Geopolitical Shockwaves, Energy Markets & Global Growth, Weekly Economic Commentary 9 Mar 2026

Download a PDF copy of the weekly economic commentary here.

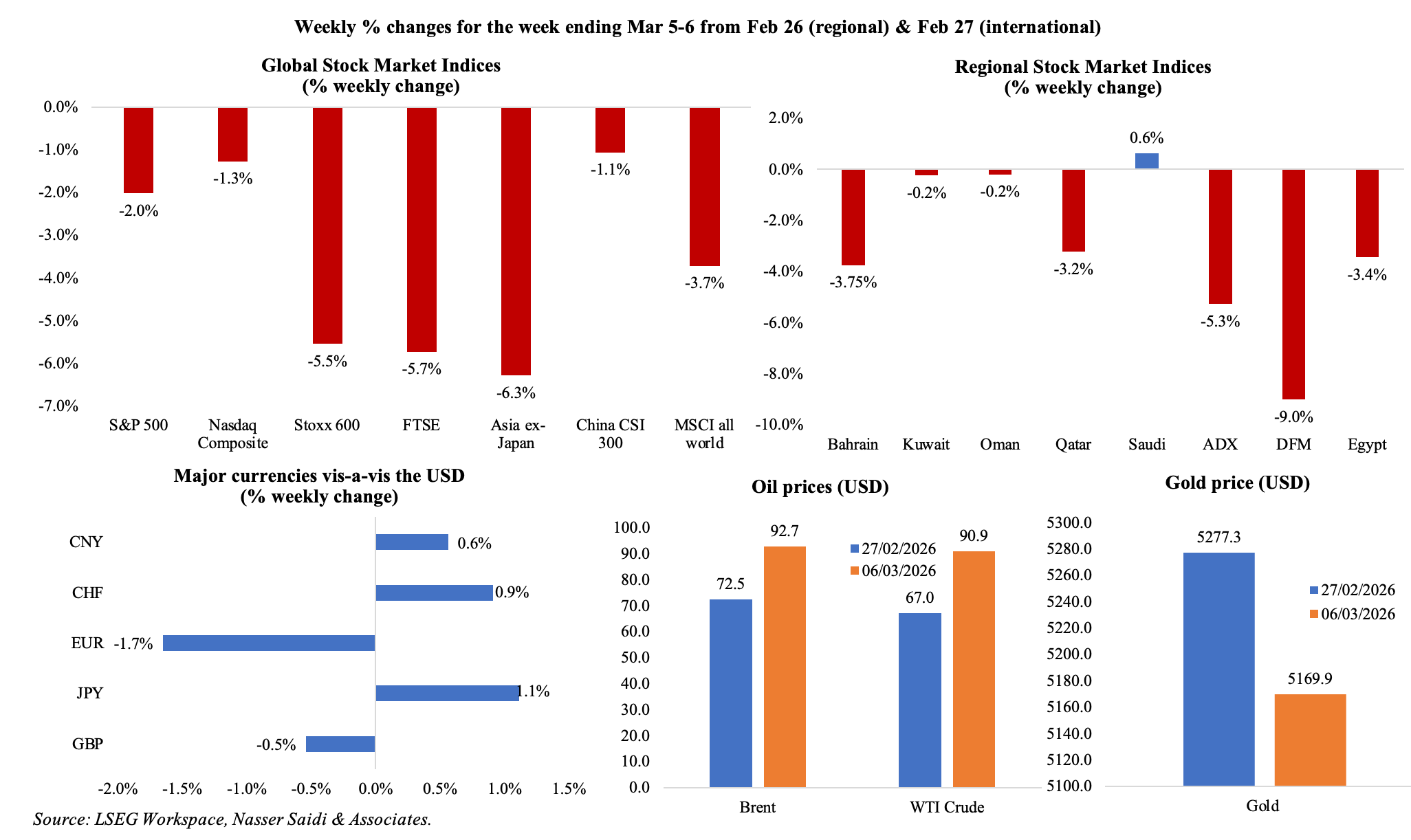

Markets

As the conflict in the Middle East further deepened, equity markets bore the brunt: S&P 500’s weekly drop of 2% was the largest weekly loss since mid-Oct, while Stoxx600’s and MSCI Asia ex-Japan’s declines of 5.5% and 6.3% were the most in almost a year and six years respectively. In the region, Saudi’s Tadawul managed to end slightly higher on the back of elevated energy prices, while Bahrain, Egypt and Qatar ended in the red, UAE’s DFM and ADX extended their losses closing 9.0% and 5.3% lower compared to the prior week. Though an unexpected drop in US payrolls cooled the USD rally, it remained one of the main beneficiaries of the geopolitical uncertainty alongside safe-haven Swiss franc; the GBP and the EUR pulled back. The conflict saw global oil prices rise to multi-year highs amid fears of a prolonged Hormuz shutdown: Brent closed at USD 92.69 a barrel, the highest since Oct 2023 and up 27% weekly while WTI surged 35.6%. Oil prices jumped to as high as USD 119 a barrel today Mar 9th (last seen in 2022) before easing slightly. Gold ended the week lower after five weeks of gains as the stronger dollar and concerns about Fed’s policy limited its gains. Investors are now pricing in a protracted period of geo-economic instability, resulting in an evident flight to safe-haven assets.

Global Developments

US/Americas:

- Recent labour market data suggest gradual slowing in US employment conditions. Nonfarm payrolls unexpectedly tumbled in Feb, down 92k following Jan’s downwardly revised 126k gain: this was the sixth drop since Jan 2025 and the second largest so far. The healthcare and leisure & hospitality sectors lost 28k and 27k jobs respectively. Average hourly earnings ticked up 3.8% yoy in Feb (Jan: 3.7%). Labour force participation rate eased slightly to 62%, the lowest reading since Dec 2021 (Jan: 62.1%). Unemployment rate inched up to 4.4% in Feb (Jan: 4.3%).

- Non-farm productivity grew at a 2.8% annualised rate in Q4, slowing from the 5.2% uptick in Q3, while unit labour costs were up 2.8% (Q3: -1.8%). Average productivity growth stood at 2.2% in 2025, slowing from the 3.0% increase in 2024. Moderating wage pressures and still-solid productivity growth should help ease inflation risks, supporting expectations of a soft landing.

- Private sector in the US added 63k jobs in Feb, the most since Jul (Jan: 11k), thanks to education & healthcare sectors (adding 58k) followed by construction (19k) and information (11k). ADP also disclosed that pay premium for switching employers hit a record low in Feb.

- Initial jobless claims held steady at 213k in the week ended Feb 28, with the 4-week average slipping 4.75k to 215.75k. Continuing jobless claims increased by 46k to 1.868mn in the week ended Feb 21.

- Fed Beige book showed slight to moderate growth in seven out of 12 districts while sales dampened due to greater economic uncertainty, “increased price sensitivity” and high-income households driving most of the growth as lower-income consumers pulled back on spending. Though tariffs increased costs for businesses in nine of the twelve districts, manufacturers reported increase in new orders amid strong demand for data centres and energy infrastructure.

- Retail sales grew 3.2% yoy in Jan (Dec: 2.4%) though in monthly terms sales fell 0.2% (the first drop since Oct). Sales at motor vehicles and auto part dealerships fell in Jan (-0.9% mom), as did sales at gas stations (-2.9%).

- S&P Global manufacturing PMI in the US ticked up to 51.6 in Feb compared to the preliminary reading of 51.2 though slowing from Jan’s 52.4. New orders and output continued to rise, albeit at slower rates, though respondents stated that higher prices, tariffs and adverse weather conditions were affecting demand. Services PMI slipped to 51.7 (from 52.3) as labour intensive sectors continue to be dragged down by worker shortages, high costs and low consumer confidence”.

- ISM manufacturing PMI declined to 52.4 in Feb (Jan: 52.6) as new orders eased (55.8 from 57.1) as did production (53.5 from 55.9) while employment rose (48.8 from 48.1) and prices paid surged to the highest since Jun 2022 (70.5 from 59).

- ISM services PMI jumped to 56.1 in Feb (Jan: 53.8), the most since Aug 2022, thanks to the surge in new orders (to a 17-month high of 58.6 from 53.1) and employment (51.8 from 50.3) and prices paid slipped (63 from 66.6).

Europe:

- Eurozone GDP grew by 0.2% qoq and 1.2% yoy in Q4, slower than previous estimates. For the full year 2025, GDP grew by 1.5% following a 1.1% gain in 2024. The highest growth rates were recorded in Ireland (+12.3%), Malta (+4.0%) and Cyprus (+3.8%) while Germany and Finland in contrast posted the lowest (+0.2% each).

- Inflation in eurozone inched up to 1.9% in Feb (Jan: 1.7%), as services inflation accelerated to 3.4% (from 3.2%) and non-energy industrial goods inflation rose (0.7% from 0.4%). Energy prices declined (-3.2% from -4.0%) alongside steady prices of food, alcohol & tobacco (+2.6%). Core inflation also moved higher to 2.4% (vs Jan’s more than 4-year low of 2.2%).

- Producer price index in euro area fell by 2.1% yoy in Jan (Feb: -2.0%), staying negative for the sixth month in a row.

- Retail sales in the EU grew 2.3% yoy in Jan (Dec: 2.0%), with non-food product sales rising 2.9% (Dec: 2.5%) while fuel sales eased (2.0% from 3.2%).

- Manufacturing PMI in the eurozone recovered to a 44-month high 50.8 in Feb (Jan: 49.5), thanks to a rise in new orders and stronger output. Despite input costs surging to a 38-month high, business confidence jumped to a 4-year high. Services PMI ticked up to 51.9 from 51.8.

- German manufacturing PMI moved up to 50.9 in Feb (prelim: 50.7; Jan: 49.1), supported by increases in output and new orders while employment eased and input prices rose to the most in over three years. Services PMI inched up to 53.5 (prelim: 53.4; Jan: 52.4) though job losses increased at the fastest pace since Jun 2020.

- Retail sales in Germany increased 1.2% yoy in Jan (Dec: 2.5%). In monthly terms, sales shrank by 0.9% mom in Jan (Dec: +1.2%), as prices of non-food sales declined (-1.7%) alongside flat food sales.

- UK manufacturing PMI eased to 51.7 in Feb (prelim: 52; Jan: 51.8), with new orders and output improving alongside decline in employment while input prices rose to a 6-month high.

Asia Pacific:

- NBS manufacturing PMI in China declined to 49 in Feb (Jan: 49.3), the lowest since Oct, partly disrupted due to the Chinese New Year holidays. New orders and foreign sales fell sharply to 48.6 and 45.0 respectively (from 49.2 and 47.8). Non-manufacturing PMI rose to 49.5 (from 49.4): new orders fell (45.2 from 46.1) as did foreign demand (44.7 from 46.9).

- China’s RatingDog manufacturing PMI rose to 52.1 in Feb (Jan: 50.3), the most since Dec 2020, with increases in output (the most since Jun 2024) and new orders (rising for the ninth month in a row). Prices are surging: input cost inflation rose to its highest since June 2022 and output price inflation hit a 15-month high. Services PMI jumped to 56.7 in Feb (Jan: 52.3).

- China’s FDI fell by 5.7% yoy to CNY 92.01bn in Jan (Dec: -5%) despite newly established foreign enterprises rising 25.5% to 5,306 (i.e. volume of investments are down while number of projects are rising). Investment in high-tech industries inched up 0.6% yoy to CNY 33.75bn (or 36.7% of total inflows).

- Japan’s manufacturing PMI inched up to 53 in Feb (prelim: 52.8; Jan: 51.5), the most since May 2022, as output new orders and employment grew at the fastest pace since Jan 2022. Supported by demand from Europe and Asia, new exports expanded the most since Jun 2021.

- Unemployment rate in Japan ticked up to 2.7% in Jan (Dec: 2.6%), the highest since Jul 2024, as the number of unemployed grew by 60k to a 48-month high of 1.91mn. Jobs-to-applicants ratio slipped to 1.18 (from 1.2).

- Industrial production in India grew by 4.8% yoy in Jan (Dec: 8.0%), thanks to the 4.8% gain in manufacturing (Dec: 8.4%). Growth was also reported across manufacture of basic metals (13.2%), motor vehicles (10.9%) and machinery & equipment (6.2%).

- India’s current account deficit widened to USD 13.2bn or 1.3% of GDP in Oct-Dec (Jul-Sep: USD 12.3bn; Oct-Dec 2024: USD 11.3bn), as trade deficit widened (USD 93.6bn vs USD 79.3bn a year ago). Private transfer receipts increased to USD 36.9bn, thanks to remittances, from USD 31.5bn a year ago.

- India’s manufacturing PMI inched lower to 56.9 compared to the preliminary reading of 57.5 but stayed higher than Jan’s 55.4. Though new export orders grew at the slowest pace in 17 months partly due to the tariff uncertainty, new orders surged on domestic demand. Services PMI slipped to 58.1 in Feb (prelim: 58.4 and Jan: 58.5) as new order growth slowed to a 13-month low and input prices surged to a 2.5 year high.

- Singapore PMI ticked up to 50.6 in Feb (Jan: 50.5), the highest since Mar 2025, as output expanded. The electronics sector sub-index rose to 51.3 (Jan: 51.1) on higher output, new orders, exports and employment.

- Retail sales in Singapore declined 0.4% yoy in Jan, the lowest since Feb 2025, with drops across the board including in department stores (-12.3%) and supermarkets & hypermarkets (-9.7%). In monthly terms, sales rebounded, rising 6.1% mom versus Dec’s 2.7% drop.

Bottom line: As the war in the Middle East rages on, persistent disruption risks in Hormuz has seen an upward pressure on oil prices: prices jumped to as high as USD 119 a barrel on Monday (9th Mar). The G7 ministers are meeting later today to discuss the release of petroleum from strategic reserves, which might ease prices slightly. For now, the choice of Mojtaba Khamenei as the new supreme leader in Iran is unlikely to calm the situation given his hardline policy stance. In this backdrop, the prospect of a prolonged supply shock, with higher energy prices feeding into higher consumer prices, lessens the probability of a rate cut at the Fed’s next policy meeting.

Even as energy infrastructure is getting attacked in the GCC, more worrisome are news about desalination plants being targeted – about 70% of drinking water in Saudi Arabia comes from desalination and it stands at a high 90% in Kuwait (more in the Media section). Desalination is core, life-sustaining, strategic infrastructure. One of the immediate concerns in the region would be supply-side disruptions and logistical delays that could result in higher input prices; sectors such as tourism, retail and hospitality will be most affected until a diplomatic breakthrough occurs. It is possible that countries with land-based export alternatives or a route bypassing the Strait of Hormuz (e.g. Oman) could benefit during this period. We expect a surge in state-led support for resilience infrastructure (from strategic food silos to alternative export pipelines) in the GCC post-war, to ensure that the Hormuz choke point does not hold the regional economy hostage in the future. Furthermore, the GCC are likely to run larger budget deficits in coming years, given the increased security and defence spending during a period of lower oil revenues (given pauses in production).

Regional Developments

- The IMF warned that a prolonged conflict could lower regional GDP growth significantly, as uncertainty could stall long-term investment. Economies heavily dependent on tourism, logistics and capital inflows would be particularly exposed to prolonged instability, while higher oil prices may partially offset the shock for hydrocarbon exporters. Interestingly, S&P warned that GCC banks and credit channels may face strain if liquidity tightens and regional risk premia remain elevated while Fitch maintains that sovereign support and massive capital buffers provide a robust shield against immediate credit defaults (though any lasting damage to key energy infrastructure or protracted hostilities could pose risks).

- The shutdown of the Strait of Hormuz entered a critical phase following the escalation of naval hostilities, leaving tankers stranded for more than a week. The spill over into air cargo is now acute; with maritime routes blocked, demand for air freight has surged, yet capacity is constrained by the cancellation of over 1 million passenger seats. This has left high-value perishables and critical industrial parts (like aircraft components) stranded, threatening a secondary supply chain disruption in manufacturing sectors. In the near term, prolonged airspace restrictions could intensify supply chain delays and raise logistics costs across multiple industries.

- Bahrain, Iraq and Kuwait declared force majeure and announced oil output cuts after Qatar halted production of liquefied natural gas (LNG) and associated products. In contrast, Saudi Aramco could potentially keep oil flowing for up to 10 weeks even if the Strait of Hormuz is closed by leveraging its 745-mile East-West Pipeline (which, in theory, can carry up to 7mn barrels per day to the Red Sea; this level remains untested). The IEA estimated that Aramco was sending only 2mn barrels via this at start-2026, less than a third of its total capacity. The UAE also has an alternative option in Fujairah (spare capacity: 700k bpd).

- The UAE and wider GCC hospitality sectors are facing a demand vacuum as travel advisories and airspace restrictions have disrupted both leisure and business travel. The impact is not just lost revenue, but also potential for layoffs as service-sector growth slows. Furthermore, an incident at an Amazon Web Services data centre has raised concerns over the physical and cyber security of regional data centres – prompting discussions around redundancy, cybersecurity protocols and geographic diversification of cloud infrastructure.

- Slower economic activity, potential tourism declines and rising borrowing costs could challenge Bahrain’s fiscal standing, especially in the backdrop of the fiscal package approved in Dec (electricity and water rate hikes, corporate taxes). However, Aluminium Bahrain (Alba) ’s agreement to acquire Europe’s largest aluminum smelter underscores a strategic move to secure downstream market access and diversify its industrial footprint away from the GCC. Such M&A strategy may become a blueprint for other regional firms looking to hedge against local disruption, diversify revenues and integrate more deeply into global manufacturing supply chains.

- Egypt’s Minister of Petroleum and Mineral Resources assertion that the Strait of Hormuz closure poses no threat to Egypt’s energy supplies highlights the country’s diversified supply sources and domestic production capacity. While it will cushion short-term shocks, any sustained global supply disruptions could still raise import costs and fiscal pressures.

- Egypt PMI declined to 48.9 in Feb (Jan: 49.8), reflecting lower output and new orders. Firms cited softening domestic conditions and elevated input cost pressures (given higher wage costs and prices for oil & metals) while employment fell for the third month in a row.

- Egypt decided to adopt a flexible exchange rate system as part of its reform agenda, emphasising that the policy will remain market-driven despite regional geopolitical uncertainty. Exchange-rate flexibility should strengthen investor confidence in the medium-term and improve the economy’s ability to adjust to external volatility.

- According to the PM, GDP growth in Egypt touched 5.3% yoy in Q2 of the current financial year, the highest since Q3 FY 2021-22, reflecting improving economic activity. The government also announced an EGP 40bn social support package to ease cost-of-living pressures – aimed at supporting vulnerable households through wage adjustments and targeted subsidies. The government also plans to introduce a new minimum wage by end-Mar (along with the state budget) as part of broader measures aimed at offsetting rising living costs.

- Net foreign assets in Egypt rose to a record USD 29.5bn in Jan 2025, reflecting improved foreign currency inflows (supported by GCC investments and strong remittances among others) and strengthened external buffers.

- The USD 8bn investment from 200 French firms underscores Egypt’s growing appeal as a near-shore manufacturing hub for Europe across sectors including manufacturing, infrastructure, retail and energy. Given recent legislative and regulatory reforms, investors are viewing Egypt as a stable and strategic regional manufacturing and export hub.

- Reuters reported that oil production from Iraq’s main southern oilfields fell by 70% to 1.3mn barrels per day given the Strait of Hormuz blockade due to the Iran war (pre-war, production stood at 4.3mn bpd). Furthermore, crude storage had reached maximum capacity, according to an official with the state-run Basra Oil Company.

- Kuwait’s decision to cut oil production is a pragmatic response to the reality of “shut-in” risk. With storage capacity reaching its limits and no safe passage through the Strait, Kuwait Petroleum Corporation (KPC) declared force majeure.

- Kuwait’s non-oil sector PMI stood at a 15-month high of 54.5 in Feb (Jan: 53.0), driven by strong domestic demand; output and new orders rose at the fastest pace in 10- and 15-month high respectively alongside moderate employment gains. Despite persistent cost pressures (input costs at a 9-month high), forward-looking business sentiment rose to a 26-month high.

- Lebanon PMI increased by 1.1-points to 51.2 in Feb (and pre the ongoing war), the seventh consecutive month of expansion, with driven by rising new orders and stronger output amid inflationary pressures (from hikes in petrol and VAT). The 12-month outlook index ticked up to a 6-month high, though remaining in contraction.

- Oman’s positioning on the Arabian Sea has fundamentally changed its risk profile in 2026. Ratings agencies have highlighted that Oman is significantly less exposed to a Hormuz blockage compared to its GCC peers. With major ports like Salalah and Duqm sitting outside the chokepoint, Oman has emerged as a key evacuation and logistics hub, facilitating the movement of people and high-value cargo away from the primary conflict zones.

- Oman’s first listed mutual fund raised USD 70mn on the Muscat Stock Exchange, signalling domestic investors appetite for institutional-grade vehicles to stay invested in the country – also representing a step toward deepening financial markets.

- FT reported the warning fromQatar’s Energy Minister that Gulf exports could stop within weeks given disruptions around the Strait of Hormuz, underscoring the fragility of the entire regional energy complex. Qatar, producing an equivalent of roughly 20% of global LNG, has already suspended LNG production following attacks on energy infrastructure. The minister also forecast that crude prices could hit USD 150 a barrel in two to three weeks and gas prices could rise to USD 40 per million Btu if the Strait remains closed.

- Qatar’s PMI inched up to 50.6 in Feb (Jan: 50.4), though remaining below the long-run average of 52.1 (since 2017). The rate of job creation remained strong in Feb, ticking up from Jan’s nine-month low, while both output and new orders fell further. Input prices rose the most since Dec 2024 while selling prices rose for the first time in five months.

Saudi Arabia Focus

- Saudi Arabia PMI eased to 56.1 in Feb (Jan: 56.3), the softest improvement in nine months. Notably, output and new orders remained robust, supported by strong domestic demand and ongoing project approvals. Firms also reported a 4-month high rate of employment growth (among the strongest in the series) rising wage pressures and record input costs (highest since the survey began in August 2009), reflecting tight labour market conditions and capacity expansion.

- Point-of-Sale (POS) transactions in Saudi Arabia grew by 4.5% weekly to SAR 14.5bn in the week ending Feb 28th, despite a slight drop in the number of transactions (-4.6%). Spending gains was strongest in sectors such as apparel (44.2% to SAR 1.9mn) and jewelry (40.9% to SAR 510k). Though food and beverage purchases fell 11.4% week-on-week to 2.3mn, it still accounted for the largest share of total spending.

- Saudi Arabia is well-placed to facilitate a strategic shift of trade volumes from the Gulf-facing ports to Jeddah Islamic Port on the Red Sea to bypass the Strait of Hormuz if required, according to various experts. By utilizing land routes to move goods across countries, Saudi could effectively de-risk its supply chain, albeit at a higher short-term logistical cost.

- Ma’aden’s net profit more than doubling in 2025 underscores the success of the mining sector. Revenue surged 19% yoy to SAR 39bn, benefitting from higher commodity prices and stronger production capacity in phosphate, aluminium and gold. The state-owned mining company continues to pursue large-scale investment in new mining projects and exploration as Saudi Arabia seeks to expand its minerals sector.

- Despite the robust long-term fundamentals of Saudi Arabia (infrastructure, regulatory reform, market size), the immediate geopolitical risk may slow capital commitments and FDI inflows as global investors opt for a “wait-and-watch” atmosphere. Investor sentiment remains sensitive to regional security dynamics, particularly when geopolitical tensions threaten logistics routes, energy infrastructure or market stability.

UAE Focus

- Non-oil sector PMI in the UAE rose to a 12-month high of 55.0 in Feb (Jan: 54.9), thanks to a surge in domestic new orders, sustained demand across construction, real estate, logistics and technology alongside a notable uptick in business confidence. Input costs are on the rise, driven by wage adjustments and increases in material costs while output prices have risen at a modest rate as firms are opting to absorb costs to maintain market share.

- UAE’s minister of economy and tourism confirmed strategic reserves of essential goods sufficient for roughly four to six months of domestic demand, reflecting its strong macro-prudential contingency planning. While imports of fresh & essential food items continue via commercial and charter flights, despite regional tensions, this six-month buffer will help prevent panic-buying and unnecessary price hikes.

- UAE announced the successful conclusion of a Comprehensive Economic Partnership Agreement (CEPA) with Japan: bilateral non-oil trade grew 16.7% yoy to USD 20.3bn in 2025, with UAE accounting for about 39% of Japan’s trade with Arab and African nations. The agreement moves beyond oil, toward high-value technology and energy-transition corridors.

- The UAE Central Bank governor affirmed that the banking sector is well-positioned – backed by the AED 5.42trn asset base and high capital adequacy ratios – and has “a high level of preparedness to respond effectively to regional developments”. Strong regulatory oversight, solid capital buffers, financial sector diversification and healthy asset quality underpin financial stability. The governor’s focus on navigating “regional developments” suggests that while liquidity is ample, the CB UAE is maintaining a rigorous stress-testing regime to ensure that any potential localized credit defaults do not become systemic.

- ADNOC stated that its operations are continuing, by managing its offshore output and storage facilities while maintaining steady onshore operations during the conflict. This operational flexibility will ensure that the UAE remains a reliable energy supplier to its long-term contract holders in Asia, particularly Japan and South Korea.

Media Review:

Iran war will leave a complex geoeconomic legacy

https://www.ft.com/content/d2b243b8-0a36-4f48-b431-53101bea9699

The Oil Pipelines That Could Decide the Iran War

Desalination Plants: Gulf water security in focus

The Iran war puts Asia in an energy panic

https://www.economist.com/finance-and-economics/2026/03/08/the-iran-war-puts-asia-in-an-energy-panic

From 1776 to 2026: Adam Smith’s lessons for the global economy

Powered by:

![]()