Hormuz Blockade Disrupts Commodity Markets, Trade Flows and Fiscal Dynamics, Weekly Insights 8 May 2026

Hormuz blockade & commodity prices. Middle East Apr PMIs. Saudi Q1 fiscal deficit. Qatar & UAE foreign trade.

Download a PDF copy of this week’s insight piece here.

Hormuz Blockade Disrupts Commodity Markets, Trade Flows and Fiscal Dynamics, Weekly Insights 8 May 2026

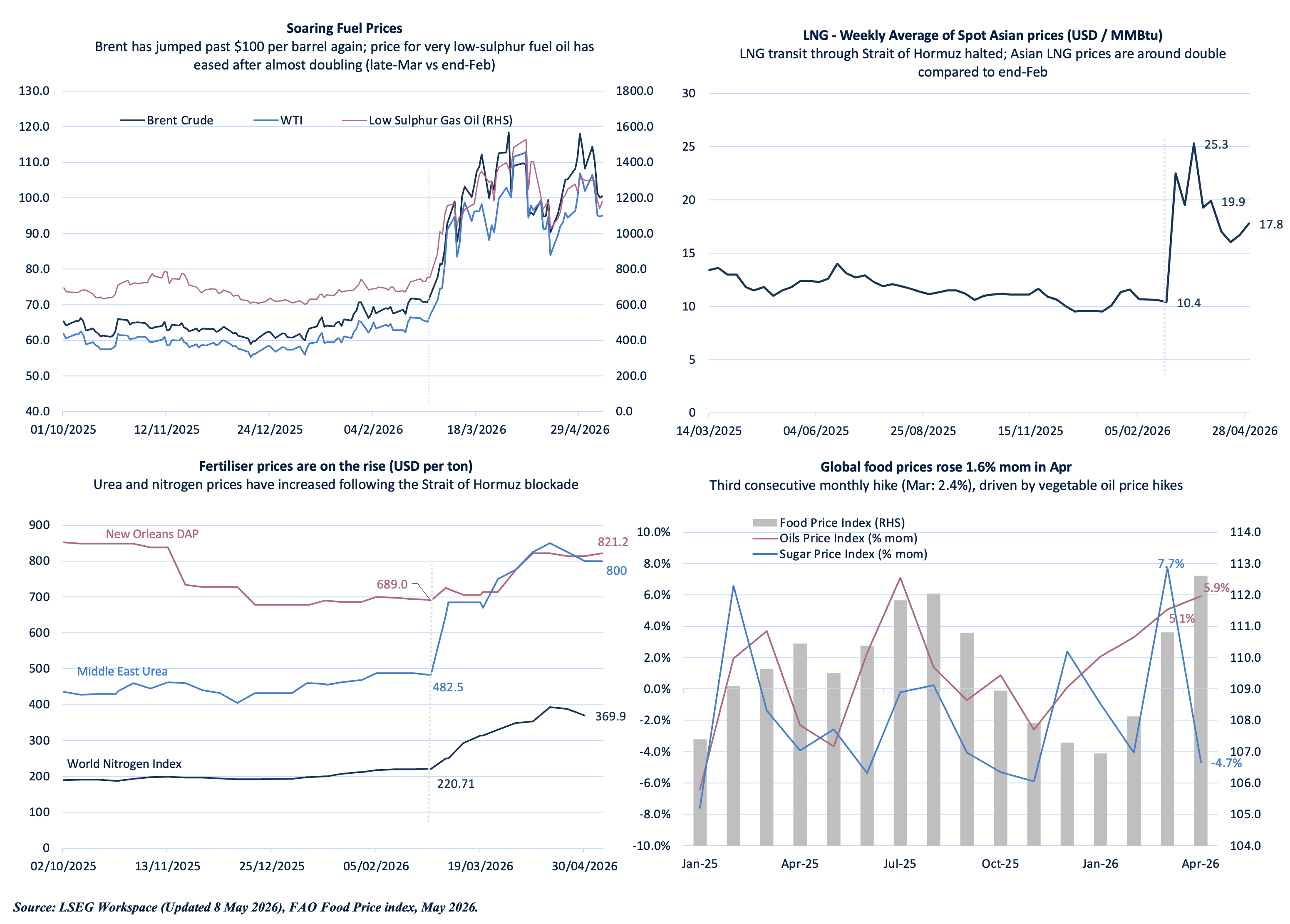

1. The Strait of Hormuz Blockade Continues to Spike Commodity Prices

- Beyond oil, supplies of critical inputs from aluminium to helium, sulphur and fertilisers (urea, ammonia, phosphates) are being disrupted leading to price hikes and spilling over into the agricultural and food markets, vehicles, semi-conductor and AI industries.

- Fuel-related pressures are visible in FAO’s food price index for Apr: it ticked up for the third month in a row (up 1.6% mom vs 2.4% in Mar), driven by increases in vegetable oil (5.9% mom and yoy).

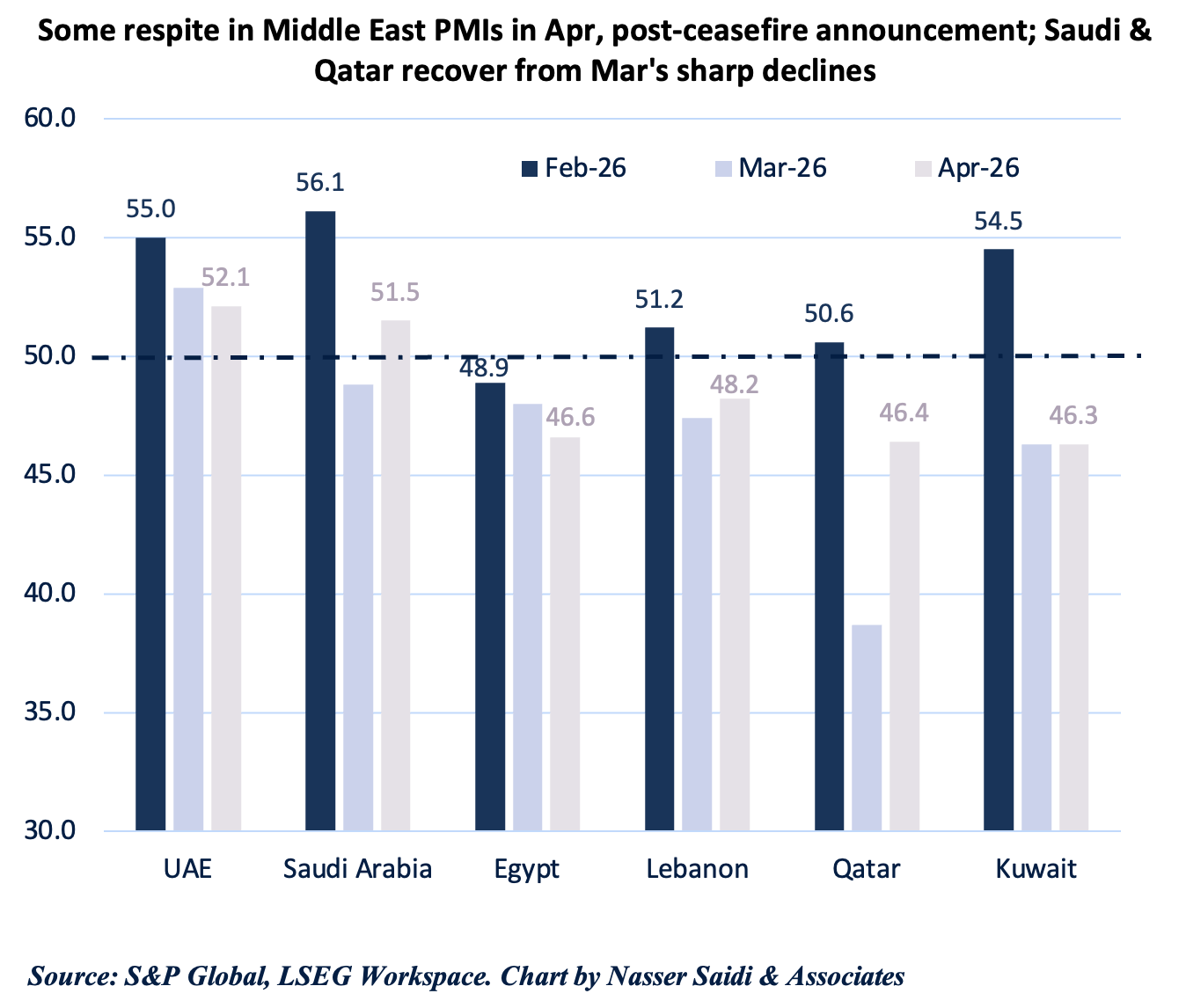

2. April headline PMI readings in the Middle East showed a mixed picture; but main messages remain slowing export orders & rising prices

- Regional PMIs reflect a significant divergence in resilience; while goods trade flows have been partially supported by safety stocks, service sector (specifically travel & hospitality) showed much deeper disruptions.

- Saudi Arabia and UAE maintained output growth by clearing existing backlogs and infrastructure projects; new orders in both reached multi-year or record lows. In Egypt and Kuwait, the contraction in output was sharper due to a collapse in consumer purchasing power and domestic logistical bottlenecks.

- New export orders have emerged as a primary indicator of distress, directly mirroring the collapse in shipping transits through the Strait of Hormuz.

- Firms across the region are facing a sharp surge in input costs, driven primarily by escalating energy, transport, and raw material expenses. In Saudi, prices rose the fastest since the survey began in Aug 2009. Firms are being forced to choose between passing on surging input costs (including high insurance premiums) to consumers or bearing significant operational losses. UAE firms raised selling prices at the fastest pace since 2011 while in Egypt firms hiked charges at the sharpest rate in nearly two years.

- Labour markets turned defensive. Egypt and Kuwait reported job shedding as firms retrenched to preserve liquidity. Hiring in UAE and Saudi Arabia remained positive but moderated significantly, as firms opted to manage existing project pipelines rather than expand headcounts amidst regional uncertainty.

- Twelve-month ahead business sentiment was cautious, as the temporary ceasefire does not resolve the underlying Hormuz blockade or the risk of future attacks / escalation. Slight optimism/ less pessimism was visible across some GCC nations, potentially due to proactive government action, longer-term expansion & infrastructure development plans.

- For businesses & investors, key signals of stabilizing confidence will be the normalization of war-risk insurance premiums and a verifiable increase in daily tanker transits versus pre-war levels.

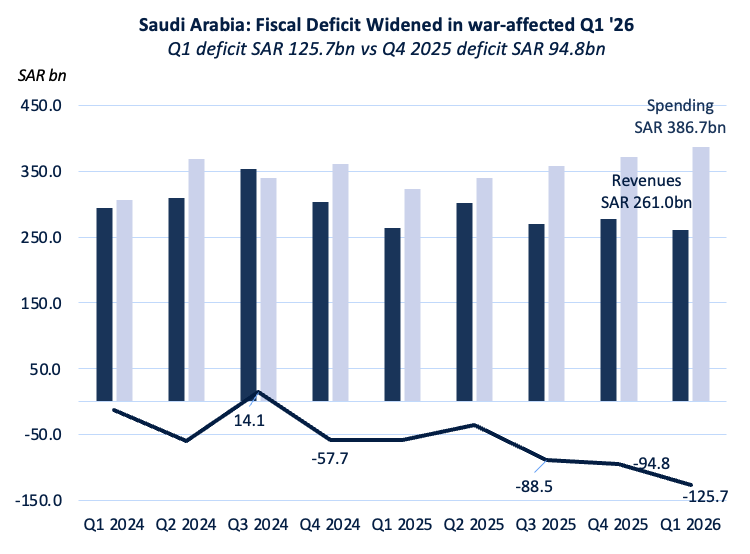

3. Saudi Arabia deficit in Q1 2026 more than doubled to SAR 125.7bn, as spending climbed by 20% amid the regional conflict

- Saudi Arabia posted a budget deficit of SAR 125.7bn in Q1 2026, more than double versus a year ago & the largest quarterly deficit on record.

- Total expenditures climbed 20% yoy to SAR 386.7bn, driven by a 26% rise in military spending (to SAR 64.7bn) and a massive three-fold increase in subsidies (to SAR 17.5bn) to mitigate conflict-driven cost-of-living pressures.

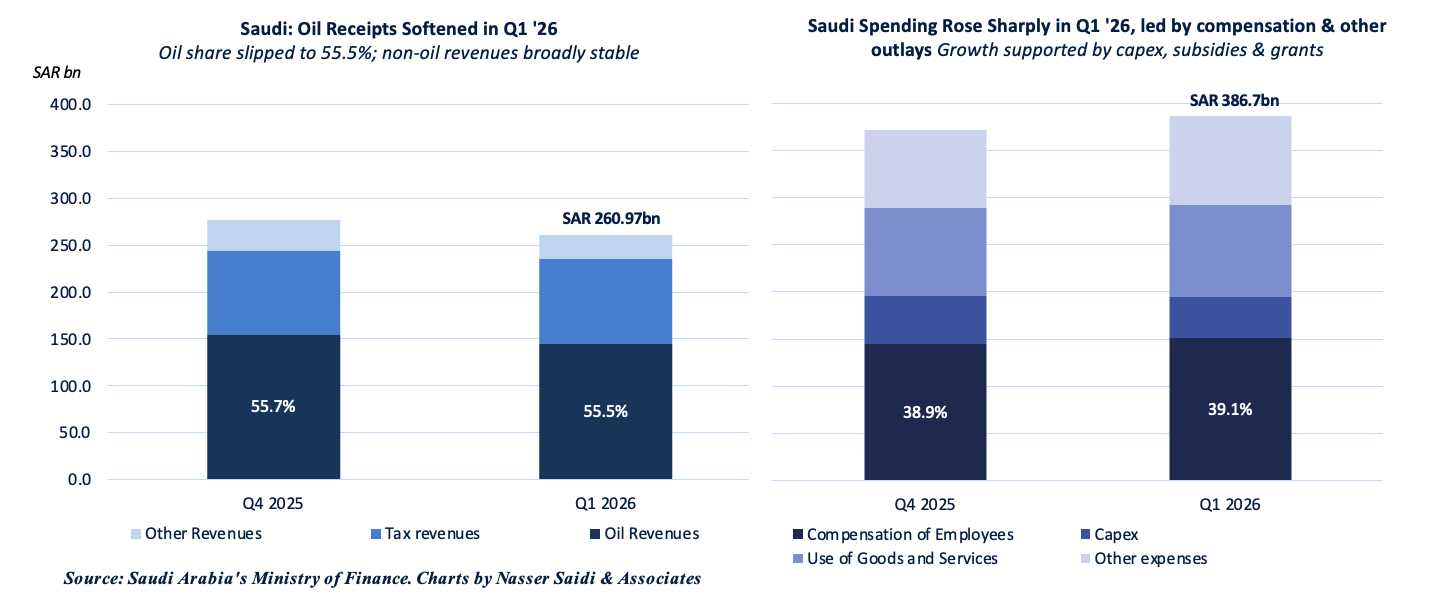

- Total revenues edged down by 1.0% yoy to SAR 261bn, hampered by a 3% decline in oil income (to SAR 144.7bn) as the blockade of the Strait of Hormuz and regional infrastructure damage impacted export volumes.

- The non-oil fiscal base remained resilient despite the ongoing conflict. Non-oil revenues rose 2.1% to SAR 116.3bn, supported by taxes on goods and services (+4.7% yoy to SAR 74.9bn). This highlights the success of continued efforts to diversify the fiscal base beyond crude oil.

- Capex grew 56% yoy to SAR 43.4bn, confirming major contracts were going ahead.

- Deficit was fully financed through borrowing, causing total public debt to rise to SAR 1.67trn by end-Mar

- Full impact of the war is likely to be more visible in Q2.

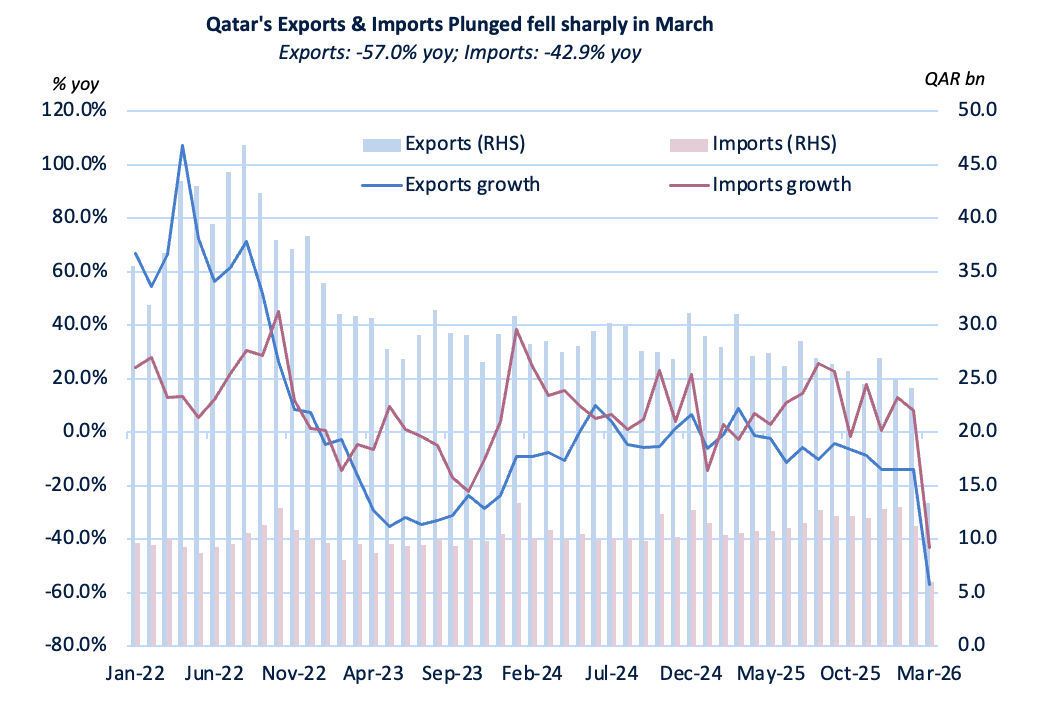

4. Qatar foreign trade almost halved in March; outlook subdued in 2026

- Qatar recorded a total trade surplus of QAR 32.2bn for Q1 2026, with total exports at QAR 62.5bn and imports valued at QAR 30.3bn.

- The abrupt March trade collapse reflects regional shipping disruptions and energy infrastructure damage. Both exports and imports nearly halved in Mar: exports plunged 45% mom to QAR 13.3bn) & imports fell by 46% to QAR 6.1bn.

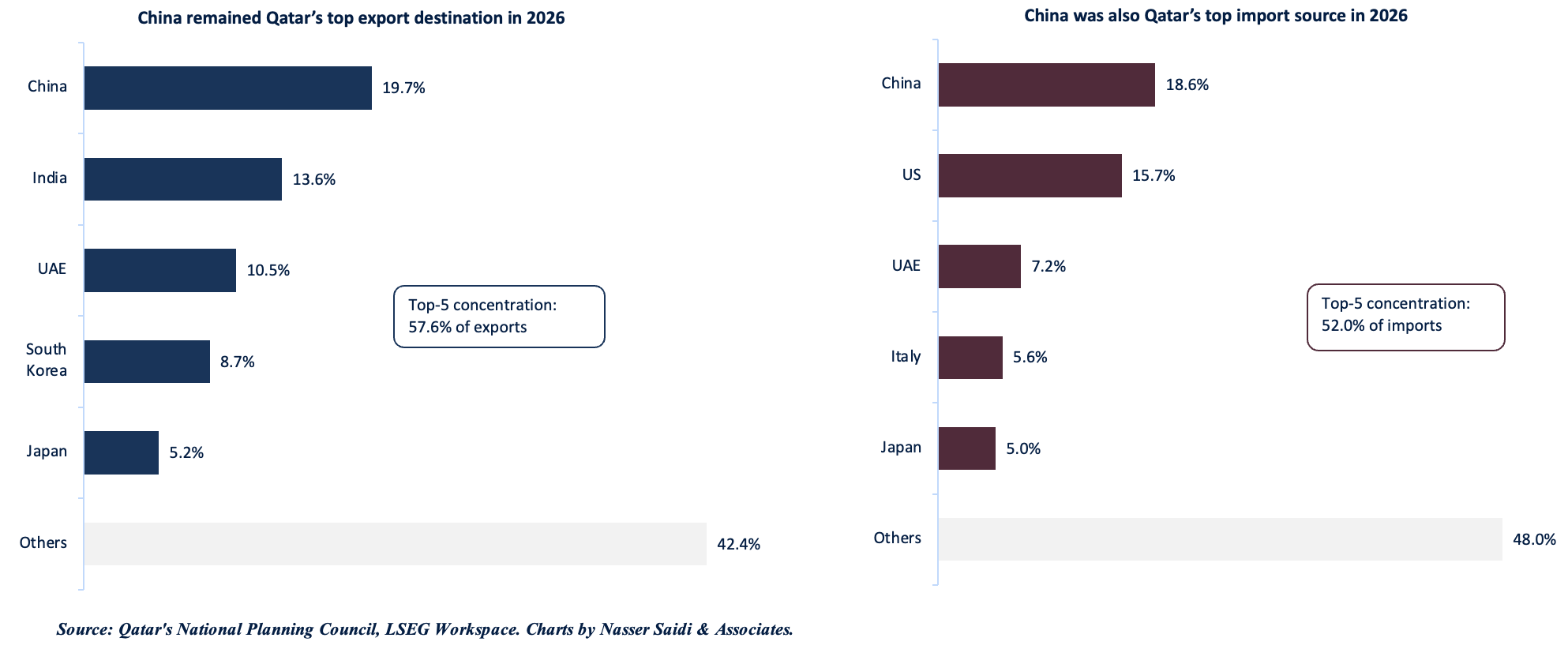

- Energy exports remained heavily weighted toward the East in Q1. Major exports destinations (for all products) were China, India, UAE, South Korea and Japan.

- To maintain national food reserves, Qatar relied on a diverse global supply chain, including major poultry imports from Brazil, rice from India and significant livestock shipments from Saudi Arabia.

- The import profile was dominated by high-tech equipment and industrial materials – from the US and China.

- Regional non-oil trade continued. Despite the disrupted security environment, non-oil trade with regional neighbours persisted, with Saudi Arabia and the UAE remaining key partners for livestock, dairy, and industrial re-exports throughout Q1.

- With full restoration of production at Ras Laffan expected to take years, not months, lost trade revenue is a given. However, there are some bright sparks: North Field Expansion is expected to come onstream next year despite delays & production from the Golden Pass LNG project is expected to start by end-2026.

- Non-oil trade re-routing via land corridors, exploration of new, alternative export channels (Turkey, Egypt) & enormous fiscal buffers to finance reconstruction should support trade flows in the meantime.

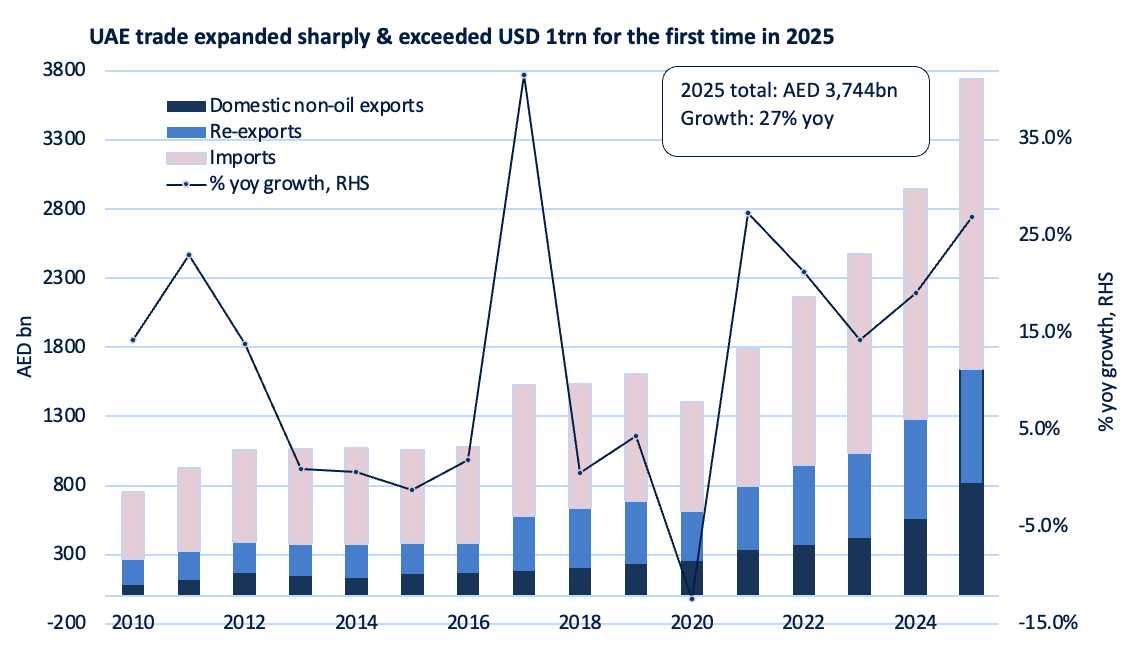

5. CEPAs and industrial exports boosted UAE non-oil foreign trade in 2025

- UAE’s non-oil foreign trade surged 27% yoy to a record-high AED 3.744trn in 2025. This performance was supported by a widening trade surplus (+19% to AED 584.1bn). WTO data show that UAE climbed to 9th globally in goods exports and 13th in imports during 2025; trade in services exceeded AED 1.14trn for the first time.

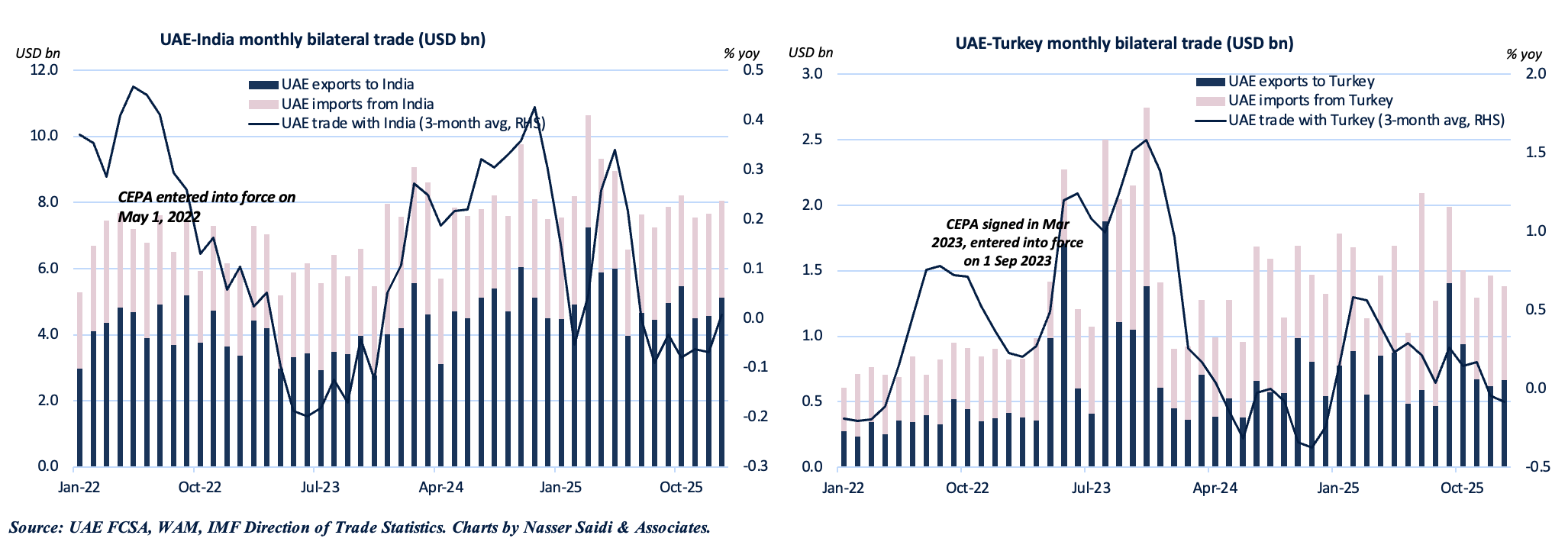

- UAE trade volumes are less correlated with oil prices, thanks to diversification efforts via products (non-oil exports, re-exports) and new markets (Comprehensive Economic Partnership Agreements or CEPAs). The UAE has concluded 36 CEPAs to date, with notable results with India and Turkey.

- Surge in Industrial Exports and Localisation: industrial (non-oil) exports reached AED 262bn in 2025, up 25% yoy. Simultaneously, the In-Country Value program successfully redirected AED 473bn+ back into the economy, strengthening domestic manufacturing capacity.

- In the backdrop of the war, UAE continues to invest in modernising its trade infrastructure: it is launching a first-of-its-kind integrated AI system to link all local and global components of the foreign trade ecosystem.

Powered by:

![]()