 15.0% yoy to AED 96.6bn in Mar, the highest on record.

- Bottomline for now is that the Central Bank’s resilience package is giving banks liquidity, capital-buffer and loan-classification flexibility to keep credit flowing.

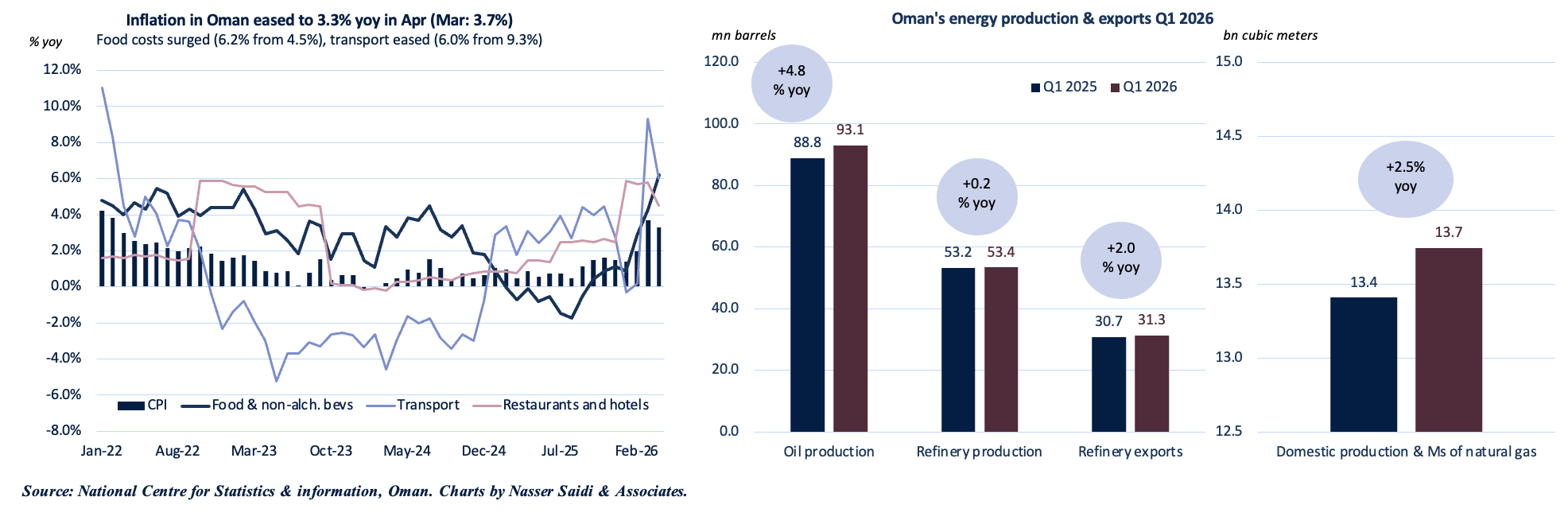

4. Inflation in Oman eases alongside expanding energy output & strategic logistics

- Headline CPI in Oman eased to 3.3% yoy in Apr, following Mar’s 3.7% (highest since Feb 2022). The food & non-alcoholic beverages segment emerged as a primary driver of domestic price hikes (6.2% yoy vs Mar’s 4.3%). Transport costs and miscellaneous goods & services costs remained high (6.0% and 9.2% respectively), though lower compared to Mar.

- Skyrocketing freight costs & war-risk insurance premiums => inflated cost of imported essentials => higher retail price of food.

- Oman has approved an OMR 50mn financial aid package for farmers & established regional food depots to stabilize domestic supply & support purchasing power.

- Oman is also successfully leveraging its geography by diverting essential trade to Salalah and Duqm ports + utilizing the Hafeet railway to create a secure, land-based supply chain for itself and its GCC neighbours.

- Oil production in Oman grew by 4.8% yoy to 93.1mn barrels as of end-Mar 2026. Average daily oil production saw a significant rise of 6.7% to 1.1mn barrels per day in Mar.

- Oman’s geography gives it more flexibility than other GCC producers heavily dependent on the Strait of Hormuz: this shows in oil exports up 3.2% yoy to 26.5mn barrels in Mar.

- Natural gas supply also rose, with total domestic production and imports of natural gas up 2.5% yoy to 13.7bn cubic meters by end-Mar. Industrial sector was the largest consumer of natural gas (share of 18.1%) followed by power generation (under 10%).

- Electricity generation also saw strong growth, with total surging 16% to 10,544 GWh. This suggests robust residential, commercial & industrial demand; but, if the war keeps fuel, shipping and equipment costs elevated, utilities & energy-intensive firms could face higher operating-cost pressure.

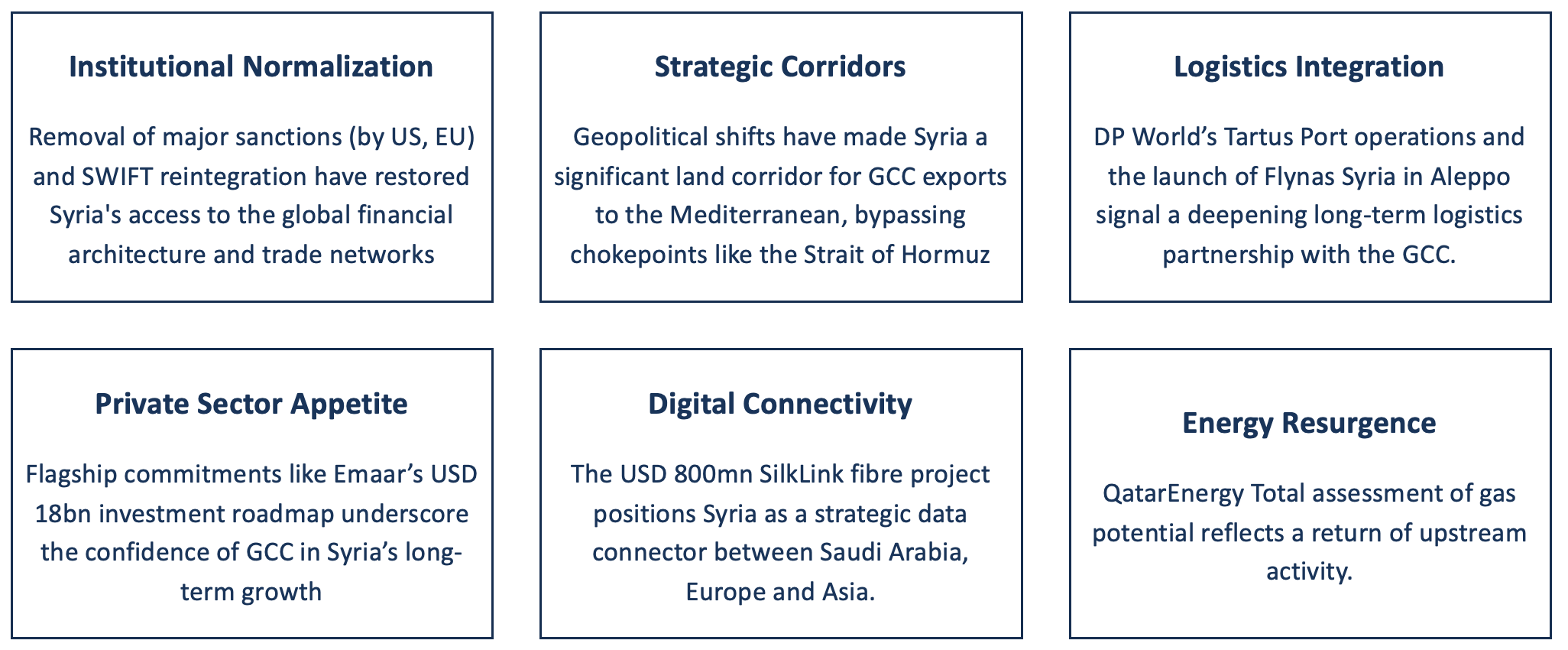

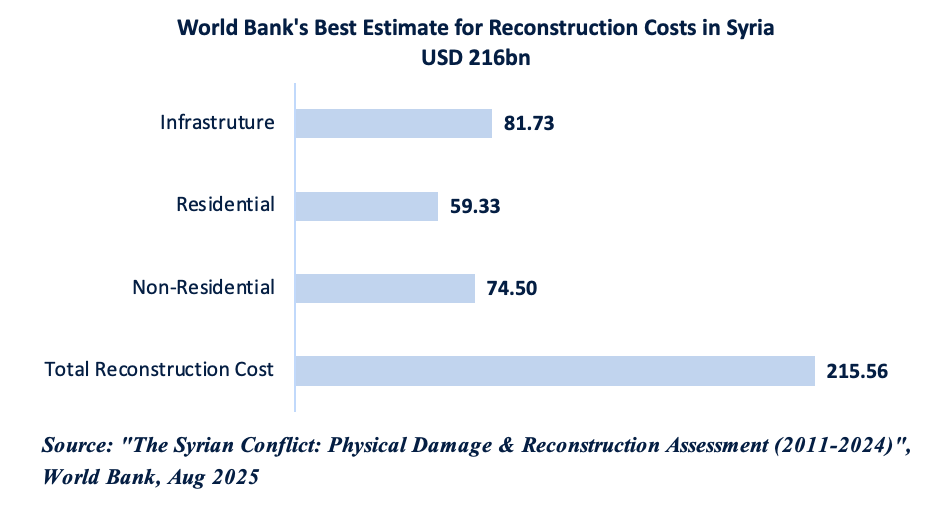

5. Gulf Confidence Pivot to Syria

Narrative Shift: Gulf investors are pivoting to Syria as the region’s primary reconstruction frontier

Slide based on comments provided to The National’s article https://www.thenationalnews.com/news/mena/2026/05/15/as-syria-moves-toward-economic-reopening-lebanon-remains-stuck-in-a-cycle-of-crises/

Powered by:

![]()