Ceasefire: But, No Early Return to Normalcy, Weekly Insights 10 Apr 2026

Ceasefire & impact. Weak Middle East PMIs. Post-war thoughts on KSA IP & Qatar GDP.

Download a PDF copy of this week’s insight piece here.

Ceasefire: But, No Early Return to Normalcy, Weekly Insights 10 Apr 2026

1. Impact of the 14-day fragile ceasefire announcement

- Immediately after the fragile ceasefire was announced, there was a spike in global equity and bond markets and regional indices (e.g. Dubai saw its highest intraday gain in 11 years this week). However, market reaction is an overly optimistic relief rally rather than a structural upward trend, unless war is called off by all parties and long-standing issues resolved. This is unlikely to be resolved in the next few weeks.

- The sharp drop in oil and gas prices is almost entirely due to the removal of the threat of “obliteration”, though a geopolitical risk premium will remain entrenched for the foreseeable future. Brent crude was down 12.7% this week (steepest since Aug 2022) & WTI was down 13.4% (the most since Apr 2020)

- Despite the ceasefire, a return to normalcy will likely take months; major shipping lines remain cautious, noting it will take at least six to eight weeks to regain a normal network. Shipowners require firm security assurances before exiting and re-entering the Strait of Hormuz. War risk insurance rates remain high.

- Around 60+ energy infrastructure assets in the GCC were hit by drone and missile strikes. Recovery is hindered by physical damage to energy, transport and digital infrastructure inflicted during the conflict (e.g. outages to major digital services like AWS).

- QatarEnergy expects it would take about 5 years to repair & restore 17% of its damaged capacity.

- UAE’s Emirates Global Aluminium & Bahrain’s Alba: account for nearly half of the GCC’s aluminium capacity. After being hit in end-Mar EGA expects 12 months to restore its output & Alba had announced a controlled shutdown of 19% of its capacity before the attacks. Kpler’s optimistic scenario has only “20% of curtailed capacity to return in Q4”.

- Impact on Saudi facilities – attacks on the East-West Pipeline took out 700kbpd; also disrupted refining and liquids exports at Ras Tanura, Yanbu, Jubail and Riyadh.

- Inflationary pressures: Even with lower fuel costs, the six-week price spike has already seeped into industrial, manufacturing and logistics costs. Industrial and consumer price inflation and higher core inflation will remain a primary challenge for central banks for months to come, raising the risk of higher interest rates along with lower economic growth rates. The risk of Stagflation is growing.

- FAO food price index ticked up in Mar (2.4% mom) and further increases in oil and fertiliser prices are expected to push more people to acute food insecurity. Food price inflation exceeded overall inflation in 57.1% of more than 140 countries tracked by the World Bank between Q4 2025-Q1 2026.

- Fiscal strain on food & energy importers: the ceasefire not resolve the depreciation of exchange rates, capital outflows, or the fiscal strain caused by higher debt, energy prices and subsidy bills.

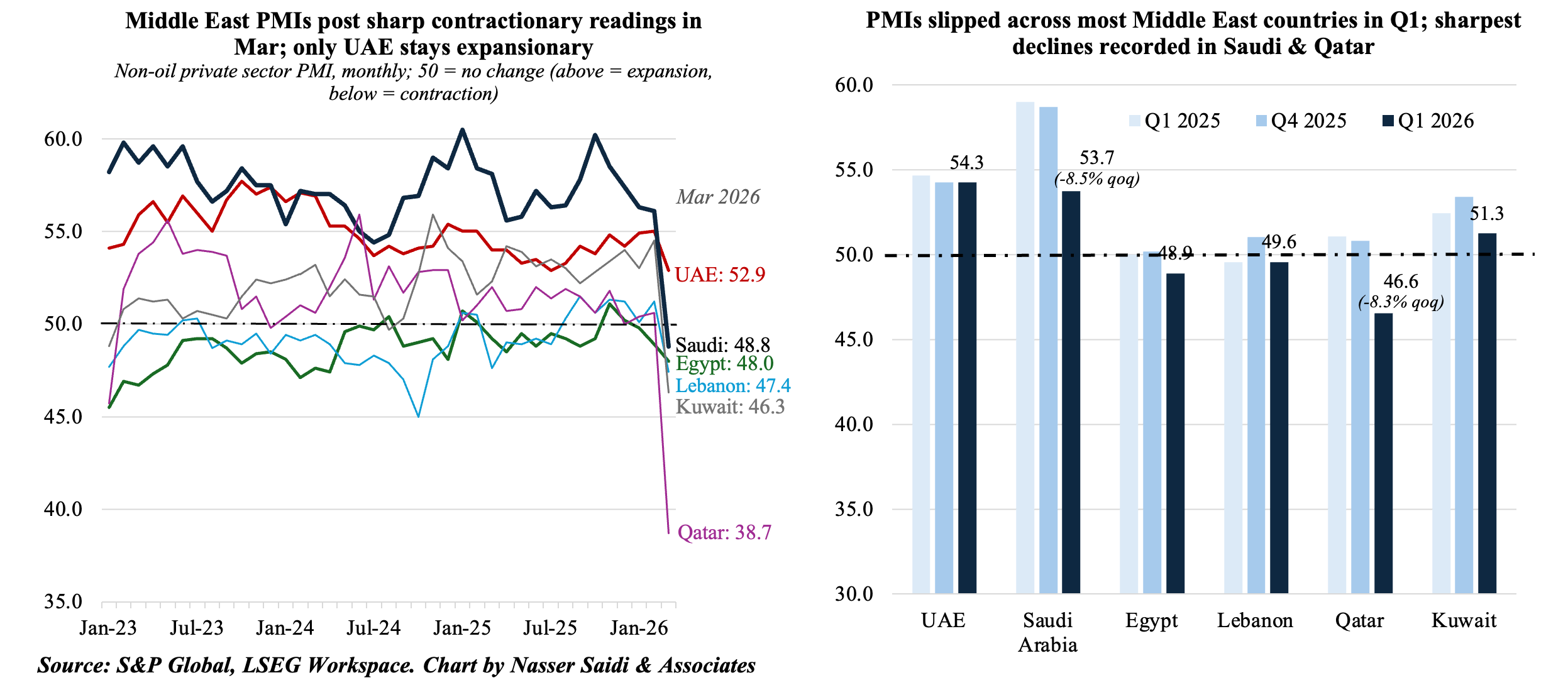

2. March PMI readings in the Middle East shows weakening momentum everywhere

- Headline PMIs across the Middle East showed UAE as the only economy still in technical expansion; the sharpest declines were recorded in Qatar (11.9 points), Kuwait (8.2 points) and Saudi (7.3 points). Egypt and Lebanon plunged deeper into contraction.

- Output weakened sharply across the region, with Saudi Arabia recording the steepest one-month decline in output its PMI survey’s history. UAE’s output was at its weakest pace since mid-2021; Egypt & Lebanon slipped into outright contraction as higher energy costs and security risks disrupted production and day-to-day operations.

- New orders effectively stalled, with firms and clients delaying spending and new commitments. Export demand was the hardest-hit, reflecting the immediate trade shock from the disruption of Gulf shipping routes. Kuwait and Qatar saw external demand weaken sharply as sea freight options disappeared, while Saudi Arabia’s non-oil exports, particularly petrochemicals and plastics, faced acute logistical bottlenecks.

- Input cost pressures intensified: in UAE and Saudi Arabia, the main driver was procurement and transport (given higher war-risk insurance, rerouted shipping and supply-chain disruption). In Egypt and Lebanon, currency weakness and import costs also played a role.

- Labour markets also turned more defensive. Hiring slowed in Kuwait and Qatar (19-month low).

- Business expectations fell to a five/six-year lows; in Qatar, 70% of respondents expect a decline in output in the next 12 months. The regional picture shows weakening momentum everywhere. Lebanon remains in entrenched crisis conditions, with macroeconomic and financial stress alongside humanitarian strain.

- World Bank estimates GCC growth to slow to 1.3% in 2026 (2025: 4.4%) & MENAP (excluding Iran) to grow by 1.8% (2024: 4.0%).

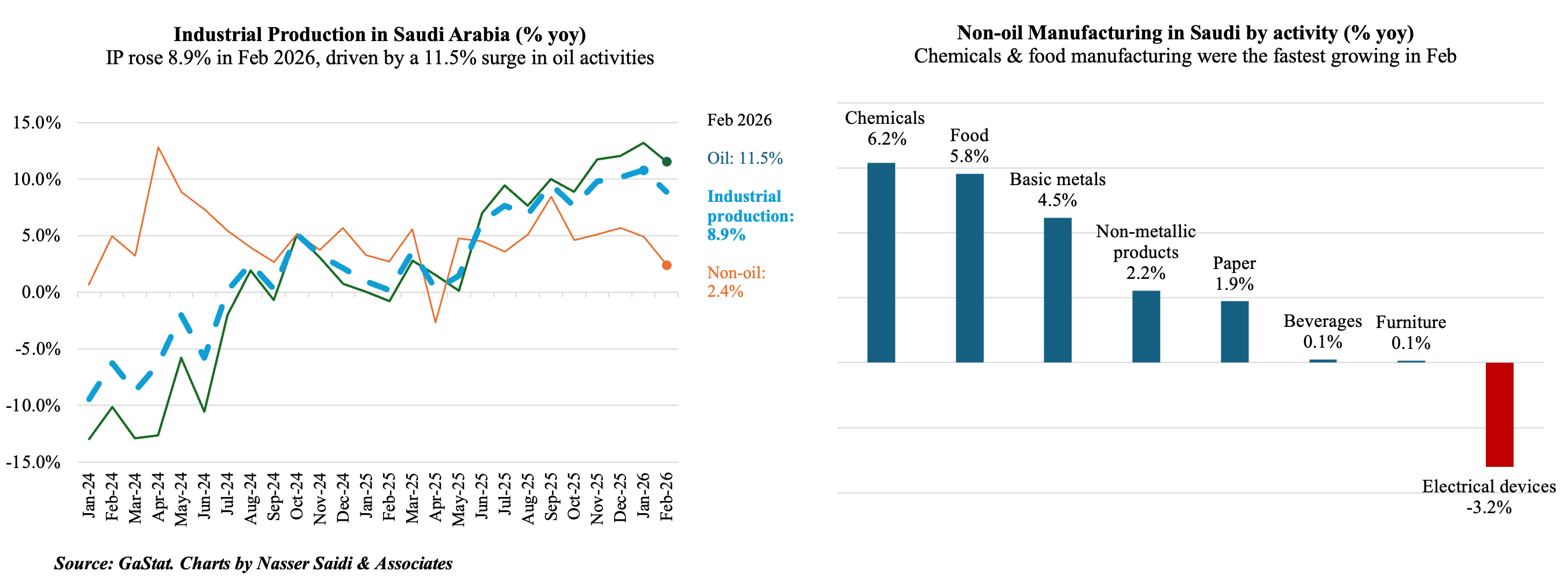

3. Saudi Arabia: Strong Feb industrial data to give way to a war-driven hit to exports & revenues

- Saudi Arabia’s Industrial Production Index rose 8.9% yoy in Feb 2026, led by mining and quarrying (+13.0%), while manufacturing expanded 3.6% and the oil activities index rose 11.5%; versus 2.4% growth in non-oil activities.

- The Feb strength was closely tied to higher crude output: Saudi oil production rose to 10.1mn barrels per day (bpd) in Feb, supporting industrial activity before the regional conflict began to weigh on sentiment and operations in March.

- OPEC+ increase is unlikely to translate into meaningful near-term supply gains: although a modest 206k bpd output increase was agreed for April, this was quickly overtaken by war-related disruptions.

- Export disruption rather than production policy is key. With the Strait of Hormuz blockade, Saudi Arabia’s crude export capacity had become heavily dependent on the East-West Pipeline (carrying oil to the Red Sea, operating at full 7mn bpd capacity). The pipeline was hit on day ceasefire was declared, reportedly reducing its throughput by 700k bpd.

- Direct attacks on oilfields and refineries imply a material loss of export revenues: strikes have cut Saudi oil production capacity by around 600kbpd & throughput on its East-West Pipeline by about 700kbpd; also disrupted refining and liquids exports (at Ras Tanura, Yanbu, Jubail and Riyadh); will slow production of coke, refined petroleum products & chemical products. Altogether, this points to weaker oil export revenues, tighter fiscal conditions and softer industrial data from Q2 2026 onward.

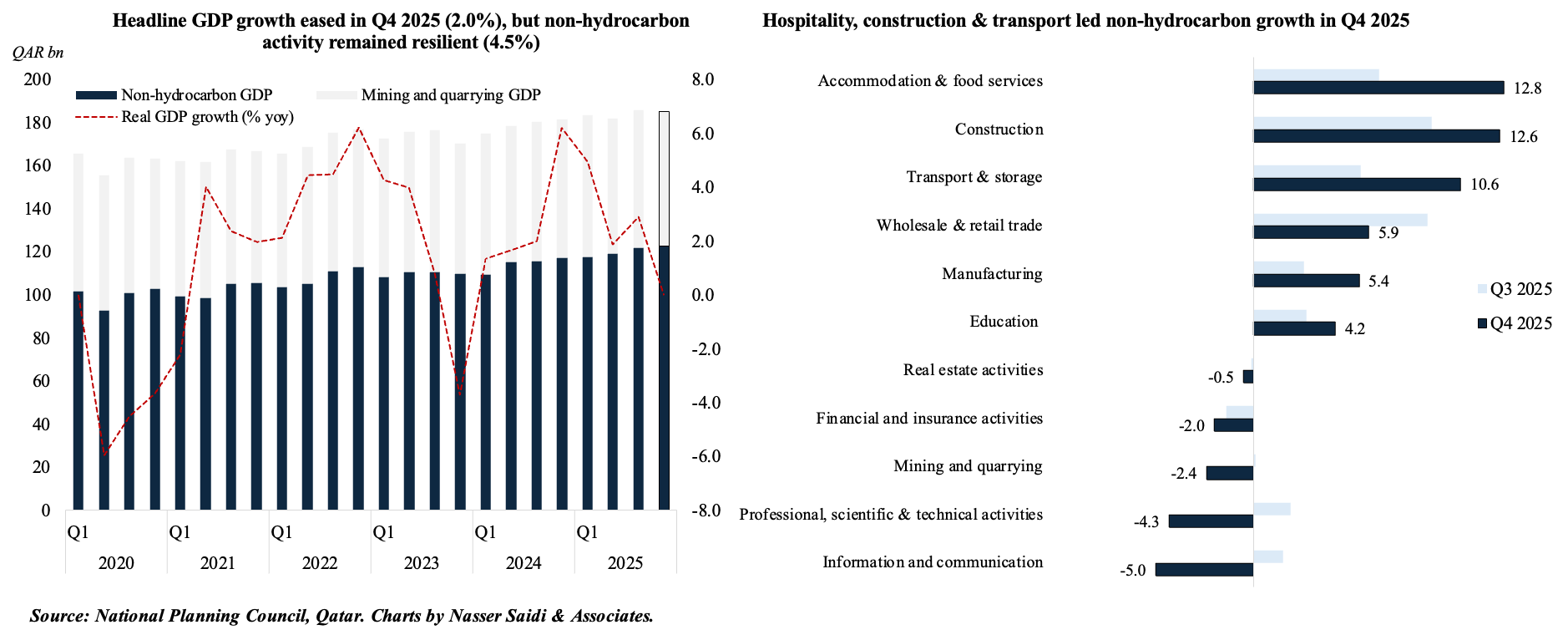

4. Qatar: Energy-sector disruption drives a sharp deterioration in 2026 outlook

- Real GDP growth in Qatar eased to 2.0% yoy & 2.9% qoq in Q4 2025; weakness in mining and quarrying (-2.4%) outweighed robust non-hydrocarbon growth (+4.5%).

- The conflict has triggered a major supply shock: attacks on Ras Laffan reportedly knocking out approximately 8 million tonnes per annum of LNG capacity, or about 17% of Qatar’s export capacity (leading to an estimated revenue loss of USD 20bn). At that time, it was stated that repairs to the facilities could take up to five years (due to delays in replacement of the gas turbines). For reference, the entire plant has the capacity to produce 77mn tons of LNG a year.

- Trade and logistics disruptions have amplified the shock, with the Strait of Hormuz effectively closed and regional energy shipments severely constrained. Qatar’s top buyers in Asia are either shifting trade partners (e.g. India turning to Russia) or changing products (e.g. Japan’s move to coal) to meet domestic demand.

- Qatar’s real GDP is now projected to contract in 2026 (World Bank estimate: -5.7%), with hydrocarbon activity likely to remain under pressure for months even after hostilities ease, given repair timelines and shipping bottlenecks.

- Medium-term risks are rising. Delays to the North Field Expansion & force majeure on some long-term contracts raise downside risks to export revenues, capital expenditure and sovereign risk perceptions.

Powered by:

![]()