Massive downgrades in IMF’s growth forecast; GCC estimates too optimistic: Weekly Insights 17 Apr 2026

Massive downgrades in IMF’s growth forecast; GCC estimates too optimistic, Weekly Insights 17 Apr 2026

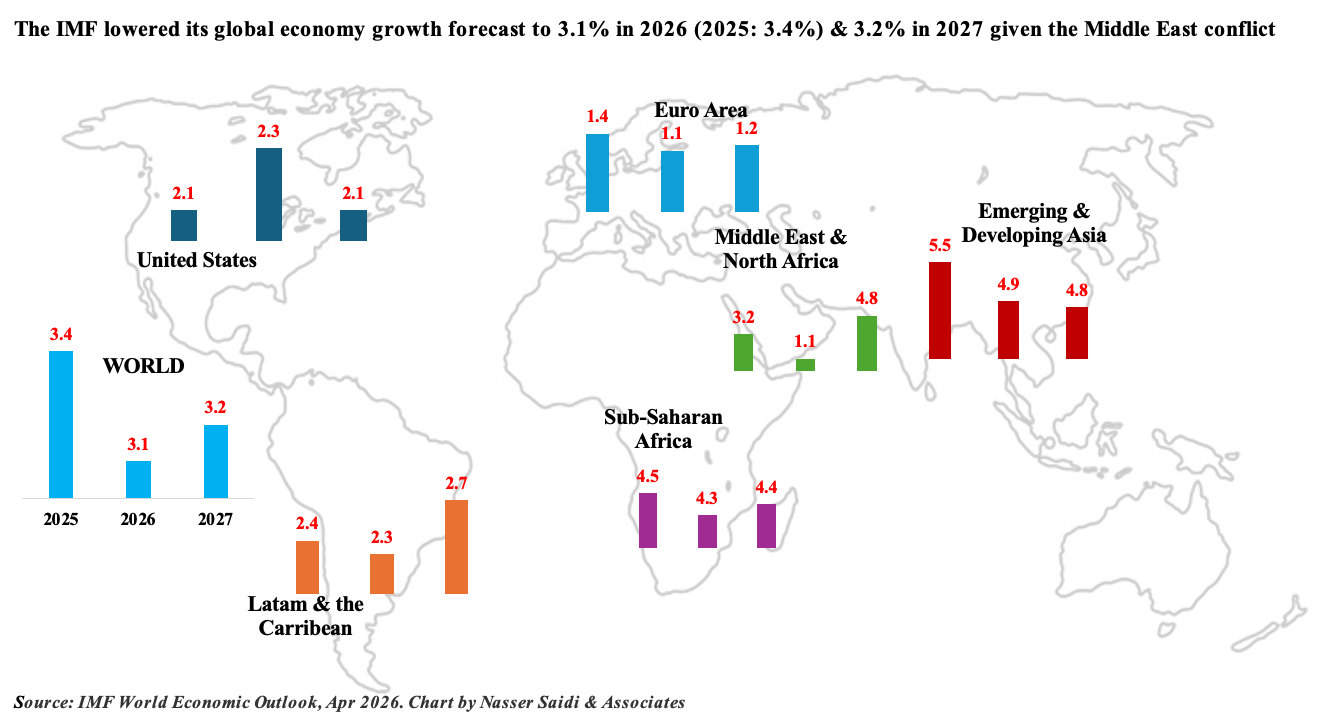

1. Global economy will slow to 3.1% in 2026, an impact from the war in Iran: IMF

- Under the assumption that the Middle East conflict remains limited (reference scenario), IMF projects global economic growth to slow to 3.1% in 2026 (2025: 3.4%) before ticking up to 3.2% in 2027 – figures that remain well below pre-pandemic averages. However, in a severe scenario, involving broader & longer regional instability, IMF warns growth could be constrained to 2.0% this year and next.

- Emerging market economies (EMEs) was the worst hit, with growth projected at 3.9% in 2026 and 4.2% in 2027 (2025: 4.4%); growth rates in Middle East & North Africa significantly revised down compared to Oct 2025 (1.1% and 4.8% in 2026 and 2027, from 3.2% in 2025) while Sub-Saharan Africa remained relatively stable (4.3% and 4.4% from 4.5% in 2025). Growth in Emerging Asia is estimated to slow (2026: 4.9% vs 5.5% in 2025), as growth slows in India (6.5% from 7.6%) and China (4.4% from 5.0%). Asia, given high dependence on O&G exports and commodities such as urea and helium from the GCC, are among the most affected by the war in Iran.

- Global headline inflation is expected to tick up modestly to 4.4% in 2026 (reference scenario) but compares to over 6% under the severe scenario. These pressures are particularly acute in emerging markets and developing economies, especially for commodity importers facing higher energy costs. Any changes to trade policy will have a spillover effect on global growth.

- Many additional downside risks are outlined including: (a) Intensification of conflicts and/or political tensions; (b) extended shocks to supplies of essential raw materials; (c) trade disruptions; (d) disappointment in the profitability of (and so a collapse of investment in) AI; (e) prolonged fiscal deficits & ever greater accumulations of public debt; and (f) damage to crucial institutions notably central banks among others.

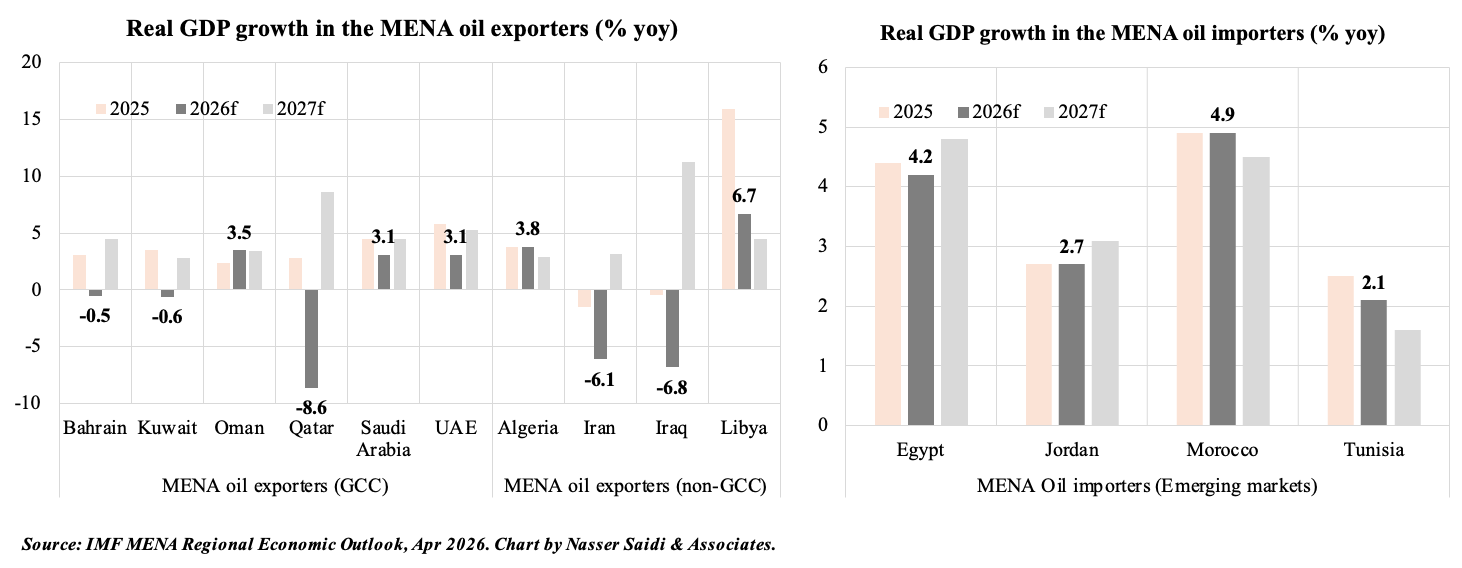

2. Adverse effects from the Iran war plunges growth in the MENA region, especially GCC

- IMF’s forecasts are on the optimistic side. There has been differential impact on the region (based on logistical resilience & infrastructure exposure). For oil and gas exporters most exposed to the hostilities, the IMF projects significant economic contractions in 2026: Iran (-6.1%), Iraq (-6.8%) and Qatar (-8.6%) – driven by damage to energy infrastructure and the functional closure of the Strait of Hormuz.

- Saudi Arabia, UAE & Oman are expected to maintain positive growth, though at reduced rates. Saudi Arabia and Oman’s growth forecasts were moderately lowered, given its relative less vulnerability due to alternative export routes and significant fiscal buffers.

- Oil exporters such as Algeria and Libya stand to benefit from the higher oil prices as its export movements are not dependent on the Strait.

- Regional oil importers like Egypt and Jordan will feel the impact from surging commodity prices. Egypt’s growth projection was cut to 4.2%, as the country grapples with higher import costs and a potential decline in remittances from workers in the GCC.

- The IMF has refrained from issuing a formal 2026 projection for Lebanondue to the direct impact of the war, noting that the shock is immediate and the extent of infrastructure damage in the south is still being assessed.

- Across the region, the scaling up of defence spending to address geopolitical tensions is expected to weaken fiscal & external sustainability. For energy and food importers, power & fuel subsidy bills will strain fiscal space; high levels of debt & tighter financial conditions may raise debt financing costs. Such countries will require external intervention and access to liquidity & financial facilities.

- While a regional rebound to 4.8% growth is forecast for 2027, this is entirely predicated on the assumption that energy production and transportation will be normalized within the next few months. Expect further downgrades can be expected at the July update.

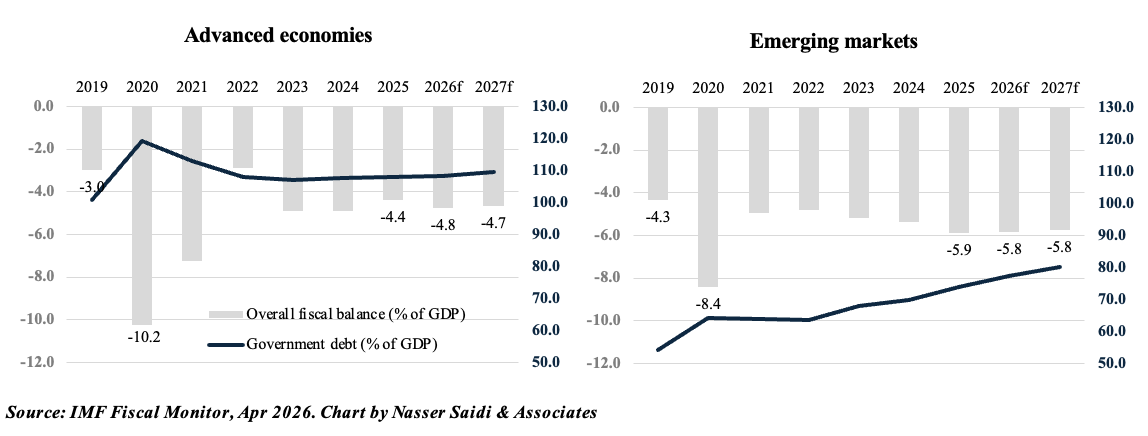

3. Global public debt is on a path of continued accumulation

- The IMF’s Fiscal Monitor highlights that scaling up defence spending in response to geopolitical tensions can often worsen fiscal sustainability and increase public debt by 14 percentage points while crowding out essential social spending.

- Global public debt is on a path of continued accumulation: rose to just under 94% of GDP in 2025 and is set to reach 100% by 2029, a year earlier than projected in Apr 2025. The IMF notes that current levels are comparable to the peaks seen after World War II.

- The conflict in the Middle East could further strain government finances through higher food and fuel prices, tighter financial conditions, lower economic activity and rising defence spending.

- Total US debt alone is expected to reach USD 38.8trn in 2026, heightening vulnerabilities and potentially eroding the traditional safe-haven status of US Treasuries. While the USD has seen upward pressure due to its safe-haven appeal, persistent inflation and high debt levels could lead to a crash in bond markets if institutional credibility is eroded.

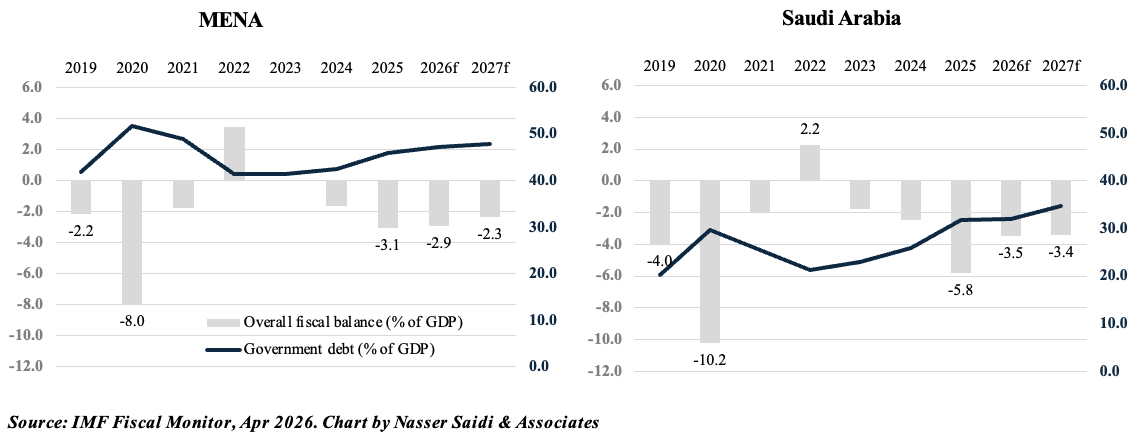

4. Conflict in the Middle East could further strain government finances

- Fiscal balances in the MENA region will continue to record deficits in 2026-27 (after posting a surplus 0.2% of GDP in 2023), with Saudi Arabia running fiscal deficits (3.4% in 2026-27 though lower than 5.8% in 2025). This also reflects increase in interest expenses.

- Public debt levels in MENA have been rising for almost a decade: more than half the countries have higher than pre-pandemic debt to GDP levels.

- Fiscal pressures will arise from four main channels in 2026: lower revenues, larger energy subsidy bills, potential refugee-related spending & higher borrowing costs.

- Among GCC, Bahrain’s public debt as share of GDP is the highest (147.6% in 2025, rising to 157.3% in 2026) while Oman has seen a sharp decline (an estimated 35.8% in 2025 from close to 70% in 2020).

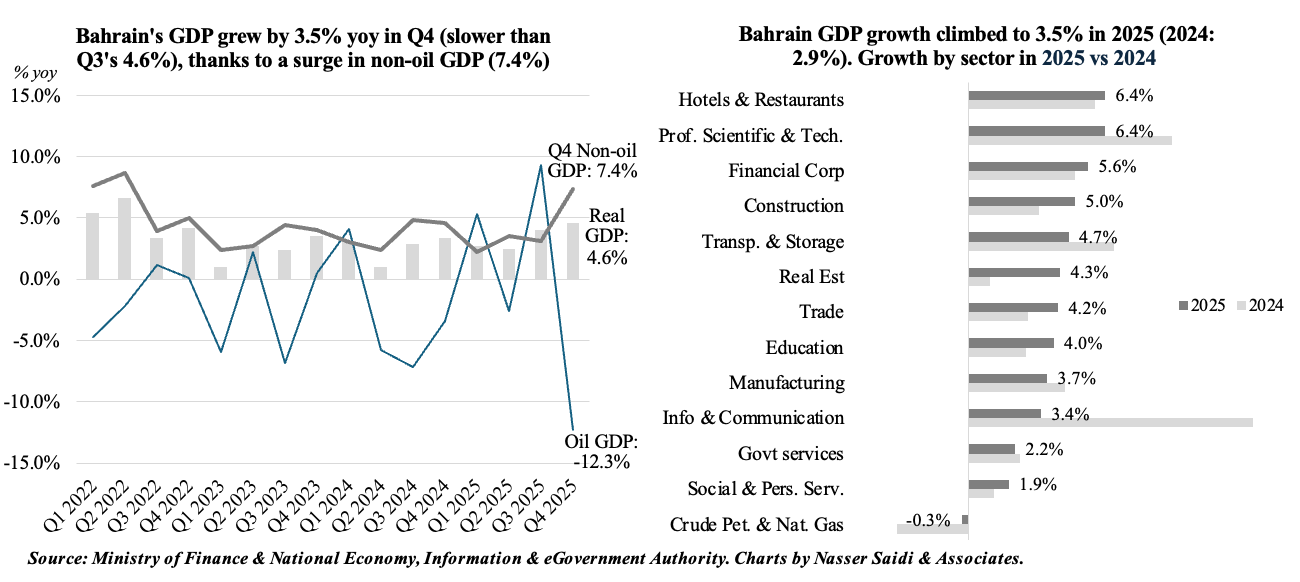

5. Bahrain’s GDP grew 3.5% yoy in 2025, thanks to a non-oil sector boost (4.1%). Middle East conflict to lead to GDP contraction in ‘26; fiscal pressures to accelerate

- Bahrain’s real GDP grew by 3.5% yoy to BHD 17.87bn in 2025. Non-oil GDP growth accelerated in Q4 2025 (7.4%), propping up overall growth rate of 4.6% (amid a 12.3% drop in crude oil & petroleum activity.

- The non-oil sector contributed 85.8% of Bahrain’s total GDPat constant prices in 2025; financial and insurance activities was the largest contributor (17.6%) followed by manufacturing (15.1%) and public administration (8.4%). In 2025, oil-related activities contracted 0.3% while the non-oil sector surged by 4.1%. The financial sector acted as a critical anchor, growing by 5.6% and a primary contributor to inward FDI stock (65% of total inward FDI stock at BHD 11.6bn in Q4).

- The war in Iran has radically altered this trajectory, with GDP now projected to contract in 2026. The closure of the Strait of Hormuz in early March stranded aluminium and oil exports (which collectively provide over two-thirds of government revenue). The situation was further worsened by direct damage to industrial assets: the Sitra refinery was attacked twice, dashing hopes for increased oil production; aluminium production at Alba had shutdown 19% of its capacity in early March.

- Bahrain is facing rising fiscal pressure due to increased security spending and the need to protect critical desalination infrastructure (supplies 90%+ of potable water in the country). To maintain monetary stability, Bahrain signed an AED 20bn central bank currency swap agreement with the UAE (to support cross-border transactions). The Central Bank also rolled out a loan deferral & liquidity support program.

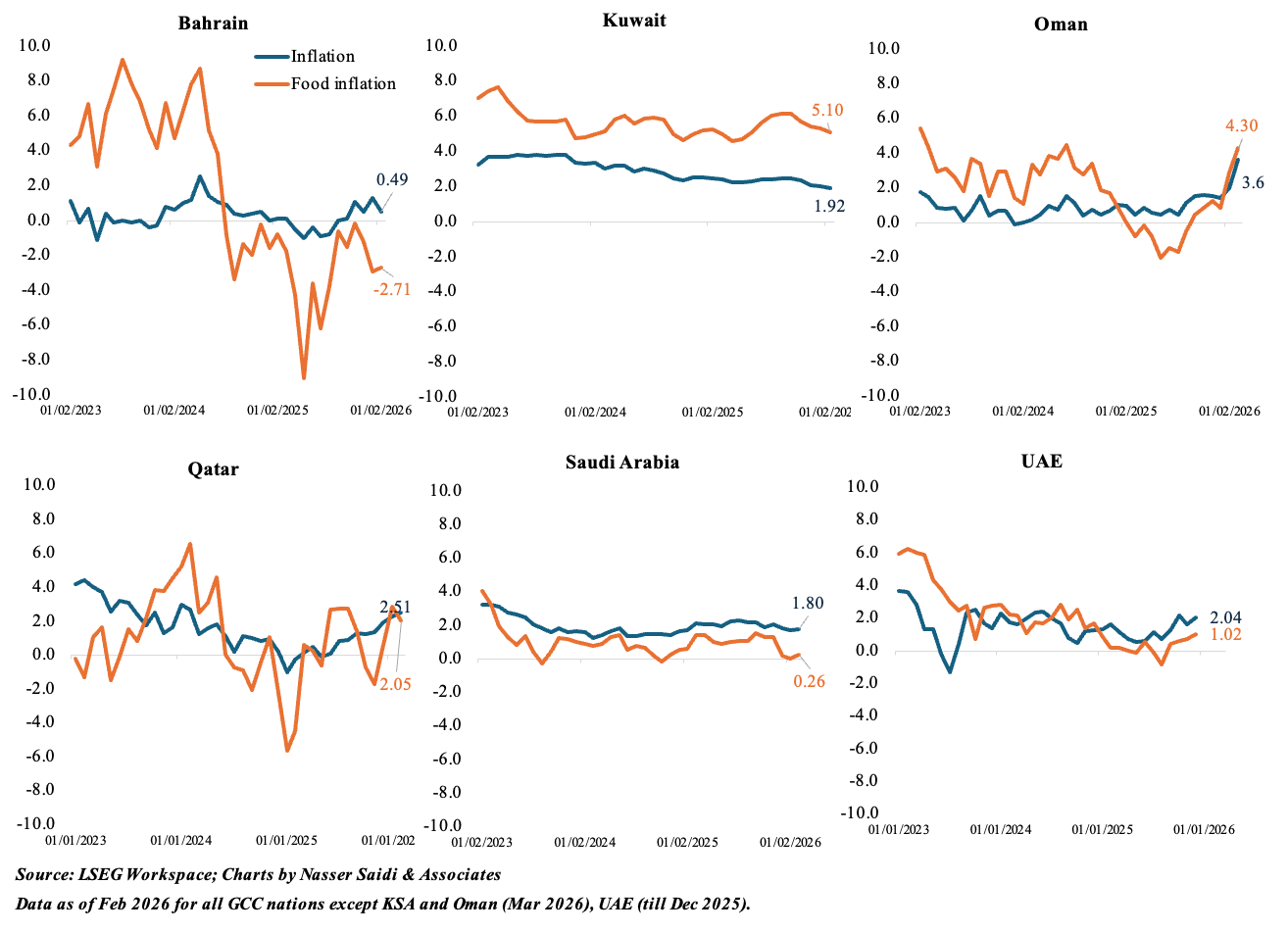

6. GCC headline inflation remains relatively low vs MENA peers: Saudi & Oman posted upticks in Mar (1.8% and 3.6% resp) but was lower than Egypt’s 15.2%; for Feb, GCC’s highest was in Qatar (2.5%) vs 12.3% in Lebanon. Food inflation is inching up across the board. Given the war in Mar, many GCC countries introduced price controls to prevent runaway inflation (due to supply changes)

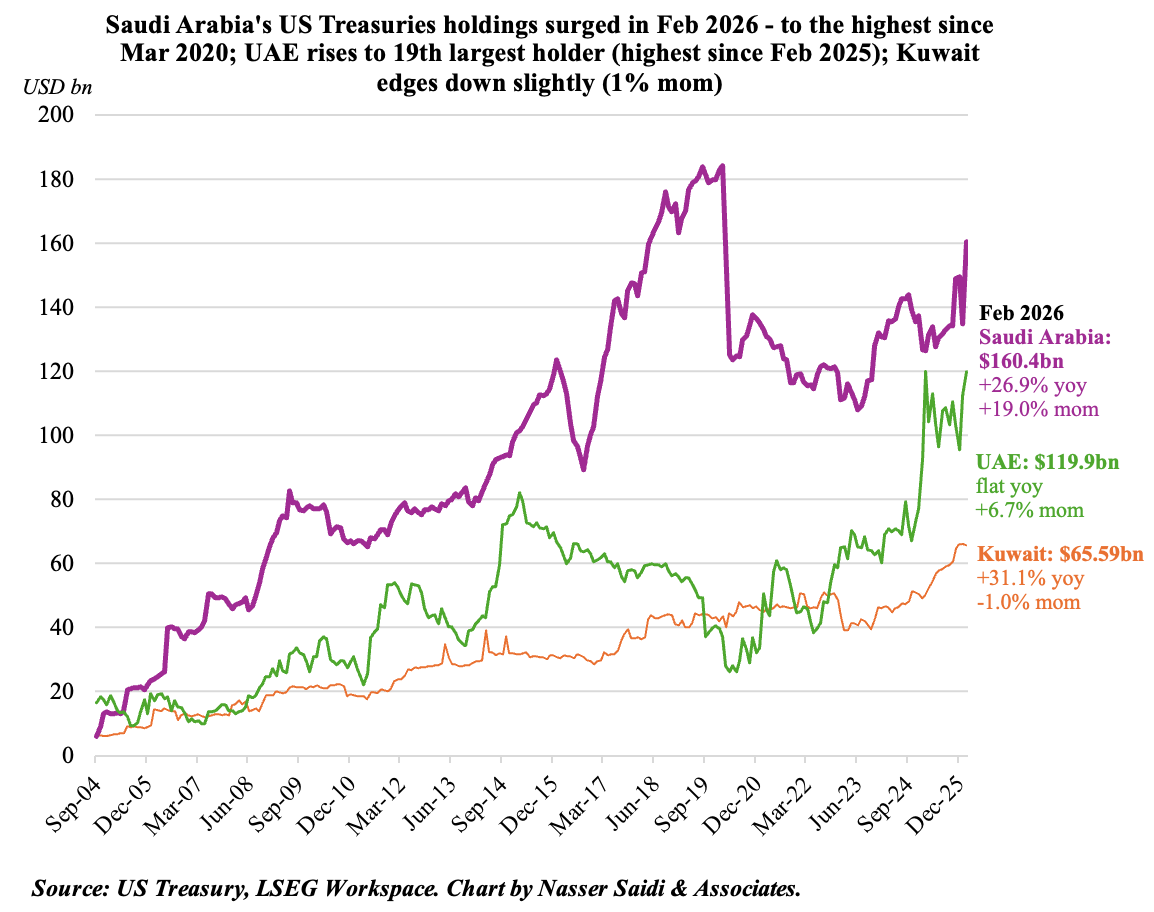

7. Saudi Arabia US Treasuries holdings surge in Feb; UAE’s climbs to 19th globally

- Foreign holdings of US Treasury securities reached a record USD 9.49trn in Feb (2.1% mom).

- IMF issued a stark warning that the massive surge in US debt (expected at USD 38.8trn in 2026) is eroding Treasuries safe-haven premium it once commanded. This erosion is evidenced by narrowing spreads between Treasuries & AAA-rated corporate bonds. The Iran war has already cost USD 200bn+ & there is no debt consolidation plan yet

- Japan continued as the dominant holder of US Treasury securities (USD 1.2395trn, its largest reading since Feb 2022). China continues to trim its exposure to US debt: holdings fell 9% since the start of 2025 to USD 693.3bn in Feb.

- Saudi Arabia’s holdings of US Treasuries surged by 26.9% yoy & 19% mom to USD 134.8bn in Jan, the most since Mar 2020. Saudi ranked 17th globally, rising one place ahead of South Korea which decreased its holdings (to USD 140.9bn). UAE increased its holdings further to USD 119.9bn (6.7% mom & flat in yoy terms), the highest since Feb 2025, to become the 19th largest holder globally. Kuwait’s holdings dipped slightly to USD 65.59bn (-1% mom). Higher percentage holdings by GCC is also a reflection of lower holdings by China and others, resulting in higher relative shares.

- FT reported that Abu Dhabi, Qatar & Kuwait raised nearly USD 10bn through private placements of US dollar bonds in Apr.

Powered by:

![]()